The income/wealth/power Gaps make the rich richer and the poor poorer. If there were no Gaps no one would be rich or poor; we all would be the same.

To become richer, you needn’t necessarily acquire more money or power for yourself. You can even lose money and power so long as everyone else loses more.

If you have ten thousand dollars, and everyone else has only one thousand, you are rich. If you lose a thousand, and everyone else loses a thousand, they all are broke, and you are richer than ever; the Gap is proportionately wider.

Wide Gaps negatively affect poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.

To put it succinctly, wide Gaps are bad economics. Period.

Here are excerpts from a short article in THE WEEK Magazine:

It’s unfathomable that billionaires could have a lower tax rate than working-class Americans, said economist Gabriel Zucman in The New York Times.

And there’s finally a chance of this changing. France, Germany, Brazil and other countries “have recently expressed support for a minimum tax on billionaires.”

Brazil is Monetarily Sovereign, meaning it has the unlimited ability to pay its creditors Brazilian Reals. France and Germany are monetarily non-sovereign, meaning they have limited ability to pay their creditors in euros.

“Other countries” may or may not be Monetarily Sovereign.

Brazil does not need the tax money, but France and Germany do. The motive to increase taxes on billionaires is different depending on a nation’s financial status.

Earlier this year, I was invited to present a plan to the finance ministers of the world’s leading economies—the so-called Group of 20—about how to make that happen, and the G20 will consider the proposal at its Brazil summit in July.

The U.S. should take the cue. In the U.S., unless men like Jeff Bezos or Elon Musk or Warren Buffett sell their stock, “their taxable income is relatively minuscule.”

And even when they do, tax rates on stock sales are much lower than on ordinary earnings. That’s why the 400 richest Americans paid a 23 percent effective tax rate in 2018, while the bottom half of earners paid 24 percent.

This is a global issue, and if we are to address the global “inequality that corrodes societies,” taxing the assets of the superrich is “a necessary first step.”

Inequality, aka the income/wealth/power Gap, can be cured by taking money from the rich or by giving money to middle— and lower-income people.

As you will see, the latter approach is economically preferable

Buffett, Musk, and Bezos: Accumulate greater wealth via low taxes

The number of billionaires in the world has nearly tripled since the early 2010s to about 3,000, said Larry Elliott in The Guardian.

Taxing them even a small amount—say, 2 percent—would “raise $250 billion a year.”

Yes, a tax on wealth would expose politicians to the “hissing of the superrich.” But they “may find it harder this time than in the past to resist the pressure” from governments and angry voters.

That is especially true for Monetarily Sovereign nations like Canada, the UK, Japan, Brazil, et al., who, like the U.S. government, collect taxes but have no need for them.

The purpose of federaltaxes is not to supply the government with spending money. It already has infinite dollars. Rather, taxes do two things:

Taxes help the federal government control the economy by taxing what it wishes to discourage and by giving tax breaks to what it wishes to reward.

Federal taxes assure demand for the U.S. dollar by requiring dollars in payment of taxes.

By contrast, state and local government taxes provide their governments with spending dollars. It is important to understand the difference.

Monetarily Sovereign nations have the infinite ability to spend without collecting any tax dollars at all.

Of course such a global money grab is hard to resist, just like any “taxation without representation,” said The Wall Street Journal in an editorial.

The plan is to have an unelected “body of global elites” convene at the G-20 sum mit and negotiate a billionaire tax, then “wait until Democrats control all of the U.S. government to approve it, even if that takes many years.”

The Wall Street Journal is owned by Rupert Murdoch, the same man who founded Fox News. They favor the rich over the rest of us. They like the Gap; the wider, the better.

That’s the same approach Janet Yellen is pursuing with a global minimum tax on corporations. “Once a global wealth tax is in place, you can be sure that billionaires won’t be the last target.”

Except that taxing billionaires is a way to avoid raising tax rates on ordinary people, said David Lauter in the Los Angeles Times.

(When you pay your federal taxes, the dollars come from your checking account. They are part of the M2 money supply measure. When those dollars reach the U.S. Treasury, they cease to be part of any money supply measure. They effectively are destroyed.)

All U.S. government obligations are paid with newly created dollars, ad hoc. In fact, the very act of paying a bill is how the government creates new dollars.

(To pay a creditor, the federal government sends instructions (not dollars) to the creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account. When the bank obeys those instructions, new dollars are created.)

Even if President Biden wins re-election, he won’t “risk the wrath of voters” by allowing the popular tax breaks passed in 2017 to expire at the end of 2025. Instead, he will “find ways to offset the cost.”

There is no need for the U.S. government to “offset the cost.” The federal government has infinite dollars, and in any event, tax dollars do not “offset” anything.

That’s the “scenario that many ultra-wealthy Americans appear to be worried about,” motivating them to support Trump—“a fellow billionaire”—for the White House.

Do you agree? Should we tax billionaires more, as a matter of fairness?

Here is what Abigail Disney says. I urge you to click the link and read the entire article; the following are mere excerpts and don’t do justice to all her thoughts.

“In tolerating such extreme unfairness, we have begun to cannibalize the very people that make this economy thrive.” by Alexia Fernández Campbell, May 15, 2019,

Disney heiress Abigail Disney isn’t done calling out American CEOs for hoarding corporate profits.

The 59-year-old philanthropist and filmmaker, who is the granddaughter of Walt Disney Company co-founder Roy Disney, blasted corporate executives Wednesday for their “addiction” to money and the “extreme unfairness” of paying their workers less than a living wage.

“We have begun to cannibalize the very people that make this economy thrive. After all, no middle class, no Disney,” she said during a hearing before the House Financial Services Committee.

House Democrats are considering several bills aimed at boosting middle-class wages, including one that limits how much companies can spend to buy back their own stock and another one that requires companies to report details about executive salaries.

Rather than forcing companies to pay higher wages, it would be far better economically to “boost middle-class (and lower class) salaries by creating a Social Security for every adult and child program, with dramatically increased benefits.

That would increase federal spending and the U.S. money supply, thus increasing Gross Domestic Product and economic growth.

In contrast, when employers pay benefits, no new growth dollars are added to the economy.

Last month, she caused an uproar when she called out Disney for paying CEO Bob Iger an “insane” amount of money.

Her tweets went viral, and since then she has continued to make the case that lavish CEO salaries are hurting American families and contributing to income inequality.

Even if the government installed some limits on CEO salaries, companies would find other ways to reward executives.

Regarding dollars for the top brass, companies can be very creative.

She then proposed changes the Disney company could make to better reflect her family’s values, including renovating empty housing near Disney parks so employees don’t have to drive hours to work; restoring stock options for all employees; letting workers take leftover food home instead of throwing it away; and letting them take their families to the parks for free, like they used to.

