If you use ChatGPT and ask it, “What is the difference between Modern Monetary Theory (MMT) and Monetary Sovereignty (MS),” you might be told something like this direct quote from the AI:

Modern Monetary Theory (MMT)Inflation Causes: MMT posits that inflation can be caused by excessive federal deficit spending, which increases aggregate demand beyond the productive capacity of the economy.When too much money chases too few goods, prices rise, leading to inflation.

Inflation Control: MMT advocates for using fiscal tools, such as taxation and government spending adjustments, to manage demand and control inflation.It also supports the use of monetary policy, including interest rate adjustments by the Federal Reserve, to help control inflation. By raising interest rates, the Fed can dampen borrowing and spending, reducing inflationary pressures.Mitchell’s Monetary SovereigntyInflation Causes:

According to Mitchell’s concept of Monetary Sovereignty (MS), all inflations are caused by shortages of key goods and services, not merely by aggregate demand exceeding supply.This perspective emphasizes that inflation results from supply-side constraints, such as disruptions in production, supply chain issues, or shortages of essential commodities.

Inflation Control: Mitchell’s approach argues that federal spending should be directed at alleviating these shortages to control inflation. For example, investing in infrastructure, technology, and education can increase productive capacity and address supply constraints.It opposes the use of interest rate hikes to control inflation, arguing that increasing interest rates raises business costs (e.g., higher borrowing costs), which can exacerbate inflation rather than cure it.

Key DifferencesSource of Inflation: MMT: Focuses on demand-pull inflation due to excessive spending.Monetary Sovereignty: Emphasizes cost-push inflation due to supply shortages.

Policy Tools for Inflation:MMT: Uses both fiscal policy (taxation and spending adjustments) and monetary policy (interest rate changes) to manage inflation.Monetary Sovereignty: Advocates for targeted federal spending to address supply shortages and improve productive capacity, rejecting interest rate hikes as counterproductive.

Implications for Economic PolicyFiscal Policy: Both MMT and Monetary Sovereignty agree that the federal government, as a monetary sovereign, can use fiscal policy effectively to manage the economy. However, the focus differs:MMT: Balances between managing demand and supply.Monetary Sovereignty: Focuses more on addressing supply-side issues directly.

Monetary Policy: MMT: Supports the use of interest rate adjustments alongside fiscal measures.Monetary Sovereignty: Criticizes interest rate hikes, suggesting they increase costs for businesses and can worsen inflation, advocating instead for supply-side interventions.

Practical ExamplesSupply Shortages: During the COVID-19 pandemic, supply chain disruptions led to shortages of key goods, contributing to inflation. Mitchell’s approach would advocate for targeted investments to resolve these shortages, while MMT might consider both demand management and supply-side measures.

Interest Rate Policy: In periods of high inflation, MMT might support interest rate hikes to cool down demand, whereas Monetary Sovereignty would likely oppose such measures, focusing instead on increasing supply through strategic spending.

ConclusionUnderstanding the nuanced differences between MMT and Mitchell’s Monetary Sovereignty can lead to more informed and effective economic policies.

While MMT incorporates both demand and supply considerations and supports a combination of fiscal and monetary tools, Mitchell’s Monetary Sovereignty places greater emphasis on addressing supply-side constraints and rejects interest rate hikes as a tool for controlling inflation.

Both perspectives offer valuable insights into managing modern economies, highlighting the importance of context-specific approaches to economic policy.

Your benevolent friend.

The AARP is the self-anointed protector of the aged. Its website says:

“AARP represents the needs of the more than 100 million older Americans with lifestyles and political views as diverse as any group in the United States.

“We concentrate on the issues most important to those in the 50+ community as they age: economic security; health care; access to affordable, quality long-term care; creating and maintaining livable communities; consumer protections; caregiving; and ensuring that our democracy works better for all.”

Unfortunately, AARP has long published articles claiming that the Medicare and Social Security trust funds are running short of dollars and soon will need to cut benefits or increase taxes – specifically FICA – which supposedly supports those trust funds.

It’s all wrong:

1. The so-called “trust funds” are not real trust funds. They are merely bookkeeping notations that track dollars coming and dollars going out.

The federal government can raise, lower, or erase those numbers whenever it wishes.

2. Those “trust funds” don’t pay for anything. The government pays for Social Security and Medicare benefits like it pays for everything else: the military, roads, dams, Congress, the Supreme Court, the White House, NASA, etc.

It signs legislation that approves the creation of dollars and then pays for things with those newly created dollars. It can do this endlessly.

