I often listen to the public radio show, “Freakonomics Radio” by Stephen J. Dubner. Today, the story was about insurance and how intractable it is, both from the insurance providers’ and the buyers’ perspectives.

We all have some forms of insurance: Life, health, accident, liability, home, personal property, unemployment, retirement, and many others.

Lloyds of London has a reputation for creating individualized policies to insure anything: An actress’s legs, a quarterback’s arm, a pianist’s fingers.

Among the several insurance problems, the fundamental problem is adverse selection. The insurance company wants to cover people who will not have an immediate claim. The buyer wants to get his money’s worth in claims.

A life insurance seller wants young, healthy customers who will not make claims for many years while paying premiums all those years.

All insurers want the insured to buy as soon as possible, then wait a long time before making a claim (for instance, a health policy) or never make a claim (an auto liability policy),

But the insured ideally would like to purchase his insurance as late as possible — just before making a claim — or never.

To minimize adverse selection, insurers hire actuaries. These people use research and probability formulas to determine the likelihood of a person making a claim and how significant that claim is might be.

This leads to another problem: Adverse denial. Suppose those who will make the fewest and most minor claims are the only people accepted, and all others are denied. In that case, many people will be denied insurance, and the basic premise of insurance — to protect against misfortune — would be lost.

For example, on average, black people get sick and die sooner than white people. If the law allowed, insurance companies would charge blacks higher premiums than whites or refuse insurance to blacks altogether.

However, the law does not allow this, so the premiums charged to white people must be higher than they ordinarily would be to make up the difference.

Any time an insurer accepts something other than the lowest possible risk, the lowest risk people must pay more. Some, but not all, of this can be baked into the premiums. For example, most life insurance policies consider age and prior illness when determining premiums. But no insurer can consider every possible risk category and remain competitive.

So, in general, the lowest-risk people do, in part, fund higher-risk people for all sorts of insurance.

That said, a substantial portion of our population is not financially protected by insurance, either because no company will insure them or because the premium is higher than what people wish to pay.

In short, the risk is too high for any potential insurer, and the premium is too high for potential insureds.

The fact that the problem is considered intractable puzzles me because we already have solved it, not just once, but many times.

Medicare, for instance, solves it for the worst health risks: Older people who already are sick with terminal illnesses cannot be refused when they reach the qualifying age.

More than 18 percent of Americans depend on Medicare for their health coverage, and in 2019 Medicare the enrollment reached over 60 million.

You can start receiving Medicare Part A (hospital insurance) benefits with no premium once you are 65 or older if you or your spouse worked and paid Medicare taxes for a certain period. You can know you are eligible for premium-free Medicare A if one of the following applies to you:

You currently receive or are eligible for Social Security.You currently receive or are eligible for Railroad Retirement Board (RRB) benefits.You or your spouse served in a Medicare-covered government job.

You can purchase Medicare Part B benefits if you are eligible for Medicare Part A. It is a voluntary program that requires you to pay monthly premiums. For 2022, the standard premium is $170.10 (or higher, depending on income).

No matter how sick you are, even on death’s doorstep, you can receive insurance if you meet the above requirements.

How does the government avoid adverse selection? Mostly, it doesn’t. Yes, there are qualifications; adverse selection is not the consideration.

Why can the government afford Medicare when private insurance companies must worry about adverse selection? Contrary to popular belief, people with FICA deducted from their salaries do not fund Medicare.

The federal government, being Monetarily Sovereign, has the infinite ability to create U.S. dollars.

It neither needs nor uses tax dollars to pay for anything. Even if total FICA collections equaled $0, the federal government still has the infinite power to fund something better than our current Medicare.

The government could fund a comprehensive, no-deductible Medicare for every man, woman, and child in America.

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes:Scott Pelley: Is that tax money that the Fed is spending?Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

And that is the solution to the healthcare insurance problem. The federal government should “use the computer to mark up the size of the account” and fund a form of Medicare far better than current Medicare.

I have Medicare, but I also pay for a concierge primary care doctor. I pay her an annual fee in addition to what she receives from Medicare.

My previous primary care doctor, who received Medicare reimbursement, had about 2,500 patients. My concierge doctor self-limits to about 600 patients. This allows her more time to do precisely what she studied for years to do: Treat patients.

She spends time studying my particular needs and discussing my health with me. If I go into the hospital, she has admittance privileges and can oversee my treatment there while discussing my case with all the doctors and nurses.

The federal government has sufficient resources to pay every primary care doctor to be a concierge doctor who can spend the time each patient deserves.

(The federal government also has the resources to provide free medical schooling for all prospective doctors, so there would be plenty of people available to be the abovementioned concierge doctors.)

