The purpose of any government is to protect and improve the lives of the people. However, when proposals are made to achieve these goals, we are often met with two main objections:

- The government can’t afford it, and

- It will cause inflation.

The “can’t afford it” objection often leads to name-calling, such as “socialism,” “communism,” and “anti-capitalism.” This name-calling serves as a substitute for genuine thought. Labeling something doesn’t prove whether it’s good or bad.

It just demonstrates that the name-caller doesn’t want to discuss facts and believes the name alone is sufficient.

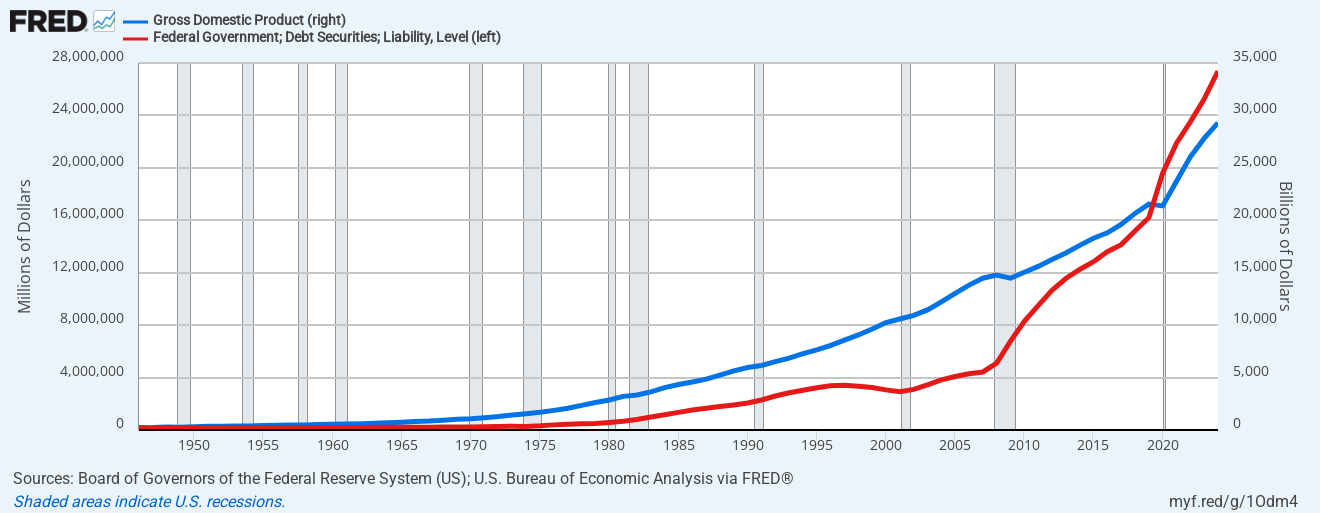

Some individuals who prefer not to engage in name-calling yet are concerned about federal budgets can be persuaded by the facts surrounding Monetary Sovereignty. This concept highlights that the federal government can create an unlimited amount of dollars instantly and spend them in any manner it chooses.

These individuals recognize that the federal government differs from state and local governments, which are not monetarily sovereign. Federal deficits and debt do not limit its spending capacity. Economic growth requires federal deficits, as they inject growth dollars into the economy.

Insufficient federal deficit spending has caused every recession and depression in U.S. history.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

There are several programs that a government, having infinite money, easily can afford. Among them are:

- End FICA

- Comprehensive, no-deductible, free Medicare for every American, regardless of age and medical history

- Social Security for every American

- Free college for all Americans who want it.

- Housing subsidies for all

- Food subsidies for all

Though such programs would cost trillions, the federal government can create trillions simply by voting and then pressing computer keys.

Once debt worriers see that the government can’t run out of dollars and that deficit spending is necessary to fulfill the federal government’s obligations of “protect and improve,” they resort to their final objection: “But it would cause inflation.”

Does Federal Deficit Spending Cause Inflation?

There are no major historical inflations that were primarily caused by a Monetarily Sovereign government spending “too much.”

Every severe inflation episode traces back to real shortages, production collapses, or exchange-rate breakdowns, not to government deficits.

Here are some of the major inflations people think were caused by excessive spending — and why that belief is wrong:

1. Weimar Germany (1921–1923): Popular myth: runaway printing caused inflation.

Reality: Germany lost its industrial Ruhr region during the French occupation. This led to a massive drop in coal and steel output. Reparations required payment in foreign currency. The government was forced to buy foreign currency at any price. Workers were paid NOT to work during Ruhr resistance. Production collapsed.

Cause: Severe loss of real output + currency collapse, not spending.

2. Zimbabwe (2000s): Popular myth: reckless printing for government spending.

Reality: Mugabe’s land reforms destroyed commercial farming, which resulted in a 40%–60% drop in agricultural output. Corn and tobacco production collapsed. Drought worsened food supply.

Cause: Food shortage.

3. Hungary (1945–46): Worst hyperinflation ever/ Popular myth: runaway spending after WWII.

Reality: Production collapsed from war damage. Transportation, factories, and agriculture all were destroyed. Occupying Soviet forces extracted resources.

Cause: War-induced physical destruction and confiscation of supplies, causing massive shortages.

4. United States (1970s): Popular myth: The government spent too much during Vietnam and the Great Society.

Reality: The OPEC oil embargo in 1973 and the second oil shock in 1979. Oil prices quadrupled, which led to cost increases everywhere. Inflation tracked energy prices almost perfectly.