Here is a sample — a direct quote, actually — of what AARP has been telling people:

The trust funds from which Social Security benefits are paid won’t run short of money until 2035 — a year later than was predicted in last year’s report.

And, the Medicare trust fund for part A, which helps pay for inpatient hospital visits will cover all its bills until 2036 — five years longer than forecast last year.

And here’s the key paragraph. It contains facts you seldom are told by any of the media:

Other Medicare programs, including Part B doctor’s services and outpatient care and Part D prescription drugs, will have enough money indefinitely because premiums and federal contributions are automatically adjusted each year to cover costs.

That is the phrase to remember: ” . . . federal contributions are automatically adjusted each year to cover costs.”

It states very simply and clearly that the government pays whatever is needed to keep Part B viable forever. It is a tacit admission that at least some part of Medicare is not beholden to “trust funds” or to tax collections.

This begs the obvious question: If the government pays for some of Part B, why doesn’t it pay for all of Part B and Part A?

I asked the Copilot AI this question, and this is what it said: ”

“The reason Part A is not fully funded by the government is likely due to the historical structure of Medicare and the way it was initially designed.

Greenspan

“Part B is partially funded by monthly premiums paid by beneficiaries and general tax revenue. The rationale behind this split may be to ensure that beneficiaries contribute to the cost of outpatient services while still receiving essential coverage.”

Those monthly premiums come out of your Social Security benefits. You need the money; the federal government doesn’t.

The inevitable conclusions are:

1. Since federal contributions are automatically adjusted each year, no calculation is made about whether the federal government can afford these contributions; affordability is assumed.

2. When Medicare and Social Security were created (1935 and 1965, respectively), the U.S. was still on a form of gold standard. Its money-creation ability was limited by its gold supplies. It was only partially Monetarily Sovereign.

This ended in 1971, when the government became fully Monetarily Sovereign. As Alan Greenspan said during a 1985 congressional hearing,“There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Bernanke

3. Thus, the federal government can pay for Social Security and Medicare without levying any taxes. Ben Bernanke said during an interview with Scott Pelley on March 12, 2009, when asked if the money the Federal Reserve (Fed) spends is tax money, “It’s not tax money… We simply use the computer to mark up the size of the account.”

4. From an affordability standpoint, the federal government could afford to fully fund a comprehensive, no-deductible Medicare and a far more generous Social Security—for all Americans of any age—without ever levying taxes.

This fact leaves doubters with two objections, both unmoored from fact:

Objection: Federal funding of Medicare and Social Security is Socialism.

Fact: Socialism is government ownership and control, not just spending. The above proposals would change nothing regarding ownership and control, so they would not move us any closer to Socialism.

Objection: Federal funding of Medicare and Social Security would cause inflation.

The most recent inflation was caused by COVID-related shortages of oil, food, computer chips, lumber, metals, labor, and other necessities, not by low interest rates or excessive federal spending.

The shortages and inflation are being cured by additional federal spending to acquire and distribute the scarce goods.

Summary

AARP acknowledges the easily and often proven fact that although state and local taxes fund state and local spending, federal taxes do not fund federal spending.

The federal government easily could fund Medicare and Social Security for all and forever.

The claims about the imminent need to limit benefits or raise taxes do not comport with reality, which is that the government should increase benefits and eliminate FICA forever.

If you are tired of the dire warnings that serve only to widen the income/wealth/power Gap between you and the very rich, tell this to your Congressional representative.

Do it today and every tomorrow, and tell your friends to do it too.

As Galileo taught us, some truths take a while to be accepted.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell;MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell; https://www.academia.edu/

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

South Florida leaders want to head off ‘silver tsunami’ aging crisis

By Lisa J. Huriash || South Florida Sun Sentinel UPDATED: July 17, 2024

Lisa J. Huriash

Broward County said it is aggressively encouraging construction — and helping fund — affordable housing for seniors.

South Florida leaders are urging a state planning council to tackle the impending “silver tsunami” as concerns grow for retirees’ well-being as they age.

At a recent meeting of the South Florida Regional Planning Council, chairman Steve Geller, who is also a Broward County commissioner, said he would push for aging issues to be discussed at a broader conference this fall where experts could guide policy suggestions.

The conference will include Palm Beach, St. Lucie, Monroe, Broward, Miami-Dade, Martin and Indian River counties, which is about one-quarter of the state’s population.

“Concerns are growing” among Florida leaders who will “push for” discussion of aging issues and to “address” and “tackle” the financial problems of one-quarter of the state’s population. No word yet about the three-quarters.

With all that pushing, addressing, tackling, and concern, we can be confident that our elderly will be well taken care of. Not.

