From Wikipedia: Ignaz Philipp Semmelweis was a Hungarian physician and scientist who was an early pioneer of antiseptic procedures and was described as the “savior of mothers.” Postpartum infection, also known as puerperal fever or childbed fever, consists of any bacterial infection of the reproductive tract following birth, and in the 19th century was common and often fatal. Semmelweis discovered that the incidence of infection could be drastically reduced by requiring healthcare workers in obstetrical clinics to disinfect their hands. In 1847, he proposed hand washing with chlorinated lime solutions at Vienna General Hospital’s First Obstetrical Clinic, where doctors’ wards had three times the mortality of midwives’ wards. The maternal mortality rate dropped from 18% to less than 2%, and he published a book of his findings, Etiology, Concept and Prophylaxis of Childbed Fever, in 1861. Despite his research, Semmelweis’s observations conflicted with the established scientific and medical opinions of the time, and his ideas were rejected by the medical community. He could offer no theoretical explanation for his findings of reduced mortality due to hand-washing, and some doctors were offended at the suggestion that they should wash their hands and mocked him for it. In 1865, the increasingly outspoken Semmelweis allegedly suffered a nervous breakdown and was committed to an asylum by his colleagues. In the asylum, he was beaten by the guards. He died 14 days later from a gangrenous wound on his right hand that may have been caused by the beating.I hope I won’t be similarly confined because, for 25 years, I have struggled to explain what seems to me to be the simple concepts of Monetary Sovereignty. The question: Is Monetary Sovereignty so simple, so obvious, that you believe “it can’t be that easy‘? (It is.) Or, “if it were that simple, someone else would have thought of it.” (Others have.) Or, “that’s not what schools, economists, and the media teach.” (That’s the problem.) Here are three simple facts about our economy. 1. Money is not a physical thing. Gold, silver, and paper are not money, but they can represent money.

A dollar bill is a title to a dollar, not a dollar itself. All forms of money merely are bookkeeping entries. For example, a $10 gold coin is just a title to $10. The coin always is worth exactly $10 as money, though it may be worth thousands as barter. As money, that gold coin is worth neither more nor less than a $10 paper bill or the $10 on your checking account bank statement. Thus, money is just government-approved numbers on a statement. The U.S. government has the infinite ability to create these bookkeeping entries simply by pressing computer keys. 2. A government having the infinite ability to create, spend, and control a specific currency is sovereign over that money and it is called “Monetarily Sovereign.” The governments of the U.S., Japan, the UK, Canada, and Australia are examples of Monetary Sovereignty over their respective currencies.These three fundamentals seem simple and straightforward. Yet, for perhaps 25 years, I have failed to help most people understand them. #1 confuses those who mistakenly believe the pieces of green-printed paper in their wallet are actual dollars, not just titles to dollars. #2 is vaguely understood except by all those who believe federal finances are the same as personal finances.. #3 is denied outright by those whose vision of supply and demand makes them believe excessive demand caused inflation rather than a lack of supply. To help people understand, I have given examples of the Monopoly game, which can be played without physical paper “money”—just a balance sheet—and that, by rule, the Bank (a corollary for the federal government) cannot run short of money. I have presented graphs demonstrating how inflations are closely related to oil costs, not to federal spending. I have presented graphs showing that recessions occur immediately after reductions in federal deficit spending growth and are cured by increased federal deficit spending growth. I have shown that every depression in U.S. history has come shortly after the federal government reduced deficit spending.Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

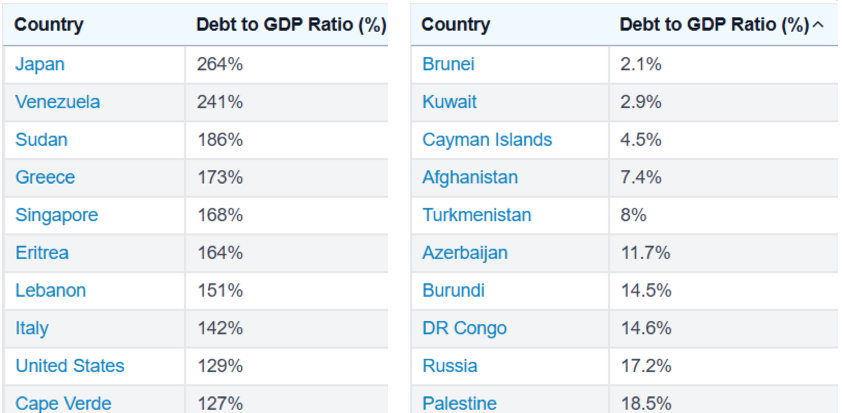

The governments of Italy, France, Germany, and Greece are monetarily non-sovereign. They do not have their own sovereign currencies. Instead, they use the euro, over which the European Union (EU) is sovereign. These nations can run short of euros, while the EU cannot. The nations rely on taxes; the EU needs no taxes. The Monetarily Sovereign U.S. government cannot unintentionally run short of its money. Given a creditor’s demand for a million, or a billion, or a trillion trillion dollars, the U.S. government could pay immediately, without collecting a single penny in taxes. What does that tell you about federal debt? Just as the U.S, cannot unintentionally run short of dollars, the EU cannot run short of euros. Contrast with any monetarily non-sovereign entities — euro nations, businesses or people — which do not have the infinite ability to pay bills and can run short of whatever currency they are using. 3. Government spending of its Monetarily Sovereign currency is not inflationary. Historically, all inflation is supply-based — i.e, shortage(s) of critical assets, usually oil and/or food — not demand-based. While government spending can increase demand for specific products, this doesn’t cause inflation, which is an overall increase in the prices of almost all products.