Cause: Energy shortage.

5. Post-COVID Inflation (2021–2022): Popular Myth: Stimulus checks “overheated” the economy.

Reality: Factory shutdowns caused durable goods shortages. Global shipping breakdown caused container-related shortages. Semiconductor shortages led to car and truck shortages. Energy price spikes. Labor shortages.

Cause: Widespread shortages of virtually all supplies and means of production.

6. Latin American inflations: Argentina, Brazil (various decades) Popular myth: Populist spending,

Reality: Debt denominated in foreign currency. Currency crises make imports unaffordable. Prices rise because supply shrinks.

Cause: Currency crisis leads to supply failures.

7. Confederate States of America (Civil War): Popular myth: Currency printing.

Reality: Massive destruction of productive capacity. The Union blockade cut off imports. Farms and railroads were destroyed.

Cause: War shortages

Conclusion: There is no major historical example where government spending caused inflation. Every well-studied inflation is rooted in: Energy shortages, food shortages, and the loss of production capacity,

8. Yugoslavia, 1992–1994: Popular myth: Excessive government spending.

Reality: Civil war shortages: Slovenia had only ~8% of Yugoslavia’s population but produced about 20%+ of total GDP and an even larger share of high-value industrial output. Lost production capacity of electronics, electrical machinery, pharmaceuticals, metals and machinery. UN santions caused loss of imports (fuel, food, medicines). Breakup of supply chains between republics.

Cause: War shortages, sanctions, economic isolation.

SUMMARY

A Monetarily Sovereign government cannot unintentionally run short of its sovereign currency. It can pay for anything denominated in its currency, provided that currency is accepted by the populace.

Inflation is not caused by “too much money chasing too few goods.” Instead, it results from a scarcity of essential goods, particularly energy and food.

Typically, inflation is caused by:

- War shortages

- Oil producer price gouging

- Pandemic shortages of labor, goods, and services.

- Weather that affects food production

- Government mismanagement of supply sources.

- Shipping interference

- Monetary non-sovereignty causing a money shortage

No high inflation in world history was driven primarily by deficits in a Monetary Sovereign nation. The mechanism is always real resource scarcity, not the nominal size of the money supply.

HYPERINFLATION

Hyperinflation is a very rapid general increase in the prices of goods and services, exceeding 50% per month. Prices increase when goods and services are in short supply.

Here is a brief background on hyperinflations since 1900:

War & Occupation

Germany (1921–1923) –Sortages of coal and industrial output collapsed after the Ruhr occupation; food imports were scarce.

Hungary (1945–1946) – Post-WWII destruction left food and housing in extreme shortage.

Greece (1941–1946) – Axis occupation caused famine; food and fuel were critically short.

China (1948–1949) – Civil war disrupted grain supply and transport; rice shortages drove inflation.

Philippines (1942–1944) – Japanese occupation currency collapsed as rice and basic goods disappeared.

State Collapse & Civil War

Yugoslavia (1992–1994) – Sanctions and war cut off oil and food imports; shortages everywhere.

Zimbabwe (2007–2009) – Land seizures destroyed agriculture; maize and wheat shortages were central.

Congo/Zaire (1991–1996) – Civil war disrupted mining and food supply; fuel shortages were common.

Angola (1991–1999) – Civil war devastated agriculture; food and fuel were scarce.

Mozambique (1980s–1990s) – Civil war destroyed farming; food shortages drove inflation.

Nicaragua (1987–1991) – War and sanctions cut off imports; food and fuel shortages.

Commodity & External Shocks

Bolivia (1984–1986) – The Collapse of tin exports led to a foreign exchange shortage; imported fuel and food became unaffordable.

Peru (1988–1990) – Debt default plus falling exports; shortages of imported fuel and food.

Venezuela (2016–present) – Oil price collapse cut off foreign exchange; imports of food and medicine dried up.

Chronic Fiscal Mismanagement

Argentina (1989–1990) – Loss of confidence in the austral; shortages of imported fuel and consumer goods.

Brazil (1980s–1994) – Chronic deficits; shortages less acute, but inflation fed by wage-price spirals and import dependence.

Turkey (1990s–2001) – Fiscal deficits; not classic shortages, but reliance on imported energy created vulnerability.

Israel (1983–1985) – Fuel imports were a pressure point.

Post-Soviet Transition

Russia (1992–1994) – Collapse of Soviet supply chains; food and fuel shortages were widespread.

Ukraine (1993–1995) – Grain and energy shortages after the USSR’s collapse.

Georgia (1993–1995) – Energy shortages (electricity, fuel) and food scarcity.

Armenia (1992–1994) – Blockades caused fuel and food shortages.

Belarus (1994–2000) – Energy and food supply disruptions during transition.

Baltics (early 1990s) – Energy shortages after the Soviet breakup.

The Pattern

Food shortages dominate in war-torn or agrarian economies (Hungary, Greece, Zimbabwe, Nicaragua).

Energy shortages dominate in industrial economies or those reliant on imports (Germany, Yugoslavia, Venezuela, and post-Soviet states).

Export collapse (tin in Bolivia, oil in Venezuela, agriculture in Zimbabwe) removes foreign exchange, making imports of food and fuel impossible.

Rodger Malcolm Mitchell

Twitter: @rodgermitchell

Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell;

MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell;

……………………………………………………………………..

A Government’s Sole Purpose is to Improve and Protect The People’s Lives.

MONETARY SOVEREIGNTY