Geller said more attention is needed to deal with the anticipated wave of older Americans who are facing retirement without a pension like their parents relied on, and face unique transportation and healthcare problems as they age.

And the above-mentioned housing problem.

The median personal income for people age 65 and older is $29,740, according to the federal Administration for Community Living.

Imagine trying to survive on $29,740 a year. And that’s the median, meaning half the seniors are trying to survive on less, much less.

“I don’t think we are prepared for it,” Geller said after the meeting.

That was the understatement of the decade.

Meeting the transportation needs of an aging population, including new signage, changing paratransit to add low floors and improved audio and visual announcements, more community shuttles and vans, and “safe transitioning” for seniors to stop driving.

It’s good to meet the “transportation needs” of the elderly. Action should be taken immediately.

Geller also said there could be a consideration to create crosswalks that give seniors more time to get across the street.

Yes, crosswalks that give the elderly more time to cross are good. Now, let’s get to the biggest problems.

The costs of long-term care average more than $100 per day nationwide for a four-hour daily home health aide.

What about the elderly who need more than four hours of care?

Yet “the majority of older adults will need these services, and those with meager incomes, who are most likely to require them, have the fewest resources to pay for them,” according to a November study by the Harvard Joint Center for Housing Studies.

According to the report, about 85% of seniors age 75 and older in Miami-Dade and Broward who live alone cannot afford daily home care in addition to housing and other necessities.

Former Fed Chairman Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Think about it. You work your whole life, and then, in your senior years, you live in misery. That is America. Of course, it’s unnecessary, but you wouldn’t think so if you look at the excuses for not helping these senior citizens.

While Ms. Huriash is right to be concerned about the monetarily non-sovereign Broward County’s ability to fund support for seniors, the entire problem could be solved via Monetarily Sovereignfederal funding.

The federal government could fund all the solutions by pressing a few computer keys but fails to do so. Here are examples of the phony excuses the ignorant and/or lying con artists shovel on you:

Too many beneficiaries and supported by too few taxpayers: The U.S. population is aging rapidly, leading to more beneficiaries than the working population contributing to the funds.

Trust Fund Depletion: The Social Security Old-Age and Survivors Insurance (OASI) Trust Fund is projected to be able to pay 100% of scheduled benefits until 2033. After that, it will only be able to cover about 79% of benefits unless changes are made.

Rising Hospital Costs: The Hospital Insurance (HI) Trust Fund, which funds Medicare Part A, is projected to be able to pay 100% of benefits until 2036. After that, it will only cover about 89% of benefits.

Rising Healthcare Costs: The Supplemental Medical Insurance (SMI) Trust Fund, which covers Medicare Parts B and D, is adequately financed but faces rapidly rising costs, increasing the financial burden on beneficiaries and taxpayers.

Former Fed Chairman Ben Bernanke: “The U.S. government (can) produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.:

Excuse #1. Too many beneficiaries and supported by too few taxpayers.

Two huge lies were packed into one short sentence. The working population pays FICA taxes, but FICA taxes don’t fund anything.

Your tax dollars come from the “M2 money supply measure,” and when they reach the Treasury, they cease to be part of any money supply measure.

They disappear from the economy and effectively are destroyed.

The Treasury keeps a record of the dollars it receives, but it neither needs nor uses those dollars.

Even if it didn’t receive a single dollar, the federal government has the infinite ability to create dollars to support an infinite number of beneficiaries.

In summary, federal taxes and taxpayers do not fund federal spending, and we don’t have too many beneficiaries

Excuse #2. Trust fund depletion.

The Social Security Old-Age and Survivors Insurance (OASI) Trust Fund is not a trust fund, and it doesn’t pay for anything.

A federal trust fund is nothing more than an accounting mechanism used by the federal government to track earmarked receipts (money designated for a specific purpose or program) and corresponding expenditures.

It’s just a record-keeping device, not a funding source.

The largest and best-known trust funds supposedly finance Social Security, portions of Medicare, highways and mass transit, and pensions for government employees.

Federal trust funds bear little resemblance to their private-sector counterparts, and therefore the name can be misleading.

“Sorry. This pail is empty. I can’t give you any water.”

A “trust fund” implies a secure source of funding.However, a federal trust fund is simply an accounting mechanism that tracks inflows and outflows for specific programs.

In private-sector trust funds, receipts are deposited, and assets are held and invested by trustees on behalf of the stated beneficiaries.

In federal trust funds, the federal government does not set aside the receipts or invest them in private assets.

Rather, the receipts are recorded as accounting credits in the trust funds and then combined with other receipts that the Treasury collects and spends.

