When my wife died, I decided I didn’t need two homes, so I gave my Illinois home to my children and moved permanently to Florida.

Because we don’t have snow and ice, the weather here generally is more accommodating for us elderly than up north, though the occasional hurricane can be stressful.

An article in the South Florida Sun Sentinel describes a growing problem- local and national. Here are some excerpts:

As South Florida’s seniors grow older, experts warn of the ‘silver tsunami’ financial crisis By Lisa J. Huriash | lhuriash@sunsentinel.com, November 18, 2024 Aging experts unveiled a grim outlook for aging seniors who increasingly are impoverished and dependent on government help to get by. And in South Florida, they say the numbers are reaching more of a crisis level as the number of seniors grow, often with no pensions and not enough savings — relying instead on Social Security benefits. “If you aren’t being kept up at night by the impending ‘silver tsunami,’ then you aren’t paying attention,” declared Broward County Commissioner Steve Geller, who is also the chair of the South Florida Regional Planning Council.

Also, keep in mind the tsunami of misinformation and disinformation regarding the so-called “impending insolvency” of Social Security and Medicare, the two main federal benefits received by the elderly.

Commonly referred to as the “silver tsunami,” residents age 65 and older are projected to number more than 2.13 million in the seven-county region by 2050, reflecting an increase of 54.5% since 2021, according to the Planning Council.

While the article discusses South Florida, the situation is nationwide.

The U.S. population of 65 and older has grown significantly over the past decade.

From 2010 to 2020, this age group increased by 38.6%, from 40.3 million to 55.8 million, the fastest growth rate since 1880 to 1890.

Over the past decade, the increase of 15.5 million people in this age group is the largest-ever 10-year numeric gain. This rapid growth is largely driven by the aging of the Baby Boomer generation (those born between 1946 and 1964), who began turning 65 in 2011.

Of these residents, 520,000 will be 85 years of age or older, reflecting a projected increase of 133.6% from 2025 to 2050. A conference about “preparing for the silver tsunami” was held Friday at Florida Atlantic University in Boca Raton, presented by the South Florida and Treasure Coast Regional Planning Councils. There, experts shared what the future could look like, using figures from the U.S. Census, and studies by state agencies, the Federal Reserve Bank, and more:

— By 2034, Americans ages 65 and older will outnumber those 18 and younger for the first time.

— Nearly half of elderly unmarried women rely on Social Security for 90% of their income, compared to 22% of all seniors.

— Older Americans are carrying more debt into retirement.

— The age-85-and-older population in southeast Florida will more than double in 25 years, which means the need for more elder care.

— The median income for American adults is $50,290 while their average annual expenses are $57,818.

Social Security

The average monthly Social Security benefit is $1,907, or $22,884 a year. “There is a disconnect of how much people understand they have to save,” said Angela Antonelli, a research professor and executive director of the Georgetown University Center for Retirement Initiatives. One in five Americans rely on Social Security for 90% or more of their income, she said. “Social Security does not keep you out of poverty,” she said.

Social Security could and should keep you out of poverty. There is no excuse for a Monetarily Sovereign nation, with the infinite ability to create dollars, to allow its elderly citizens to fall into poverty.

Affordability is not a factor for a Monetarily Sovereign government. Even without collecting a penny in taxes, the federal government could fund a generous version of Social Security, which would keep you out of poverty. So why not?

On Friday, experts urged policymakers to use the information to try to think of ways to create change when it comes to crucial areas of health care, transportation, housing and finances.Nan Rich, a panelist, said “right now we have a crisis in our community when it comes to seniors,” especially as the condos they purchased in the 1970s now are in need of expensive repairs and maintenance.

Pallet shelters. Are these little boxes the solutions for your Grandma? Is this the best America can do for its elderly? “Pray it doesn’t rain, granny.”

Florida is monetarily non-sovereign. Unlike the U.S. federal government, Florida cannot create infinite money. It would need to levy taxes to fund senior healthcare, transportation, housing, and finances.

The federal government, by contrast, could and should do it without taxes.

