South Florida leaders want to head off ‘silver tsunami’ aging crisis

By Lisa J. Huriash || South Florida Sun Sentinel UPDATED: July 17, 2024

Lisa J. Huriash

Broward County said it is aggressively encouraging construction — and helping fund — affordable housing for seniors.

South Florida leaders are urging a state planning council to tackle the impending “silver tsunami” as concerns grow for retirees’ well-being as they age.

At a recent meeting of the South Florida Regional Planning Council, chairman Steve Geller, who is also a Broward County commissioner, said he would push for aging issues to be discussed at a broader conference this fall where experts could guide policy suggestions.

The conference will include Palm Beach, St. Lucie, Monroe, Broward, Miami-Dade, Martin and Indian River counties, which is about one-quarter of the state’s population.

“Concerns are growing” among Florida leaders who will “push for” discussion of aging issues and to “address” and “tackle” the financial problems of one-quarter of the state’s population. No word yet about the three-quarters.

With all that pushing, addressing, tackling, and concern, we can be confident that our elderly will be well taken care of. Not.

Geller said more attention is needed to deal with the anticipated wave of older Americans who are facing retirement without a pension like their parents relied on, and face unique transportation and healthcare problems as they age.

And the above-mentioned housing problem.

The median personal income for people age 65 and older is $29,740, according to the federal Administration for Community Living.

Imagine trying to survive on $29,740 a year. And that’s the median, meaning half the seniors are trying to survive on less, much less.

“I don’t think we are prepared for it,” Geller said after the meeting.

That was the understatement of the decade.

Meeting the transportation needs of an aging population, including new signage, changing paratransit to add low floors and improved audio and visual announcements, more community shuttles and vans, and “safe transitioning” for seniors to stop driving.

It’s good to meet the “transportation needs” of the elderly. Action should be taken immediately.

Geller also said there could be a consideration to create crosswalks that give seniors more time to get across the street.

Yes, crosswalks that give the elderly more time to cross are good. Now, let’s get to the biggest problems.

The costs of long-term care average more than $100 per day nationwide for a four-hour daily home health aide.

What about the elderly who need more than four hours of care?

Yet “the majority of older adults will need these services, and those with meager incomes, who are most likely to require them, have the fewest resources to pay for them,” according to a November study by the Harvard Joint Center for Housing Studies.

According to the report, about 85% of seniors age 75 and older in Miami-Dade and Broward who live alone cannot afford daily home care in addition to housing and other necessities.

Former Fed Chairman Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Think about it. You work your whole life, and then, in your senior years, you live in misery. That is America. Of course, it’s unnecessary, but you wouldn’t think so if you look at the excuses for not helping these senior citizens.

While Ms. Huriash is right to be concerned about the monetarily non-sovereign Broward County’s ability to fund support for seniors, the entire problem could be solved via Monetarily Sovereignfederal funding.

The federal government could fund all the solutions by pressing a few computer keys but fails to do so. Here are examples of the phony excuses the ignorant and/or lying con artists shovel on you:

Too many beneficiaries and supported by too few taxpayers: The U.S. population is aging rapidly, leading to more beneficiaries than the working population contributing to the funds.

Trust Fund Depletion: The Social Security Old-Age and Survivors Insurance (OASI) Trust Fund is projected to be able to pay 100% of scheduled benefits until 2033. After that, it will only be able to cover about 79% of benefits unless changes are made.

Rising Hospital Costs: The Hospital Insurance (HI) Trust Fund, which funds Medicare Part A, is projected to be able to pay 100% of benefits until 2036. After that, it will only cover about 89% of benefits.

Rising Healthcare Costs: The Supplemental Medical Insurance (SMI) Trust Fund, which covers Medicare Parts B and D, is adequately financed but faces rapidly rising costs, increasing the financial burden on beneficiaries and taxpayers.

Former Fed Chairman Ben Bernanke: “The U.S. government (can) produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.:

Excuse #1. Too many beneficiaries and supported by too few taxpayers.

Two huge lies were packed into one short sentence. The working population pays FICA taxes, but FICA taxes don’t fund anything.

Your tax dollars come from the “M2 money supply measure,” and when they reach the Treasury, they cease to be part of any money supply measure.

They disappear from the economy and effectively are destroyed.

The Treasury keeps a record of the dollars it receives, but it neither needs nor uses those dollars.

Even if it didn’t receive a single dollar, the federal government has the infinite ability to create dollars to support an infinite number of beneficiaries.

In summary, federal taxes and taxpayers do not fund federal spending, and we don’t have too many beneficiaries

Excuse #2. Trust fund depletion.

The Social Security Old-Age and Survivors Insurance (OASI) Trust Fund is not a trust fund, and it doesn’t pay for anything.

A federal trust fund is nothing more than an accounting mechanism used by the federal government to track earmarked receipts (money designated for a specific purpose or program) and corresponding expenditures.

It’s just a record-keeping device, not a funding source.

The largest and best-known trust funds supposedly finance Social Security, portions of Medicare, highways and mass transit, and pensions for government employees.

Federal trust funds bear little resemblance to their private-sector counterparts, and therefore the name can be misleading.

“Sorry. This pail is empty. I can’t give you any water.”

A “trust fund” implies a secure source of funding.However, a federal trust fund is simply an accounting mechanism that tracks inflows and outflows for specific programs.

In private-sector trust funds, receipts are deposited, and assets are held and invested by trustees on behalf of the stated beneficiaries.

In federal trust funds, the federal government does not set aside the receipts or invest them in private assets.

Rather, the receipts are recorded as accounting credits in the trust funds and then combined with other receipts that the Treasury collects and spends.

Further, the federal government owns the accounts and can, by changing the law, unilaterally alter their purposes and raise or lower collections and expenditures.

Emphasis: The federal government canunilaterally alter the (trust funds’) purposes and raise or lower collections and expenditures.

When you are told that a federal trust fund will run out of money on a certain date, that means Congress could easily increase the balance to match future spending simply by deciding to do so, but so far, it hasn’t.

The federal government could (and should) increase the balance of any trust fund by trillions of dollars merely by passing a law without collecting a dollar in taxes.

Excuse #3 and #4. Rising hospital and healthcare costs

Hospitals and health systems have repeatedly confronted a range of financial and operational challenges, including historic volume and revenue losses, as well as skyrocketing expenses.

When coupled with rising inflation and growth in input prices, these expense increases have been severely detrimental to hospital finances, leading to billions in losses and over 33% of hospitals operating on negative margins.

Throughout the pandemic, Congress has provided various forms of support and resources to hospitals to help them manage the increased demands and financial pressures.

Here are some key resources and support measures:

Financial Support

Provider Relief Fund:Established under the CARES Act, this fund provided financial assistance to healthcare providers to compensate for revenue losses and increased costs due to the pandemic.

Paycheck Protection Program (PPP): This program offered loans to healthcare providers to help them retain employees and cover operational costs.

Increased Medicare Payments: Congress increased Medicare payments for inpatient COVID-19 admissions by 20% and provided additional payments for administering COVID-19 vaccines.