Further, the federal government owns the accounts and can, by changing the law, unilaterally alter their purposes and raise or lower collections and expenditures.

Emphasis: The federal government canunilaterally alter the (trust funds’) purposes and raise or lower collections and expenditures.

When you are told that a federal trust fund will run out of money on a certain date, that means Congress could easily increase the balance to match future spending simply by deciding to do so, but so far, it hasn’t.

The federal government could (and should) increase the balance of any trust fund by trillions of dollars merely by passing a law without collecting a dollar in taxes.

Excuse #3 and #4. Rising hospital and healthcare costs

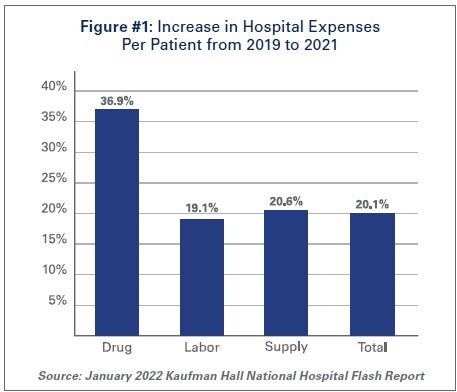

Hospitals and health systems have repeatedly confronted a range of financial and operational challenges, including historic volume and revenue losses, as well as skyrocketing expenses.

When coupled with rising inflation and growth in input prices, these expense increases have been severely detrimental to hospital finances, leading to billions in losses and over 33% of hospitals operating on negative margins.

Throughout the pandemic, Congress has provided various forms of support and resources to hospitals to help them manage the increased demands and financial pressures.

Here are some key resources and support measures:

Financial Support

Provider Relief Fund:Established under the CARES Act, this fund provided financial assistance to healthcare providers to compensate for revenue losses and increased costs due to the pandemic.

Paycheck Protection Program (PPP): This program offered loans to healthcare providers to help them retain employees and cover operational costs.

Increased Medicare Payments: Congress increased Medicare payments for inpatient COVID-19 admissions by 20% and provided additional payments for administering COVID-19 vaccines.

Resources for COVID-19 Response

Vaccines and Treatment: Funding was allocated for the development, distribution, and administration of COVID-19 vaccines and treatments.

Personal Protective Equipment (PPE): Resources were provided to ensure hospitals had adequate PPE for their staff3. Testing and Contact Tracing: Additional funding was directed towards expanding testing capabilities and contact tracing efforts.

Support for Rural Hospitals

Rural Health Care Providers: The American Rescue Plan Act included $8.5 billion to reimburse rural healthcare providers for expenses and lost revenues related to COVID-19.

Workforce Development

Workforce Support: Funding was provided for workforce development to ensure hospitals had the necessary staff to handle the increased patient load.

Congress and the President voted for trillions of dollars in support, some in loans and some in outright support. None was matched by increased taxes. The federal government simply did what it always does: It passed laws that created the money from thin air.

The federal government has the infinite ability to pass such laws.

Excuse #5. Politics

Here’s where the real lying comes into play. You are being told that solving all these problems requires raising taxes, cutting benefits, or increasing the retirement age.

It is an absolute lie whose purpose is to widen the income/wealth/power Gap between the rich and the rest of us. The lie is told at the behest of the rich, who become richer when the Gap widens.

The federal government is Monetarily Sovereign. It has the infinite ability to create U.S. dollars for any purpose. It does not need to collect taxes to fund anything, and it certainly does not need to borrow dollars, cut benefits, or increase the retirement age.

Federal taxation has two purposes, neither of which is to fund federal spending:

To control the economy by taxing what the government wishes to restrict and by giving tax breaks to what the government wishes to reward. (Currently, the government wishes to reward the rich by giving them tax breaks that are not available to the rest of us.)

To guarantee demand for the U.S. dollar by requiring taxes to be paid in dollars.

If you are old, or expect to be, don’t bother asking the federal government for help. They will lie to you.

They will tell you they can’t afford to give you comprehensive, no-deductible, completely free Medicare, nor can they give it to your spouse and children.

A lie.

They will tell you there are too many people asking for too much money.

A lie.

They will tell you that because doctor, nursing, hospital, drug, service, and equipment costs have risen, there is not enough money left in trust funds to care for the elderly, let alone younger Americans.

A lie.

They will tell you the only way to “save” existing Medicare is to raise your taxes and/or to cut your benefits.

A lie.

These are all lies on behalf of the rich, who want to widen the income/wealth/power Gap below them.

They bribe the politiciansvia campaign contributions and promises of lucrative employment opportunities.

They bribe the media via ownership and advertising dollars.