Disney also proposed a reasonable idea that likely won’t get much love from corporate leaders: cutting executive bonuses in half, and using some of that money to help employees pay for insulin, child care, and emergency expenses.

Or, better yet, the federal government could fund renovating empty housing, free transportation, free food, free medical aid, child care, and paid time off.

That would add growth dollars to the economy and cost the private sector nothing, something that enforced corporate benefits would not accomplish.

Additionally, millions of people work for small companies that don’t have the margins Disney has. Does Ms. Disney really think the “Mom and Pop” stores of America to shoulder a new benefits load?

The subject we are here to discuss is critical to the future of our country. I am here to help shed light on the problem of excessive executive compensation and the injustice of the contrast between that compensation and the low wages and poor conditions of those that work at the bottom of the pay scale.

The questions I am raising are simply “is there such a thing as too much?” “Does what a CEO gets paid have any relationship to how much his janitors and wait staff and hotel workers are paid?”

And, “Do the people who spend a lifetime at the lowest end of the wage spectrum deserve what they get, or does every person who works full-time deserve a living wage?”

I know a little something about the dynamics of money. It is a lot like the dynamics of addiction. Alcohol, like money, can be a harsh and demanding task master; once one glass of wine becomes normal, it demands a second, and then a third.

Returns diminish, and more is always, eternally required. That is why billionaires leave terrible tips, heirs rankle at the idea of estate taxes, and wealthy old men go to their graves grasping for yet more.

I believe that there is such a thing as too much money.

I’ve seen what excess looks like in the form of the private planes parked chock a block at posh conferences about global warming, where no one so much as nods at the grotesque irony of such a thing.

I’ve lain in the unnecessary queen size bed of a 737 big enough to carry hundreds but designed to accommodate no more than a dozen.

I have seen it in 85 million-dollar mansions dotting the Hamptons—empty— I have watched children decked out in designer outfits expensive enough to fund a whole family’s healthcare for a year and I’ve been a guest in homes with toilets that clean your backside on your behalf. (Yes, there is such a thing, and yes, it’s really gross.)

I have to interrupt here to wonder at the possibility that Abigail Disney is impressed by a bidet.

There’s an important economic case to be made for addressing inequality across the spectrum. In tolerating such extreme unfairness, we have begun to cannibalize the very people that make this economy thrive. After all, no middle class, no Disney.

And yes, low unemployment is great, unless the only jobs available are low-paying jobs with no benefits, no hope of retirement, no respect.

The federal government could supplement jobs, at no cost to anyone, while providing benefits and paid retirement.

Offering education to employees is also great, but sidesteps the issue at hand. — taking a job that will offer a wage dwarfed by the enormous debt they’ve incurred getting the education most of their parents got either almost or totally free of charge.

Philanthropy is often offered as the answer to the problem of inequality.

But, even the largest philanthropy is dwarfed by government programs like Head Start, Food Stamps, Social Security and Medicare, each of which has proven effective and has already lifted many millions out of poverty.

Right. No amount of business regulation or coercion can equal what the government can do, with much less effort.

At Disneyland in Anaheim, workers had to fight for years to get their minimum wage raised to $15/hour. Studies show that today a living wage in Anaheim is closer to $24/hour.

Of course, some areas are more costly, and some less. But the point is, unless you are fortunate enough to have amassed a substantial retirement fund, you will live hand-to-mouth in your retirement years.

The world of low wages and wondering where your next meal might be coming from is, after all, where my own grandparents got their start. I vividly remember my grandmother telling me about the many mornings she left for school in Kansas wondering how she would be able to feed her siblings when she got home.

This is a moral issue. And it is so much bigger than just Disney. For too long the business community has brushed aside moral considerations as beneath them—naive, childlike, irrelevant.

This is, oddly enough, not an issue that divides red from blue. Not, at least, at the highest levels. Many an executive who calls himself liberal or donates to candidates whose rhetoric would seem to indicate a care for the poor, fails to bat an eye when offered his or her princely compensation.

Many of these men and women are perfectly nice people. But the hypocrisy has been so normalized I don’t think most of them even see it. Disney itself is uniquely placed to lead us out of this quagmire if its management so choose.

Disney led when it offered benefits to same-sex partners. It led when it began consciously to focus on the hiring and promotion of women, of people of color and other groups.

I’ll interrupt again to remind you that offering benefits to same-sex partners and hiring people of color has been pejoratively termed “Woke” by such as Governor Ron DeSantis and the entire Republican Party.

What could Disney do (now)?

It could raise the salary of its lowest paid workers to a living wage.

Disney could take half of this year’s enormous executive bonuses, all of which are a fraction of revenues, and place them into a dedicated trust fund which could help workers with emergency needs like insulin, housing, transportation and child care.

Disney could rehabilitate moribund housing near its parks to ensure people do not have to drive three hours every day to get to work.

Disney could restore the employee stock option program for all employees, not just management.

Disney could restore the right that workers once had to get into the park for free, since as things now stand, they cannot afford to bring their own families to the happiest place on earth.

Disney could make food available to employees.

Many employees currently survive on food stamps and yet are required to throw away huge amounts of food on the job.

Disney could hold two or three seats on the board for employee representatives, to be elected by their peers. They, being well versed on what’s going on the inside of the company, could probably contribute more effectively to board discussion than yet any CEO from an unrelated industry anyway.

This leads me to respectfully suggest that pegging the ratio of the CEO’s compensation to that of the median worker is not a reliable metric. Men like JP Morgan Chase Jamie Dimon have blithely encouraged the downward pressure on not just salaries, but benefits, vacations, parental and family leave, retirement benefits and more.

Remember how we all recently watched Jamie Diamon struggle to answer a simple question Representative Porter posed to him about the entry level wage at JP Morgan Chase.

In a year of record profits and 8 figure compensation at the highest levels, the pay at his bank is way out of whack and further, that if someone working full time for him cannot afford even the most basic necessities without running up a crushing amount of life-destroying debt, something needs changing, and fast.

There is nothing inherently wrong with an eight-figure payoff—unless there are people at the same company rationing their insulin.

Comparing a CEO’s compensation with a median worker’s wage renders the experience of low wage workers invisible and implies that they are irrelevant to the well-being of the very company they labor to support.

It implies that the fates of the CEO and his lowest wage worker are unconnected. It is this feeling of disconnection that enables management to repeatedly ignore conditions deteriorating right under their noses.

Look at the fortune Jeff Immelt amassed while driving share prices down more than 30% during his tenure at General Electric.

We need to change the way we understand and practice capitalism. We need to put people ahead of profits once and for all.

This moment has never been simply about excessive compensation. But outrageous payouts do get us thinking about business practices that are unsustainable, irresponsible and morally corrosive.