There is also an expectation that more seniors are facing being homeless, and Rich said she’s trying to make headway there, too: The county is expected to soon make a decision on whether to build Pallet shelters, tiny transitional houses for the homeless. Miami-Dade County has nearly half a million residents age 65 and older. But poverty is the highest for seniors than any other age group, said Tyler Moroles, assistant division director of the Section 8 Housing Choice Voucher Program for Miami-Dade. While housing is expensive for everyone — the median rent is $2,100 which requires a salary of $75,600 to be affordable — it’s nearly impossible for the thousands of seniors in public housing. The average senior income there is $14,691 a year. The county is now redeveloping 1,800 public housing units to create more living spaces. This year, 137,000 applicants have applied for housing vouchers, he said, and only 5,000 of those were chosen. “It’s a national issue, we’re trying to deal with it,”he said.

There is no good reason why the states are left to deal with national issues where the fedeal government’s money provides a solution.

Among the issues that the experts pondered: What changes does government need to prepare for, such as “granny flats” to allow housing additions so multiple generations can live together “to encourage senior-friendly housing” and allow seniors to age in place.

“Senior friendly” Pallet shelters? Really? Is that where you would like t0 spend your remaining days?

Health careThere is a national shortage of 30,000 geriatricians, said Dr. Naushira Pandya, the chair of Geriatrics at NSU. “There will never be enough geriatricians for what we need,” she said. “The need is really great.” It’s an “intellectual challenge” to treat the host of medical issues, but it doesn’t get the same level of enthusiasm as other medical fields, she said.

Becoming a geriatrician requires 12-14 years of college and $200,000 – $350,00 in tuition, including undergraduate and medical school tuition, plus living expenses during residency and fellowship.

While the government may be unable to give you back the years, it can undoubtedly underwrite the costs.

That panel conversation sparked an idea to attract more doctors to specialize in geriatrics by state Sen. Gayle Harrell, R-Stuart, who noted how this year’s “Live Healthy” legislation assists in loan repaymentsfor doctors who work in underserved areas.

What a concept! Put them deeply in debt and then force them to work in low-remuneration areas, so paying off the debt will be especially difficult.

How about this: No loans. Have the federal government pay their all their expenses, and give them a supplemental salary if they work in “underserved areas.”

Transportation“Most adults will outlive their ability to drive by seven to 10 years,” warned panelist Laura Streed, the senior associate state director of AARP of Florida. Chris Stephenson, the transportation mobility director of the Senior Resource Association in Indian River County, which provides services including Meals on Wheels and adult day care: “Isolation can have profound health consequences. Yet if seniors don’t have adequate transportation they are homebound.}He shared a popular program in Palm Beach County that has adapted “to meet the needs of our senior population.” It uses Uber and other ride-sharing companies “to fill the gaps” to get seniors to public transit stations, which might be too far to reach by walking. Karen Deigl, president and CEO of Senior Resource Association urged policy makers to enhance public transit by creating routes that connect to neighboring counties, make transit accessible with wheelchair lifts and low floors, and a voice that calls out each stop, and allow same-day trip requests. Because “some people just shouldn’t drive,” she said. Lisa J. Huriash can be reached at lhuriash@sunsentinel.com. Follow on X, formerly Twitter, @LisaHuriash

CONCLUSION

The population is aging which leads to multiple problems. Many possible solutions have been proposed, almost all of which involve funding.

The federal government, being Monetarily Sovereign, has the infinite ability to fund anything without collecting taxes.

Strangely, the resistance to “big government” seems not to extend to big state and local government—just big federal government—though the federal government is the one entity that easily can fund all the solutions without burdening taxpayers.

Even more strangely, the resistance to” big government” comes primarily from the party that elevated a dictator wanna-be to the Presidency.

Go figure.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell;MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell; https://www.academia.edu/

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

South Florida leaders want to head off ‘silver tsunami’ aging crisis

By Lisa J. Huriash || South Florida Sun Sentinel UPDATED: July 17, 2024

Lisa J. Huriash

Broward County said it is aggressively encouraging construction — and helping fund — affordable housing for seniors.

South Florida leaders are urging a state planning council to tackle the impending “silver tsunami” as concerns grow for retirees’ well-being as they age.

At a recent meeting of the South Florida Regional Planning Council, chairman Steve Geller, who is also a Broward County commissioner, said he would push for aging issues to be discussed at a broader conference this fall where experts could guide policy suggestions.

The conference will include Palm Beach, St. Lucie, Monroe, Broward, Miami-Dade, Martin and Indian River counties, which is about one-quarter of the state’s population.

“Concerns are growing” among Florida leaders who will “push for” discussion of aging issues and to “address” and “tackle” the financial problems of one-quarter of the state’s population. No word yet about the three-quarters.