They bribe the economists via university endowments and employment in “think tanks.”

They do everything possible to brainwash you into believing federal finances are like personal finances when the two are polar opposites. The false comparison is called the Big Lie in economics.

As you read this prediction, keep in mind it came twenty-three years ago.

“We have to live within our means. We have to reduce our deficit, and we have to get back on a path that will allow us to pay down our debt. And we have to do it in a way that protects the recovery, protects the investments we need to grow, create jobs, and helps us win the future.

“Even after our economy recovers, our government will still be on track to spend more money than it takes in throughout this decade and beyond. That means we’ll have to keep borrowing more from countries like China.

“That means more of your tax dollars each year will go towards paying off the interest on all the loans that we keep taking out. By the end of this decade, the interest that we owe on our debt could rise to nearly $1 trillion.

“By 2025, the amount of taxes we currently pay will only be enough to finance our health care programs — Medicare and Medicaid — Social Security, and the interest we owe on our debt. That’s it. Every other national priority -– education, transportation, even our national security -– will have to be paid for with borrowed money.

“Now, ultimately, all this rising debt will cost us jobs and damage our economy. It will prevent us from making the investments we need to win the future. “

“We won’t be able to afford good schools, new research, or the repair of roads -– all the things that create new jobs and businesses here in America.

“Businesses will be less likely to invest and open shop in a country that seems unwilling or unable to balance its books. “And if our creditors start worrying that we may be unable to pay back our debts, that could drive up interest rates for everybody who borrows money -– making it harder for businesses to expand and hire, or families to take out a mortgage.

“Around two-thirds of our budget — two-thirds — is spent on Medicare, Medicaid, Social Security, and national security. Two-thirds. Programs like unemployment insurance, student loans, veterans’ benefits, and tax credits for working families take up another 20 percent.

“What’s left, after interest on the debt, is just 12 percent for everything else.”

That is the doom and gloom Obama fed you then; it’s the same diet of liesyou’ve been fed since 1940; and it’s the same utter nonsense you’ll hear today and tomorrow.

It’s the same lies you’ll be told every time the ridiculous, unnecessary “debt ceiling” comes up for debate — you know, the nonsense that paralyzes Congress every few months and is resolved simply by raising the ceiling withno adverse aftereffects.

(Since it already has been raised more than a hundred times, why not just get rid of it? Congress has been bribed to posture about lies.)

And now, thirteen years later, none of Obama’s predictions have come true. Why? Because they all were lies.

Every single time we have paid down the so-called “debt,” we have had recessions and depressions—not some of the time, butevery time.

The rich want you to believe the government can’t afford Medicare, Medicaid, Social Security, unemployment insurance, student loans, veterans’ benefits, and tax credits for working families.

Of course, nothing is said about the costs of those tax breaks for the richthat allowed a billionaire like Donald Trump to pay less income tax than did for the past ten years.

The rich want those cuts expanded. Trump has promised to expand them if he is elected. The rich are happy that Trump’s poor suckers will vote for his tax cuts.

It’s nice that so many people have written to me expressing outrage at the Big Lie. I appreciate your sentiments. But really, folks, I’m already in your corner and have been for twenty-five-plus years. And I’m pushing 90, so if you think Trump and Biden are too old, well . . .

If you want to make a difference, direct your outrage at someone who can do something about it. The politicians, the media, and the university economists.

Call them. Scream at them. Do it again, and again, and again. Every day. Twice a day. Never let up. Let them know you aren’t fooled.

Get your friends involved—and their friends, and theirs. Start a “Truth Club.” Bombard the information sources with truth bombs.

If you do nothing, nothing will happen. The lies will continue. The rich will grow richer. And years from now you will . . . As the poet Thoreau said, “The mass of men lead lives of quiet desperation.”

Today’s irony: John Stossel authored a book titled, “Myths, Lies, and Downright Stupidity.”

He also is a Libertarianand worked for Fox News, both of which explain much, the former explaining ignorance about Monetary Sovereignty and the latter explaining reluctance to speak the facts.

Here is an article he wrote:

Our Government is Now So Deep in Debt that Taxpayers Must Spend $1 Trillion a Year Just In Interest

In a recent video, libertarian pundit John Stossel delves into the alarming state of America’s national debt.

Stossel highlights a staggering reality: taxpayers now must shell out $1 trillionannually just to cover the interest on the federal debt.

This figure surpasses even the country’s defense spending, underscoring the severity of the fiscal crisis.

What should be alarming to anyone who has trusted Stossel’s claims is that he displays abject ignorance of Monetary Sovereignty.