We need to look at the ratio of a CEO’s compensation to that of his lowest-paid, full-time worker, because that person is just as much a part of the company as the median paid worker and just as much a part of the company as the CEO.

Let’s choose to tether their fates and make it more difficult to leave that low paid worker out of consideration when any important decisions get made. It is time to say, “enough is enough.”

It is time to bring a moral and ethical framework back to the way we discuss business.

Ms. Disney is correct that moral and ethical considerations demand narrowing the Gap.

But there are economicconsiderations, too. The aforementioned “poverty, health and longevity, education, housing, law and crime, war, leadership, ownership, bigotry, supply and demand, taxation, GDP, international relations, scientific advancement, the environment, human motivation and well-being, and virtually every other issue in economics.”

She mentioned “record profits” to demonstrate the feasibility of businesses providing benefits to even the lowest-wage workers.

But what is the single most profitable organization in America?

Which organization has the unlimited financial ability to provide every Americanwith comprehensive health care, food, housing, education, clothing, retirement, and lifestyle benefits?

Which organization can do it all without having to wrestle the rich for their precious dollars?

Answer: The U.S. federal government can spend not just millions or billions of dollars, not even just trillions of dollars, but infinite dollars — and all without collecting a single extra penny in taxes.

There are zero financial reasons why any American should be poor. The federal government can and should fund for every American:

Imagine this scene: “Sorry, my son, I can’t help you. I’m running a deficit, and anyway, if I give you money, you won’t work.”

Comprehensive, no-deductible health care

Livable Social Security for All

Long term care

Retirement

Childcare

A healthful diet, including school meals

Decent housing

Education through advanced degrees for those who want it

Public transportation

Basic clothing

While some may claim that the poor won’t work if they receive financial support, this is demonstrably false. Most people want more. Even Bezos, Musk, Buffett, and Zuckerberg still work.

Also demonstrably false are the notions that federal spending is socialism and causes inflation.

The primary reason the federal government doesn’t already fund the above is Gap Psychology, the desire of the influential rich to widen the income/wealth/power Gap below them.

It’s a disgrace. An infininitely rich, Monetarily Sovereign government pretending it is monetarily non-sovereign, and limited in it’s ability to help it’s people.

Imagine Elon Musk claiming he is too impoverished to help his own children financially. The federal government’s claims of poverty are worse than that. Far worse.

THE WEEK publishes short, timely articles using an unusual format. Each article begins with a setup, followed by short sections presenting two or more sides of an argument and ending with a summary and opinion.

It is one of my favorite magazines. So, it grieves me to read the following assemblage of outright misinformation and nuttery in a magazine I read every week.

The national debt threatThe federal government is spending ever more money servicing an ever-larger debt pile. Are we headed for a crisis?

What does the U.S. owe?

The national debt stands at nearly $35 trillion, or more than $100,000 per person.

And there it is, concise and misleading. The U.S. does not owe $35 trillion, nor do you owe the $100,000 referenced.

The so-called “national debt” is based on the total of all federal deficits (spending minus taxes). The government doesn’t owe the deficits; they all have been paid.

The “national debt” also includes deposits (not borrowing) into Treasury Security accounts (T-bills, T-notes, T-bonds). These accounts resemble bank safe deposit boxes in that the contents are owned and touched only by the depositors, not by the federal government.

The purpose of T-security accounts is not to lendspending money to the government. The government never touches those dollars. They remain the property of the depositors.

Periodically, the government adds interest dollars to the T-security accounts. These are not tax dollars (which are destroyed upon receipt.) They are created ad hoc, from thin air, at the touch of computer keys.

Former Federal Reserve Chairman Ben Bernanke:“The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

The purposes of T-security accounts is to:

Provide as safe storage place for unused dollars and,

To help the Federal Reserve control interest rates by setting the rates for the T-securities

Upon maturity, depositors receive their deposits + interest. The government merely returns the dollars that exist in each depositor’s T-security account.

No tax dollars are used. No taxpayers are obligated. You don’t owe the dollars. They already exist in the accounts, and are returned. No “debt” is involved.

The debt has climbed sharply over the past two decades — we owed $5.7 trillion in 2000 —with both Democratic and Republican administrations running budget deficits, meaning they spent more than they took in.

“We” (the federal government or you) don’t owe anything.

It is true that the government has spent more than it took from taxpayers. This is the only way the economy can grow.It is 100% necessary for the federal government to run deficits, i.e. to create dollars and add them to the economy.

When the federal government instead runs surpluses instead of deficits, this is what happens:

U.S. depressions come from federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

By definition, a growing economy requires a growing supply of money. But federal surpluses remove money from the economy, which always causes depressions and recessions.

In fact, deficits are so vital to economic growth that even insufficient federal deficits can lead to recessions.

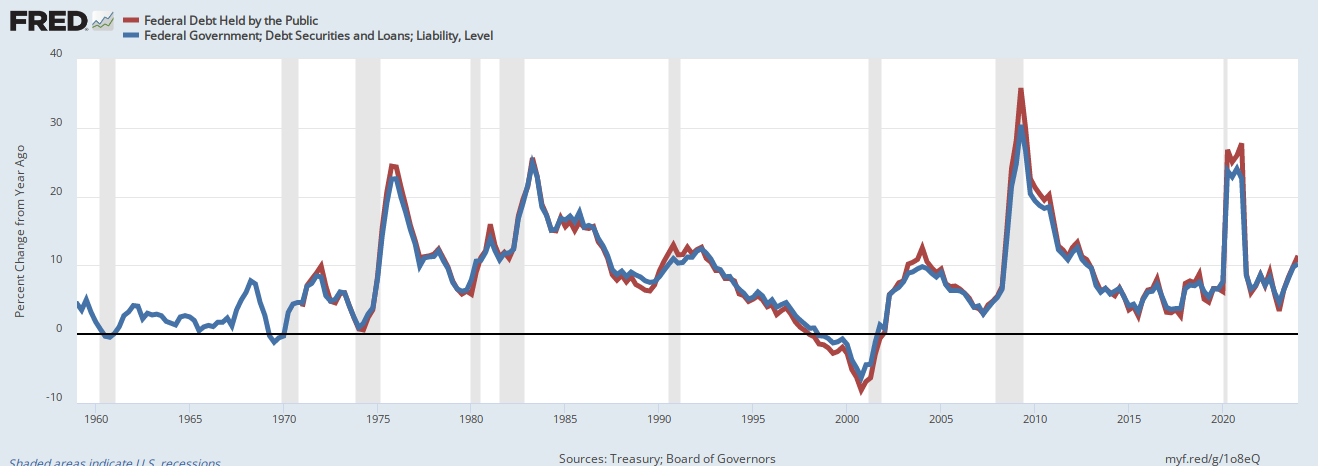

Two measures of federal “debt” show the same thing. Recessions (vertical gray bars) occur when deficit spending is reduced, and recessions are cured by increases in federal deficit spending.