With all that pushing, addressing, tackling, and concern, we can be confident that our elderly will be well taken care of. Not.

Geller said more attention is needed to deal with the anticipated wave of older Americans who are facing retirement without a pension like their parents relied on, and face unique transportation and healthcare problems as they age.

And the above-mentioned housing problem.

The median personal income for people age 65 and older is $29,740, according to the federal Administration for Community Living.

Imagine trying to survive on $29,740 a year. And that’s the median, meaning half the seniors are trying to survive on less, much less.

“I don’t think we are prepared for it,” Geller said after the meeting.

That was the understatement of the decade.

Meeting the transportation needs of an aging population, including new signage, changing paratransit to add low floors and improved audio and visual announcements, more community shuttles and vans, and “safe transitioning” for seniors to stop driving.

It’s good to meet the “transportation needs” of the elderly. Action should be taken immediately.

Geller also said there could be a consideration to create crosswalks that give seniors more time to get across the street.

Yes, crosswalks that give the elderly more time to cross are good. Now, let’s get to the biggest problems.

The costs of long-term care average more than $100 per day nationwide for a four-hour daily home health aide.

What about the elderly who need more than four hours of care?

Yet “the majority of older adults will need these services, and those with meager incomes, who are most likely to require them, have the fewest resources to pay for them,” according to a November study by the Harvard Joint Center for Housing Studies.

According to the report, about 85% of seniors age 75 and older in Miami-Dade and Broward who live alone cannot afford daily home care in addition to housing and other necessities.

Former Fed Chairman Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Think about it. You work your whole life, and then, in your senior years, you live in misery. That is America. Of course, it’s unnecessary, but you wouldn’t think so if you look at the excuses for not helping these senior citizens.

While Ms. Huriash is right to be concerned about the monetarily non-sovereign Broward County’s ability to fund support for seniors, the entire problem could be solved via Monetarily Sovereignfederal funding.

The federal government could fund all the solutions by pressing a few computer keys but fails to do so. Here are examples of the phony excuses the ignorant and/or lying con artists shovel on you:

Too many beneficiaries and supported by too few taxpayers: The U.S. population is aging rapidly, leading to more beneficiaries than the working population contributing to the funds.

Trust Fund Depletion: The Social Security Old-Age and Survivors Insurance (OASI) Trust Fund is projected to be able to pay 100% of scheduled benefits until 2033. After that, it will only be able to cover about 79% of benefits unless changes are made.

Rising Hospital Costs: The Hospital Insurance (HI) Trust Fund, which funds Medicare Part A, is projected to be able to pay 100% of benefits until 2036. After that, it will only cover about 89% of benefits.

Rising Healthcare Costs: The Supplemental Medical Insurance (SMI) Trust Fund, which covers Medicare Parts B and D, is adequately financed but faces rapidly rising costs, increasing the financial burden on beneficiaries and taxpayers.

Former Fed Chairman Ben Bernanke: “The U.S. government (can) produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.:

Excuse #1. Too many beneficiaries and supported by too few taxpayers.

Two huge lies were packed into one short sentence. The working population pays FICA taxes, but FICA taxes don’t fund anything.

Your tax dollars come from the “M2 money supply measure,” and when they reach the Treasury, they cease to be part of any money supply measure.

They disappear from the economy and effectively are destroyed.

The Treasury keeps a record of the dollars it receives, but it neither needs nor uses those dollars.

Even if it didn’t receive a single dollar, the federal government has the infinite ability to create dollars to support an infinite number of beneficiaries.

In summary, federal taxes and taxpayers do not fund federal spending, and we don’t have too many beneficiaries

Excuse #2. Trust fund depletion.

The Social Security Old-Age and Survivors Insurance (OASI) Trust Fund is not a trust fund, and it doesn’t pay for anything.

A federal trust fund is nothing more than an accounting mechanism used by the federal government to track earmarked receipts (money designated for a specific purpose or program) and corresponding expenditures.

It’s just a record-keeping device, not a funding source.

The largest and best-known trust funds supposedly finance Social Security, portions of Medicare, highways and mass transit, and pensions for government employees.

Federal trust funds bear little resemblance to their private-sector counterparts, and therefore the name can be misleading.

“Sorry. This pail is empty. I can’t give you any water.”

A “trust fund” implies a secure source of funding.However, a federal trust fund is simply an accounting mechanism that tracks inflows and outflows for specific programs.

