EMERGENCY! THE FEDERAL GOVERNMENT IS RUNNING SHORT OF DOLLARS!

Who wants you to believe that nonsense? The rich, of course. They want to widen the income/wealth/power Gap between them and you — and REASON is happy to oblige.

They say the so-called “national debt” will be “more expensive.”

The definition of “more expensive” is: An entity having infinite dollars (the U.S. governement) will pump more stimulus dollars into the private sector (aka “the economy’), thus not only helping the private sector grow, but also accomplishing many important economic tasks.

That’s what REASON means by “more expensive.”

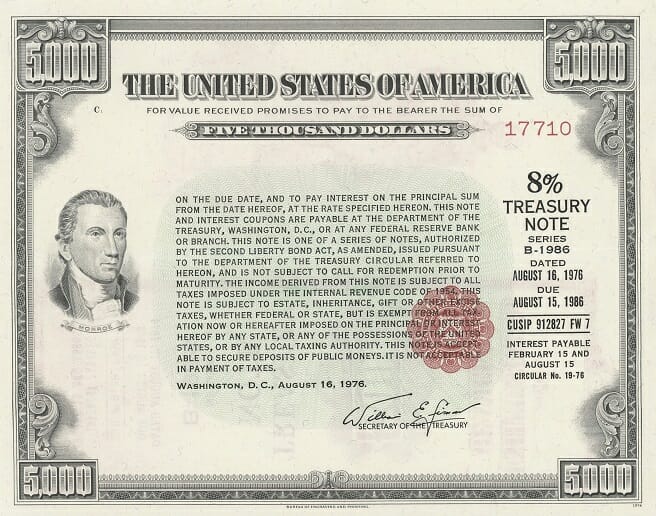

The U.S. government can’t run short of these, or these,or these.

The Treasury bond, the dollar bill and the Treasury check all are titles to dollars. Just as a car title is not a car, and a house title is not a house, the above three titles are not dollars. They merely represent dollars, which have no physical existence.

The so-called “national debt” refers to the total of dollars deposited from non-federal sources into T-security (T-bills, T-notes, T-bonds) accounts.

They are not debts of the federal government, which neither needs, uses, nor even touches the dollar in those accounts, except to return them upon maturity. Unlike real debts, the “national debt” is not a financial burden on the federal government or on taxpayers.

The sole purposes of the “national debt” are to provide a safe parking place for unused dollars (thus helping to stabilize the dollar), and to help the Federal Reserve control interest rates (by setting a base rate).

Recent comments from Federal Reserve Chair Jerome Powell hinted that the Fed may soon get serious about hitting the monetary brakes to slow the economy.

Until recently, inflation was described as transitory. But at some point, that story has to change.

For REASON, economic growth is bad, so the economy must be “slowed.” Actually, for REASON, government and all government spending are bad, and there is no acceptable level of either.

Price levels likely will rise into 2022. The all-item consumer price index (CPI) was up more than 5 percent on a year-over-year basis for July, August, and September. The increase for October was 6.2 percent—the largest jump since 1990.

The Fed considers 2 percent inflation to be its goal. Obviously, there is a large gap between that and what we are seeing.

The inflation rate is reflected in interest rates that borrowers must pay, especially for longer-term debt. Lenders hope to be paid back with at least as much purchasing power.

If they believe inflation will tick away at 4 percent, interest rates will tend to rise. Higher interest rates mean higher interest costs on all forms of public and private debt.

As a result, mortgage rates will rise, all forms of construction will suffer, and businesses will postpone making large investments in plants and equipment.

REASON, which wants the economy to “hit the brakes,” suddenly becomes conserned about construction, and businesses investing in plants and equipment, thus criticizing both sides of the same stimulus question.

Now consider the public debt—especially the federal debt, which ballooned as a result of large budget deficits in recent years. (In 2020, the federal government raised $3.4 trillion in revenue and spent $6.6 trillion.)

Translation: The federal government pumped $3.2 trillion net growth dollars into the economy, and you should be shocked.

The interest cost of the national debt was $253 billion in 2008, equivalent to $325 billion in 2021 dollars; it remained around that level through 2015.

Even though the debt doubled in those years, sharply falling interest rates and low inflation helped contain costs.

But that was yesterday. With today’s higher inflation and rising interest rates (perhaps with more to come), the Congressional Budget Office (CBO) estimates that the interest cost of public debt is $413 billion in 2021, stated in current dollars.

Obviously, any dollar spent on interest cannot be spent on government benefits or services.

REASON, demonstrates its ignorance about federal financing, by implying that if the government spends dollars on interest it doesn’t have enough dollars to spend on benefits or services (which REASON hates, anyway).

Of course, if REASON had evan an ounce of knowledge about federal financing, they would admit that the federal government has infinite dollars to spend, so interest payments do not in any way preclude other spending.

Looking ahead, the CBO expects more of the same. For 2026, it projects that the interest rate on 10-year Treasury bonds, currently 1.5 percent, will be 2.6 percent, and that the interest cost of the federal debt will rise to $524 billion.

For 2030, the projections are 2.8 percent and $829 billion, respectively, all stated in current dollars for the noted years.

In other words, the federal government will pump $524 billionand $829 billion interest into the economy in 2030.

Now we are talking about real money. To put $829 billion into perspective, in 2020 the United States spent $714 billion on the military, $769 billion on Medicare, and $914 billion on all nondefense discretionary spending, all stated in 2020 dollars.

Back-of-the-envelope calculations strongly suggest that some spending categories will have to give.