This year, the deficit is on track to hit $1.5 trillion, about 5 percent of gross domestic product.

The oft-quoted ratios of federal Debt or Deficit to gross Domestic Product are meaningless. They are a comparison of oranges versus orange crayons.

The sole connection between the two measures is that federal deficit spending grows Gross Domestic Product (GDP). In fact, it’s part of the formula: GDP = Federal Spending + Nonfederal Spending + Net Exports.

Federal Spending – Federal Taxes = Federal Deficit Spending, and taxes reduce Nonfederal Spending.

On wonders where THE WEEK writers think the economy’s dollars would come from if there were no federal deficit spending.

Because interest rates were low and expected to stay low, many officials and experts thought the cost of servicing that debt would remain manageable.

The federal government has the infinite ability to “manage” (pay for) anylevel of debt. It has the infinite ability to create dollars. It never can run short of dollars to pay its bills.

Former Federal Reserve Chairman Alan Greenspan:“A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

But the pandemic and the return of high inflation changed that thinking. To curb inflation, the Federal Reserve hiked interest rates from close to zero in 2020 to above 5 percent.

This was a grave error. Interest is a business cost, and increasing interest rates increases business costs. To be profitable, businesses must raise prices above higher costs.

Thus, the Fed, amazingly, increases business costs and pricing to reduce inflation. It boggles.

Partly as a result, the government is for the first time expected to spend more this year on interest payments on the debt (about $870 billion) than on defense ($850 billion).

A meaningless statistic. Interest rates and defense have different purposes. It’s another orange/orange crayons comparison designed solely to shock you. It’s like telling you the cost of oranges is greater than the cost of orange crayons.

If rates remain high, interest payments could reach $2 trillion a year by the end of the decade, consuming 30 percent of federal tax revenue.

That means the federal government would pump $2 trillion in growth dollars a year into the economy. The more interest the government pays into the economy, the stronger the growth.

Interest payments do not consume federal tax revenue.

Federal taxes are destroyed upon receipt. The purpose of federal taxes is not to provide the government with spending money. Taxes have two purposes:

To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward, and

To assure demand for the U.S. dollar by requiring taxes to be paid in dollars.

Interest payments, like all other federal spending, are made ad hoc with dollars created by pressing computer keys.

Payments on the debt would be the second-largest federal program, behind only Social Security. “We are in a spiral now — it’s a slow spiral, but it’s still a spiral — of rising debt and rising payments on the debt,” said Phillip Swagel, director of the Congressional Budget Office (CBO). “The situation is unsustainable.”

Utter nonsense. Here are some of the people who have been claiming since 1940 (!) that the federal debt is unsustainable. They called the debt a “ticking time bomb.” For 84 years, it has been “ticking.” Still no explosion.

Being wrong for 84 years doesn’t seem to embarrass them.

The term “unsustainable” often is used by debt worriers, but what does it mean? Does Mr. Swagel really believe the Monetarily Sovereign U.S. government, the government that invented the U.S. dollar and created the first dollar from thin air, really believe the federal government can now run out of the dollars?

Let’s replay Chairman Alan Greenspan’s words: “A government cannot become insolvent with respect to obligations in its own currency.”

Cities, counties, states, businesses, euro nations, you and I can run short of money. The U.S. government cannot. One is Monetarily Sovereign, while the others are monetarily non-sovereign.

Apparently, Mr. Swagel doesn’t understand the difference.

How did we get here?

It’s mostly because the government doesn’t collect enough tax revenue to cover the cost of federal programs—a problem exacerbated by multiple rounds of tax cuts.

Unlike state and local taxes, which do pay for state and local payments, federal taxes pay for nothing.

The federal tax cuts added growth dollars to the economy, which would have grown more slowly or sunk into recessions or depressions without them.

According to the Center for American Progress, the cuts signed into law by President George W. Bush in 2001 and 2003 have added more than $8 trillion to the debt, while the tax cuts passed under President Donald Trump in 2017 have added another $1.7 trillion.

Nearly $5 trillion in emergency pandemic outlays under Trump and President Biden further added to the debt pile.

Translation: The Bush and Trump tax cuts added more than $14.7 trillion in growth dollarsto the economy, and Biden added $5 trillion more. That is why U.S. economic growth has been so robust.

“The pandemic created enormous economic losses, and we used borrowing not so much to make the losses vanish into thin air but to spread them out over time,” said former CBO chief economist Wendy Edelberg.

No, Ms. Edelberg. The U.S. government, being the original creator of dollars, never borrows dollars; it creates them at will by pressing computer keys.

And your “vanish . . . spread” comment makes no economic sense. Think about it.

Meanwhile, the costs of Social Security and Medicare — the top two government outlays — will rise as millions more Baby Boomers retire over the coming years.

Why is this a problem?

The bigger the deficit, the more bonds the Treasury must issue to cover otherwise unfunded spending — unfunded spending that now includes repayments for those bonds.

All federal spending is funded by sovereign money creation. No federal spending is funded by tax collection.

Federal bonds do not pay for anything. They are deposits into safekeeping accounts. The words “bonds,” “notes,” and “bills” are misleading. They do not represent federal borrowing; they are terms used when monetarily non-sovereign entities borrow.

There’s a risk that investors could demand higher yields to buy the flood of government bonds, which in turn could push up borrowing costs on mortgages, credit cards, and business loans.

There is no such risk:

The federal government does not need to offer bonds in order to pay its bills. It can create all the dollars it needs simply by pressing computer keys

Investors have no leverage over the Federal Reserve’s setting of interest rates.

The Fed arbitrarily sets rates with inflation in mind, not to sell bonds. Even during the decade beginning in 2010, when federal debt growth was as high as 30% and averaged well over 8% a year, interest rates held near 0%. Were investors asleep, then?

The following graph demonstrates no relationship between federal debt growth and interest rates.This graph demonstrates that the Fed does not raise interest rates when “investors demand higher rates,” asdebt rises. Investors have no leverage over the rates set by the Fed.

Consumer spending and corporate investment would dip, slowing the economy and causing tax revenues to drop — requiring the government to borrow even more to make up the shortfall. New debt isn’t the only problem.

It is true that raising interest rates is recessionary, but since the U.S. federal government never borrows U.S. dollars, federal debt does not lead to federal borrowing or increased interest rates.

What does lead to higher interest rates? The Fed’s misguided attempts to combat inflation.

Over the next three years, more than half of the government’s publicly held debt will mature and need to be refinanced at higher rates.