In private-sector trust funds, receipts are deposited, and assets are held and invested by trustees on behalf of the stated beneficiaries.

In federal trust funds, the federal government does not set aside the receipts or invest them in private assets.

Rather, the receipts are recorded as accounting credits in the trust funds and then combined with other receipts that the Treasury collects and spends.

Further, the federal government owns the accounts and can, by changing the law, unilaterally alter their purposes and raise or lower collections and expenditures.

Emphasis: The federal government canunilaterally alter the (trust funds’) purposes and raise or lower collections and expenditures.

When you are told that a federal trust fund will run out of money on a certain date, that means Congress could easily increase the balance to match future spending simply by deciding to do so, but so far, it hasn’t.

The federal government could (and should) increase the balance of any trust fund by trillions of dollars merely by passing a law without collecting a dollar in taxes.

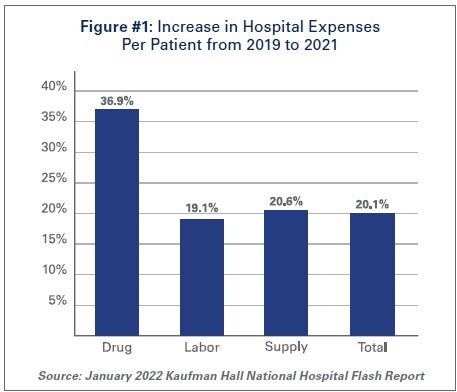

Excuse #3 and #4. Rising hospital and healthcare costs

Hospitals and health systems have repeatedly confronted a range of financial and operational challenges, including historic volume and revenue losses, as well as skyrocketing expenses.

When coupled with rising inflation and growth in input prices, these expense increases have been severely detrimental to hospital finances, leading to billions in losses and over 33% of hospitals operating on negative margins.

Throughout the pandemic, Congress has provided various forms of support and resources to hospitals to help them manage the increased demands and financial pressures.

Here are some key resources and support measures:

Financial Support

Provider Relief Fund:Established under the CARES Act, this fund provided financial assistance to healthcare providers to compensate for revenue losses and increased costs due to the pandemic.

Paycheck Protection Program (PPP): This program offered loans to healthcare providers to help them retain employees and cover operational costs.

Increased Medicare Payments: Congress increased Medicare payments for inpatient COVID-19 admissions by 20% and provided additional payments for administering COVID-19 vaccines.

Resources for COVID-19 Response

Vaccines and Treatment: Funding was allocated for the development, distribution, and administration of COVID-19 vaccines and treatments.

Personal Protective Equipment (PPE): Resources were provided to ensure hospitals had adequate PPE for their staff3. Testing and Contact Tracing: Additional funding was directed towards expanding testing capabilities and contact tracing efforts.

Support for Rural Hospitals

Rural Health Care Providers: The American Rescue Plan Act included $8.5 billion to reimburse rural healthcare providers for expenses and lost revenues related to COVID-19.

Workforce Development

Workforce Support: Funding was provided for workforce development to ensure hospitals had the necessary staff to handle the increased patient load.

Congress and the President voted for trillions of dollars in support, some in loans and some in outright support. None was matched by increased taxes. The federal government simply did what it always does: It passed laws that created the money from thin air.

The federal government has the infinite ability to pass such laws.

Excuse #5. Politics

Here’s where the real lying comes into play. You are being told that solving all these problems requires raising taxes, cutting benefits, or increasing the retirement age.

It is an absolute lie whose purpose is to widen the income/wealth/power Gap between the rich and the rest of us. The lie is told at the behest of the rich, who become richer when the Gap widens.

The federal government is Monetarily Sovereign. It has the infinite ability to create U.S. dollars for any purpose. It does not need to collect taxes to fund anything, and it certainly does not need to borrow dollars, cut benefits, or increase the retirement age.

Federal taxation has two purposes, neither of which is to fund federal spending:

To control the economy by taxing what the government wishes to restrict and by giving tax breaks to what the government wishes to reward. (Currently, the government wishes to reward the rich by giving them tax breaks that are not available to the rest of us.)

To guarantee demand for the U.S. dollar by requiring taxes to be paid in dollars.

If you are old, or expect to be, don’t bother asking the federal government for help. They will lie to you.

They will tell you they can’t afford to give you comprehensive, no-deductible, completely free Medicare, nor can they give it to your spouse and children.