The above-mentioned “back-of-the-envelope calculations neglect to mention that the federal deficit spending is not constrained by lack of dollars. It is infinite.

Finally, we come to the heart of the issue.

The United States is experiencing an inflationary surge caused fundamentally by the injection into the economy of trillions of dollars—stimulus and other spending—without an accompanying rise in production of goods and services that might be purchased with the new dollars. It’s rising demand plus troubled supply.

All inflations are scarcity-based. None are spending-based. Increased deficit spending to cure shortages would end the inflation.

The government has been spending massively for many years, without the long-feared inflat

These forces will be with us until the stimulus dollars work their way through the economy and the federal government stops printing more money.

When the federal government stops “printing” (technically the wrong term) money we will have a recession, just as we always do when money creation stops.

Reductions in federal “debt” growth (blue line) cause receissions (gray vertical bars) which are cured by increases in federal “debt” growth.

As the process continues, our government—the source of inflation in the first place—will face hard choices when paying for past and future deficits and rising debt.

The federal government pays for all its spending, promptly. Yet, the so-called federal debt is composed of T-securities that are as much as 30 years old. They pay for nothing.

All federal obligations are paid for immediately. The government faces no “hard choices” when paying its debts. It has the infinite ability to create dollars.

The federal government cannot unintentionally run short of dollars.

The so-called “debt is about $25 trillion. The U.S. government does not owe anyone or any thing $25 trillion.

The government could pay off the $25 trillion of T-securities today simply by returning the $25 trillion dollars already deposited into T-security accounts. No burden on the government. No tax dollars involved. No taxpayers burdened.

BRUCE YANDLE is a distinguished adjunct fellow with the Mercatus Center at George Mason University, dean emeritus of the Clemson College of Business and Behavioral Sciences, and a former executive director of the Federal Trade Commission.

This does not speak kindly of the Mercatus Center and GME or of the FTC, who seem to be devoid of information about federal financing.

Per Wikipedia: “The Mercatus Center at George Mason University is a libertarian non-profit free-market-oriented[2][3] research, education, and outreach think tank founded by Koch Industries executives and directed by Tyler Cowen…. The Koch family has been a major financial supporter of the organization since the mid-1980s.[6][7] Charles Koch serves on the group’s board of directors.[8][6]”

The only thing this so called “think tank” thinks about is how to deceive policy makers (and media) into widening the gap at the behest of their primary benefactor, Charles Koch.

Right. Calling it “debt” is intentionally misleading. It actually is: “Deposits In T-Security Accounts.”

27,9% is owned by private individuals and entities in the U.S.

30.9% is owned by outsiders

Then if the total “debt” is claimed to be say, $25 trillion, the correct headline would be “Net of $14.7 Trillion Is DEPOSITED In T-Security Accounts.” (58.8% X 25)

Suddenly, that doesn’t sound so scary.

And of course, when those $14.7 trillion deposits reach maturity, the federal government returns the dollars that already reside in the accounts. It’s a simple transfer of existing dollars from one account to another. No burden on anyone.

Tell that to your Congressperson and ask him/her, “What’s all the shouting about?”

These gifts are no different from the federal taxes we pay, other than being voluntary rather than mandated. Despite what the public is being told, these gifts do not reduce the amount the public deposits into T-security accounts. Nor do they reduce the amount China deposits into its T-security accounts at the Fed.

If you or China decide to buy a T-bond, someone’s gift to the government will not affect your or China’s decision.

Happy New Year Rodger! Just wanted to thank you for your posts, including this one, so “Thanks!

LikeLike

🙂

LikeLike

Per Wikipedia: “The Mercatus Center at George Mason University is a libertarian non-profit free-market-oriented[2][3] research, education, and outreach think tank founded by Koch Industries executives and directed by Tyler Cowen…. The Koch family has been a major financial supporter of the organization since the mid-1980s.[6][7] Charles Koch serves on the group’s board of directors.[8][6]”

The only thing this so called “think tank” thinks about is how to deceive policy makers (and media) into widening the gap at the behest of their primary benefactor, Charles Koch.

LikeLike

Amen

LikeLike

Funny they aren’t putting their own money where their mounth is by advocating a mass movement of ‘gifts’ to pay down the scary ‘debt’ sooner: https://fiscal.treasury.gov/public/gifts-to-government.html https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

LikeLike

Right. Calling it “debt” is intentionally misleading. It actually is: “Deposits In T-Security Accounts.”

27,9% is owned by private individuals and entities in the U.S.

30.9% is owned by outsiders

Then if the total “debt” is claimed to be say, $25 trillion, the correct headline would be “Net of $14.7 Trillion Is DEPOSITED In T-Security Accounts.” (58.8% X 25)

Suddenly, that doesn’t sound so scary.

And of course, when those $14.7 trillion deposits reach maturity, the federal government returns the dollars that already reside in the accounts. It’s a simple transfer of existing dollars from one account to another. No burden on anyone.

Tell that to your Congressperson and ask him/her, “What’s all the shouting about?”

LikeLike

What would RMM like to ask the givers of these “gifts” that were deleted out of existence upon receipt: https://www.treasurydirect.gov/govt/reports/pd/gift/gift.htm

My Senator Ron Johnson would likely say something about the ‘deep state’ and secret societies within the FBI.

LikeLike

These gifts are no different from the federal taxes we pay, other than being voluntary rather than mandated. Despite what the public is being told, these gifts do not reduce the amount the public deposits into T-security accounts. Nor do they reduce the amount China deposits into its T-security accounts at the Fed.

If you or China decide to buy a T-bond, someone’s gift to the government will not affect your or China’s decision.

LikeLike