Recently, I had a conversation with a young man who told me that federal deficit spending causes inflation.

If you took an economics course in school, you probably agree with him because that is what they teach. His logic was simple. He has been taught:

Federal deficit spending increases the supply of dollars. When one increases the supply of any product, without increasing demand, the value of that product decreases. When the value of the dollar decreases, we experience inflation.

Adding money to the economy increases demand, which, in the absence of increased supply, causes shortages, which create inflation.

The problem with #1 is that money is unlike any other product or service. The demand for money is relatively inelastic.

Example: You own a Tesla and learn that Teslas are now on sale at bargain prices. Will you buy an additional Tesla?

Or you see that tomatoes are on sale, but you have a dozen at home. Do you want additional tomatoes? Probably not.

But you have a million dollars and hear of an investment that will pay you another million at no risk. Do you want that additional million dollars? Probably so.

Currency printing didn’t cause inflation. Scarcities cause inflation, which causes a government to print currency.

The point: Federal deficit spending adds dollars to the economy, but that additional supply doesn’t reduce the dollar’s value.

In fact, if those extra dollars are used to obtain products or services that are in short supply, they can reduce the inflation caused by the shortages.

That is the problem with #2, because when the federal government spends dollars in the economy, the economy usually responds by increasing the supply of goods and services.

While deficit spending can be inflationary if it leads to excessive demand without corresponding increases in supply, spending can address supply-side constraints, boost productivity, and ultimately help reduce inflation.

There can be no economic growth without federal deficit spending.

The illusion that deficit spending causes inflation may come from hyperinflations, where governments print currencies in response to inflations.

It’s the “wheelbarrows filled with currency” visual we all have seen.

In those situations, inflation has been caused by scarcities of critical products and services, such as oil, food, labor, transportation, etc., and the additional dollars do nothing to relieve those scarcities.

When a government fails to address the real causes of inflation but instead prints currency, the inflation worsens,

The illusion of cause and effect is reversed. Money “printing” doesn’t cause inflation. Inflation can cause money printing if a government doesn’t understand what really causes inflation: Shortages of crucial goods and/or services.

It’s like a baseball team losing by five runs because it is short of good pitchers. So it trades its few decent pitchers for more hitters and starts losing by ten runs.

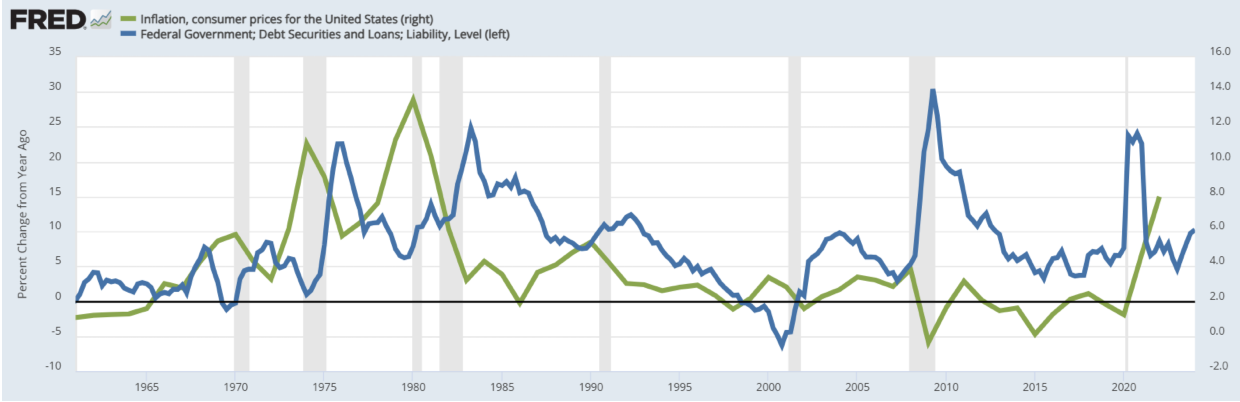

Here is a graph demonstrating the relationship (or rather, lack of relationship) between federal deficit spending and inflation:

The blue line shows the annual inflation rate in the U.S. The red line shows the annual deficit increase in the U.S. The lines are not parallel. Recessions (gray vertical bars) result from declining deficit growth and are cured by increased deficit growth.

Presumably, if federal deficit spending caused inflation, the two lines would generally be parallel. They are not. In fact, they tend to move in opposite directions.

One could use the above graph to demonstrate that federal deficit spending often cures inflation by reducing the shortages that do lead to inflation.