Resources for COVID-19 Response

Vaccines and Treatment: Funding was allocated for the development, distribution, and administration of COVID-19 vaccines and treatments.

Personal Protective Equipment (PPE): Resources were provided to ensure hospitals had adequate PPE for their staff3. Testing and Contact Tracing: Additional funding was directed towards expanding testing capabilities and contact tracing efforts.

Support for Rural Hospitals

Rural Health Care Providers: The American Rescue Plan Act included $8.5 billion to reimburse rural healthcare providers for expenses and lost revenues related to COVID-19.

Workforce Development

Workforce Support: Funding was provided for workforce development to ensure hospitals had the necessary staff to handle the increased patient load.

Congress and the President voted for trillions of dollars in support, some in loans and some in outright support. None was matched by increased taxes. The federal government simply did what it always does: It passed laws that created the money from thin air.

The federal government has the infinite ability to pass such laws.

Excuse #5. Politics

Here’s where the real lying comes into play. You are being told that solving all these problems requires raising taxes, cutting benefits, or increasing the retirement age.

It is an absolute lie whose purpose is to widen the income/wealth/power Gap between the rich and the rest of us. The lie is told at the behest of the rich, who become richer when the Gap widens.

The federal government is Monetarily Sovereign. It has the infinite ability to create U.S. dollars for any purpose. It does not need to collect taxes to fund anything, and it certainly does not need to borrow dollars, cut benefits, or increase the retirement age.

Federal taxation has two purposes, neither of which is to fund federal spending:

To control the economy by taxing what the government wishes to restrict and by giving tax breaks to what the government wishes to reward. (Currently, the government wishes to reward the rich by giving them tax breaks that are not available to the rest of us.)

To guarantee demand for the U.S. dollar by requiring taxes to be paid in dollars.

If you are old, or expect to be, don’t bother asking the federal government for help. They will lie to you.

They will tell you they can’t afford to give you comprehensive, no-deductible, completely free Medicare, nor can they give it to your spouse and children.

A lie.

They will tell you there are too many people asking for too much money.

A lie.

They will tell you that because doctor, nursing, hospital, drug, service, and equipment costs have risen, there is not enough money left in trust funds to care for the elderly, let alone younger Americans.

A lie.

They will tell you the only way to “save” existing Medicare is to raise your taxes and/or to cut your benefits.

A lie.

These are all lies on behalf of the rich, who want to widen the income/wealth/power Gap below them.

They bribe the politiciansvia campaign contributions and promises of lucrative employment opportunities.

They bribe the media via ownership and advertising dollars.

They bribe the economists via university endowments and employment in “think tanks.”

They do everything possible to brainwash you into believing federal finances are like personal finances when the two are polar opposites. The false comparison is called the Big Lie in economics.

As you read this prediction, keep in mind it came twenty-three years ago.

“We have to live within our means. We have to reduce our deficit, and we have to get back on a path that will allow us to pay down our debt. And we have to do it in a way that protects the recovery, protects the investments we need to grow, create jobs, and helps us win the future.

“Even after our economy recovers, our government will still be on track to spend more money than it takes in throughout this decade and beyond. That means we’ll have to keep borrowing more from countries like China.

“That means more of your tax dollars each year will go towards paying off the interest on all the loans that we keep taking out. By the end of this decade, the interest that we owe on our debt could rise to nearly $1 trillion.

“By 2025, the amount of taxes we currently pay will only be enough to finance our health care programs — Medicare and Medicaid — Social Security, and the interest we owe on our debt. That’s it. Every other national priority -– education, transportation, even our national security -– will have to be paid for with borrowed money.

“Now, ultimately, all this rising debt will cost us jobs and damage our economy. It will prevent us from making the investments we need to win the future. “

“We won’t be able to afford good schools, new research, or the repair of roads -– all the things that create new jobs and businesses here in America.

“Businesses will be less likely to invest and open shop in a country that seems unwilling or unable to balance its books. “And if our creditors start worrying that we may be unable to pay back our debts, that could drive up interest rates for everybody who borrows money -– making it harder for businesses to expand and hire, or families to take out a mortgage.

“Around two-thirds of our budget — two-thirds — is spent on Medicare, Medicaid, Social Security, and national security. Two-thirds. Programs like unemployment insurance, student loans, veterans’ benefits, and tax credits for working families take up another 20 percent.

“What’s left, after interest on the debt, is just 12 percent for everything else.”

That is the doom and gloom Obama fed you then; it’s the same diet of liesyou’ve been fed since 1940; and it’s the same utter nonsense you’ll hear today and tomorrow.

It’s the same lies you’ll be told every time the ridiculous, unnecessary “debt ceiling” comes up for debate — you know, the nonsense that paralyzes Congress every few months and is resolved simply by raising the ceiling withno adverse aftereffects.

(Since it already has been raised more than a hundred times, why not just get rid of it? Congress has been bribed to posture about lies.)

And now, thirteen years later, none of Obama’s predictions have come true. Why? Because they all were lies.

Every single time we have paid down the so-called “debt,” we have had recessions and depressions—not some of the time, butevery time.

The rich want you to believe the government can’t afford Medicare, Medicaid, Social Security, unemployment insurance, student loans, veterans’ benefits, and tax credits for working families.

Of course, nothing is said about the costs of those tax breaks for the richthat allowed a billionaire like Donald Trump to pay less income tax than did for the past ten years.

The rich want those cuts expanded. Trump has promised to expand them if he is elected. The rich are happy that Trump’s poor suckers will vote for his tax cuts.

It’s nice that so many people have written to me expressing outrage at the Big Lie. I appreciate your sentiments. But really, folks, I’m already in your corner and have been for twenty-five-plus years. And I’m pushing 90, so if you think Trump and Biden are too old, well . . .

If you want to make a difference, direct your outrage at someone who can do something about it. The politicians, the media, and the university economists.

Call them. Scream at them. Do it again, and again, and again. Every day. Twice a day. Never let up. Let them know you aren’t fooled.

Get your friends involved—and their friends, and theirs. Start a “Truth Club.” Bombard the information sources with truth bombs.

If you do nothing, nothing will happen. The lies will continue. The rich will grow richer. And years from now you will . . . As the poet Thoreau said, “The mass of men lead lives of quiet desperation.”

Because the populace has been pumped with wrong information about Monetary Sovereignty (MS), what should be easily understood is widely misunderstood. Does even the great Warren Buffett not get it?

He understands federal finance and strongly favors Social Security, yet does even he not know how that program is financed?

We have tried to make the simple even simpler with such posts as:

Airlines are sovereign over their mileage points. They cannot run short of points and can give them any value they choose. They are in “points debt” because they issue more points than they receive back from customers.

At its core, Monetary Sovereignty is dead simple. It merely says:

The U.S. federal government created an arbitrary number of dollars and gave them an arbitrary value by passing laws.

The government retains the power to pass infinite laws, create infinite dollars, and give dollars any values it chooses.

Because of these powers, the government cannot run short of dollars. It pays all its obligations with newly created dollars and does not need tax dollars.