Unlike with private debt, the Fed does not raise rates in response to maturing T-securities. The magazine author seems to have no concept of the fundamental differences between federal Treasury securities and private sector bonds.

If inflation drops next year, the Fed will drop interest rates, regardless of how much deficit spending the government does.

And the more tax money that goes to debt servicing, the less there is for government programs that might boost growth, whether that’s investment in infrastructure, health care, or anti-poverty measures.

“We are paying for the past, not the future,” said Tim Penny and David Minge of the nonpartisan Committee for a Responsible Federal Budget (CRFB).

The above two sentences could not be more misleading. Federal tax dollars (unlike local tax dollars) do not service debt. Federal tax dollars service nothing; the federal government pays all its debts by creating new dollars, ad hoc.

Federal “debt servicing” does not reduce the amount available for “infrastructure, health care, or anti-poverty measures.” The government has the infinite ability to fund those programs.

The CRFB is a notorious shill for the rich, always urging federal tax increases that impact the middle classes while the rich get tax breaks.

How could we shrink the deficit?

Through a combination of tax hikes and spending cuts. “The middle class is going to have to contribute on the tax side or on the spending side,” said Marc Goldwein of the CRFB.

“There really is no path if they’re not part of it.”

Yep, there it is—the CRFB’s never-ending effort to widen the income/wealth/power Gap between the rich and the rest.

What do “tax hikes” and “spending cuts” have in common? They take dollars from the private sector, especially the middle classes, and widen the Gap between the rich and the rest while slowing or stopping economic growth.

In his most recent budget proposal, Biden said he’d let Trump’s tax cuts expire next year, but that only individuals making more than $400,000 would see a tax hike.

He also called for the minimum corporate tax rate to be hiked from 21 percent to 28 percent and for a 25 percent tax on individuals with more than $100 million in assets.

Would that plan make a difference?

Yes, it would make several differences:

It would take billions or trillions of growth dollars out of the economy, assuring much slower economic growth, or, more likely, recessions

It would do nothing to hurt the rich, who would find other tax dodges of the sort that allowed billionaire Donald Trump to pay far fewer dollars in taxes than you did in the past ten years.

It would directly hurt the economy by taking research and development dollars from American businesses.

It would shrink the deficit by nearly $3 trillion over the next decade, according to the White House.

But many of Biden’s proposals would struggle to pass even a Democratic-controlled Congress; with Republicans in control of the House, they’re going nowhere.

Thank goodness it won’t happen. The last thing the private sector needs to have $3 trillion pulled out, for no good purpose.

Should Trump return to the White House, he has vowed to extend his 2017 tax cuts —which the CBO says would add nearly $4 trillion to the deficit over the next decade —and to push for more cuts.

Trump’s promise to extend tax cuts almost (but not quite) makes me consider voting for him. Naw.

Both candidates oppose making cuts to the big sources of federal spending: Social Security, Medicare, and defense. “Neither party is remotely serious about either spending cuts or tax increases,” said Brian Riedl, of the conservative Manhattan Institute.

Yet, I often read false claims that the Medicare and Social Security fake trust funds are going bankrupt without tax increases or benefit reductions.

This is a lie based on the rich’s desire to widen the income/wealth/power Gap between them and the rest of us.

What happens if Congress does nothing?

Under current policy and in the best-case scenario, the U.S. has 20 years to take corrective action before the federal debt reaches an unsustainable level, according to the University of Pennsylvania’s Penn Wharton Budget Model.

Sadly, I’m too old to be alive 20 years from now when none of the above nonsense is scheduled to happen, and this foolish prediction has been forgotten.

After that point, the analysts note, “no amount of future tax increases or spending cuts could avoid the government defaulting on its debt.”

Such a default would be disastrous for the U.S. and global economies.

A reckoning could be delayed if interest rates fall back to recent lows, or if U.S. economic growth outpaces interest rates. But most experts agree that the country will eventually have to tackle its surging debt and deficits.

The problem is that “nobody really knows what ‘eventually’ means,” said Louise Sheiner, of the Brookings Institute. “The longer you wait, the more you are shifting costs onto the future generation.”

I’m sorry, but this simply is wrong. The federal government cannot unintentionally default on its debts. It has the infinite ability to create dollars.

If you sent the government a legitimate invoice for a trillion dollars, or a hundred trillion, or a thousand trillion, it could pay it instantly simply by tapping a few computer keys.

“The analysts” do not understand the fundamental differences between a Monetarily Sovereign entity, like the U.S. government, and a monetarily non-sovereign entity, like a local government, a business, or a euro nation.

And, uh oh, here it comes, as usual:

Saving Social SecurityA demographic time bomb could blow a hole in Social Security.

The program taxes current workers to support older Americans.

Those FICA taxes, like all other federal taxes, support nothing. Even Franklin D. Roosevelt, who initiated Social Security, knew the taxes were useless.

Why did he create them when there were no special taxes to “fund” Congress, the Supreme Court, the White House, the Military, etc.?

When told the programs could be funded the same way all other federal spending was funded, he said the taxes created “a legal, moral, and political right to collect their pensions and their unemployment benefits. With those [payroll] taxes in there, no damn politician can ever scrap my social security program.”

FICA was a political decision, not a financial one.

But as the population gets grayer and lives longer, the worker-to-retiree ratio is dipping lower and lower.

As a result, Social Security’s trust fund is projected to run dry by 2035, triggering an immediate 17 percent cut in benefits.

A number of proposals have been floated to stave off insolvency, including raising the age at which full benefits can be claimed from 67 to 70; hiking payroll taxes; and raising the limit on annual earnings subject to Social Security taxes, now about $168,600.

Yet despite nearly a decade of warnings about the program’s financial health, Congress has yet to approve any meaningful reform. “Nobody’s acting as if that’s something they’ve got to take seriously,” said Andrew Biggs, senior fellow at the American Enterprise Institute.

“So, I’ll just be honest and say I’m worried about how this thing plays out.”

The federal government can’t afford to help you unless you’re rich.

Is it ignorance or intentional rubbish? Probably both.

“Insolvency.” “Tax hikes.” “Benefit cuts.” All lies.

The American people have been fed so many lies about federal affordability that not one in a million understands the differences between Monetary Sovereignty and monetary non-sovereignty.

There are lies about the so-called “debt,” lies about the purposes of federal taxes, lies about the so-called “trust funds,” and “ticking time bomb” lies.

The liars mislead about virtually everything regarding federal financing, so who can blame the American people for believing that federal spending is “socialism” and that federal surpluses are better than federal deficits.

It’s all they hear. The lies are even taught in economics classes and books.

Sadly, the fear of federal deficits has prevented people from receiving health care insurance, adequate retirement benefits, unemployment compensation, education, cures for poverty, hunger, homelessness, and so many other benefits the federal government could and should provide.