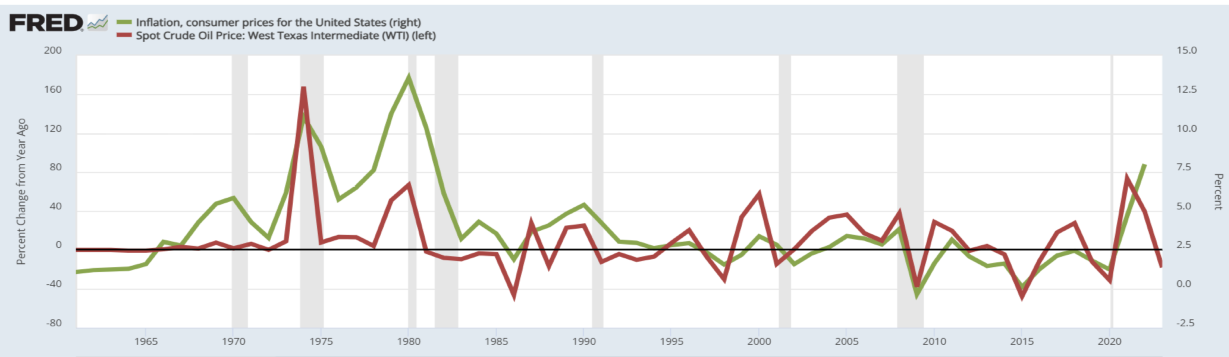

By comparison, please look at the following graph:

The blue line again shows the annual inflation rate. The green line shows the annual percentage changes in oil prices.

The lines in the above graph are essentially parallel, indicating a close relationship between oil prices and inflation.

Changes in oil supplies have had a far more profound and sudden effect on oil prices than changes in oil demand, which generally are slow.

Overall, the graphs suggest that federal deficit spending plays, at most, a minor role in inflation, and possibly none at all, while oil supplies (in addition to supplies of food, shipping, labor, and other products) are the main drivers of inflation.

Our most recent inflation was caused by COVID-related shortagesof oil, food, shipping, labor, metals, wood, and other products. When these shortages were eased by federal deficit spending, inflation eased.

This is an important fact because the threat of inflation is often used as an excuse for not federally funding social programs like Social Security, Medicare, and anti-poverty efforts.

The income/wealth/power Gapis what makes the rich wealthy. Without the Gap, no one would be rich; we would all be the same. The wider the Gap, the wealthier are the rich.

The wealthy are aware of this, and in their efforts to become even richer, they try to widen the Gap by increasing their own wealth and power and/or diminishing the resources of others.

One way they do this is by claiming that the social programs are becoming insolvent and so must be cut or taxes increased.

However, it is difficult for them to deny that the federal government could afford to fund these programs. Even the lie that the federal government would have to borrow dollars is easily debunked for two reasons:

As a Monetarily Sovereign entity, the federal government can create dollars at will by simply pressing keys on a computer.

Former Fed Chairman Ben Bernanke:“The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Even if the notion of future borrowing and increased interest payments were accurate (it isn’t), it would be of no significance to an entity that possesses the unlimited capacity to settle its debts by pressing computer keys. Statement from the St. Louis Fed:

“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

So, the rich resort to the false claim that federal spending causes inflation.

What they fail to mention is the following graph, which highlights the relationships between federal deficits and recessions:

When federal deficit growth (red) decreases, we have recessions (vertical gray bars). Recessions always are cured by increases in federal deficit growth.

Economic growth requires money growth. Here is an example of the close relationship between economic growth and money growth

Gross Domestic Product (GDP) closely mirrors money (debt) growth.

The formula for Gross Domestic Product shows how money growth is necessary for economic growth:

GDP = Federal Spending + Non-Federal Spending + Net Exports

Net Exports generally are negative. (We import more than we export). So, GDP growth relies on federal and non-federal spending growth.

Federal Spending is a large part of M3, which in turn, is a large part of GDP. Federal Spending growth is necessary for GDP (economic) growth.

Then, of course, there is the fact that federal surpluses (the extreme version of deficit reduction) cause depressions (the extreme version of recessions). In fact, every depression in American history has resulted from surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

All money is a form of debt. Have you noticed that every dollar bill (“bill” is a word that denotes debt) is a Federal Reserve note (“note” is another word denoting debt)?

Each bill is signed by the Treasurer and the Secretary of the Treasury.

The U.S. dollar is nothing more than a number on the federal government’s books. It is not a physical entity. There are no physical dollars. The U.S. dollar bill is a title to a dollar showing that the bearer is owed a dollar by the United States government.

For example, an author owns a story he has written, though the story is not a physical entity. Similarly, the federal government is an author of federal dollars, though those dollars are not physical entities. And just as the author can create infinite stories, the government can create infinite dollars.

All debt requires collateral. The collateral for federal debt is “full faith and credit.”

This may sound nebulous to some, but it involves certain, specific, and valuable guarantees, among which are:

A. –The government will accept only U.S. currency in payment of debts to the government

B. –It unfailingly will pay all its dollar debts with U.S. dollars and will not default

C. –It will force all your domestic creditors to accept U.S. dollars if you offer them to satisfy your debt.

D. –It will not require domestic creditors to accept any other money

E. –It will take action to protect the value of the dollar.

F. –It will maintain a market for U.S. currency

G. –It will continue to use U.S. currency and will not change to another currency.

H. –All forms of U.S. currency will be reciprocal, that is five $1 bills always will equal one $5 bill and vice versa.

The value of debt, i.e., the U.S. dollar, is based in part on the value of its collateral. Should any of A – H no longer be in effect, the dollar’s value would plummet.