The federal ‘debt” is not debt as you know it, and taxpayers do not owe it. The misnamed “debt” is the total of deposits into Treasury Security accounts (T-bills, T-notes, T-bonds).

Those federal bills, notes, and bonds are nothing like the private sectorbills, notes, and bonds. They merely are depositsinto accounts that are wholly owned by the depositors.

The U.S. federal government is Monetarily Sovereign—i.e., it has the infinite ability to create its sovereign currency, the U.S. dollar, at the touch of a computer key.

It has no need to borrow dollars from anyone, and indeed, it never does borrow dollars.

The government does not owe the dollars held in Treasury Security accounts for the simple reason it never takes ownership of those dollars.

The accounts resemble safe deposit boxes in that the government merely holds the dollars for safekeeping and returns them to the owners, plus interest, upon maturity.

Thus, the purpose of T-securities is not to provide spending funds for the government, which already has infinite spending funds. The purposes are:

To provide a safe storage place for unused dollars, safer than any bank. Because dollars are so vital to world trade, safe storage for billions of unused dollars is vital to stabilize the value of all currencies.

To help the Federal Reserve control interest rates by providing a “floor” interest rate, above which all lending is determined.

Again, the important fact that Stossel misses: The federal government does not borrow U.S. dollars. Who says so? How about:

Former Federal Reserve Chairman Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wantsand paying it to somebody.”

Former Federal Reserve Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishesat essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

All of this is true because the U.S. is Monetarily Sovereign. This is not just true of the U.S. government. Other entities are Monetarily Sovereign. For example, the European Union is sovereign over the euro:

Former President of the European Central Bank Mario Draghi: (ECB): “We cannot run out of money.”

So, any thinking person would ask themselves, if the U.S. federal government can produce as many dollars as it wishes, why would it ever borrow dollars? It doesn’t.

When President Richard Nixon divorced the U.S. from gold in 1971, the final limitation on the government’s ability to create money by pressing computer keys was lifted.

Seemingly, John Stossel either is clueless about Monetary Sovereignty, or being a Libertarian, he doesn’t want youto know about it. So, he writes misinformation or disinformation, depending on motive.

Stossel starts by lamenting the depth of America’s debt, which has reached unprecedented levels. He notes that the annual interest payments on this debt have ballooned to $1 trillion.

Those interest payments, which are not a burden on U.S. taxpayers and are created at virtually no cost to the government, help grow the U.S. economy.

The reason: A growing economy requires a growing money supply. Net federal spending (spending minus taxes) adds growth dollars to the economy.

Gross Domestic Product = Federal Spending + Nonfederal Spending + Net Imports

The above formula demonstrates the crucial role federal spending plays in economic growth.

Reduce federal spending, and you reduce GDP unless, somehow, Nonfederal Spending increases dramatically.

However, adding fewer federal dollars to the economy decreases Nonfederal Spending. If federal spending decreased, we would need a massive increase in Net Exports for GDP to increase.

Economic growth requires federal spending growth.

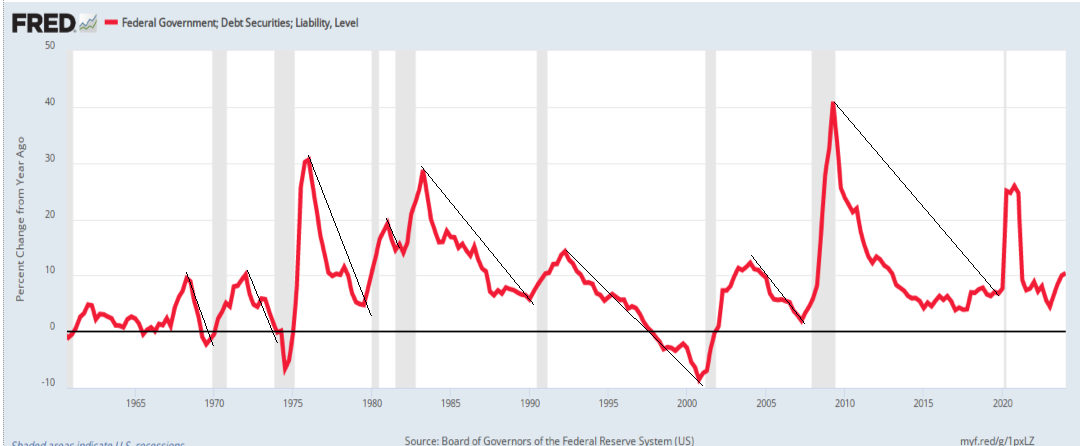

Declines (black diagonal lines) in federal “debt” growth (red) lead to recessions (vertical gray bars), which are cured by increased “debt” growth.