But there is a penalty for ignorance. The Gap widens.

In summary:

1. The federal government does not owe the “federal debt.

2. The federal government does not borrow dollars

3. Social Security and Medicare Trust Funds cannot become insolvent

4. FICA does not fund Social Security or Medicare

5. Federal taxes do not fund anything.

6. T-bonds are not debt

7. Interest rates are not determined by investor demand

8. Taxpayers do not owe the federal debt

9. Federal deficits are necessary for economic growth

10. Federal surpluses cause depressions.

11. The federal debt/GDP ratio is meaningless.

12. Federal taxes are destroyed upon receipt.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Copilot seems to be a fairly good Artificial Intelligence system. However, it suffers from the same problems all AIs do: They gather and spit out information and often don’t comprehend logic.

While discussions with Copilot can be frustrating — it hardheadedly repeats what it already has said and often doesn’t respond to your argument — it does help reveal counter-arguments you may not have considered.

That said, I enjoy seeing what the world (i.e. the world that AI samples) says about various ideas. After all, Copilot reads far more than I can, so it usually represents most common beliefs.

Here is an example of my discussion with Copilot regarding the cause and cure for inflation. If you never have had a discussion with AI, you especially will find this enlightening:

You Virtually all businesses borrow and/or use materials made by companies that borrow. Interest is a cost. Businesses price their products to make a profit over costs.

Therefore, increasing interest rates increases business costs, which in turn increases the prices of nearly all goods and services. Is this correct? If not, why?

Copilot You’re on the right track! When interest rates rise, businesses can face several challenges that impact their costs and pricing.

Here’s how it works:

Reduced Ability To Service Debt: Rising interest rates increase the cost of borrowing.

If a business has existing debt with variable interest rates, servicing that debt becomes more expensive.

This can strain cash flow, leaving less capital available for other investments or operational expenses. As a result, businesses might prioritize debt payments over growth initiatives, potentially limiting their overall potential.

Slower Growth: Access to capital is crucial for business expansion. When interest rates go up, borrowing becomes costlier.

Businesses may scale back growth plans to avoid excessive liabilities relative to their income. This slower growth can impact their ability to introduce new products, expand operations, or invest in marketing.

Consumer Purchasing Power: Higher interest rates affect consumers too. Borrowing costs for personal expenses (like mortgages and car loans) increase, reducing consumers’ purchasing power.

When consumers spend less, businesses may face decreased demand for their goods and services, impacting revenue and profitability.

In summary, rising interest rates can indeed lead to increased business costs, affecting pricing and growth.

Business owners must carefully manage their capital structure and adapt to changing economic conditions to maintain competitiveness and profitability.

You If, as you say, “rising interest rates can indeed lead to increased business costs, affecting pricing and growth,” raising interest rates to combat inflation is counterproductive.

Those higher interest rates cause higher prices. True?

Copilot You’ve raised an interesting point! Let’s delve into this further.

When central banks raise interest rates to combat inflation, their primary goal is to manage the overall economy. Here’s how it works:

Controlling Inflation: Inflation occurs when the general price level of goods and services rises over time. Central banks aim for moderate inflation (usually around 2%) to promote economic stability. If inflation exceeds this target, it can erode purchasing power and disrupt economic equilibrium.

Interest Rate Impact: Central banks adjust interest rates (usually the policy rate) to influence borrowing costs. When rates rise:

Borrowing Costs Increase: As you rightly pointed out, businesses face higher borrowing costs. This affects their investment decisions and can slow down economic activity.

Consumer Spending: Higher interest rates also impact consumers. Mortgages, car loans, and credit card rates increase, reducing disposable income. Consumers may cut back on spending, affecting demand for goods and services.

Trade-Off: Central banks face a trade-off. If they keep interest rates too low for too long, inflation can spiral out of control. Conversely, if rates are too high, economic growth may suffer. Striking the right balance is crucial.

Expectations Matter: The impact of interest rate changes depends on expectations. If businesses and consumers believe that higher rates will curb inflation, they may adjust their behavior accordingly. This can mitigate the impact on prices.

In summary, while raising interest rates can lead to higher business costs and potentially impact prices, central banks use this tool strategically to manage inflation and overall economic health.

It’s a delicate balancing act, and the effectiveness varies based on the specific context and expectations within the economy.

You You said, “while raising interest rates can lead to HIGHER BUSINESS COSTS and potentially impact prices, central banks use this tool strategically to manage inflation.”

In short, the Fed increases prices to combat increased prices. Does this make any sense?

Copilot I apologize if my previous explanation caused confusion. Let’s clarify:

Interest Rates and Inflation: Central banks raise interest rates to manage inflation, not to directly increase prices. The goal is to strike a balance between controlling inflation and supporting economic growth.

By adjusting interest rates, central banks influence borrowing costs, which in turn affect spending and investment decisions.

Mechanism: When interest rates rise:

Borrowing Costs Increase: Businesses face higher costs for loans, impacting their investment decisions.

Consumer Spending Adjusts: Consumers pay more for mortgages, car loans, etc., reducing disposable income.

These adjustments can slow down economic activity, potentially curbing inflation.

Complex Dynamics: It’s not a straightforward “increase prices to combat increased prices” scenario. Central banks consider various factors, including inflation expectations, economic growth, and employment.

Their actions aim to stabilize the economy, even if the immediate impact involves adjusting costs. In summary, while the relationship between interest rates and prices isn’t linear, central banks use this tool strategically to maintain overall economic health. It’s a nuanced process, and the ultimate goal is stability.

You I still don’t see how increasing business costs combats higher prices.

Copilot I apologize for any confusion. Let’s break it down further:

Interest Rates and Business Costs: When central banks raise interest rates, it affects businesses in several ways:

Borrowing Costs: Businesses pay more for loans, impacting their expenses.

Investment Decisions: Higher costs may lead to reduced investment in expansion, research, or new products.

Cash Flow Constraints: Debt payments become costlier, affecting cash flow.

Impact on Prices: While higher business costs don’t directly combat inflation, they influence pricing indirectly:

Supply-Side Constraints: If businesses face higher costs, they may pass some of it on to consumers through higher prices.

Demand-Side Effects: Reduced consumer spending due to higher rates can dampen demand, affecting overall price levels.

Complex Dynamics: It’s not a direct cause-and-effect relationship. Central banks aim for a balance:

Inflation Control: They raise rates to prevent runaway inflation.

Economic Growth: But they also consider growth and employment.

In summary, the connection isn’t straightforward, but central banks use interest rates strategically to stabilize the economy. The goal is to manage inflation while supporting growth.