Another key factor influencing the value of the U.S. dollar is interest rates. Investments denominated in dollars, such as bonds and Treasury securities, are more sought after when they offer higher interest rates.

Be cautious with this, as the value of a bond decreases when interest rates rise. Newly issued bonds offer higher rates and compete with older bonds.

The key point is that dollars do not lose value, and inflation is not caused by the federal government’s increasing deficit spending. The government could easily fund Social Security and Medicare without imposing FICA taxes or triggering inflation.

The wealthy classes’ arguments for cutting SS and Medicare benefits and raising taxes are unfounded and based on misleading claims.

IN SUMMARY

Inflations are caused by scarcities, often due to oil and food shortages. Shortages of shipping, labor, metals, wood, and electronics can also be significant factors.

While deficit spending can be inflationary if it leads to excessive demand without corresponding increases in supply, spending can address supply-side constraints, boost productivity, and ultimately help reduce inflation.

Without federal deficit spending, there can be no economic growth and no solution to scarcity. The lack of federal debt growth causes recessions and depressions. Recessions are cured by federal (money) deficit growth.

The federal government could and should fund a comprehensive, no-deductible Medicare and Social Security for every man, woman, and child, regardless of age and income, while eliminating FICA.

We’ll end this post with excerpts from an article on the MSN website:

Some House Republicans (show) interest in reviving the party’s longtime passion for gutting the social safety net in the wake of Donald Trump’s reelection and the coming Republican trifecta.

Reports have surfaced about cuts to programs like Medicaid and food stamps to offset the cost of extending Trump’s 2017 tax cuts.

Others are openly suggesting that Medicare and Social Security may be on the chopping block as part of Elon Musk and Vivek Ramaswamy’s performative venture into government spending cuts through the new Department of Government Efficiency.

But MAGA Republicans on Capitol Hill who recently spoke to TPM were unwilling to be pinned down on the issue.

The Republican Party promulgates public ignorance about the differences between federal (Monetarily Sovereign) finances and personal (monetarily non-sovereign) finances to put forth a “small government” agenda that will widen the income/wealth/power Gap between the rich and the rest of us.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell;MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell; https://www.academia.edu/

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

(Bloomberg) — Even before global finance chiefs fly into Washington over the next few days, they’ve been urged in advance by the International Monetary Fund to tighten their belts.

Two weeks ahead of a potentially era-defining US election, and with the world’s recent inflation crisis barely behind it, ministers and central bankers gathering in the nation’s capital face intensifying calls to get their fiscal houses in order while they still can.

The IMF’s Fiscal Monitor on Wednesday will feature a warning that public debt levels are set to reach $100 trillion this year, driven by China and the US.

Managing Director Kristalina Georgieva, in a speech on Thursday, stressed how that mountain of borrowing is weighing on the world.

How to lie with facts. Use meaningless numbers and compare non-comparable things.

Before we continue, let me show you the graphs showing the debt/GDP ratios of several countries. Look at the graphs and tell me what is misleading about them.

The graphs at the right have two main problems:

1. They combine two completely different things: Monetarily Sovereign nations and monetarily non-sovereign nations.

A Monetarily Sovereign nation has the infinite ability to create its own sovereign currency. It never can run short of money to pay its bills.

The U.S. cannot run short of dollars. China cannot run short of yuan. Japan cannot run short of yen, and the UK cannot run short of pounds. These nations are Monetarily Sovereign.

They all can pay any debt denominated in their sovereign currency, merely by tapping a computer key.

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

By contrast, Germany, France, and Italy are monetarily non-sovereign. They all use the euro, and can run short of euros to pay their debts. They must borrow from the European Union (EU) when they run short of euros.

The G-7 graph is a mongrelization of Monetarily Sovereign and monetarily non-sovereign nations (Canada, France, Germany, Italy, Japan, United Kingdom, United States) and thus is useless and misleading.

2. The debt/Gross Domestic Product ratio, which is the subject of the graphs is meaningless, though it often has been used by those who do not understand Monetary Sovereignty.

Here are the ten nations with the supposedly “worst” (highest) ratios:

Debt to GDP Ratio (%); Japan 264%, Venezuela 241%, Sudan 186%, Greece 173%, Singapore 168%, Eritrea 164%, Lebanon 151%, Italy 142%, United States 129%, Cape Verde 127%

Japan and the U.S. are ranked worst, along with Sudan, Greece, Lebanon, and Cape Verde.

Who would you prefer to lend to, Japan or Cape Verde? The United States or Sudan?