Even if the federal government didn’t collect a penny in taxes, it could continue spending forever. No payment, however large, is a burden on the federal government or on federal taxpayers.

The posts gave examples of Monetary Sovereignty with airline mileage points, Monopoly dollars, and store coupons.

In each case, the issuer cannot run short of the points/dollars/coupons because all are numbers on computers typed at the creator’s whim.

Warren Buffett

Yet, despite that simplicity, even great financial brains seem confused:

Social Security has long been a subject of intense discussion in America, but investing legend Warren Buffett’s position on the issue is unmistakably clear.

During Buffett’s company, Berkshire Hathaway’s annual shareholders meeting in 2005, an audience member posed a blunt question: “I’m asking for your opinion on Social Security. Shall we call it the government-sponsored Ponzi scheme for retirees?”

Buffett’s answer was wrong.

He explained that, while it was proposed as insurance because that was “the only way [President Franklin] Roosevelt could get it passed,” Social Security is essentially a “transfer payment by the people who are in their productive years to the people who are past their productive years.”

And Buffett liked that mechanism.

“I think that the obligation for the people who do well in this society is to provide a reasonable level of sustenance for those beyond their productive years,” he said.

No, no, no. Social Security is nothing like “a transfer payment from people in their productive years to people past their productive years.”

And while he may imply there is a moral obligation for the productive people to aid those past productive years, that is not how Social Security operates.

Target is sovereign over its coupons. It cannot run short of coupons; it makes all the rules re. its coupons, and it runs “coupon deficits” (receives fewer coupons than it issues) and is in “coupon debt” (the total coupons issued is more than the coupons received.)

If it did, two things would be necessary:

1. Social Security would have to be supported by more affluent people, which it is not. Even the FICA tax, which ostensibly supports SS, is collected mostly from medium-to-lower salariedpeople — and only from the first $160K of salary.

I wonder whether Mr. Buffett collects any salary at all. If he obtains all his income via stock gains, dividends, interest, and other non-salary sources, he doesn’t pay FICA. No “transfer” there.

2. More importantly, and contrary to popular belief, FICA does not fund Social Security (or Medicare.) All federal spending is funded by newly created dollars.

Tax dollars, which begin, in the M2 money supply measure, suddenly disappear from anymoney supply measure when they hit the U.S. Treasury. They effectively are destroyed.

Ask yourself , “How much money can the federal government spend in any given year? Given that the government has the infinite ability to create dollars, how many dollars can it spend?

Right, it can spend infinite dollars. It never can run short.

What is any number added to infinity? Infinity. Those FICA dollars disappear into an infinite dollar hole, never heard from again.

The fake Social Security and Medicare Trust Funds, which supposedly receive FICA dollars and spend those dollars on benefits, do no such thing. In fact, they aren’t even trust funds.

They are bookkeeping mechanisms that only record inflows and outflows. They aren’t “trust funds” if the federal government can add to them, take from them, or revise them in any way and at any time it chooses?

If you go to any federal finance website, you will see how the government implies or even states outright that federal taxes fund federal spending. Yet, clearly, this isn’t true. Even if the federal government collected zero taxes, it could continue spending forever.

That is the reality of all large Monetarily Sovereign entities.

Consider the European Union, which is sovereign over the euro:

The federal government is sovereign over its “coupons,” aka dollars. It cannot run short of dollars; it makes all the rules re. its dollars, and it runs “dollar deficits” (receives fewer dollars than it issues) and is in ” debt” (the total dollars issued is more than the dollars received.)

No large Monetarily Sovereign nation can run short of its own sovereign currency — unless it wants to.

Why would it want to? To foster the false belief that benefits to the middle- and lower-income groups are unaffordable and unsustainable without benefit cuts or tax increases.

That is the basis for the Big Lie: “Social Security and Medicare can’t continue unless we cut your benefits or increase your taxes.”

Who benefits from the Big Lie: The rich who run America. They are rich because of a wide financial Gapbetween them and the rest of us. The wider the Gap, the richer they are.

There are two ways the rich widen the Gap:

They increase their net income with tax dodges for which they bribe politicians.

They reduce your net income by falsely claiming that benefits are unaffordable and unsustainable. They bribe the media and politicians to tell that lie.

Although Mr. Buffett seems to try to claim the high ground by “complaining” that his secretary pays a higher tax rate than he does, it’s hard to believe he doesn’t understand the realities of Monetary Sovereignty.

Therefore, I believe he intentionally lies about Social Security being a “transfer payment by the people who are in their productive years to the people who are past their productive years.”

Sadly, you receive the Big Lie from three groups the rich bribe: Politicians, news media, and educators. And there are the lies coming from the rich, themselves.

That Niagara Falls of false information drowns out the truth, which is why the simplicity of Monetary Sovereignty is so difficult for many people to understand.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

I believe the people at AARP understand that our government, being Monetarily Sovereign, never can run short of its own sovereign currency, the U.S. dollar.

They must know that even if all federal tax collections — income taxes, payroll taxes, etc. — and every other form of federal government income totaled zero, the government could continue spending forever.

The sole purposes of federal taxes (unlike state, local taxes) are not to provide the government with spending money, but:

To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

To assure demand for the U.S. dollar by requiring taxes to be paid in dollars

And the hidden reason: To help the very rich become richer by widening the Gap between the rich and the rest.

Stated simply, the U.S. federal government can pay for anything it wishes without taxing anyone.

AARP claims it “is the nation’s largest nonprofit, nonpartisan organization dedicated to empowering Americans 50 and older to choose how they live as they age. Advocating for people age 50-plus is at the heart of our mission.”

So why does the AARP repeatedly indicate the federal government can’t afford to pay for a comprehensive, no deductible Medicare benefit for every man, woman, and child in America?

Could their lucrative insurance business be the reason?

Here are excerpts from an article in the October, 2023 AARP Bulletin: (By Dena Bunis, who covers Medicare, health care, health policy and Congress. She also writes the Medicare Made Easy column for the AARP Bulletin. An award-winning journalist, Bunis spent decades working for metropolitan daily newspapers, including as Washington bureau chief for The Orange County Register and as a health policy and workplace writer for Newsday.)

For decades, as Americans approached their 65th birthday, all they had to do to get Medicare, the nation’s government-sponsored health insurance for older adults, was sign up.

The program wasn’t all that complicated. You went to the doctor armed with your Medicare card. Your physician or hospital took care of you and billed Medicare. Then you —or the supplemental (Medigap) planyou bought — paid your out-of-pocket share. Easy.

Today’s Medicare isn’t your grandparents’ program. New enrollees have an immediate big decision to make: Should they enroll in original Medicare (also referred to as traditional Medicare) or sign up for the private insurance managed care alternative, Medicare Advantage (MA)?

But why? Why is a decision needed?

AARP doesn’t explain why there are two plans, and why people are forced to choose between them. AARP also doesn’t explain why everyone, young or old must pay for some form of healthcare insurance, or have an employer pay.

In short, AARP doesn’t discuss the true question: Why doesn’t the federal government simply pay for everyone’s healthcare?