A lie.

They will tell you there are too many people asking for too much money.

A lie.

They will tell you that because doctor, nursing, hospital, drug, service, and equipment costs have risen, there is not enough money left in trust funds to care for the elderly, let alone younger Americans.

A lie.

They will tell you the only way to “save” existing Medicare is to raise your taxes and/or to cut your benefits.

A lie.

These are all lies on behalf of the rich, who want to widen the income/wealth/power Gap below them.

They bribe the politiciansvia campaign contributions and promises of lucrative employment opportunities.

They bribe the media via ownership and advertising dollars.

They bribe the economists via university endowments and employment in “think tanks.”

They do everything possible to brainwash you into believing federal finances are like personal finances when the two are polar opposites. The false comparison is called the Big Lie in economics.

As you read this prediction, keep in mind it came twenty-three years ago.

“We have to live within our means. We have to reduce our deficit, and we have to get back on a path that will allow us to pay down our debt. And we have to do it in a way that protects the recovery, protects the investments we need to grow, create jobs, and helps us win the future.

“Even after our economy recovers, our government will still be on track to spend more money than it takes in throughout this decade and beyond. That means we’ll have to keep borrowing more from countries like China.

“That means more of your tax dollars each year will go towards paying off the interest on all the loans that we keep taking out. By the end of this decade, the interest that we owe on our debt could rise to nearly $1 trillion.

“By 2025, the amount of taxes we currently pay will only be enough to finance our health care programs — Medicare and Medicaid — Social Security, and the interest we owe on our debt. That’s it. Every other national priority -– education, transportation, even our national security -– will have to be paid for with borrowed money.

“Now, ultimately, all this rising debt will cost us jobs and damage our economy. It will prevent us from making the investments we need to win the future. “

“We won’t be able to afford good schools, new research, or the repair of roads -– all the things that create new jobs and businesses here in America.

“Businesses will be less likely to invest and open shop in a country that seems unwilling or unable to balance its books. “And if our creditors start worrying that we may be unable to pay back our debts, that could drive up interest rates for everybody who borrows money -– making it harder for businesses to expand and hire, or families to take out a mortgage.

“Around two-thirds of our budget — two-thirds — is spent on Medicare, Medicaid, Social Security, and national security. Two-thirds. Programs like unemployment insurance, student loans, veterans’ benefits, and tax credits for working families take up another 20 percent.

“What’s left, after interest on the debt, is just 12 percent for everything else.”

That is the doom and gloom Obama fed you then; it’s the same diet of liesyou’ve been fed since 1940; and it’s the same utter nonsense you’ll hear today and tomorrow.

It’s the same lies you’ll be told every time the ridiculous, unnecessary “debt ceiling” comes up for debate — you know, the nonsense that paralyzes Congress every few months and is resolved simply by raising the ceiling withno adverse aftereffects.

(Since it already has been raised more than a hundred times, why not just get rid of it? Congress has been bribed to posture about lies.)

And now, thirteen years later, none of Obama’s predictions have come true. Why? Because they all were lies.

Every single time we have paid down the so-called “debt,” we have had recessions and depressions—not some of the time, butevery time.

The rich want you to believe the government can’t afford Medicare, Medicaid, Social Security, unemployment insurance, student loans, veterans’ benefits, and tax credits for working families.

Of course, nothing is said about the costs of those tax breaks for the richthat allowed a billionaire like Donald Trump to pay less income tax than did for the past ten years.

The rich want those cuts expanded. Trump has promised to expand them if he is elected. The rich are happy that Trump’s poor suckers will vote for his tax cuts.

It’s nice that so many people have written to me expressing outrage at the Big Lie. I appreciate your sentiments. But really, folks, I’m already in your corner and have been for twenty-five-plus years. And I’m pushing 90, so if you think Trump and Biden are too old, well . . .

If you want to make a difference, direct your outrage at someone who can do something about it. The politicians, the media, and the university economists.

Call them. Scream at them. Do it again, and again, and again. Every day. Twice a day. Never let up. Let them know you aren’t fooled.

Get your friends involved—and their friends, and theirs. Start a “Truth Club.” Bombard the information sources with truth bombs.

If you do nothing, nothing will happen. The lies will continue. The rich will grow richer. And years from now you will . . . As the poet Thoreau said, “The mass of men lead lives of quiet desperation.”