Now, here are the ten nations with the “best” (lowest) debt/GDP ratios: Brunei 2.1%, Kuwait 2.9%, Cayman Islands 4.5%. Afghanistan 7.4%. Turkmenistan 8%, Azerbaijan 11.7%, Burundi 14.5%, DR Congo 14.6%, Russia 17.2%, Palestine 18.5%

That’s right. According to the IMF, those are the financially safest places in the world.

The debt/GDP ratio is akin to a butter/butterfly ratio. Completely and utterly useless, yet here is the equally useless IMF shrieking about it.

This is what the IMF says about itself:

The International Monetary Fund (IMF) is an organization that aims to ensure the stability of the international monetary system. Its primary purposes are to:

1. Foster collaboration among countries to achieve global monetary stability.

2. Promoting exchange rate stability

3. Support economic policies that promote growth and reduce poverty.

4, Offer loans and financial aid to member countries facing balance of payments problems or economic crises.

5. Provide economic and financial advice.

It does none of those, except #4, which it uses like a loan shark, extorting unreasonable terms from weak countries. And really, would you take “economic and financial advice” from a group that doesn’t know the difference between Monetary Sovereignty and monetary non-sovereignty.

It is like taking medical advice from a quack doctor who doesn’t know the difference between heartburn and sunburn.

Continuing with the article:

“Our forecasts point to an unforgiving combination of low growth and high debt — a difficult future,” she said. “Governments must work to reduce debt and rebuild buffers for the next shock — which will surely come, and maybe sooner than we expect.”

For a Monetarily Sovereign nation “high debt” generally means the government is pumping more growth dollars into the economy. Lack of debt growth leads to recessions:

A decline in debt growth (red line) causes recessions (vertical gray bars) which are cured by an increase in debt growth.

Thus, the IMF’s “cut debt” advice is diametrically wrong, like taking blood from a patient to cure his anemia.

Some finance ministers may get further reminders even before the week is over.

UK Chancellor of the Exchequer Rachel Reeves has already faced an IMF warning of the risk of a market backlash if debt doesn’t stabilize. Tuesday marks the last release of public finance data before her Oct. 30 budget.

The UK tax office is taking a tougher approach to clawing back debts, insolvency specialists say, a bid to squeeze £5 billion ($6.5 billion) in extra revenue.

The above simple proves that many government economists are as financially ignorant as the IMF economists.

We have the same problem in the U.S., with so-called experts claiming our federal debt (which isn’t “federal” and isn’t “debt”) is a “ticking time bomb.” Total bullshit.

What Bloomberg Economics Says: “For all the talk of black holes, the overall effect of Reeves budget will be a policy that’s looser, not tighter, relative to the previous government’s plans.”

As it should be if the UK wants economic growth. If the UK is foolish enough to listen to the IMF and cut debt (which means take dollars out of the economy), it will have a recession.

Meanwhile, Moody’s Ratings has slated Friday for a possible report on France, which faces intense investor scrutiny at present. With its assessment one step higher than major competitors, markets will watch for any cut in the outlook.

France, being monetarily non-sovereign, does risk it’s debt being too high to service. The EU, which is Monetarily Sovereign, could solve France’s financial problems by simply giving them euros. That would cost European taxpayers nothing, and would prevent debt from being an issue.

As for the biggest borrowers of all, the glimpse of the IMF’s report already published contains a grim admonishment: your public finances are everyone’s problem.

True for monetarily non-sovereign nations; not true for Monetarily Sovereign nations.

“Elevated debt levels and uncertainty surrounding fiscal policy in systemically important countries, such as China and the United States, can generate significant spillovers in the form of higher borrowing costs and debt-related risks in other economies,” the fund said.

We’ll end with the final dollop of bullshit from the IMF. China’s and the US’s increase in debt means other nations are being enriched by dollars and yuan. The more these two governments spend on foreign goods and services, the better all the other governments’ finances will be.

As usual, the fools and con men of the IMF offer diametrically the opposite of good advice.

I suggest a motto for the science of economics: “The easy we make impossible, but it takes forever.”

I say that because of my 25 years critiquing economics articles, and most recently because of an article titled, “Do Budget Deficits Cause Inflation?”

The answer to the question is, “No, not for Monetarily Sovereign nations,” and the article comes to that “No” conclusion. Except:

It never differentiates between Monetarily Sovereign governments (which create and control the value and supply of the money they use) and monetarily non-sovereign governments (cities, counties, states, euro nations, nations that use another nation’s currency, and nations that peg their currency to another nation’s currency}.

It never mentions shortages of critical goods and services, most commonly oil, food, and labor, which are the real causes of inflation.

It complexifies a straightforward solution: To cure a problem, eliminate the cause of the problem. In the case of inflation, the cause is shortages. To cure inflations, eliminate the shortages.

Keith Sill, Senior Vice President of Research and Director of the Real-Time Data Research Center. keith.sill@phil.frb.org (215) 574-3815

In 2004, the federal budget deficit stood at $412 billion and reached 4.5 percent of gross domestic product (GDP).