All drivers need auto liability insurance. The federal government should provide it free. All homeowners and renters need insurance. The federal government should provide it.

There is no logical reason why more affluent people can afford insurance while poorer people cannot. Ironically, it is the poorer who need insurance more than, the richer.

The Freakonomics radio show ignored the fundamental truths about the American economy:

The solution to many of life’s problems stares us in the face, yet disinformation from the top prevents it.

No, federal financing is not the dreaded “socialism” (which is government ownership and direction, not just government funding.)

And no, federal spending does not cause inflation. On the contrary, federal spending can reduce inflation by acquiring goods and services, the scarcity of which is the real cause of inflation.

There is a solution. We need only to recognize it.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

I continually am puzzled by the misunderstanding (“disunderstanding”?) of Monetary Sovereignty. It is both simple and obvious, yet many (most?) people have trouble comprehending it.

MS is based on just four simple facts:

In the 1780s, the U.S. federal government created the laws that created the U.S. dollar from thin air — as many dollars as it wished – and gave them the value it wished.

The government’s own laws give it the power to continue creating dollars, infinitely

The government’s own laws give it the power to continue changingthe valueof the dollar — a power it has used many times.

The government can change its laws at will.

Really, what could be simpler, more obvious, and less controversial?

Derived from these simple, obvious facts comes the following:

The U.S. federal government never unintentionally can run short of U.S. dollars.

No agency of the government can run short of dollars unless the government wishes it.

Federal taxes are not used or needed to fund federal spending.

By changing the value of the dollar, the government has absolute control over inflation

And that’s it. Monetary Sovereignty.

Intuition is powerful. Many of us prefer to believe our intuition than believe facts.

Interestingly, where fiction parallels facts, you might not believe the facts about the fiction, while still believing fiction about the facts.

That is, you might read a historical novel of fiction, and not believe the background facts presented. Yet, you might be fooled by a conspiracy theory website presenting fiction as fact.

So here is the explanation that may appeal to intuition as well as to facts.

You probably have played the hugely popular board game, Monopolytm. As a game, it’s fiction, but you believe and understand the facts (i.e. “rules.’)

Here are some of the facts.

The game is played with multiple players plus a Bank. The Bank pays Monopoly dollars to the players for various benefits.The Bank collects taxes, fines, loans and interest from the players.The Bank “never goes broke.” If the Bank needs money, it may issue as many dollars as needed by printing on scraps of paper or simply by creating a bookkeeping tally.

Example of a Monopoly running tally

A sample tally is demonstrated by the illustration at the right.

It reveals three things:

I. Monopoly money is not physical. Those printed $500, $100, $50, $20 $10 $5, and $1 bills aren’t dollars in of themselves.They merely representdollars, just as the numbers on a tally represent dollars.II. The Bank can createan infinite supply of Monopoly dollars.

If needed, the Bank instantly could pay Tom, Dick, Harry, or Bob $1, or $100, or $1,000,000,000 in Monopoly dollars.

In the tally, there is no need to create a column for the Monopoly Bank.

This lack of a column demonstrates the Bank’s ownership of infinite dollars.

It also demonstrates that all dollars sent to the Monopoly Bank are destroyed upon receipt.

If Tom, for instance, sent $100 to the Bank, his $4,400 would be reduced to $4,300. So, what happened to the $100 Tom paid? They simply disappeared. They no longer exist.

Although the Bank can create infinite dollars this creation process does not create Monopoly Bank “debt.” The Monopoly Bank does not borrow dollars nor does it owe any dollars.

Thus, taxes are not levied to “pay off” any Monopoly Bank debt.

By rule, the Monopoly Bank simply creates all the dollars it needs. Although the Bank is not precluded from keeping track of the dollars it receives from players, that record would not indicate how many dollars the Monopoly Bank “owes” or has.

There is no ongoing debt owed by the Monopoly Bank.

All of the above is easily understood by you and by virtually anyone else who has played the game.

Now, in the above paragraphs, substitute the words, “U.S. federal government” for the word “Bank.” And substitute “members of the public” for “players.”

The facts remain essentially the same.

There are multiple members of the public plus the federal government.

The federal government pays dollars to the public for various benefits.

The federal government collects taxes, fines, loans, and interest from the public.

The federal government “never goes broke.” If the federal government needs money, the government may issue as much as needed by printing on paper or simply by creating a bookkeeping tally.

[Former Fed Chairman, Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”]

Continue reading and substituting until you come to the part that some people have difficulty understanding:

The federal government does not borrow dollars nor does it owe any dollars. Taxes are not levied to “pay off” any federal government debt.

[Quote from Ben Bernanke when, as Fed chief, he was on 60 Minutes:

Scott Pelley: Is that tax money that the Fed is spending?