You’ve seen it time and again. We go into a recession, so what does the government do? It increases deficit spending to get us out of the recession.

It always amazes me that people easily accept the fact that federal deficit spending can cure a recession but fail to see that it can also prevent one.

As soon as our deficit spending cures a recession, what do we do? At the behest of the Stossels of the world, we again begin to cut deficit spending because it carries the word “deficit,” which increases the “debt” (which isn’t federal and isn’t debt).

It isn’t federal because the money is owned by the depositors, not by the federal government. It isn’t debt because the federal government doesn’t owe the money; it merely stores it for the owners.

Imagine your team is losing a baseball game. You know you need to score net runs (more runs than the opposition) to win. So you score net runs and begin to win.

The owner of this storage facility didn’t borrow bicycles and a scooter from this customer. They are not part of the facility owner’s debt.

But because you’re ahead, you decide you no longer need to score net runs until you start losing again.

Call that Libertarianism (or “Stosselism”)

This enormous sum not only hampers the nation’s financial flexibility but also threatens its long-term economic stability.

Stossel is confused by the word “debt.”

Imagine you own a self-storage facility, and someone stashes some bicycles in it.

Your financial flexibility wouldn’t be threatened.

And if they gave you more bicycles to put in your storage facility, your financial flexibility still wouldn’t be threatened.

And if they said, “You owe me all those bicycles,” you would say, “They’re yours. Take them out.”

That is exactly how T-bills, T-notes, and T-bonds work. The federal government stores depositors’ money but doesn’t own it. Depositors can have it back without any burden on the government or on taxpayers.

Stossel warns that this unsustainable path will “cripple our future,” yet politicians seem more focused on increasing spending rather than addressing the debt issue.

And there it is again, that word the Libertarians love to use: “Unsustainable.” Except for one problem: They never explain why the federal government can’t “sustain” a so-called “debt” that has been growing since 1940 when it was first called a “ticking time bomb.”

Since 1940, that “time bomb” has been “ticking” year after year while America’s economy grows stronger and stronger.

“Gimme a break”

Stossel criticizes politicians from both major parties for their contradictory statements and actions regarding the national debt.

While some politicians claim to have reduced the deficit, the reality is starkly different.

The debt continues to rise, now increasing by $1 trillion every 100 days.

This disconnect between rhetoric and reality is a significant concern for Stossel, who highlights the bipartisan nature of this fiscal irresponsibility.

The only “disconnect between rhetoric and reality” is Stossel’s claim.

Reflecting on past events, Stossel recalls the bipartisan support for the largest stimulus bill in U.S. history, passed during the early stages of the COVID-19 pandemic.

The stimulus bill did exactly what it was supposed to do. It added the dollars that cured shortages, reduced COVID-19 inflation, ended a recession, and led to today’s growing economy.

This legislation saw overwhelming approval in the Senate, demonstrating a rare moment of unity.

However, Stossel points out that the bill included numerous expenditures that lacked direct relevance to the pandemic, such as funding for NPR and the Kennedy Center.

This, he argues, exemplifies the government’s tendency to spend lavishly without considering the long-term fiscal implications.

Is Stossel saying it was wise to spend economic stimulus money to cure COVID but not to spend money that aids independent news broadcasts? What exactly is he arguing against? COVID dollars are OK, but non-COVID dollars are bad?

Addressing potential solutions, Stossel discusses the commonly proposed ideas of raising taxes on the wealthy or printing more money.

He dismisses these options as insufficient or harmful.

Taxing billionaires, he explains, would only cover a fraction of the debt, while printing more money – a concept embraced by proponents of Modern Monetary Theory – risks severe inflation.

He cites historical examples, including Zimbabwe and 1920s Germany, where unchecked money printing led to economic disasters.

Again, Stossel parrots common (but wrong) beliefs.

A price increase in any one product can come from an increase in demand for that product or from a sudden shortageof that product.

But inflation is an increase in prices for virtually all products and services.

Historically, government spending can’t cause a general increase in demand. When the government increases spending on Social Security, Medicare, and the military (the three largest balance sheet items), this doesn’t suddenly result in increased demand for virtually all products and services.

All inflations in history have been caused by shortages of critical goods and services, most often oil and food.

The current inflation was not caused by increased demand. There was no sudden increase in demand.

What was sudden? COVID. The current inflation was caused by COVID-related shortagesof oil, food, shipping, steel, wood, computer chips, labor, and many other products and services.

The price of oil affects the prices of virtually all other products and services. Historically, oil shortages parallel inflation.