Though not at a record level, the deficit as a fraction of GDP is now the largest since the early 1980s.

Moreover, the recent swing from surplus to deficit is the largest since the end of World War II.

Comment: The deficit as a fraction of GDP is irrelevant to inflation. Federal deficits are beneficial because they add GDP growth dollars to the economy.

Federal surpluses take dollars from the economy, causing depressions and recessions. Mr. Sill could have answered the title question with two simple graphs:

There is no relationship between federal deficit spending (blue line) and inflation.There is a strong relationship between the oil supply (red line) and inflation.

Inflation is caused by shortages of critical goods and services, most often oil, food, and labor.

The flip side of deficit spending is that the amount of government debt outstanding rises: The government must borrow to finance the excess of its spending over its receipts.

Comment: The federal government, being Monetarily Sovereign, never borrows. Why would it? It has the infinite ability to create its sovereign currency, the U.S. dollar, at virtually no cost (aka, “seigniorage”).

Further, unlike state/local government taxes, which fund state/local spending, federal taxes do not fund federal spending.

Federal taxes are destroyed upon receipt, while state and local tax dollars remain in the economy’s private banks. To finance all its spending, the federal government creates new dollars ad hoc.

It does this regardless of taxes collected. Even if federal tax collection totaled $0, the government could continue spending forever.

For the U.S. economy, the amount of federal debt held by the public as a fraction of GDP has been rising since the early 1970s. It now stands at a little over 37 percent of GDP.

The debt/GDP fraction is meaningless. It has no predictive or analytical power and does not tell anything about an economy’s health.

Do government budget deficits lead to higher inflation? When looking at data across countries, the answer is: it depends. Some countries with high inflation also have large government budget deficits. This suggests a link between budget deficits and inflation.

Yet for developed countries, such as the U.S., which tend to have relatively low inflation, there is little evidence of a tie between deficit spending and inflation.

Mr. Sill falsely equates “developed” with Monetary Sovereignty. However, there are “developed” nations – for example, Italy, France, Greece, etc. that are monetarily non-sovereign. They use the euro.

Why are budget deficits are associated with high inflation in some countries but not in others? Government deficit spending is linked to the quantity of money circulating in the economy through the budget restraint, i.e. the relationship between resources and spending.

Money spent has to come from somewhere: In the case of local and national governments, from taxes or borrowing.

But, nationalgovernments can also use monetary policy to help finance the government’s deficits.

I believe that Mr. Sill’s use of “resources” means the amount of money a government can spend, which it gets from taxes or borrowing.

Since he doesn’t differentiate among Monetarily Sovereign, monetarily non-sovereign, and “nationally,” his comments are either partially or totally wrong. First, a reminder about the differences between monetary policy and fiscal policy:

Monetary policy involves changing the interest rateand influencing the money supply.

Fiscal policy involves the government changing tax rates and spending levels to influence aggregate economic demand. (“Aggregate demand” is Gross Domestic Product at a specific time.)

Here are the sources of confusion:

1. Raising interest rates causes prices to rise. The cost of every product includes the cost of interest. Amazingly, this is the Fed’s tool to combat inflation. The Fed’s theory seems to be that raising prices will reduce demand, causing a recession that supposedly will cure inflation.

In short, the Fed causes inflation to cure inflation while claiming to hope a recession doesn’t occur but secretly relies on recession to cure inflation. (Clear?)

Of course, a result can also be stagflation, a combination of recession and inflation, at which point Fed Chairman Jerome Powell, having no solutions, will hide in his closet and pray. (The cure for stagflation is federal deficit spending to obtain and distribute the scarce products while adding growth dollars to the economy.)

2. As the issuer of its money, only a Monetarily Sovereign government can change interest rates by fiat. It sets the lowest rate on its Treasury Securities.

Because a monetarily non-sovereign government is not an issuer of money, it cannot unilaterally change interest rates. It must rely on markets or the issuer of its money.

For example, Italy cannot arbitrarily raise interest rates on euro-based loans. It uses the euro but is not the issuer.

3. Monetarily Sovereign governments don’t borrow their own currency. The above-mentioned Italy, being monetarily non-sovereign, borrows euros.

In short, Sill, an economist at the Fed (!), is confused about what different kinds of governments can do. Next, he confuses households with our Monetarily Sovereign government:

Budget constraints are a fact of life we all face. We’re told we can’t spend more than we have or more than we can borrow.

The U.S. government “has” infinite dollars, so it does not borrow dollars. Those federal T-securities are not a form of borrowing, which is what a monetarily non-sovereign government does when it needs money.

Rather than providing the U.S. government with dollars, T-securities:

Provide a safe parking place for unused dollars — safer than any other storage place (i.e., bank accounts, safe deposit boxes, etc.) The government never touches those dollars. They remain the property of the depositors.