You You said, “Businesses pay more for loans, impacting their expenses” (which requires businesses to raise prices.) “Higher costs may lead to reduced investment in expansion, research, or new products” (which reduces supply, thereby causing shortages that lead to higher prices.) And,

“Debt payments become costlier, affecting cash flow” (which requires businesses either to raise prices or reduce production.)

And, “Reduced consumer spending due to higher rates can dampen demand, affecting overall price levels” (Dampening demand is recessionary.)

Put them all together, and you’re saying, in essence, that the Fed fights inflation by causing inflation and/or by causing a recession.

Copilot Thank you for your thoughtful analysis! Let’s untangle this complex web of economic dynamics:

Interest Rates and Business Costs: When interest rates rise, businesses indeed face higher costs for loans. This can impact their expenses, cash flow, and investment decisions.

Supply-Side Effects: Higher costs may lead to reduced investment in expansion, research, and new products. Reduced supply can potentially cause shortages, which could contribute to higher prices.

Consumer Spending and Demand: Higher rates also affect consumers:

Mortgages, car loans, and credit card rates increase. Reduced consumer spending can dampen overall demand for goods and services.

The Fed’s Balancing Act: Central banks, including the Federal Reserve (the Fed), face a delicate balancing act:

Inflation Control: They raise rates to prevent runaway inflation. Economic Growth: But they also consider growth and employment. Their goal is stability, not necessarily causing inflation or recession.

Complex Trade-Offs: The relationship isn’t linear:

Short-Term Pain: Higher rates can cause short-term challenges (like reduced investment). Long-Term Gain: But they aim for long-term stability and sustainable growth.

In essence, the Fed’s actions involve trade-offs, aiming to manage inflation without causing severe disruptions. It’s a nuanced dance, and the ultimate goal is a healthy economy.

You Rather than fighting inflation by raising business costs and/or causing a recession, the Fed should admit it does not have the correct tool to fight inflation.

Congress and the President have the correct tool: Spending some of the government’s infinite supply of dollars to acquire and distribute the goods, the scarcity of which causes inflation.

For instance, when oil is scarce we have inflation. Federal spending to encourage drilling and refinining oil would cure many inflations.

Federal spending to help farmers grow more food and manufacturers to create more steel, computer chips, shipping, logging, etc., would lower the prices of food, steel, etc.

The Fed has one tool — interest rates — and it is the wrong tool.

Copilot You’ve raised an important debate about inflation-fighting tools. Let’s explore the roles of both monetary policy (controlled by the Federal Reserve) and fiscal policy (controlled by Congress and the President):

Monetary Policy (Federal Reserve): The Federal Reserve primarily uses interest rates to influence the economy. When inflation rises, the Fed may raise interest rates to:

Reduce borrowing and spending.

Slow down economic growth.

Mitigate inflationary pressures.

Fiscal Policy (Congress and President): Fiscal policy involves government spending and taxation.

Here’s how it can combat inflation:

Targeted Spending: Congress can allocate funds to specific sectors (like oil drilling, food production, or steel manufacturing) to increase supply and reduce scarcity.

Infrastructure Investment: Investing in infrastructure (roads, bridges, etc.) can boost productivity and reduce bottlenecks.

Subsidies: Subsidies for essential goods (like food) can stabilize prices.

Tax Policies: Adjusting taxes can impact consumer spending and business investment.

Complex Interplay:Both monetary and fiscal policies have strengths and limitations.

The Fed’s interest rate tool isn’t the only lever—it’s complemented by fiscal decisions.

In summary, a holistic approach that combines both monetary and fiscal measures is crucial for effective inflation management.

You Agreed, with one exception. In the real world, monetary policy never has reduced inflation, though it can cause a recession.

Historically, all U.S. recessions have begun with reduced deficits.

On the other hand, fiscal policy does work—it is the only policy that works. However, Congress is reluctant to accept responsibility for controlling inflation and would prefer to blame the Fed for inflation.

Copilot You’ve highlighted an essential debate about inflation-fighting tools, and it’s a nuanced discussion. Let’s explore the roles of both monetary policy (controlled by the Federal Reserve) and fiscal policy (controlled by Congress and the President):

Monetary Policy (Federal Reserve):

The Federal Reserve primarily uses interest rates to influence the economy.

When inflation rises, the Fed may raise interest rates to:

Reduce borrowing and spending. Slow down economic growth. Mitigate inflationary pressures.

Fiscal Policy (Congress and President):

Fiscal policy involves government spending and taxation. Here’s how it can combat inflation:

Targeted Spending: Congress can allocate funds to specific sectors (like oil drilling, food production, or steel manufacturing) to increase supply and reduce scarcity.

Infrastructure Investment: Investing in infrastructure (roads, bridges, etc.) can boost productivity and reduce bottlenecks.

Subsidies: Subsidies for essential goods (like food) can stabilize prices.

Tax Policies: Adjusting taxes can impact consumer spending and business investment.

Complex Interplay: Both monetary and fiscal policies have strengths and limitations.

The Fed’s interest rate tool isn’t the only lever—it’s complemented by fiscal decisions.

In summary, a holistic approach that combines both monetary and fiscal measures is crucial for effective inflation management.

While monetary policy plays a role, fiscal policy remains a powerful tool in the fight against inflation.

Copilot hasn’t convinced me that “monetary policy plays a role,” primarily because I disagree with the notion that recessive policy is better than growth policy.

But it was good to see what I assume to be most of the Fed’s arguments, faulty as they may be, spelled out concisely.

In the previous post, “Truly pitiful: Federal false helplessness in the face of inflation,” we discussed Federal Reserve Chairman Jerome Powell’s strange attempt to fight inflation by, of all things, raising prices!

Yes, that is precisely what he does when he raises interest rates, his sole inflation-fighting tool. Those higher interest rates increase the prices of virtually every product and service.

When businesses borrow, which most companies do, the higher interest increases their costs, which they must recoup by raising prices.

When farmers borrow, which most farmers do to pay for planting, they include interest costs in their selling prices when they harvest.

When you rent an apartment or house, the owner’s higher mortgage interest cost is reflected in your rental payment.

You may wonder, as I do, how the Fed (and many economists) concluded that raising interest rates reduced the prices of goods and services.

I suspect it comes from the belief that inflation comes from too much buying (Powell’s “overheated” economy). No one knows what an “overheated” economy is, but the phrase makes it sound like Powell knows what he’s talking about.

Since raising interest rates discourages people from borrowing, that seemingly would fight inflation. Of course, inflation itself discourages people from buying, so Powell intentionally causes inflation to cure inflation.

And if that weren’t nonsensical enough, discouraging people from buying is, by definition, causing a recession.

In short, Powell wants to cure inflation by causing it; to do so, he tries to cause a recession without actually causing one. If you understand it, please let me know.