Former Fed Chair, Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.]

The Monopoly Bank and the U.S. federal government both are Monetarily Sovereign. They both are issuers of their dollars. Neither of them can run short of dollars.

Both the Monopoly Bank and the U.S federal government have infinite dollars.

[Former Fed Chair, Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”]

Neither the Monopoly Bank nor the federal government borrows or taxes in order to pay their financial obligations. Spending by the Monopoly Bank or the U.S. federal government does not create future taxpayer obligations.

For that reason, Social Security, an agency of the federal government, cannot run short of dollars, unless that is what the government wants. Even if there were no FICA tax (which contrary to popular myth, does not fund Social Security), that agency need not run short of dollars.

The “debt clock.” You have no share.

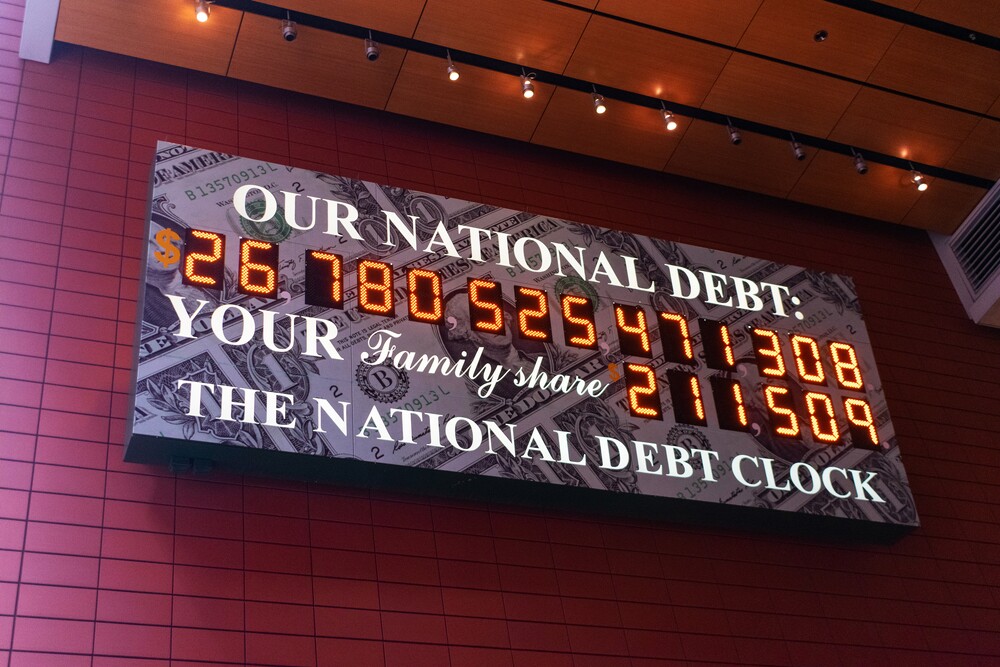

Medicare for All, college for all, upgraded infrastructure, good housing for all — every imaginable federal benefit — all are easily affordable. The so-called federal debt is not a burden on future taxpayers or on the government.

The famous “debt clock” implies the lie that somehow the federal “debt” is a danger to you, your children, and the federal government.

It is not a debt, and it is not a danger, to you or anyone.

It is just simple deposits by the public into accounts.

The parallels between the Monopoly game and federal financing are stunning.

Yet, though people tend to understand the rules of Monopoly, too many become hopelessly confused by the same set of facts when applied to real life.

Yes, one is fiction and the other is fact, but that difference is not the source of the confusion.

The confusion is caused by the longtime, ongoing, relentless dissemination of false information about the federal government’s finances and by the misnaming of T-securities as “borrowing” and “debt.” They are neither.

The misinformation is promulgated by agents for the rich, who want to prevent you from asking for the benefits the rich already receive: Retirement benefits, medical care, good housing, safe neighborhoods, college education, spending money for a good life.

Neither the government nor you owes the deposits that sit in T-security accounts. These accounts resemble bank safe deposit boxes, which the bank “pays off” simply by returning the contents. No “debt” or tax liability there.

The Monopoly board game is a good analog for the federal finance system. If you understand one, you should understand the other.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

THE SOLE PURPOSE OF GOVERNMENT IS TO IMPROVE AND PROTECT THE LIVES OF THE PEOPLE.

Gap Psychology describes the common desire to distance oneself from those “below” in any socio-economic ranking, and to come nearer those “above.” The socio-economic distance is referred to as “The Gap.”

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.Implementation of Monetary Sovereignty and The Ten Steps To Prosperity can grow the economy and narrow the Gaps:

Ten Steps To Prosperity:

Here are some of the facts.

Here are some of the facts.