Assist the Fed in controlling interest rates by setting a floor rate.

In that sense, budget constraints always hold: They reflect the fact that when we make decisions, we must recognize we have limited resources.

See the confusion? “We” and the Italian government have limited resources (money), but the U.S. government does not. It has unlimited money. Next, Mr. Sill expressly shows us his confusion between federal finance and personal finance:

Imagine a household that gets income from working and from past investments in financial assets. The household can also borrow, perhaps by using a credit card or getting a home-equity loan.

The household can then spend the funds obtained from these sources to buy goods and services, such as food, clothing, and haircuts.

It can also use the funds to pay back some of its past borrowingand to invest in financial assets such as stocks and bonds.

The household’s budget constraint says that the sum of its income from working, from financial assets, and from what it borrows must equal its spending plus debt repayment plus new investment in financial assets.

Not one word of the above applies to the U.S. government.

The government does not borrow or use dollars obtained from any source. It creates ad hoc all the funds it spends. Any income the federal government receives is destroyed upon receipt. (See: “Does the U.S. government really destroy your tax dollars?“)

The only federal budget constraint is not a budget constraint at all. Federal agencies routinely exceed budgets. The restraint is whatever Congress and the President say it is at any given moment.

Congress and the President have the unlimited ability to create dollars and stimulate the economy, plus a strong, though not unlimited, ability to obtain and distribute the scarcities causing inflation.

Mr. Sill continues with an explanation that is irrelevant to federal financing.

The household’s sources of funds and spending are all accounted for, and the two must be equal. The household may use borrowing to spend more than it earns, but that funding source is accounted for in the budget constraint.

If the household has hit its borrowing limit, fully drawn down its assets, and spent its work wages, it has nowhere else to turn for funds and would, therefore, be unable to finance additional spending.

I have no idea what Mr. Sills hoped to accomplish by giving household finances as his explanation for federal finances. The two are fundamentally opposite.

Here, Mr. Sills makes sure to show you that he doesn’t understand the difference between the federal government’s Monetary Sovereignty and your household’s monetary non-sovereignty:

Just like households, governments, face constraints that relate spending to sources of funds.

Governments can raise revenue by taxing their citizens, and they can borrow by issuing bonds to citizens and foreigners. In addition, governments may receive revenue from their central banks when new currency is issued.

Governments spend their resources on such things as goods and services, transfer payments such as Social Security to its citizens, and repayment of existing debt.

Central banks are a potential source of financing for government spending, since the revenue the government gets from the central bank can be used to finance spending in lieu of imposing taxes or issuing new bonds.

No, the U.S. government is not “just like households. It does not raise revenue by taxing you. It doesn’t borrow from the central bank. It doesn’t have an existing debt to repay.

And it finances its spending not with taxes or bonds but by creating new money ad hoc. Who says so, Mr. Sill? Your former bosses:

Former Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Mr. Sill’s article continues for many more paragraphs, so I will just quote one more thought:

There may be limits on the government’s ability to borrow or raise taxes. Obviously, if there were no such limits, there would be no constraint on how much the government could spend at any point in time.

Congress and the president are the only constraints on federal spending. Unlike your checking account, There are no financial constraints. That is why net spending (spending vs. taxing) has risen to $32 trillion.

Certainly governments are limited in their ability to tax citizens. (That is, the government can’t tax more than 100 percent of income.) But are governments constrained in their ability to borrow?

Monetarily non-sovereign governments are constrained by their full faith and credit, i.e., their credit rating. Monetarily Sovereign governments have no need to borrow, so there is no constraint.

Indeed they are. Informally, the value of government debt outstanding today cannot be more than the value of the government’s resources to pay off the debt.

The U.S. government has the infinite ability to pay for anything. Just ask Fed Chairmen Greenspan and Bernanke.

How do governments pay their current debt obligations? One way is for the government to collect more tax revenue than it spends. In this case, the surplus can be used to pay bondholders.

Wrong. All a federal surplus does is reduce Gross Domestic Product, i.e., cause a recession or depression.

Another way to finance existing debt is to collect seigniorage revenue and use that to pay bondholders.

Half right, half wrong. “Collect seigniorage” is a fancy way to say “print money.”

Seigniorage is the difference between the face value of dollars and the cost of creating them, which comes close to zero. However, holders of U.S. Treasury bonds are paid in two ways: Seigniorage pays the interest, and the principal is paid by returning the bondholder’s deposit.

Finally, the government can borrow more from the public to pay existing debt holders.

Wrong again. The federal government does not borrow, though monetarily non-sovereign governments do borrow.

SUMMARY

It is discouraging to read an article written by the Senior Vice President of Research and Director of the Real-Time Data Research Center for the Federal Reserve that displays so little understanding of Monetarily Sovereign finance.

The article claims that federal finance is similar to personal finance, but it does not demonstrate any knowledge of the vast differences.