Zimbabwe’s inflation was not caused by currency printing. The Zimbabwe government took land from farmers and gave it to people who didn’t know how to farm. The predictable result was food shortages, which caused Zimbabwe’s hyperinflation.

The Zimbabwe government’s misguided response was to print currency. The correct response would have been to spend money on increased food production while obtaining and distributing food.

The infamous German hyperinflation was caused by a complex series of events, beginning with Germany’s WWI war reparation payments that caused shortages of goods.

Using German hyperinflation as an example of what could happen in America demonstrates Stossel’s superficiality and ignorance of economic history.

German government deficit spending actually increased massively as the inflation ended (partly thanks to the end of the international gold standard) to fund the greatest war machine the world ever had known.

Stossel outlines the grim alternatives facing the U.S.: defaulting on the debt or continuing on the current path.

Defaulting would devastate the savings of everyone who invested in America and wouldn’t solve the underlying problems. Continuing on the current trajectory, however, only deepens the debt, making eventual solutions more painful and disruptive.

Federal “debt” (deposits) increased from about $43 billion in 1940 to about $33 trillion today, an 82,400% increase.

If, in 1940, someone had told Stossell the federal “debt” (deposits) would increase 82,400 percent in the next 84 years, he would have predicted inflations, recession, depression, stagflation, and every other calamity you could imagine.

Yet here we are, with the world’s most successful economy, powerful growth, and full employment. (Now we must reduce the income/wealth/power Gap between the rich and the rest.)

Despite the severity of the debt crisis, Stossel notes that politicians rarely take meaningful action. They talk about reducing the deficit and debt but fail to implement substantial changes.

He cites past presidents who have acknowledged the problem without delivering effective solutions, leading to the doubling of the national debt under recent administrations.

Someone, please tell Stossel that Clinton actually did reduce the federal debt. The result is shown below.

Debt reduction requires the federal government to run a surplus, that is, to take dollars out of the economy.Stossel should learn how reducing the “debt” works in the real world.

Here is the result of every “debt” reduction since 1804:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Only one period of federal surplus (“debt” reduction) has occurred since 1940, and it caused a recession.

Stossel emphasizes the importance of cutting government spending or at least slowing its growth. He criticizes the current political climate, where both major parties seem more interested in spending increases rather than fiscal restraint.

Why does Stossel want to slow growth? He’s a Libertarian. That is the only answer I can give.

This lack of willingness to address the debt issue leaves the country on a path towards economic instability and potential bankruptcy.

Oh, really. Here is what someone knowledgeable says:

Alan Greenspan:“A government cannot become insolvent with respect to obligations in its own currency.”

People in the comments shared their thoughts on this situation: “The average person had no clue how bad of shape we’re in. Politicians have ruined this once great nation.

“Ruined our once great nation”?? Does this look like it has been ruined?

The above graph shows the real (inflation-adjusted) per capita growth of America’s Gross Domestic Product (blue line). That is solid per-person growth, not the “ruined” nation that Stossel claims.

The red line shows the federal “debt” (deposits) over the same period. As they have grown, so has GDP.

Another commenter added: “Our economy is struggling with uncertainties, housing issues, foreclosures, global fluctuations, and the pandemic aftermath, causing instability.

Rising inflation, sluggish growth, and trade disruptions need urgent attention from all sectors to restore stability and stimulate growth.”

Who exactly was this “other commenter”? Donald Trump? Fox News?

When exactly did any nation not have “uncertainties, housing issues, foreclosures, trade disruptions, instability, and global fluctuations”? It’s called reality.

COVID-related inflation is not rising; it’s falling. Growth certainly is not sluggish. And what “trade disruptions” have been caused by federal deficit spending? Stossel never says, preferring to bleat meaningless generalities.

In concluding his video, Stossel urges viewers to share and spread awareness about the national debt crisis. He believes that increasing public awareness is crucial to pressuring politicians to take necessary actions.

The $1 trillion annual interest payment is a clear indicator of the urgent need for fiscal responsibility and sustainable economic policies.

The $1 trillion interest payment indicates that the federal government has no trouble pumping growth dollars into the economy.

What do you think? What specific steps can the government take to reduce the national debt without compromising essential services?

How can the public hold politicians accountable for their fiscal policies and spending decisions? What are the long-term economic consequences if the national debt continues to grow at the current rate?

These are good questions for which Stossel has no answers. How would he cut federal deficit spending without cutting Medicare, Social Security, the military, and the thousands of other programs the government funds?

If the national “debt” (deposits) continue to grow at the current rate, the economy probably will continue to grow at the current rate.