AARP profits by providing in their words, “health security, financial stability and personal fulfillment. AARP also works for individuals in the marketplace by sparking new solutions and allowing carefully chosen, high-quality products and services to carry the AARP name.”

Clearly, Medicare for All would be a financial disaster for AARP.

The two options not only differ in how they operate but increasingly in what coverage and services they provide. Making the decision requires looking down two roads that more and more are heading in different directions.

Original Medicare’s biggest draw remains the freedom enrollees have to go to any doctor or hospital in the country that takes Medicare.

In most cases, you don’t need a referral to go to a specialist or get a covered procedure done. It’s a simple fee-for-service insurance structure that was once commonplace across America but has mostly vanished for those under 65.

InMedicare Advantage, plans can feel more familiar, as they closely resemble the managed care plans offered by many employers, often in the form of a health maintenance organization (HMO) or preferred provider organization (PPO).

An MA plan is the one-stop-shopping alternative that bundles hospital, doctor and prescription drug coverage.

Most offer extra benefits not in original Medicare. MA plans also cap how much beneficiaries must pay out of pocket each year, something original Medicare does not.

The sole purpose of government is to improve and protect the lives of the people. That said, there is no reason why a federally funded plan cannot do everything Medicare + Medicare Advantage + every company-funded plan does — and without charging the American people one cent.

That is one way our government should improve and protect our lives.

(And no, this isn’t “socialism,” which is government ownership and control. It’s merely government funding, which is what the government currently does millions of times a day.)

Another big difference: Original Medicare is managed entirely by the federal government (oversight by Congress, day-to-day operations by the Centers for Medicare & Medicaid Services (CMS), meaning it is not operated for a profit.

That’s not exactly correct. The payment is managed by the government, but the services come from the private sector. The doctors, hospitals, the technicians, etc. are in the private sector.

The exception is the VA health system, which is owned and operated by the federal government.

Advantage plans, by contrast, are operated by private and often for-profit organizations that get flat-rate payments from the government to provide health care to an enrollee.

The financial difference is more apparent than real. The federal government still pays, but with Medicare Advantage, private insurance companies and their profit requirements are inserted as (unnecessary) middlemen between the providers and the government.

MA’s promise of extra benefits and lower premiums has been effective. In 2008, only 22 percent of beneficiaries were in Advantage plans. Since then, enrollment in these managed care plans has more than doubled and continues to grow.

In 2023, more than half of Medicare’s 60 million beneficiaries who have both Medicare parts A and B are enrolled in an MA plan.

And that’s the irony of the entire system. The government pays for both medical plans, but they offer different benefits. Medicare could (and should) offer the same or even better benefits MA offers. But it doesn’t.

Why? Because Americans have been brainwashed into believing that Medicare “can’t afford” to provide such benefits, and that in some mysterious way, Medicare can run out of money.

Medicare now finds itself at a crossroads. Based on current patterns, it won’t be long before enrollment in MA plans substantially overtakes enrollment in original Medicare.

Does the original need to be changed to remain competitive with MA? More fundamentally, will original Medicare as envisioned by President Lyndon Johnson and Congress in 1965 cease to exist in the years to come?

“I genuinely do believe that the future of Medicare lies in Medicare Advantage,” says James E. Mathews, executive director of the Medicare Payment Advisory Commission (MedPAC), established by Congress to analyze the program and provide advice. Mathews expects there will be a “natural migration” to MA, but he’s not sure whether that means original Medicare will disappear.

“It remains to be seen whether there is going to be some subset of the Medicare population for whom Medicare Advantage simply will not work.”

Medicare and Medicare Advantage will work if the benefits of both plans are blended into a Medicare for All plan.

Preserving and strengthening Medicare is one of AARP’s key policy concerns. That includes maintaining original Medicare.

“We strongly believe that traditional Medicare should be protected and strengthened and that there has to be a level playing field between traditional Medicare and Medicare Advantage,” says Megan O’Reilly, AARP vice president for health and family issues.

CMS Administrator Chiquita Brooks-LaSure oversees all Medicare operations. She says her priority is to strengthen both options. “I believe it’s critical that people have a choice between traditional original Medicare and Medicare Advantage,” Brooks-LaSure said in aninterview with AARP.

It’s like claiming that people should have a choice between an all-meat diet and an all-vegetable diet. Most people would prefer to blend the two into one complete plan.

Even experts who are most bullish on Medicare Advantage say they don’t expect original Medicare to go away. The main reason is choice.

Chiquita Brooks-LaSure, Administrator of the Centers for Medicare & Medicaid Services. Does she really not know that the federal government can fund one plan that offers every benefit?

The case for keeping original Medicare

Under original Medicare, you can go to any doctor, lab or hospital in the U.S. that participates in the program (about 90 percent of medical professionals do).

In MA plans, enrollees mostly must go to providers within the plan’s network, and these networks are highly regionalized. Going out of network means facing a much higher copay for each visit. In some cases, the care may not be covered at all.

“There are always going to be a lot of people who are going to say, ‘Look, I want to go to a doctor I want, and I don’t want to be limited,’ ” says Tom Scully, who was CMS administrator from 2001 to 2003 and is a supporter of Medicare Advantage. As a result, “I think original Medicare will never go away.”

“I believe it’s critical that people have a choice between traditional original Medicare and Medicare Advantage.”

— Chiquita Brooks-LaSure, CMS Administrator

Until they enroll, many Americans don’t realize how costly and complicated Medicare can be. That is especially true if you choose original Medicare.

Most original enrollees must make three regular insurance payments: one for basic Part B coverage, one for a Part D prescription plan, and one more for a Medigap policy to cover some or all of the expenses that Medicare doesn’t.

And there are other expenses on top of the premiums; for example, original Medicare Part B has an annual deductible ($226 in 2023); there’s also a deductible for every hospital visit, which in 2023 is $1,600. Those charges take a heavy financial toll.

All those premiums, deductibles an lack of coverage are unnecessary. The federal government could, and should fund one program encompassing all benefits. Why force people to forego some benefits?

By contrast, an Advantage plan enrollee usually has just one recurring payment: It includes the government-mandated Part B coverage cost and, in some cases, a small additional premium, which varies by what plan you choose and where you live.

You pay various copays and deductibles for your services and doctor visits, but the rest is fully covered by the plan, and you know going in what the copay is for the different providers. Costs under MA can also add up, though, especially if you need hospital care; most plans have a per-day hospital charge.

An important dividing line when choosing a Medicare path is whether a beneficiary can afford to pay the added monthly costs of a Medigap policy to supplement original Medicare coverage, as well as for a separate Part D prescription plan.

The federal government could and should pay for the above coverages.

The difference in “choice” between original Medicare and an MA plan isn’t simply which doctor you can see.

In an MA plan, the care you need is likely to be more scrutinized than in an original plan.

Insurers that run MA plans often require what’s calledprior authorizationbefore paying for your tests and procedures; that means a doctor must get approval for recommended care from internal reviewers before the treatment will be covered.

Why does MA require prior authorization, while Medicare does not? MA is ruled by the profit motive, while Medicare is ruled by the political motive.

MA can refuse unprofitable procedures. Medicare can afford to fund procedures that have political support, regardless of cost.

Some MA plans also require referrals to specialists, meaning if you wish to see, say, a cardiologist, you’ll need your primary care doctor’s blessing.

People in original Medicare usually don’t need referrals to see specialists, and as long as Medicare covers a test or treatment a doctor orders, except in a few situations, Medicare will pay for it.

If you develop a health condition that requires specialized surgery or highly advanced therapies to treat; in an MA plan, you likely won’t be coveredif you seek care from a doctor or medical center that specializes in your issue but is out of the network.

The above is the result of the profitmotive taking precedence.

On the other hand, most MA plans have benefits that original Medicare does not. The out-of-pocket cap is a big one; in 2023, MA enrollees know they won’t have to pay more than $8,300 in total annual health costs, although many plans have lower out-of-pocket limits than that.

Once again, there is no out-of-pocket cap in original Medicare.

Why are people subject to any out-of-pocket costs, when the federal government has infinite money to pay for medical care? No reason outside of the false claims that the federal government can run short of money.

Most MA plans cover basic dental, vision and hearing services.

Why does Medicare not cover dental, vision and hearing? Again, no good reason. Just the Big Lie about federal finances.

Some provide what are called Medicare flex cards that beneficiaries can use to pay for over-the-counter medications and other drugstore items, as well as healthy food.

In recent years,Congress began allowing MA plansto pay for making improvements to beneficiaries’ homes, such as wheelchair ramps and shower grips in bathrooms. Some plans pay for gym membershipsor transportation to doctors’ offices.

These are benefits the federal government could and should support; they increase the health of the people.

David Lipschutz, associate director of the Center for Medicare Advocacy, supports the ability of Medicare to help pay for nonmedical services that can help keep an older American healthy.

But he says it’s not fair that enrollees must be in a Medicare Advantage plan to take advantage of those extras. “One should not be forced to enroll in a private plan to access such services,” Lipschutz says.

No, it’s not fair that people should be forced to pay for any medical benefits when the federal government has the infinite ability to pay.

Imagine you have a few trillion dollars to your name, and your daughter needs expensive surgery. Would you pay for her the life-saving health care? The government has many trillions. It should follow its mandate to protect our lives.

Advocates and patients agree that MA plans seem fine as long as you’re healthy. But too often, beneficiaries with serious illnesses find it more difficult to get the care they say they need.

A 2022 report from the Government Accountability Office (GAO), a congressional watchdog, found that “Medicare Advantage beneficiaries in the last year of life left the program to join traditional Medicare at twice the rate of other beneficiaries. This could indicate potential problems with their care.”

The profit motive incentivizes private insurance companies to be excellent premium collectors but reluctant health care providers.

“Denials may be more frequent in Medicare Advantage plans than in traditional Medicare for people who have serious health problems,” says Tricia Neuman, senior vice president and head of the Medicare program at KFF, formerly the Kaiser Family Foundation.

That could be a real concern. When people age into Medicare, they tend to be healthier than they will be as they grow older and have more health problems, and that may not be top of mind.”

A federally funded, comprehensive, no-deductible Medicare for All would not have that problem.

Original Medicare may have another disadvantage: television. Throughout the year, but most prominently during Medicare open enrollment season each fall, ads for Medicare Advantage plans blanket broadcast and cable television stations.

From NFL Hall of Famer Joe Namath to “Captain Kirk” William Shatner to Jimmie Walker of “dy-no-mite” fame, celebrities urge older adults to call an 800 number and get lots of extras and benefits from Medicare Advantage plans.

Individual insurers also run ads, and some Medigap plans take to the airwaves. There are no such commercials for original Medicare.

Plenty of money for advertising; not enough for benefits.

“There’s nothing that helps lay out the trade-offs” between original and Medicare Advantage, says Gretchen Jacobson, vice president of Medicare at the nonpartisan Commonwealth Fund. “So if you just pay attention to the Medicare Advantage marketing, you may not really understand what the advantages and disadvantages are.”

“When we did focus groups with brokers, many said they are paid more to put people into Medicare Advantage plans, sometimes much more”

— Gretchen Jacobson, vice president of Medicare at the nonpartisan Commonwealth Fund.

And here is where the profit motive really comes into play:

“When we did focus groups with brokers, many said they are paid more to put people into Medicare Advantage plans, sometimes much more,” Jacobson said. But “if they were going into Medicare tomorrow, most of them said they would choose to be in traditional Medicare.”

These brokers do not get any commission for helping someone enroll in original Medicare. Likewise, they said most Part D prescription plans don’t offer commissions; for those that do, the rate is low.

As for Medigap policies, an agent might get some money for signing people up, but agents say it’s not as much as what they get for a Medicare Advantage enrollment.

The combination of insurance company advertising and insurance broker commissions puts people into Medicare Advantage, when that may not be the wisest choice, and certainly not the least expensive choice (which would be federally funded Medicare for All).

Universal health care for everyone in the United States promises only government inefficiency and health care that ignores the realities of the country and the free market.

“The VA system is not only costly with inconsistent medical care results, it’s an American example of a single-payer, government-run system.

We should run from the attempts in our state to decrease competition in the health care system and increase government dependency, leaving our health care at the mercy of a monopolistic system that does not need to be timely or responsive to patients.

The above supposedly is a negative about Medicare for All, except it isn’t. It is a negative about something no one proposes: VA-style federally owned and operated hospitals with providers being employees of the government.

It’s a fake, perhaps intentionally misleading, negative that no one wants. Medicare for All would be federally funded, not owned and operated. It would be an expanded version of Medicare without the FICA tax.

2. The challenges of universal health care implementation are vastly different in the U.S. than in other countries, making the current patchwork of health care options the best fit for the country.

Though the majority of post-industrial Westernized nations employ a universal healthcare model, few—if any—of these nations are as geographically large, populous, or ethnically/racially diverse as the U.S.

Different regions in the U.S. are defined by distinct cultural identities, citizens have unique religious and political values, and the populace spans the socio–economic spectrum. Moreover, heterogenous climates and population densities confer different health needs and challenges across the U.S.

Thus, critics of universal healthcare in the U.S. argue that implementation would not be as feasible—organizationally or financially—as other developed nations.”

Yes, blah, blah, blah, America is too big, too diverse, too climate-challenged, all great arguments except for one small detail. Medicare already has solved those fake problems. It funds health care all over our big country, and is quite popular, thank you.

3. Government controlis a large driver of America’s health care problems.

Bureaucrats can’t revolutionize health care – only entrepreneurs can. By empowering health care entrepreneurs, we can create an American health care system that is more affordable, accessible, and productive for all,” explains Wayne Winegarden, Senior Fellow in Business and Economics, and Director of the Center for Medical Economics and Innovation at Pacific Research Institute.

Someone please tell Mr. Winegarden that bureaucrats wouldn’t be in charge of revolutionizing anything. They merely would write the checks, just as they do now for Medicare.

4. Universal health care would increase wait times for basic care and make Americans’ health worse.

If coverage was nearly universal, cost sharing was very limited, and the payment rates were reduced compared with current law, the demand for medical care would probably exceed the supply of care–with increased wait times for appointments or elective surgeries, greater wait times at doctors’ offices and other facilities, or the need to travel greater distances to receive medical care. Some demand for care might be unmet.

Rephrasing the objection: “If everyone could get free healthcare, there wouldn’t be enough doctors, nurses, and hospitals to treat us rich folks. It’s better that some poorer people do without, so we don’t have to.”

The same objection could have been made to original Medicare.

However, if the federal government, which can afford anything, pays enough to those doctors, nurses, and hospitals, more people will enter the profession and more hospitals will be built.

It is a fake objection, the purpose of which is to widen the income/wealth/power Gap between the rich and the rest.

5. Universal health care would raise costs for the federal government and, in turn, taxpayers.

Medicare-for-all, a recent universal health care proposal championed by Senator Bernie Sanders (I-VT), would cost an estimated $30 to $40 trillion over ten years.

The cost would be the largest single increase to the federal budget ever.

Here, we have come to the Big Lie in economics, the lie that federal taxes fund federal spending. It is a lie promulgated by the very rich to discourage those who aren’t rich from asking for benefits.

The rich use the confusion between monetarily non-sovereign local and state governments vs, Monetarily Sovereign federal government.

State and local governments cannot create dollars at will, so they rely on tax income to fund their spending. The federal government can create dollars at will, so it does not use tax dollars. In fact, the federal government destroys all your tax dollars upon receipt.

You pay your taxes with dollars from your checking account which are part of the M2 money supply measure. Once your tax dollars reach the U.S. Treasury, they no longer are part of any money supply measure. They effectively are destroyed.

The Federal Reserve creates dollars at willby purchasing securities from a bank (or securities dealer) and paying for the securities by adding a credit to the bank’s reserve(or to the dealer’s account) for the amount purchased. In short, the Fed creates dollars from thin air, whenever it wishes.

Former Fed Chair Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Fed Chair Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Thus, the federal government can, at the touch of a computer key, fund a free, comprehensive, no deductible, Medicare program to protect every man, woman, and child in America.

SUMMARY

There is not a single financial reason why the government doesn’t improve and protect the lives of the people’s health, one of the jobs for which it was formed.

Every argument against free Medicare for all is based on ignorance and/or a lie. In creating Medicare, we already have done the hard part. It is only left to us to expand Medicare while ending all medical taxes and fees, and voila, we have Medicare for All.

Sadly, the rich and the insurance companies prevent the government from doing its job.

You don’t have free, comprehensive, no-deductible health care. Don’t blame “insolvency,” lack of money, inflation, lack of caregivers, or any other factor.

Blame the rich and the private insurance providers like AARP et al, for promulgating theBig Lie.

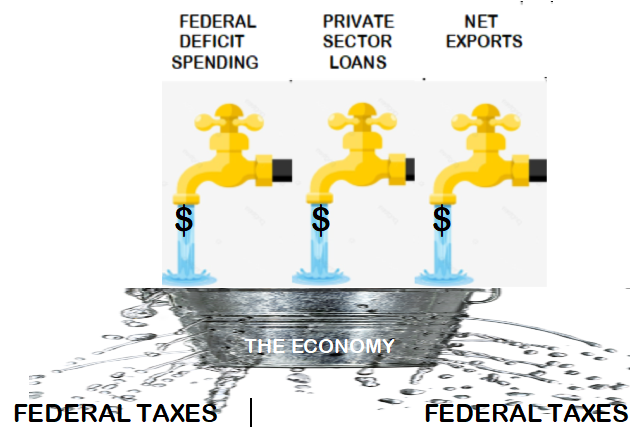

Every day, U.S. dollars are createdby federal government spending and by private sector lending.

And every day, dollars are destroyed by federal taxing and by private sector loan repayment.

Because private sector loans eventually are repaid, they do not permanently add dollars to the economy. By contrast, federal spending seldom is balanced by federal taxes — the government runs deficits almost every year — and those deficit dollars not offset by taxes, are permanently added to the economy.

Thus, federal deficits are the primary way dollars are permanently added to the economy.

The trajectory of Gross Domestic Product (GDP – red) parallels the M2 money supply trajectory.

America’s population is growing, and we have inflation every year. Further, our imports generally exceed our exports, so dollars leave the economy.

Just to remain level on a real (inflation-adjusted) per capita basis, our economy requires a growing supply of dollars:

GDP = Federal Spending + Nonfederal Spending + Net Exports

Mathematically, the economy (GDP) can’t grow unless the money supply increases. Without federal deficit spending, both “Federal Spending” and “Nonfederal Spending” would decrease, and “Net Exports” already is below zero.

In summary, the federal government must grow GDP to account for:

Inflation: According to the Bureau of Labor Statistics consumer price index, the average inflation rate of the US dollar between 1970 and today was 3.98% per year. This means that today’s prices are 7.93 times as high as average prices since 1970. So far, in 2023, the inflation rate has been about 8%. The Federal Reserve aims for 2% inflation.

Population growth: According to the United Nations, the population of the United States in 1970 was 205,052,174. As of 2023, the population of the United States is estimated to be 339,996,563. Therefore, the population of the United States today is approximately 65.8% higher than in 1970. The current population of U.S. in 2023 is 339,996,563, a 0.5% increase from 2022 or about 2 million more people.

Net imports: According to the World Bank, the U.S. trade balance for 2021 was $ 861.71B, a 37.32% increase from 2020.

Economic growth. Just to achieve zero economic growth, the U.S. government must run deficits that overcome Inflation, Population growth, and Net imports of $861B. For economic growth, the federal government must run additional deficits.

Federal deficits add growth dollars to the economy. Federal taxes take growth dollars away from the economy.

There are various ways to calculate how much the federal deficit needs to be to achieve economic growth.

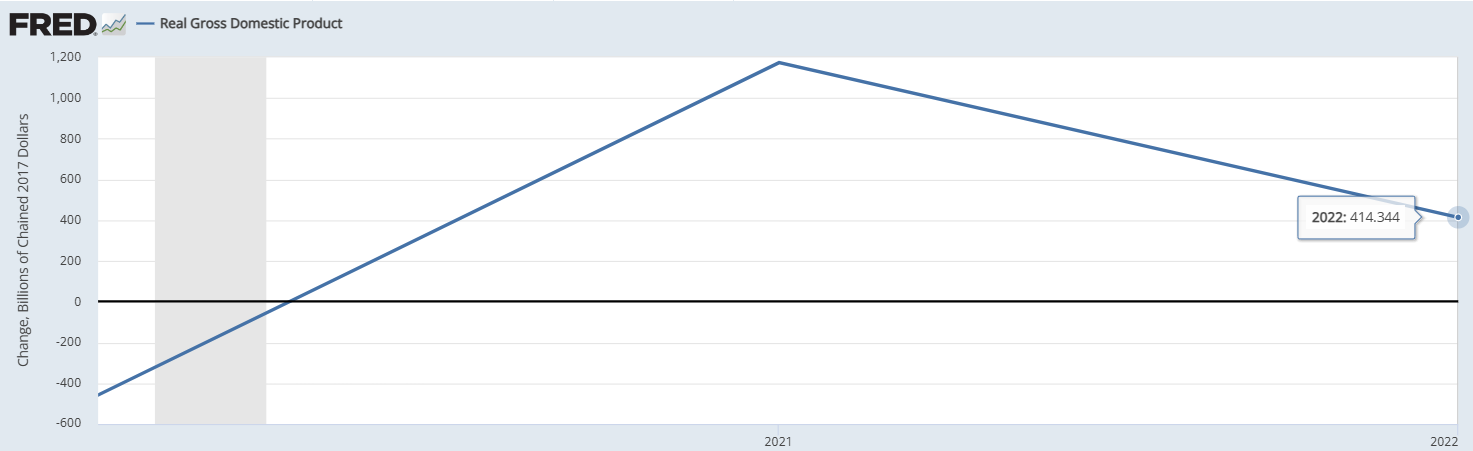

Here is a genuinely rough estimate, only as an example. The most recent GDP increase was $414 Billion.

That increase was achieved with a $1.7 Trillion deficit and $861 Billion Net Imports. This left about $839 Billion in the economy.

At 8% inflation, achieving the same level of GDP growth, Population Growth, and Net Imports would require a federal deficit of (108% x 1.7 Trillion) $1.8 Trillion.

Again, this is just “back of the envelope” stuff, leaving out many variables. It’s only to demonstrate one fact: Deficits are necessary for economic growth. Period.

$10 trillion in added debt shows ‘Bush and Trump tax cuts broke our modern tax structure’Jon Queally, Common Dreams, October 22, 2023, 7:05AM ET$10 trillion in added debt shows ‘Bush and Trump tax cuts broke our modern tax structure.’

The “modern tax structure” is broken, but not because of “added debt.” It’s broken because the purpose of federal taxes differs from the purpose of state/local taxes.

Federal taxes do not fund federal spending. Our Monetarily Sovereign government funds its spending by creating new dollars ad hoc.

No tax dollars are used. Taxes are paid with dollars from the M2 money supply measure. But when they reach the Treasury, they disappear from any money supply measure. The Treasury has infinite dollars; no measure exists.

Federal tax dollars effectively are destroyed upon receipt.

Today, federal taxes have two explicit purposes and one hidden purpose.

Federal taxes help the government control the economy by taxing what the government wishes to discourage and giving tax breaks to what the government wishes to reward.

Federal taxes also assure demand for the U.S. dollar by requiring dollars to be paid for all tax obligations.

The hidden purpose is to enrich the wealthy by widening the income/wealth/power Gap between the rich and the rest of us. The tax structure contains tax loopholes not available to the rest of us. These were put there via political bribes from the rich.

The U.S. Treasury Department on Friday released new figures related to the 2023 budget that showed a troubling drop in the nation’s tax revenue compared to GDP — a measure that fell to 16.5% despite a growing economy — and an annual deficit increase that essentially doubled from the previous year.

This above is an oblique reference to the meaningless Federal debt/GDP ratio. It is a ratio that compares two unrelated measures. Federal “debt” is nothing like actual debt. It is deposits into Treasury Security accounts (T-bills, T-notes, T-bonds).

These accounts are held by the government but are owned by the depositors (the buyers of those T-securities). The government never uses those dollars other than to add interest.

Upon maturity, the government merely transfers the dollars from the depositors’ T-security accounts to the depositors’ checking accounts. It is a simple asset transfer like moving dollars from your savings account to your checking account.

This so-called “debt” is not a financial burden on anyone — not on the government or on taxpayers.

The purpose of those accounts is not to provide spending money to the government. Rather, they are a safe place to store unused dollars, which stabilizes the dollar and helps provide demand for the dollar.

The other side of the Debt/GDP ratio, GDP, is total spending in America. It is not related in any way to deposits into T-security accounts.

The Debt/GDP ratio predicts nothing. It measures nothing. The ratio does not indicate the federal government’s ability to pay its bills, an infinite ability. The federal government cannot run short of dollars. Not now. Not ever.

The ratio does not indicate the economy’s health, which is characterized by such measures as inflation, employment, unemployment, GDP growth, healthcare, etc.

Look at any list comparing the ratio among the world’s various nations, and you will not be able to discern anything about those nations. For example:

Countries with the Highest Debt-to-GDP Ratios (%) Venezuela — 350% Japan — 266% Sudan — 259% Greece — 206% Lebanon — 172% Cabo Verde — 157% Italy — 156% Libya — 155% Portugal — 134% Singapore — 131% Bahrain — 128% United States — 128%

Countries with the Lowest Debt-to-GDP Ratios (%) are Brunei — 3.2%, Afghanistan — 7.8%, Kuwait — 11.5%, Congo (Dem. Rep.) — 15.2%, Eswatini — 15.5%, Burundi — 15.9% Palestine — 16.4% Russia — 17.8% Botswana — 18.2% Estonia — 18.2%

As you can see, the debt/GDP ratios tell you nothing about the economies of any country. Low ratios mean nothing. High ratios mean nothing.

Similarly, tax revenue/GDP means nothing. Yet the author, Jon Queally, finds it “troubling.”

That ratio tells you nothing about the government’s ability to pay its bills (which, again, is infinite). It tells you nothing about the current or future health of the economy.

The only thing this ratio tells you is how many dollars the government is taking from the private sector compared to spendingin the private sector. While Queally is concerned about the ratio being too low, he really should be concerned about it being too high.

Taking money from the economy is recessionary. The higher the tax revenue/GDP ratio, the fewer growth dollars remain in the economy. In finding the reduced ratio “troubling,” Queally has it all backwards, which is typical for people who do not understand Monetary Sovereignty.

It is far more troubling that economists find a meaningless ratio “troubling,”

“The deficit unexpectedly jumped this year to roughly $2 trillion.”

Bobby Kogan, senior director for federal budget policy at the Center for American Progress, has argued repeatedly that growing deficits in recent years have a clear and singular chief cause: Republican tax cuts that benefit mainly the wealthy and profitable corporations.

Federal deficits add growth dollars to the economy. The bigger the deficit, the more GDP growth.

The problem arises not because the deficits are too large but rather because they benefit the very rich by narrowing the income/wealth/power Gapbetween the rich and the rest.

The solution is not to levy more taxes on the general public or to reduce federal spending, both recessionary. The solution is to narrow the Gap by taxing the rich more and the rest of us less.

The first step should be to eliminate the FICA tax. It is America’s most regressive tax, punishing low-level salaried people the most.

Despite claims that FICA funds Medicare and Social Security, it does nothing of the sort. Medicare and Social Security benefits are funded by federal government money creation. If FICA were eliminated, this would have no effect on the government’s infinite ability to pay benefits.

Like all tax dollars, those FICA dollars are destroyed upon receipt by the U.S. Treasury.

In response to the Treasury figures released Friday, Kogan said that “roughly 75%” of the surge in the deficit and the debt ratio, the amount of federal debt relative to the overall size of the economy, was due to revenue decreases resulting from GOP-approved tax cuts over recent decades. “

Of the remaining 25%,” he said, “more than half” was higher interest payments on the debt related to Federal Reserve policy.

Federal tax cuts and federal interest payments both add growth dollars to GDP. It is hard to explain why anyone would wish to take more dollars from the private sector and give them to the Monetarily Sovereign federal government.

“We have a revenue problem due to tax cuts,” said Kogan, pointing to the major tax laws enacted under the administrations of George W. Bush and Donald Trump. “

The Bush and Trump tax cuts broke our modern tax structure. Revenue is significantly lower and no longer grows much with the economy.”

Is it possible for an economist to be too ignorant to understand that taxes take dollars outof the economy, which is recessionary?

And he offered this visualization about a growing debt ratio:

“The point I want to make again and again and again is that, relative to the last time CBO was projecting stable debt/GDP, spending is down, not up,” Kogan said in a tweet Friday night. “

It’s lower revenue that’s 100% responsible for the change in debt projections. If you take away nothing else, leave with this point.”

This truly is beyond ignorant. Kogan claims taking money from the economy is good for the economy, while adding dollars to the economy is bad for the economy.

In a detailed analysis produced in March, Kogan explained that, “If not for the Bush tax cuts and their extensions — as well as the Trump tax cuts — revenues would be on track to keep pace with spending indefinitely, and the debt ratio (debt as a percentage of the economy) would be declining.

It’s difficult to understand how a thinking human could claim that taking dollars from the monetarily non-sovereign private sector and giving them to the Monetarily Sovereign federal government somehow is good for America.

Shall we now apply leeches to cure anemia? Same ignorance.

Instead, these tax cuts have added $10 trillion to the debt since their enactment and are responsible for 57 percent of the increase in the debt ratio since 2001, and more than 90 percent of the increase in the debt ratio if the one-time costs of bills responding to COVID-19 and the Great Recession are excluded.

As we have shown, the debt/GDP ratio is meaningless. And as for the federal “debt,” it isn’t even debt. It is deposits into Treasury Security accounts, which more than anything, resemble safe deposit boxes.

The federal government does not spend the dollars in T-bill, T-note, and T-bond accounts. The government never touches those dollars, all of which are the property of the depositors.

Those so-called deposits are not a debt burden on the federal government. As each account reaches maturity, the dollars in the accounts are returned to their depositors.

It’s a simple asset exchange from the depositor’s T-security account to the depositor’s checking account.

Just as with deposits into safe deposit boxes, the contents of T-security accounts are not owed or owned by the federal government.

“Tax giveaways for the wealthy are continuing to starve the federal government of needed revenue: those passed by former Presidents Trump and Bush have added $10 trillion to the debt and account for 57 percent of the increase in the debt-to-GDP ratio since 2001,” read the statement.

“If not for those tax cuts, U.S. debt would be declining as a share of the economy.”

It is not possible to “starve the federal government” of dollars. It creates all the dollars it needs, at the touch of a computer key.

Kogan has no idea what Monetary Sovereignty means. He seems to think federal finances are like personal finances.

Whitehouse, who chairs the Senate Budget Committee, said the dip in federal revenue and growth in the overall deficit both have the same primary cause: GOP fealty to the wealthy individualsand powerful corporations that bankroll their campaigns.

GOP “fealty to the wealthy individuals” is well known. The only people more ignorant that those who worry about the meaningless Debt/GDP ratio are the middle- and lower-income people who vote for the party that tries to cheat them every day.

“In their blind loyalty to their mega-donors, Republicans’ fixation on giant tax cuts for billionaires has created a revenue problem that is driving up our national debt,” Whitehouse said Friday night.

“Even as federal spending fell over the last year relative to the size of the economy, the deficit increased because Republicans have rigged the tax code so that big corporations and the wealthy can avoid paying their fair share.”

The “giant tax cuts for billionaires” is not a federal debtproblem. The debt is no problem at all.

The tax cut for billionaires is a Gapproblem. The wider the Gap between the rich and the rest, the wealthier and more powerful the rich become and the poorer and more powerless the rest of us become.

Offering a solution, Whitehouse said, “Fixing our corrupted tax code and cracking down on wealthy tax cheats would help bring down the deficit.

It would also ensure teachers and firefighters don’t pay higher tax rates than billionaires, level the playing field for small businesses, and promote a stronger economy for all.”

The goal is not to “bring down the federal deficit.” The deficit enriches the economy. The goal is to narrow the Gap between the rich and the rest.

None of the latest figures — those showing that tax cuts have injured revenues and therefore spiked deficits and increased debt — should be a surprise.

Tax cuts reduce federal revenues. Federal revenues come out of the economy. Tax cuts enrich the economy. Is this so hard to understand? Growing GDP requires growing the money supply.

In 2018, shortly after the Trump tax cuts were signed into law, a Congressional Budget Office report predicted precisely this result: that revenues would plummet; annual deficits would grow; and not even the promise of economic growth made by Republicans to justify the giveaway would be enough to make up the difference in the budget.

“The CBO’s latest report exposes the scam behind the rosy rhetoric from Republicans that their tax bill would pay for itself,” Sen. Chuck Schumer (D-N.Y.), and now Senate Majority Leader, said at the time.

“Republicans racked up the national debt by giving tax breaks to their billionaire buddies, and now they want everyone else to pay for them.”

The Republicans lie; the Democrats lie. The media lie. The politicians lie. The economists lie. They all tell the Big Lie that federal spending is funded by federal taxes.

The purpose of the Big Lie is to make you believe the federal government cannot afford to give you benefits unless taxes are increased.

The plan is to make you ignorant so you will not demand increases in Medicare and Social Security benefits, poverty aids, infrastructure aids, and all the other benefits that supposedly are “unaffordable.”

For all the empty promises and howling from the GOP and their allied deficit hawks, the economic prescription they forced through Congress has resulted in an annual deficit of more than double, all while demanding the nation’s poorest and most vulnerable pay the price by demanding key social programs—including food aid, education budgets, unemployment benefits, and housing assistance — be slashed.

And being ignorant about federal finances, many of the “poor and most vulnerable” keep voting for Republicans.

Meanwhile, the GOP majority in the U.S. House — with or without a Speaker currently holding the gavel — still has plans to extend the Trump tax cuts if given half a chance.

In May, a CBO analysis of that pending legislation found that such an extension would add an additional $3.5 trillion to the national debt.

In other words, it would add 3,5 trillion growth dollars to the economy.

“Republicans racked up the national debt by giving tax breaks to their billionaire buddies, and now they want everyone else to pay for them,” Whitehouse said at the time.

“It is one of life’s great enigmas that Republicans can keep a straight face while they simultaneously cite the deficit to extort massive spending cuts to critical programs and support a bill that would blow up deficits to extend trillions in tax cuts for the people who need them the least.”

It’s one of life’s great mysteries why people who author articles about economics fail to understand that federal taxes remove growth dollars from the economy, federal deficit spending adds growth dollars to the economy, and the federal government never can run short of dollars but the economy can..

Chiquita Brooks-LaSure in Washington, DC, on August 23, 2023.")