Cities, counties, states, businesses, and euro nations can run short of money. The federal government cannot, and a key figure in the Federal Reserve seems to not understand that.

The answer to the title question is, “No, deficits do not cause inflation. Inflation is caused by shortages of key goods and services, most often oil, food, and labor.

Deficit spending can cure inflation by paying for scarce goods and services and ending shortages.

Seems like a simple question — “When will the U.S. government run out of U.S. dollars?”

Sadly, the media writers, economists, and politicians don’t seem to know. Some claim “soon.” Some claim “eventually.” A few say “never.”

Scott Horsley

For instance, Scott Horsley:

Scott Horsley is NPR’s Chief Economics Correspondent. He reports on ups and downs in the national economy as well as fault lines between booming and busting communities.Horsley spent a decade on the White House beat, covering both the Trump and Obama administrations. Before that, he was a San Diego-based business reporter for NPR, covering fast food, gasoline prices, and the California electricity crunch of 2000. He also reported from the Pentagon during the early phases of the wars in Iraq and Afghanistan.Horsley earned a bachelor’s degree from Harvard University and an MBA from San Diego State University.

Mr. Horsley seems to believe the government will run out of money in 2033 or maybe in 2036. I say that because of the article he wrote:

Congress has less than a decade to fix Social Security before the popular program runs short of cash, threatening a sharp cut in benefits for nearly 60 million retirees and family members, according to a government report released Monday.

Social Security (SS) is an agency of the U.S. government. The only two ways SS can run out of dollars are:

If Congress and the President want it to run out, or

If the U.S. government runs out.

Can the government run out of its sovereign currency, which it created from scratch in the 18th century?

For millions of years, there was no U.S., no U.S. laws, and no U.S. dollars. Then suddenly, in the late 1780s, a group of men created a government from thin air.

This government passed laws, also from thin air. Some of the laws created the U.S. dollar, again from thin air.

That government created as many laws as it wished, and those laws created as many dollars as the law-writers wished.

It all was arbitrary.

So, returning to the question, “When will the U.S. government run out of U.S. dollars?”

The report from Social Security trustees predicts the retirement program’s trust fund will be exhausted in November of 2033.

Despit what you repeatedly have been told, it isn’t a trust fund. It’s just a line item in a balance sheet. (See: “The phony trust fund controversy.“) The government can change those numbers to whatever it chooses at any time it chooses.

Congress votes; the President approves; someone presses a computer key; and a one billion dollar “trust fund” instantly becomes a fifty billion dollar “trust fund.”

At that point, benefits would automatically be cut by 21%, unless lawmakers adopt changes before then.

Among the laws the government created were the laws creating Social Security.

As an agency of the government, Social Security is funded the same way as every other agency: Congress votes, and the President approves.

Congress and the President have unlimited freedom to decide how much any agency will receive:

Mandatory spending – funding for Social Security, Medicare, veterans benefits, and other spending required by law. This typically uses over half of all funding. (Congress and the President make the law)

Discretionary spending – federal agency funding. Congress sets funding levels for these each year. This usually accounts for around a third of all funding. (Congress and the President set the levels)

Interest on the debt – this usually uses less than 10 percent of all funding. Congress and the President decide how much interest to pay and tax).

In short, every penny of federal spending ultimately is decided by Congress and the President. It all returns to the fundamental question, “When will the U.S. government run out of U.S. dollars?”

By now, I’m sure you know the answer: The U.S. government cannot unintentionally run short of U.S. dollars.People don’t realize that FICA doesn’t fund Social Security and Medicare and that those trust funds are fictions.

Even if the government had to pay someone a billion, a trillion, or a billion trillion dollars today, it could do so simply by passing a law and pressing a computer key.

Former Federal Reserve Chairman Alan Greenspan:“A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Federal Reserve Chairman Ben Bernanke:“The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Statement from the St. Louis Fed:“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

The answer to the question, “When will the U.S. government run out of U.S. dollars?” is a resounding, NEVER, unless Congress and the President make that arbitrary decision.

You and I are limited in our money supply. Your state, county, and city governments are limited. All businesses are limited. Banks are limited. Even euro nations are limited. All are monetarily non-sovereign.

They were not the original creators of the U.S. dollar.

By contrast, the U.S. government is Monetarily Sovereign. It was the creator of the dollar. It cannot unintentionally run short — not now, not in 2033, not in 2036, not ever.

So why do writers like Scott Horsley think SS and Medicare, agencies of the federal government, will run short?

There’s some good news in the new forecast. Thanks to higher-than-expected worker productivity and a decline in expected disabilities, Social Security isn’t burning through cash as fast as trustees predicted a year ago.

Still, the long-term demographic challenges haven’t gone away.

A growing number of baby boomers are collecting benefits, while there are fewer people in the workforce paying taxes for each retiree.

Given today’s low birthrates, that mismatch is not expected to change for decades, although a surge in immigration helps.