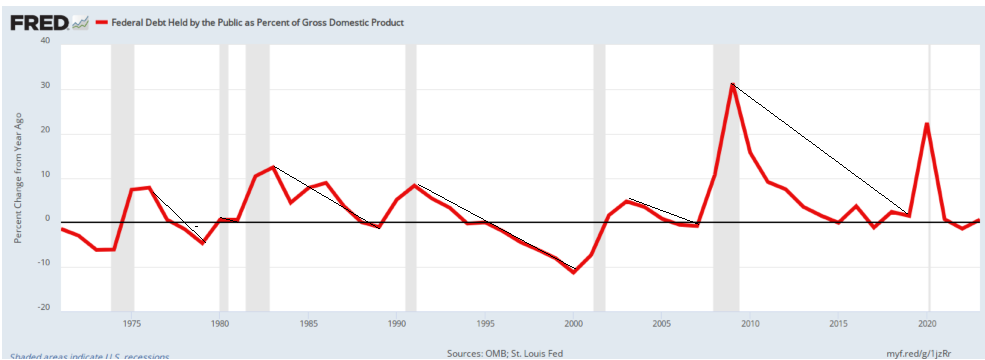

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

I have published articles by thought leaders from 1940 to today who falsely claimed that the federal debt is a ticking time bomb. During those 84 years, the debt grew from $40 billion to $30 trillion, yet this so-called “debt bomb” never exploded. I encounter articles daily discussing the dangers of federal debt and deficits. Currently, Congress is struggling with the absurd federal debt limit, which ignores the government’s unlimited capacity to meet its financial obligations. Even this morning, I read again about how federal agencies like Social Security and Medicare are in danger of running short of money, though Congress could supply all the funds needed just by voting. Every day, dollars are deducted unnecessarily from paychecks to “pay for ” some federal expense when, in fact, federal taxes pay for nothing. The federal government already has infinite dollars. Think. With infinite dollars, why would it need taxes? A simple question with a simple answer, yet most people are stumped by itThe sole purposes of federal taxes are:

1. To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward and

2. To assure demand for the dollar by requiring taxes to be paid in dollars.

3. To help the rich become more affluent by providing tax breaks not available to the rest of us.

The wealthy promote the idea of “small government,” not because they genuinely believe the unfounded claim that “government is the problem,” but because they recognize that government establishes regulations they prefer to avoid. These regulations regarding clean air, clean water, food safety, and fair treatment by banks and businesses hinder the wealthy’s relentless pursuit of power and wealth, often at the expense of the rest of society. Most Congresspeople understand all these points but continue disseminating disinformation for political reasons. (Wealthy political donors pay a lower percentage of their incomes than the rest of us, so useless tax collections widen the Gap between the rich and us. The Gap makes them rich; we all would be the same without it.) Sadly, while the rich don’t want us to understand, most of us blindly follow their lead, just as the unfortunate pregnant women followed the fatal lead of mid-19th century doctors. Through the years, I have provided examples, data, and proofs. At the same time, again, some disingenuous Congressperson, deceptive economist, misleading writer, or uninformed friend assures you that Social Security and Medicare will become insolvent without tax increases or benefit cuts. Monetary Sovereignty is not complicated. It’s not, as they say, “rocket science.” It’s dead simple. However, I do not know how to help the populace understand what will benefit them. Consider the suggestion: “Eliminate FICA.” Is that too difficult to contemplate, or is it too easy to believe? What is the psychology of the millions who cannot accept the often-proven fact that the federal government has infinite money while accepting the never-proven nonsense that a Presidential election was stolen? Would you be outraged if your local car dealer tried to overcharge you or if your favorite football team refused to honor your tickets? Where is your passion against paying thousands of dollars in unnecessary taxes? Where is your anger about billionaire Trump paying far less taxes (almost nothing, actually) than you do? Why aren’t you frothing at the mouth about your doctor bills when the federal government could and should fund comprehensive, no-deductible Medicare for every man, woman, and child in America without collecting a penny in taxes? Why aren’t you screaming on the phone about proposed cuts to Social Security? If you heard about a billionaire who refuses to give his infant child enough money for medical care, would you be outraged? Well, the government is a multiple trillionaire, and you are its child. Get outraged. If I can’t convince people to make meager efforts to contact their Congresspeople about something that will save them many thousands of dollars and their health, improve their lives and their children’s lives, all at no cost, what is the purpose of reason? You’ve gone through the effort of reading this far. Why not make it meaningful? Call your Senator and Representative. Today. Now. “Why not” is the puzzle. Rodger Malcolm Mitchell Monetary Sovereignty Twitter: @rodgermitchell Search #monetarysovereignty Facebook: Rodger Malcolm Mitchell; MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell; https://www.academia.edu/……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY