The U.S. federal government is unlike state and local governments. It uniquely is Monetarily Sovereign. That means it has the infinite ability to create dollars simply by passing laws and pressing computer keys.

While state and local government can run short of dollars, the federal government cannot unintentionally run short.Not now. Not ever.

Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Federal Reserve Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Federal Reserve Chairman Jerome Powell stated, “As a central bank, we have the ability to create money digitally.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Social Security is a federal agency. Like all federal agencies, including Congress, the Supreme Court, theWhite House, the military, et al, Social Security cannot run short of dollars unless Congress and the President will it.

Congress has the infinite power to create laws, and some of these laws create dollars from thin air. So long as Congress can create laws, the U.S. always will have enough dollars for any expenditure.

In June, 2001, Paul O’Neill, Secretary of the Treasury said, “I come to you as a managing trustee of Social Security. Today we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.”

The so-called Social Security “trust fund” (which is not a real trust fund) never has assets other than “promises of the good faith and credit of the United States government.”

Those promises are what we call “dollars.”< /br>< /br>

Look at a dollar “bill.” At the very top it says, “FEDERAL RESERVE NOTE.” Bills and notes are promises of payment.

All dollars are promises by the federal government that it will accept dollars as payment, and so will everyone else in America. In fact, that is stated on the dollar bill: “This note is legal tender for all debts, public and private.”

The federal government has the infinite ability to create legal tender to pay all debts.

If I were the federal government, some people would tell you I could run short of oranges. Those are the people who tell you Social Security, Medicare, and Medicaid can run short of dollars.

Because the federal government cannot unintentionally run short of dollars, how can we explain the following article from MSN?

As Social Security teeters on the brink of insolvency, the government is exploring various proposals to ensure its sustainability.

While the program is not expected to disappear, the amount future retirees will receive is uncertain.

Have you ever heard that the White House, Congress, or the Supreme Court are “teetering on the brink of insolvency“?

No?

For the fiscal year 2024, the United States Supreme Court had a discretionary budget request of $161.3 million. Where did it get the money? There is nothing like a FICA tax to supposedly support this federal agency.

For the fiscal year 2025, the U.S. Congress has an approximately $5.9 billion budget. This budget covers the operational expenses of the House of Representatives and the Senate, including salaries, office expenses, and other administrative costs. Where did it get the money? There is nothing like a FICA tax to supposedly support this federal agency.

The White House’s annual operating budget is part of the overall budget of the Executive Office of the President (EOP). For the fiscal year 2025, the EOP has a budget request of approximately $714 million. Where did it get the money? There is nothing like a FICA tax to supposedly support this federal agency.

The answer to the questions: All federal agencies get their spending money the same way. Congress votes; the President approves; and magically, the dollars are created from thin air.

Social Security is a federal agency. Like all other federal agencies, Social Security gets its money from Congress’s votes and the President’s approval.

Contrary to popular wisdom, Social Security does not get its spending money from the FICA tax or any other source. Those FICA dollars ripped from your paycheck are destroyed the moment they reach the U.S. Treasury.

The dollars originate in checking accounts as part of the “M2 money supply measure.” When they reach the Treasury, they instantly cease to be part of any money supply measure. Effectively, they are destroyed.

Among the proposed changes, some have sparked significant controversy and resistance among the American public. A survey by the National Academy of Social Insurance (NASI) highlights six proposals that have met with strong opposition.

One of the most debated proposals involves the taxable earnings cap. This cap determines the portion of a person’s income subject to Social Security payroll taxes.

In 2025, the cap is set at $176,100. Most Americans earn below this threshold, paying taxes on their entire income, while wealthier individuals do not.

Many advocate for raising or eliminating this cap to increase contributions from the wealthiest, though this alone won’t resolve the funding crisis. The NASI survey indicates that maintaining the current cap, with only minor inflation adjustments, is unpopular.

The taxable earnings cap is an invention of the rich, to widen the income/wealth/power Gap between the rich and the rest.

Another contentious proposal is gradually raising the full retirement age (FRA) to 69. The FRA, which determines eligibility for full benefits, was previously increased from 65 to 67.

Raising it further would effectively reduce benefits for younger workers by increasing penalties for early claims and decreasing delayed retirement credits. This change is seen as a benefit cut, particularly affecting those who claim benefits in their early-to-mid-60s.

This is the “work-’til-you-die” provision that Republicans love. It penalizes those who are not rich, because they are the ones who rely on SS to survive.

Reducing cost-of-living adjustments (COLAs) is also on the table. COLAs are annual adjustments to help benefits keep pace with inflation but also increase program costs. Many seniors oppose reducing COLAs, as Social Security’s buying power has already declined.

The Senior Citizens League reports a 20% loss in buying power since 2010. There’s a push to calculate COLAs based on the Consumer Price Index for the Elderly (CPI-E), which would likely result in higher adjustments but also increase expenses.

If you are hoping to receive SS, and are not rich, but you voted for Trump, you’re getting what you voted for: Delayed SS benefits.

Increasing benefits by $250 per month for all new beneficiaries is another proposal that hasn’t gained much support. This increase wouldn’t benefit current recipients or address the issue of COLAs not keeping up with inflation.

The NASI survey found this proposal less popular than others, such as raising COLAs.

It’s not clear how this would address the phony Social Security Trust Funds so-called “insolvency.” But handing out money is a good idea.

Raising the taxable earnings cap to $ 350,000, while paying wealthier beneficiaries more, is another controversial idea. Although many support raising the cap, they oppose larger checks for high earners.

The current benefit formula replaces a smaller portion of pre-retirement income for high earners. Altering the formula to prevent larger checks for those paying more into the program would require congressional action.

The real problem is with the words, “taxable earnings.” Currently, FICA is calculated against salaries but not other taxable earnings, such as capital gains. Most of the rich do not receive significant salaries. They are too smart for that. Their income is from capital gains, stock swaps, etc. — stuff you middle-class workers seldom enjoy.

Lastly, a bridge benefit for retired workers with declining health has been proposed. Thiswould reduce early claiming penalties for those in physically demanding jobs.

While there’s demand for this change, details on its implementation and criteria are lacking.

Ultimately, the solution to Social Security’s challengesmay involve some or none of these proposals, as Congress decides the best course of action.

The solutions to “Social Security’s challenges” are:

Learn the facts about federal finance and acknowledge the federal government’s infinite ability to create dollars and to determine their value (i.e. control inflation).

Eliminate FICA. Fund Social Security by Congressional vote, like nearly all federal agencies are funded. Get rid of the fake Social Security “trust fund.” It’s not a source of dollars but rather a limit on dollars and an excuse for cutting benefits to those who are not wealthy. It’s as illogical as the current debt-limit laws.

Pay everyone of all ages a Social Security benefit, regardless of income. Elon Musk would receive the same benefits as the poorest, homeless adult. It would mean nothing to Musk but be a life saver to the poor person. (My current suggestion is about $3,000 per month for each adult and $1,500 per month for each child, with subsequent additions for inflation.)

Mitchell’s laws: The more budgets are cut and taxes inceased, the weaker an economy becomes. Austerity = poverty and leads to civil disorder. Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

This is an update of a post that ran in 2009.

Kermit the frog famously said, “It isn’t easy being green.” It also isn’t easy convincing people that traditional economics not only is hypothetically wrong, not only is factually wrong, but is wrong to such a degree it is extremely harmful to our economy.

The more extreme debt hawks believe the U.S. federal government should run a balanced budget or even have no debt at all. The more moderate debt hawks feel some debt may be necessary at times, but to them, federal debt is like bitter medicine you take only when absolutely necessary.

All debt hawks, whether extreme or moderate, are long on twisted “facts” but short on evidence.

Their “facts” inevitably include federal deficit and debt measures, projections for the future, debt/GDP ratios, and spending on Medicare and Social Security.

However, when they interpret the facts, they provide no evidence that their interpretations reflect reality.

By contrast, here are facts and a few opinions, which you may interpret for yourself.

1. Fact: Money is the way modern economies are measured. By definition, a large economy has a larger money supply than does a small economy. Therefore, a growing economy requires a growing supply of money. QED

The graph below shows the essentially parallel paths of GDP vs. perhaps the most comprehensive measure of the money supply, Domestic Non-Financial Debt:

One could argue that money begets production or that production begets money, and both would be correct. The point is that money supply (i.e. debt) and GDP go hand-in-hand. Reduced debt growth results in reduced economic growth.

Gross Domestic Product = Federal Spending + NonFederal Spending + Net Exports.

Thus, by formula, a cut in federal spending cuts GDP.

2. Fact: All money is debt and all financial debt is money. In addition to being state-sponsored, legal tender, there are four criteria for modern money:

–Monetarily Sovereign money must be defined in a standard unit of currency.

–MS money has no, or limited, intrinsic value.

–The demand for money is determined by its risk (danger of default or devaluation, i.e., inflation) and its reward (interest rates).

–To have value, money must be owned by an entity other than the entity that created it.

The above criteria describe many forms of money, including currency, bank accounts, T-securities, corporate bonds, and money markets. All forms of money are debt, and a growing economy requires a growing supply of debt/money.

2.a. Fact: Federal “deficit” is a statement of the net amount of money the federal government has created in one year. Opinion: The word “deficit” is pejorative. A more neutral description would be money “created” or “added,” as in, “The government has created $1 trillion,” or “The government has added $1 trillion to the economy.”

Compare the psychological meaning of those statements with the current phrasing, “The government has run a $1 trillion deficit.”

3. Fact: U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

4. Fact: Recessions tend to follow reductions in federal debt/money growth (See graph below), while debt/money growth has increased when recessions are resolving.

Taxes reduce debt/money growth. No government can tax itself into prosperity, but many governments tax themselves into recession.

Recessions repeatedly come on the heels of deficit growth reductions, and are cured with deficit growth increases.

5. Fact: On August 15, 1971, the federal government gave itself the unlimited ability to create debt/money by completely abandoning the gold standard. This ability is called Monetary Sovereignty.

Because the federal government now has the unlimited ability to create dollars, it neither taxes or borrows in order to obtain dollars. It simply creates them ad hoc. Tax dollars are destroyed upon receipt.

When you pay your taxes, you take dollars from your checking account. These dollars were part of the M2 money supply measure.

When they reach the Treasury, they cease to be part of any money supply measure. They effectively are destroyed. To pay its bills, the federal government creates new dollars, ad hoc.

6. Fact: Federal “debt” is the total of outstanding Treasury Securities. Here is how Treasury Securities, incorrectly termed “borrowing” come into existence.

–You tell the government to debit your checking account and credit your Treasury security account by the same amount. The process is similar to transferring money from your checking account to your bank savings account.

To “pay off” the Treasury Security, the government simply debits your T-security account and credits your checking account.

Thus, the government could pay off all its so-called “debt” tomorrow simply by debiting all T-security accounts and crediting the T-Security owners’ checking accounts.

The entire process neither adds nor subtracts money from the economy (but for interest paid).

Our Monetarily Sovereign government does not borrow the money it has already created but rather exchanges one form of U.S. money (T-securities) for another (dollars). The entire “borrowing” process is nothing more than an asset exchange.

Do T-securities have any benefit? Yes, federal interest payments add to the money supply, an economically stimulative event. Federal interest payments help the government control interest rates and the dollar’s value. (The higher the interest, the greater the value of the dollar, and the more the economy receives in growth dollars.)

The most important purpose of T-securities is to provide a safe place to store unused dollars. This stabilizes the dollar while increasing its value.

T-securities (debt) are not functionally related to the difference between taxes and spending (deficits). They are related only by laws requiring the Treasury to create T-securities in the amount of the deficit.

The Treasury can create T-securities (debt) without a deficit, and the government can run a deficit without creating T-securities. Federal debt is not functionally the total of federal deficits.

The federal government could pay off the entire so-called “debt” today, merely by returning the dollars to the T-security depositors.

7. Fact: Federal taxes, as a money-raising tool, are unnecessary, harmful and futile:

— unnecessary because since 1971 (when the U.S. government became fully Monetarily Sovereign), the government has had the unlimited ability to create money without taxes,

— harmful because taxes reduce the money supply, which reduction leads to recessions and depressions, and

–futile because tax money sent to the government is destroyed upon receipt by the U.S. Treasury.

When you send taxes to the government, you are sending M2 dollars, but when they reach the Treasury, they cease to be part of any money supply measure. They effectively are destroyed.

Our Monetarily Sovereign government does not store dollars for future use. It can create unlimited dollars ad hoc by paying bills.

The so-called “debt” merely accounts for the total outstanding T-securities created out of thin air by the federal government.

The government decides to create T-securities equal to the deficit, but this requirement became obsolete in 1971 when we went off the gold standard and became Monetarily Sovereign.

Today, the federal government creates money by spending, i.e. it credits checking accounts to pay its bills. This crediting of checking accounts adds dollars to the economy.

The federal “deficit” is the net money created in one year and the federal “surplus” is the net money destroyed in one year. In short, deficit spending creates money and taxing destroys money. If taxes fell to $0 or rose to $100 trillion, this would not affect by even one dollar, the federal government’s ability to spend.

Further, (opinion)all tax (money-destroying) systems are unfair. See: http://rodgermitchell.com/FairTaxes.html. For a country with the unlimited power to create money, spending is not related in any way to taxing.

8. Fact: Contrary to popular myth, there is no post-gold standard relationship between federal debt and inflation. (See graph, below)

Also, contrary to popular myth, inflation is not caused by “excessive federal spending.” Inflation is caused by shortages of crucial goods and services, most often oil and/or food. (See the graph, below)

In this regard, hyperinflations are not caused by “money-printing,” but rather by shortages. So-called “money printing” (ala Zimabwe and Germany), were the governments’ response to hyperinflation, not the cause.

The Zimbabwe inflation was caused by food shortages. (The government stole land from farmers and gave it to non-farmers.) Money “printing” was the faulty response to inflation, not the cause.

The most recent inflation was caused by COVID-related shortages of oil, food, shipping, computer chips, metal, housing, lumber, and labor, among other things. As the shortages have been reduced, so has the inflation.

WWII Context: During World War II, many consumer goods were in short supply because production was focused on the war effort. When the war ended, the supply of goods resumed, and the previously unmet demandwas suddenly able to be fulfilled.

Oil Crises: Similarly, during the oil crises of the 1970s, the reduced supply of oil caused prices to spike, not because of a sudden increase in demand, but because the existing demand couldn’t be met.

COVID-19 Pandemic: Supply chain disruptions and production bottlenecks during the pandemic created shortages in various goods, leading to price increasesonce supply constraints eased and the pent-up demand was met.

While the underlying demand might have been consistent, the ability to fulfill that demand was constrained by supply issues. When supply bottlenecks were removed, the previously suppressed demand could finally be expressed, leading to price increases.

Latent Demand: The concept of latent demand suggests that consumers’ desire for goods remains constant, but it is the availability of those goods that fluctuates.

Supply Constraints: Supply-side constraints create temporary mismatches between demand and supply, leading to inflationary pressures once those constraints are lifted.

Observing changes over time can reveal the true causes of economic phenomena. By examining what happens just before and during an inflationary period, we often find that supply-side disruptions are the primary drivers.

Gradual Demand Changes: Demand usually changes slowly, giving the economy time to adjust. This gradual change rarely leads to significant price fluctuations on its own.

Sudden Supply Changes: Supply-side shocks, such as natural disasters, geopolitical events, or production bottlenecks, can occur rapidly and unpredictably. The economy struggles to adjust quickly to these disruptions, leading to price increases as a balancing mechanism.

9. Fact: There is no post-gold standard relationship between federal debt and your taxes.

Unlike state/local governments, which are monetarily non-sovereign, the federal government does not use tax dollars to pay its bills. It creates new dollars, from thin air, every time it pays a creditor.

The sole purposes of federal taxes are:

–To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

–To assure demand for the U.S. dollar by requiring all federal taxes to be paid in dollars.

Taxes do not pay for federal spending. Federal spending creates dollars.

9.a. Fact: Federal deficit spending does not use “taxpayers’ money.” Federal spending creates money ad hoc.

When the government spends it credits bank accounts. No taxes involved. By definition, deficit spending means taxes do not equal this year’s spending let alone previous year’s spending. Only surpluses use taxpayers’ money, by causing recessions.

For the above reasons, our children and grandchildren will not pay for today’s money creation. Still, they will benefit from today’s deficit spending — better infrastructure, army, education, R&D, safety, security, health, and retirement.

Any time you hear or read about the federal government spending “taxpayers’ money,” know that the person is ignorant about Monetary Sovereignty. The federal government doesn’t spend taxpayers’ money. Period.

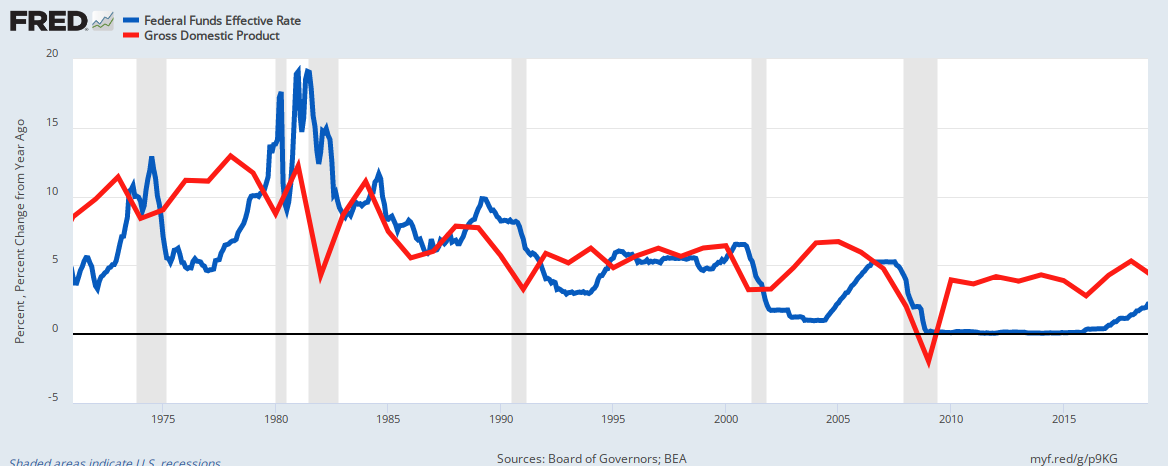

10. Fact: There is no post-gold standard relationship between low interest rates and high GDP growth. Opinion: The opposite seems true:

The interest rate and economic growth lines move in opposite directions.

Why do high interest rates stimulate? Opinion: High rates force the federal government to pay more interest, pumping more money into the economy.

The Fed increases interest rates to fight inflation. But increasing interest rates increases the prices of goods and services, i.e. causes inflation.

The Fed, in a sense, is using leeches to fight anemia.

11. Fact: The Federal debt/GDP ratio is a meaningless fraction, because it measures two, mathematically incompatible pieces of data. It’s an apples/oranges comparison. GDP is a one-year measure of output; federal debt is the net outstanding T-securities created since the nation’s birth.

The T-securities created years ago affect this year’s debt in the debt/GDP ratio, while even last year’s GDP does not affect this ratio. See: Debt/GDP

Because federal debt is the total of T-securities, and the federal government has the functional ability to stop creating T-securities at any time, the Debt/GDP ratio easily could fall to 0, depending on federal law.

11.a. Fact: The debt/GDP ratio does not measure the federal government’s ability to pay its bills. The government does not pay bills with GDP; it creates the money ad hoc to pay its bills.

Were GDP to be $0, the government still could pay bills of any size, simply by crediting the bank accounts of its creditors.

12. Facts: In 1979, gross federal debt was $800 billion. In 2009 it reached $12 trillion, a 1400% increase in 30 years. During that period, GPD rose 440% (annual rate of 5.5%>) with acceptable inflation. The same 1400% increase would put the debt at $180 trillion in 2039, a mean annual deficit of $5+ trillion.

This calculates to a 9.5% annual debt increase for the past 30 years. Repeating that growth rate would put the 2010 deficit at about $1.14 trillion, and the 2011 deficit at about $1.25 trillion. The deficit for year 2039 would be about $15.8 trillion.

Opinion: I know of no reason why the results would not be the same as they have been in the past 30 years. However, increasing the debt growth rate above 9.5% might show even better results:

In the 10 year period, 1980 – 1989, federal debt grew 210%, from $900 billion to $2.8 trillion (a 12% annual debt increase), while GDP grew .96% from $2.8 trillion to $5.5 trillion (a 7% annual increase). During that same period, inflation fell from 14.5% in 1980 to 5.2% in 1989. See graph, below.

The peaks and valleys of federal deficits (blue) generally correspond to the peaks and valleys of real (inflation adjusted) Gross Domestic Product growth. The reason: GDP = Federal Spending + Nonfederal Spending + Net Exports

Facts: In summary, large deficits have coincided with real (inflation adjusted) GDP growth

12. Facts: Any health insurance proposal that covers more people will cost more money. Extracting that money from doctors, hospitals, pharmaceutical companies, by necessity, would reduce the availability of health care.

Increasing taxes on any individuals (even the wealthy) or on businesses, will depress the economy by removing money from the economy. Only the federal government can supply additional money while stimulating the economy.

13. Fact: Social Security is supported neither by FICA nor by a trust fund. Were FICA eliminated, and benefits doubled, Social Security still would not go bankrupt unless Congress decided to make this happen.

In June, 2001, Paul O’Neill, Secretary of the Treasury said, “I come to you as a managing trustee of Social Security. Today we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.“

Yet, SS continues to pay benefits. Your Social Security check comes from a mythical trust fund that contains no money and receives no money.

Social Security (and Medicare) benefits are paid ad hoc by the U.S. government, not from a trust fund, and are not dependent on FICA taxes. which (opinion:) can and should be eliminated. See: FICA

14. Fact: The finances of the federal government are different from yours and mine and businesses’ and state, county and city government finances.

Unlike the federal government, which is Monetarily Sovereign, we cannot create unlimited amounts of money to pay our bills. We first need to acquire money, either by borrowing or by saving, to spend.

The federal government does not acquire money. It creates money by spending. As an accounting principle, the tax money you send to the government is destroyed upon receipt. Then the federal government creates new money to pay its bills. The government has no fund from which it pays bills.

Fact: Were taxes to decrease to zero, this would not change by even one penny, the federal government’s ability to spend.

Opinion: The failure to recognize the difference between the Monetarily Sovereign federal government and all other entities, which are monetarily non-sovereign, is the primary reason for recessions and depressions.

15. Fact: The federal government has the unlimited ability to create the dollars to pay any bill of any size. It never can run short of dollars; it never can go broke.

Opinion: The federal government should distribute dollars to each monetarily non-sovereign state, on a per capita basis.

The states would determine how they distribute the dollars (to counties, cities and/or taxpayers). I suggest a distribution of $5,000 per person or a total of $1.5 trillion.

Fact: In 1971, the U.S. went off the gold standard, thereby becoming a Monetarily Sovereign nation, and at that moment, all economics textbooks became obsolete. Sadly, mainstream economists, the politicians and the media have not yet caught up.

Summary: So there you have a list of facts, plus a few opinions, which I have noted. Read the facts and draw your own inferences.

You can find a great number of debt-hawk sites (i.e. Concord Coalition, Committee for a Responsible Federal Budget), which in essence are privately funded think tanks, paid to influence popular belief, with propaganda masquerading as data.

There, you will see data showing the size of the federal debt. These data are presented in a way designed to imply that the debt (money created) is too large.

But you will find no proof of these ideas. You will see no historical graphs equating debt with any negative economic outcome, simply because such graphs do not exist. Debt hawks believe federal deficits are so obviously bad, no proof is needed.

Yet, despite lacking proof, debt-hawks have foisted their opinions on the media, the politicians, weak-minded economists, and the public, much to the detriment of our economy.

The prevention and cure for a loss of democracy is an informed and energized electorate.

With Donald Trump ripping the government and the economy apart, here is what you should know during the two years before casting your vote in the next Congressional elections.

While Trump’s and the Republican ascendency in power may be a disaster for American democracy, such as it is, a few tiny glimmers of financial sunlight peek through the darkness.

For the purposes of this post, we’ll ignore the astounding parallels between Trump and Hitler while focusing on the few near-term benefits.

Here are a few excerpts from an article in USA TODAY:

Stocks soared on news of Trump’s election. Bonds sank. Here’s why. Story by Daniel de Visé, As Donald Trump emerged victorious in the presidential election Wednesday, stock prices soared. As the stock market rose, the bond market fell. Stocks roared to record highs Wednesday in the wake of news of Trump’s triumph, signaling an end to the uncertainty of the election cycle and, perhaps, a vote of confidence in his plans for the national economy, some economists said. On the same day, the yield on 10-year Treasury bonds rose to 4.479%, a four-month high. A higher bond yield means a declining bond market: Bond prices fall as yields rise. While stock traders rejoiced, bond traders voiced unease with Trump’s fiscal plans. Trump campaigned on a promise to keep taxes low.

It will be great news for the economy if he keeps that promise. Federal taxes are recessive. They remove dollars from the private sector and transfer them to the federal government, where they are destroyed.

Taxes are paid with dollars from the M2 money supply measure. When they reach the Treasury, they cease to be part of any money supply measure. Effectively, they are destroyed. Destroying M2 dollars is recessive.

Because the federal government can infinitely create dollars at the touch of a computer key, a money supply measure of federal dollars would make no sense.

No matter how many tax dollars you send to the federal government, the federal money supply measure will always be the same: infinite. That is because the U.S. government, unlike state and local governments, is Monetarily Sovereign.

It is 100% impossible for the federal government to unintentionally run short of its own sovereign currency, the dollars it created from thin air in the early 1800s.

Former Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

He also proposed sweeping tariffs on imported goods.

This will be bad news for the economy. Import tariffs are federal taxes. Like all other federal taxes, they are paid with M2 dollars that are destroyed when they reach the Treasury. Destroying dollars is recessive.

Economic growth is measured by Gross Domestic Product (GDP). GDP=Federal Spending + Non-Federal Spending – Net Imports. GDP growth requires money supply growth.

Worse, tariffs increase consumer prices, which means they add to inflation.

Even worse, tariffs invite retaliatory tariffs. They also reduce exports, which are part of the Gross Domestic Product.

Economists predict a widening deficit in Trump presidency Economists warn that Trump’s plans to preserve and extend tax cuts will widen the federal budget deficit,which stands at $1.8 trillion.

Contrary to popular wisdom, widening the federal budget deficit is good news for the economy. It means the government is pouring more growth dollars into the economy than it is taking out.

Deficits are the net amount of growth dollars the federal government adds to the economy. The federal debt is the net total of all previous deficits, i.e. the net total of all growth dollars the federal government has added to the economy.

Tariffs, meanwhile, could reignite inflation, which the Federal Reserve has battled to cool.

To summarize, import tariffs have two bad outcomes: They increase inflation and remove growth dollars from the economy.

Their ostensible purpose is to protect U.S. industry. A far wiser approach would be to cut federal taxes on businesses and support designated businesses with federal cash and favorable laws.

One example is federal farm subsidies, which boost farm profits without increasing consumer costs.

For bond investors, those worries translate to rising yields. The yield is the interest rate, the amount investors expect to receive in exchange for lending money: in this case, to the federal government.

Technical point: Because the federal government has the infinite ability to create dollars, it never borrows dollars. Though corporate bonds do represent corporate borrowing, federal bonds do not represent federal borrowing. The same word has two different meanings.

These bonds represent dollars deposited into T-bond accounts for safekeeping. The government never touches the money; it remains the property of the depositor. The purpose is to provide a save place for money holders to keep unused dollars.

The Chinese, for example, would be loath to store their billions of unused dollars in private banks.

In the current economic cycle, bond investors “might perceive there to be more risk of holding U.S. debt if there’s not an eye on a plan for reducing spending.

False. There is no spending-related risk for storing dollars in T-security accounts. The dollars always are 100% safe. This is diametrically the opposite with private sector bonds, which do suffer repayment risk.

The 10-year Treasury bond is considered a benchmark in the bond market. The yield on those bonds “began to climb weeks ago, as investors anticipated a Trump win,” The New York Times reported, “and on Wednesday, the yield on 10-year Treasury notes jumped as much 0.2 percentage points, a huge move in that market.”

This all was mere speculation, having nothing to do with real risk. Bond traders anticipated that other bond traders would think there was more risk, so they acted accordingly. It was a lemming-like approach to trading — trying to do what everyone else was going to do, before they did it.

When deficit growth decreases, we have recessions (vertical gray bars) which are cured by deficit growth increases. The reason: A growing economy requires a growing supply of money.Long-term bond yields are rising because “many investors expect that the federal government under Trump will maintain high deficit spending,” according to Bankrate, the personal finance site.

The federal government could double or triple its spending without accepting one additional dollar in deposits. Federal spending is not contingent on non-existent federal “borrowing.”

In a broader sense, bond investors worry that “we’re living beyond our means in the United States, and we have been for a very long time,” said Todd Jablonski, global head of multi-asset investing for Principal Asset Management.

This is utter nonsense. The U.S. federal government has infinite “means.” It cannot run short of dollars.

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Over the long term, Jablonski said, investors “fear that the United States’s creditworthiness is not as impeccable as it was once considered to be.” As the federal deficit grows, investors take on greater risk, and they expect to be paid a higher interest rate for loaning money to the government.

That is absolutely untrue. In 1940, when the federal debt (deposits) totaled only $400 Billion, pundits called it a “ticking time bomb.”

Exactly the same language has been used every year since. Today, after 84 years of hand-wringing, the pundits still make the same claim about our $30 Trillion debt, and we are no closer to insolvency than we were then.

This is part of the Big Lie in economics, where even respected economists continue to make the same “Earth-is-flat.” statements.

Perhaps it is taught in high schools or discussed over drinks. I can’t say, but it seldom is questioned. Strange.

If you would like to watch economists stutter, ask them:

“If federal deficits are bad, why do we run deficits to cure recessions?”

Neither Trump nor Democratic presidential candidate Kamala Harris offered a convincing plan to reduce the deficit on the campaign trail, economists said.

Politicians don’t reduce the deficit because it involves two steps—both economically bad: tax increases and/or spending reduction. Both are recessionary.

Harris promised to raise taxes on the wealthiest Americans and corporations as a source of new revenue.

Raising taxes on the wealthiest Americans has some value, but not for revenue generation. The beneficial purpose would be to narrow the income/wealth/power Gap between the rich and the rest.

Trump, by contrast, pledged to extend and even deepen his previous tax cuts. Trump has made a case that economic growth and job creation would naturally boost revenue.

Trump is correct on both counts. Deepening tax cuts benefits the economy, though he probably would again deepen them for the rich, thereby widening the income/wealth/power Gap, a terrible outcome.

Depending on the details, revenue might be boosted, but that would be bad for the economy.

The bond market may not be convinced. “If there’s a Republican sweep of House, Senate and the presidency, I expect the bond market to be wobbly,” said Jeremy Siegel, finance professor at the Wharton School of the University of Pennsylvania, speaking to CNBC on Election Day.

Yes, the bond market might be “wobbly” (whatever that means), not for functional reasons, ut rather because the Jeremy Siegels of the world predict wobbliness.

In Summary:

The federal government is uniquely Monetarily Sovereign over the U.S. dollar. It cannot unintentionally run short of dollars.

The federal government does not borrow dollars or owe so-called “debt.” The dollars deposited in T-security accounts are wholly owned by depositors, whom the government pays merely by returning their dollars.

The purpose of federal bonds is not to provide the government with spending money. The purpose is to provide a safe place for dollar holders to store unused dollars. This stabilized the value of the dollar.

Federal deficit spending and “debt” are not a burden on the government or taxpayers, nor are they a risk to depositors.

Economic growth requires federal deficit spending, which adds growth dollars. When deficits are too low, we have recessions, which are cured by increased deficits.

The Wall Street Journal is owned by Rupert Murdoch, who supports 32 times convicted felon Donald Trump. Murdoch also owns extreme right-wing Fox News, which paid an $800 million fine for lying.

Need I say more?

Here are excerpts from an article that appeared in the WSJ. Comments are noted.

Federal Debt Is Soaring. Here’s Why Trump and Harris Aren’t Talking About It. Story by Richard Rubin, richard.rubin@wsj.com

The U.S. isn’t fighting a war, a crisis or a recession. Yet the federal government is borrowing as if it were.

The U.S. federal government is Monetarily Sovereign. It has the unlimited ability to create U.S. dollars:

Alan Greenspan:“There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

If you owned a money-printing machine and had the unlimited, legal ability to create as many $100 bills as you wanted — at no cost to you — would you ever borrow dollars? Think about it.

The government has that “money-printing machine” and the legal right to create dollars. Why on earth would the government ever borrow dollars? Answer: The U.S. government never borrows dollars. Not ever.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

The confusion is semantic. In the private sector, the words “bills,” “notes,” and “bonds” denote debt. “Bills” are what you owe in your daily life. Corporate “notes” and “bonds” are evidence of corporate debt.

By contrast, Treasury bills, notes, and bonds have nothing to do with government borrowing. They are deposits into Treasury Security accounts. Depositors, like China, the UK, and private citizens like you, own the money in these accounts; the federal government doesn’t.

The federal government never accesses those dollars for federal spending. It creates new dollars to pay all its bills.

To pay a creditor, the federal government creates instructions in the form of checks or wires. The instructions tell the creditor’s bank to increase the balance in the creditor’s checking account by a certain amount.

At the moment the bank obeys those instructions, new dollars are created and added to the M2 money supply measure.

To pay off the so-called “debt,” the federal government merely returns the depositors’ dollars that already reside in their T-security accounts. (Think of a safe deposit box in which depositors place valuables. The bank doesn’t use those valuables and returns them upon request by the depositors.)

Returning existing dollars is not a financial burden on the government or on federal taxpayers.

The confusion is not only semantic but also arises from the fact that the total of deposits equals the total of federal deficits. This is an anachronism from when the federal government was not wholly sovereign over the dollar and tied itself to silver and gold.

In short, federal “debt” is nothing like personal debt. The federal government is not “in debt.” It pays all its bills timely and in full, and can continue doing so.

Since dollars are a creation of laws, so long as the federal government has the ability to pass laws, it has the ability create dollars.

This year’s budget deficit is on track to top $1.9 trillion, or more than 6% of economic output, a threshold reached only around World War II, the 2008 financial crisis and the Covid-19 pandemic.

Publicly held federal debt—the sum of all deficits—just passed $28 trillion or almost 100% of GDP.

The “debt”/GDP ratio is meaningless. It says nothing about the federal government’s ability to pay. Debt nuts often quote this number to scare you, but it has absolutely no relevance to the federal government’s ability to pay its bills.

If Congress does nothing, the total debt will climb by another $22 trillion through 2034. Interest costs alone are poised to exceed annual defense spending.

These are big numbers but completely meaningless concerning the federal government’s solvency. The misnamed “debt” could be ten times or a hundred times as large, and the federal government easily could continue to pay all its bills.

Even if the government didn’t collect a single penny in taxes and the “debt” was a hundred times larger, it still could continue to pay its bills in full and in a timely manner.

Federal taxes are different from state and local taxes. State and local governments are monetarily non-sovereign. They do not have the unlimited ability to create dollars. They use tax receipts and borrowing to pay their financial obligations.

By contrast, the U.S. federal government does not use tax dollars or borrowing to pay its bills. The purposes of federal taxes are:

To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

To assure demand for the U.S. dollar by required taxes to be paid in dollars.

Economists and policymakers already worry that the growing debt pile could put upward pressure on interest rates, restraining economic growth, crowding out other priorities and potentially impairing Washington’s ability to borrow in case of a war or another crisis.

In one sentence, the author, Mr. Rubin, has articulated the four common lies about the so-called federal debt (that neither is federal nor debt).

The U.S. Federal Reserve sets interest rates at its whim in an effort to control inflation. This has nothing to do with the size of the federal “debt” as shown by the following graph:

There is no relationship between changes in federal “debt” (bleu) and interest rates (red).

There have been scattered warning signs already, including downgrades to the U.S. credit rating and lackluster demand for Treasury debt at some auctions.

Interest rates also are set to attract depositors, an exercise that became obsolete in 1971, when the government no longer required itself to match income with outflow.

2. Credit agencies set ratings based on the debtor’s ability and likelihood of paying promptly and in full. The federal government always pays timely and in full, so why would the rating ever go down?

Answer: This is not because of the size of the “debt” but because of Congress’s political gamesmanship. The party out of power limits the party in power’s ability to pay. It uses one of the more ridiculous laws, the so-called “debt limit” (which doesn’t limit the non-existent “debt.” It limits the government’s ability to pay its daily bills).

While the federal “debt” has grown from $400 billion to $33 trillion in just 80 years, “debt” downgrades have been few and sporadic, and related only to the fear that the debt nuts will prevent the government from paying, not to the size of the “debt.”

3. Federal deficits are necessary to grow the economy. It is mathematically impossible for the U.S. economy to grow unless the federal government pumps more money into the private sector (aka, the economy) than it takes out.

4. Federal deficit spending does not “crowd out” anything. It adds lending dollars to the economy.

With more dollars on deposit, the banks can lend more easily, and when the economy has more money, it is more likely to expand by borrowing. Nothing impairs Washington’s ability to borrow; the federal government never borrows.

5. “Lackluster demand” for T-securities is not a problem for the federal government. Selling T-securities doesn’t benefit the federal government. T-securities benefit buyers looking for a safe place to store unused dollars. That is why China buys them.T-securities are more secure than any bank China could find.

T-securities have two purposes, neither of which is to provide spending funds to the U.S. government:

— To help stabilize the dollar by providing safe storage for unused dollars

— To help the Fed control interest rates.

Both Harris and Trump have promised to protect the biggest drivers of rising spending—Social Security and Medicare. And both want to extend trillions of dollars in tax cuts set to lapse at the end of 2025, amid bipartisan agreement that federal income taxes shouldn’t rise for at least 97% of households.

Those are good political promises that would benefit the economy. Of course, the reality is that debt nuts will prevail because of voter ignorance. Thus, you can expect the same strong support for cutting benefits to the middle- and lower-income groups as we have seen in the past. The eligibility age for Social Security will continue to go up, and benefits will be taxed further.

Trump has promised to exempt tips from taxation, end income taxes on Social Security benefits, eliminate taxes on overtime pay, lower tax rates for companies that manufacture in the U.S., and create a new deduction for new parents’ expenses, offering more than $2 trillion in tax cuts atop $4 trillion to extend his first-term tax cuts.

These are good ideas, but as has been typical of Trump’s promises, they’re all verbal tooth-fairy stuff. It’ll happen only in your dreams.

Harris matched Trump’s tips idea and called for an expanded child care tax credit, including $6,000 for parents of newborns.

If the Republican House allows an expanded child care tax credit and $6,000 for newborns — which it won’t.

How did the U.S. fiscal path simultaneously become economically more alarming yet politically less relevant? Federal debt and deficits have blown past various imagined red lines and feared consequences have not materialized.

Keep that phrase in mind: “Feared consequences have not materialized.” The reason: The feared consequences were based on lies. There are no adverse consequences for federal deficits.The consequences are for not running deficits or even for deficits that are too low.

Interest rates, at least until 2022, stayed low. The dollar remains the world’s reserve currency, giving the U.S. far more running room than other major countries. The U.S. of 2024 is not Greece of 2007. There is risk, but there is no fiscal crisis.

There has been no financial crisis simply because federal “debt” is not a financial crisis. The whole thing is a giant lie spun by the rich to prevent the rest of us from receiving benefits.

The tax on Social Security benefits is ludicrous. Why would any sane government tax the benefits it provides?

The fact that the U.S. dollar is the world’s most common reserve currency does not give the U.S. “more running room” (whatever that is). It merely means that the world’s banks carry more U.S. dollars in reserve to facilitate international trade.

It does not protect us from financial difficulties; Monetary Sovereignty protects us from financial difficulties.

And yes, the U.S. is not Greece (or France, Germany, or Spain), none of which is Monetarily Sovereign. Those nations are more like Illinois, New York, and Wisconsin. They cannot create the money they use. The European Union (EU) is like the U.S. federal government in that itis Monetarily Sovereign and has the unlimited ability to create euros.

“We’ve learned we borrowed more than we realized we could,” said Jason Furman, a Harvard economist who was a top aide to President Barack Obama. “And we’ve actually borrowed more than we expected.”

Actually, Mr. Harvard economist, we haven’t borrowed at all. You’re surprised because the economy has grown due to increased federal deficit spending.

You simply can’t figure out why deficit spending seems to grow the economy while insufficient deficit spending leads to recessions (which are cured by more deficit spending).

Why it’s a mystery to you is the real mystery.

When deficit growth declines, we have recessions (vertical gray bars), which are cured by deficit increases.

Sadly, this simple graph shows that declines in deficit growth repeatedly lead to recessions, which are cured by increasesin deficit growth.

Yet economically ignorant pundits continue to rail against deficit growth.

If anything, borrowing kept the economy afloat during the 2007-09 financial crisisand pandemic, and lawmakers were rewarded for it. Polls show the public is concerned about the deficit, but they also prefer politicians who dangle tax cuts, stimulus checks and money for the military.

If you believe borrowing “kept the economy afloat,” why do you oppose it?

At any rate, there was no borrowing. There was money creation, which the federal government can do in any amount, at will. The financial crisis was caused by excessive private-sector borrowing, not by non-existent federal borrowing.

The author demonstrates a failure to understand the difference between private sector and federal finances.

“No president in history, Republican or Democrat, gets a gold star or a Nobel Prize for reining in spending, the deficits and our debt,” said Rep. Jodey Arrington (R., Texas), chairman of the House Budget Committee. “Nobody gets the golden meat cleaver award.”

Thank heaven for that, because the “golden meat cleaver” cuts the legs off economic growth. (See: Ignorance is hard to conquer if the ignorant want to remain that way.)

Whoever wins in November will soon face two big fiscal tests. One is the need to raise the federal debt limit, likely in mid-2025.

No, the test will be to eliminate, not raise, the ridiculous “debt limit,” a law based on the rich’s desire to widen the income/wealth/power Gapbetween them and the rest. It is the Gap that makes them rich. Without the Gap, no one would be rich; we all would be the same. And the wider the Gap, the richer they are.

The two ways for the rich to become richer are: Gain more for themselves and/or make sure those below them have less. That is why cutting your benefits makes the rich richer.

In both 2011 and 2023, the threat of default without a debt-limit increase led to compromises that reduced red ink.

Any default would be caused by the idiotic, unnecessary “debt ceiling.” Compromises are political theatre based on lies.

The other trigger is the looming expiration of much of the 2017 tax law.

That is the tax law Trump passed to help the rich widen the income/wealth/power Gap between the rich and the rest.

It was a tax law that If Congress doesn’t act by the end of 2025, taxes would rise on most households, a path to deficit reduction that both parties say they don’t want.

Imagine that. Congress wants to keep taxes low, but not increase the deficit. Anyone have a magic wand to make that happen?

In the early 1990s, when deficits were much smaller, deficit hawks were powerful enough in both parties to produce bipartisan deals that raised taxes and lowered spending. Those agreements helped drive the budget into balance in the late 1990s. Federal debt fell to about one-third of GDP.

And that budget balancing is what led to the recession of 2001, which was cured by federal deficits.

As deficit growth fell, we had a recession, which was cured when deficit growth resumed. This has happened repeatedly in U.S. history, yet debt nuts still call for deficit reduction.

When he first ran for president in 2016, Donald Trump said he would pay off the national debt within eight years. He went in the opposite direction: Debt rose from less than $15 trillion to more than $21 trillion by the time he left office.

What?? Donald Trump lied? Hard to believe. But good thing he did. The rise in “debt” fueled economic growth.

Trump made two major decisions that broke with Republicans in Congress and drove up federal borrowing.

Republicans had long advocated making Social Security and Medicare less generousand more fiscally sustainable. To appeal to middle-class voters, Trump embraced what had long been a Democratic position and shut down discussion of broad benefit cuts.

As always, Republicans wanted to cut benefits for those who are not rich. Trump saw that the voters would not buy into the lie, so he wisely increased the “debt.”

And to call Social Security and Medicare “generous” is laughable. No one can live on Social Security benefits, and Medicare covers, at best, only 80% of costs. Still, the right-wing can hardly wait to cut, cut, cut.

Then in 2017, when House Republicans sought to cut tax rates, Trump resisted their attempts to offset the full cost. The Tax Cuts and Jobs Act Trump eventually signed into law was projected then to increase deficits by $1.5 trillion over a decade.

And it helped make the rich richer.

Once the pandemic started, Trump joined the broad economic consensus that the U.S. needed to pour money into the economy, eventually adding more than $3 trillion to the debt to provide stimulus checks, enhanced jobless benefits and other relief.

O.K., debt nuts, why does pouring money into the economy grow the economy, but only is a good thing when the economy is in trouble? It makes no sense.

President Biden and Harris expanded on Trump’s pandemic spending with the $1.9 trillion American Rescue Plan, which included another round of stimulus checks and aid to state and local governments.

The stimulus checks were a toe-in-the-water introduction of Social Security for All, which America should have. It worked as desired, which is why Congress didn’t repeat them.

Biden, with Harris’s strong backing, canceled student debt in a series of executive orders that could cost the government more than $1 trillion, according to the Committee for a Responsible Federal Budget. The plan is now stuck in litigation as (right-wing) courts have curtailed Biden’s authority to cancel debt.

“I don’t think we’ve seen a president spend nearly as much without Congress as Biden,” said Marc Goldwein, the CRFB’s senior vice president.

Biden took over where the Republican Congress played politics with the economy. Putting students into debt is as stupid as it gets for a nation that claims it needs an educated population to compete on the world stage.

What happens if Trump wins depends on Congress. If Republicans also control the House and Senate, his next term could look a lot like his first—occasional talk about debt and deficits paired with tax cuts that expand both.

“Paired with tax cuts” for the rich along with deportations of much of our workforce (which would destroy the economy), the promised firing of millions of government workers (which would destroy our government), and the hiring of Trump’s incompetent friends and relatives (which would make Trump a dictator).

In his acceptance speech at the Republican National Convention, Trump said, “We’ll start paying off debt and start lowering taxes even further.”

Nonpartisan experts say there’s virtually no chance of that. Paying off debt would require the U.S. to shift from massive deficits to surpluses.

Tax cuts would work in the opposite direction. Low tax rates can encourage growth and generate some revenue, but not enough to offset the loss of revenue, economists in both parties acknowledge.

Federal surpluses take dollars out of the economy. How this is supposed to cause economic growth is a mystery never explained by the debt nuts.

Every federal surplus in history has caused a depression, but one, the 1997 recession “only” caused a recession.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

The reason for the above is no mystery. GDP = Federal Spending + Nonfederal Spending + Net Exports. Reduce federal deficits, and you will reduce both federal spending and nonfederal spending. Simple algebra.

Trump has indicated that he wants to extend the pieces of his 2017 tax law that expire after 2025 and lower the 21% corporate tax rate to 20%, and 15% for some companies. His recent proposals—eliminating taxes on workers’ tips, overtime pay and retirees’ Social Security benefits—dig a deeper hole.

He’s also made other proposals that would entail significant new spending, including a mass deportation program and a domestic missile-defense system.

These are good proposals except for his deportation crime. This would destroy lives, destroy the economy of America and the world, and destroy America ‘s reputation. We would forever be stamped as a vicious, mean-spirited banana-republic dictatorship.

Trump has touted several ideas that could reduce deficits. One is impoundment, in which the president refuses to spend money Congress has appropriated. That’s legally and constitutionally dubious.

And economically suicidal.

The other is tariffs. Trump wants to impose a tariff of 10% to 20% on all imported goods and even higher on Chinese products. That could raise about $2.8 trillion over a decade, according to the Tax Policy Center.

That $2,8 trillion would come from the pockets of American consumersand the economy. It’s incredibly ignorant, which is why debt nuts will love it.

House Republicans have proposed capping federal spending growth at a level lower than inflation, though the party is split and some want significant increases in the defense budget.

Capping spending will cause a recession or depression, as it always has. Sadly, the American voter is ignorant about federal finances, so will vote for a damaging and unnecessary cap.

Arrington, who is helping cobble together Republicans’ agenda if they have full control of Congress, said they need to tackle spending and entitlement programs and hopes Trump, despite his statements to the contrary, could be open to that.

“We have an opportunity to live up to what we claim we believe when we campaign and why almost every Republican member was sent here to Congress by their constituents,” he said.

Arrington claims Republican constituents want Congress to cut Social Security and Medicare. That’s what his voters want? Really?

First, while the budget would raise taxes on the rich and corporations, the revenue isn’t enough to deliver the claimed deficit reduction, pay for Harris’ child tax credit and home-buyer subsidy proposals, and cover the Biden-Harris proposals to extend expiring cuts to prevent tax increases on households earning less than $400,000.

Second, the chances Congress would agree to such a plan are slim, even in the unlikely event Democrats control both the House and Senate. Biden couldn’t get centrist Democratic senators to pass his tax increases in 2022. Harris could face similar opposition and already dialed back Biden’s proposed capital-gains tax increase.

All of the above nonsense is due to one thing: The Big Lie that federal taxes fund federal spending. Let’s clarify this as simply as possible.

Federal taxes do not fund anything.

Even if the government collected $0, it could continue spending forever.

The government pays for everything by creating new dollars ad hoc.

Biden officials see next year’s tax debate as a crucial pivot point, and the White House has said any extension of expiring tax cuts should be paired with tax increases.

Ridiculous. Federal taxes pay for nothing. They are a useless drain on the economy.

Biden has proposed some Medicare savings through prescription drug pricing and has called for shoring up Social Security, which is paying out more in benefits than it collects in taxes.

Federal payment of more benefits than it collects in taxes grows the economy (aka the private sector).

But the parties are at odds over whether Social Security taxes and benefits should increase, and that gridlock means the program likely won’t be addressed for about a decade, when its trust fund is projected to be exhausted, triggering benefit cuts.

The federal government should simply pay for Social Security and Medicare to “shore up” them.

Not including interest, the U.S. government will spend $1.21 for every $1.00 it collects in revenue this year. Add interest and that climbs to $1.39.

Mathematically, that $.21 (or $.39) difference will grow the economy. Growing the economy is impossible if the federal government runs a surplus.

Voters often support balanced budgets in theory, but they also like the low taxes and higher spending of the past few decades.

Wanting federal balance budgets merely indicates that the public, having been fed the Big Lie so often, has become ignorant about federal finances.

“It’s really the combination of high deficits, high debt level, high interest burden,” said Richard Francis, the lead U.S. analyst for Fitch Ratings, one of those companies. “And we didn’t see any willingness to tackle the big issues.”

Total BS. Since 1940, the U.S. government has had high deficits, a high “debt level,” and often high interest rates, but it has never been downgraded. Why? Because Congressional infighting has become so fierce that the rating agencies were afraid the government would refuse to pay its bills out of spite toward the other side.

At some point, maybe, the U.S. will find it difficult to borrow.

The U.S. government never borrows.

At some point, interest costs may constrain policymakers.

The U.S. government has the infinite ability to pay interest.

At some point, bond investors may look at the U.S. political system and decide there’s a real risk they won’t get paid back—then begin demanding higher interest rates.

That only could happen if we continue with the astoundingly stupid, totally unnecessary, absolutely harmful “debt ceiling.”

“It’s going to be a 2029, 2030 exercise,” said Schneider of Piper Sandler.

Write to Richard Rubin at richard.rubin@wsj.com

It will be worse if publications like the Wall Street Journal continue printing lies, politicians continue speaking lies, and economists continue teaching lies to fool the public.

{kind=link}