Remember what Ben Bernanke said, “It’s not tax money… We simply use the computer to mark up the size of the account.”

The federal government does not use your tax dollars to fund its spending. You (and Mr. Horsley) may be shocked to learn that every dollar you send to the U.S. Treasury is destroyed upon receipt.

When you pay taxes, the dollars come out of your bank account, where they were part of the “M2 money supply measure.”

When the dollars reach the Treasury, they instantly disappear from M2 and are not found in any money supply measure.

They join the Treasury’s infinite money supply. Adding dollars to infinite dollars still yields infinite dollars.

These dollars, which are not part of any money supply, no longer can be found. They have been destroyed.

Why does the federal government collect taxes if not to fund spending?

To control the economy by taxing what it wishes to discourage and by giving tax breaks to what it wishes to reward.

To assure demand for the U.S. dollar by requiring taxes to be paid in dollars.

To make you believe dollars are limited by taxes, so you will not request benefits. (This doesn’t discourage the rich from requesting and getting tax benefits unavailable to you.)

Proposed FixesCongress could fix the problem by raising taxes that support Social Security, reducing retirement benefits, or some combination of the two. But a politically palatable solution has been elusive.

Mr. Horsley can think of only two fixes: Raise taxes or cut benefits. Both fixes predictably would impact the middle and lower income groups, thereby widening theincome/wealth/power Gapbetween the rich and the rest.

This is exactly what the rich want because the wider the Gap, the richer they are. Increasing your taxes and lowering your benefits makes the rich richer.

And that is precisely what the rich bribe the media, the economists, and the politicians to do.

It’s not that Mr. Horsley himself has been bribed. He may simply be following the “party line” created by others who have been bribed — just going with the flow, and not thinking about the reality that the federal government can’t unintentionally run short of dollars.

“When you see the two major candidates running for president tripping over themselves to promise what they won’t do to fix the problem, you have to worry because those kinds of reforms really start at the top,” says Maya Macguineas, president of the Committee for a Responsible Federal Budget.

Ah, yes, the famous Maya Macguineas, who repeatedly implies that the federal government is running out of dollars — now there is a “reliable” source.

The Biden administration has pledged not to touch Social Security benefits.

“Seniors spent a lifetime working to earn the benefits they receive,” Treasury Secretary Janet Yellen, who leads the trustees, said in a statement.

“We are committed to steps that would protect and strengthen these programs that Americans rely on for a secure retirement.”

Yes, yes, blah, blah, blah. “Committed to steps,” “Protect and strengthen.” And more blah, blah, blah. But what exactly are those steps?

Congressional Democrats have proposed higher taxes on the wealthy to support Social Security.

Congressional Republicans have balked at that, instead calling for reducing the benefit formula and raising the retirement age for younger workers.

The classic Democrat/Republican false choices. The Dems want to soak the rich. The GOP wants to soak the rest of us.

“Those who want to cut Social Security couch it in affordability,” says Nancy Altman, who heads the advocacy group Social Security Works.

“But of course, there’s no question we can afford it. It’s really a question of values. And as polarized as we are, we’re not polarized over this.”

Altman is confident that lawmakers will find a solution before automatic cuts take effect.

“If they didn’t act, not only would they all be voted out of office,” she says. “They couldn’t even remain in Washington. They’d be chased down the street.”

Why aren’t they already being chased? Because the public has been fed so many lies by so many “reliable sources,” the people don’t realize they are being lied to.

On first reading of this post, most people will think, “That can’t be true.” But it’s true.

The federal government could fund a comprehensive, no-deductible Medicare for every man, woman, and child in America and a generous Social Security program for everyone, all without collecting a single penny in taxes.

Yes, there’s no question we can afford it. So? So? AFFORD IT!

But the clock is ticking, and delay has already been costly.

“Every year the trustees warn us we have to make changes and the sooner we make them, the better and easier it will be,” says Macguineas. “And every year we fail to make those changes.”

Medicare and disability solvencyWhile Social Security’s retirement program is in danger of running short of cash, a separate program that supports disabled people appears to be solvent for the long term, trustees said.

Medicare’s finances have also improved somewhat in the last year, thanks to a strong economy and lower-than-expected spending. Still, the program which provides health care for nearly 67 million people, is expected to face its own cash crunch in 2036.

You have been fed lie after lie after lie. Your information sources wring their hands in mock horror that one day soon, the federal government will run short of dollars, perhaps right after the universe runs short of stars and politicians become honest.

Even the densest among us can see the solution: The federal government should pay for Social Security and Medicare, period.Eliminate FICA. It doesn’t fund SS or Medicare. It doesn’t fund anything. Those FICA dollars are destroyed upon receipt.

FICA serves only as a convenient excuse (convenient for the rich) to limit and cut your SS and Medicare benefits, thus widening the income/wealth/power Gap and making the rich richer and you poorer.

In technical terms, that pisses me off, and it should piss you off, too. What are you going to do about it?

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.