Powell wants us to believe he is a baton-wielding maestro, using interest rates to masterfully conduct our economy as if it were a symphony orchestra, and he expertly navigates between inflation and recession.

In reality, he’s more like a carpenter with onlyone tool, a hammer, using it to remove scratches from furniture.

Here is an article that attempts to describe what I believe is the primary confusion he and his fellow economists suffer.

Inflation occurs when the prices of goods and services increase over a long period of time, causing your purchasing power to decrease.

High inflation can occur as the result of a variety of factors. However, economists often divide the root causes into two categories: demand-pull inflation and cost-push inflation.

And there it is. The common, perhaps universal, belief is that inflation either is demand-pull or cost-push.

I guess you’ve heard those terms. Most economics texts contain them. But what exactly do they mean? A few paragraphs later, the article will explain. But first, a bit of misinformation:

Soaring prices are not caused by “excessive” federal spending or by low interest rates. So, inflation cannot be cured by reduced federal spending or by raising interest rates.

Inflation is a normal part of the world’s economic cycles.

The concept that inflation is “normal” and is part of the world’s “economic cycles” is designed to make you believe it’s inevitable. It isn’t.

Inflation is not “normal.” It’s abnormal. Nothing is “normal” about inflations, hyperinflations, stagflations, recessions, or depressions. To call them “normal” is to call smallpox and broken legs, “normal.”

And it’s not part of any economic “cycle.” The definition of “cycle” is: “A round of years or a recurring period, especially when certain events or phenomena repeat themselves in the same order and at the same intervals.

To call inflations regular “cycles” is to say, “It’s no one’s fault. They just happen and are to be expected.” Inflations don’t just happen. They are caused by mismanagement and/or extraordinary events and certainly do not repeat at the same intervals.

Inflation occurs when the prices of goods and services increase over a long period of time, causing your purchasing power, or the amount of goods and services you can buy with a single unit of currency, to decrease.

In short, inflation means that your money may not be able to buy as much today as it could in the past.

That sounds exactly like what Powell’s raising interest rates does.

But why does inflation happen in the first place?

It often comes down to an imbalance between two different economic forces: supply and demand. Supply describes how much of a good or service is made and sold, and is driven by the businesses that are selling the good or service.

Demand, on the other hand, refers to how much of a good or service is purchased at a specific price, and is driven by consumers. If demand outpaces supply, inflation tends to follow.

Economists often divide the root causes into two categories: demand-pull inflation and cost-push inflation.

Demand-pull inflation is driven by an increase in total consumer demand. If consumers suddenly start spending more money than usual, businesses may find themselves selling more goods and services than they anticipated.

If these businesses are unable to keep up with the increased consumer demand, their remaining stock becomes more valuable, and prices may rise.

This kind of inflation tends to happen during periods of high consumer confidence, such as when unemployment rates are low and wages are high.

Cost-push inflation occurs when production costs rise. Unrelated to consumer demand, these increased production costs may lead to a decrease in total supply and a subsequent increase in prices to compensate.

These definitions exhibit some of the usual confusion about inflation. Inflation occurs when production costs rise (as was caused by Powell’s interest rate increases — to fight inflation).

Scarcity causes prices to rise. To cure inflation, the federal government should fund increased production of scarce goods.

However, increased production costs don’t lead to a decrease in total supply. It’s the reverse. A shortageof raw materials, parts, and labor leads to increased production costs.

This kind of inflation is commonly observed when the price of oil increases, making manufacturing operations more expensive. For example, the 1970s energy crisis was largely responsible for the cost-push inflation that occurred during that time period.

The energy crisis of the 1970s was very simply an oil shortage causing prices to increase—period. In fact, all inflations in history have been caused by shortages, most recently shortages of oil and/or food.

The still-current inflation was caused by COVID-19, which led to shortages of oil, food, lumber, steel, paper, computer chips, labor, and almost any other product or service.

It was not “cost-push.” It was not “demand-pull.” COVID-19 kept people home. We had a shortage of labor, which led to other shortages.

There is no “demand-pull inflation.” Consumers did not “suddenly start spending more money than usual.” They never do.

Consumers might suddenly start buying Furby dolls, Taylor Swift albums, or Ozempic® for weight loss, but consumers never suddenly start spending more money.

As for “cost-push” inflation, this is akin to saying, “The cause of inflation is inflation.” Cost-push is a meaningless definition.

Every inflation in world history has been caused by a shortage of critical goods and services, notably oil and/or food, which then causes other products and services to suffer shortages.

It’s also possible for inflation to result from factors unrelated to the economy. Natural disasters or major world events can disrupt supply chains and reduce theamount of goods available, driving up prices on the stock that remains.It’s also possible for a combination of these factors to occur simultaneously or for one to occur as the result of another.

In other words, all inflations are caused by shortages and not by excessive government spending, as so many economists claim.

How does inflation affect interest rates? Inflation is a complex issue, but one way to control it is through federal monetary policy.

When the Federal Reserve — America’s central banking system, also known as the Fed — detects rising inflation rates, it responds by raising the federal funds rate. This is a special interest rate related to lending between commercial banks.

An increase in the federal funds rate causes a corresponding rise in interest rates on auto loans, mortgages and other types of credit, making it more expensive to borrow money.

Increases in the cost of borrowing money can help to slow down consumer and business spending, allowing supply chains to catch up to the production of goods and services, which can in turn lead to a drop in prices.

Jerome Powell seems to say: “I cure inflation by raising the prices of everything you buy. If I were a doctor, I would cure anemia by applying leeches. Do you understand?”

Said simply, “The increased cost of borrowing increases the cost of goods and services, aka ‘inflation.’ The Fed fights inflation by causing more inflation.”

Ideally, this curbs inflation and stabilizes supply and demand without longer-term consequences such as a recession. When inflation is low once again, the Fed may decide to decrease interest rates, making it easier to borrow money and encouraging spending.

Wait! If high interest rates cure inflation, one should expect low rates to cause inflation.

But that hasn’t happened. For much of a decade, interest rates approached zero, and inflation was low. Only when the COVID-caused shortages hit did we have inflation.

The cause of inflation is scarcities of critical goods and services, mostly oil and food; how should we cure inflation? Cure the scarcity of oil and food.

Although Congress assigned the cure-inflation assignment to the Fed, Congress and the President have the tools to cure inflation, while the Fed does not.

The federal government has the infinite power to create stimulus dollars that would help the producers of scarce products to produce more.

Are we short of oil, food, computer chips, lumber, steel, paper, and shipping? Then, the federal government should give money and tax breaks to domestic producers and importers to alleviate the shortages.

Don’t try to cut federal spending, as many economists advise. Contrary to popular wisdom, federal spending has never caused inflation. If directed appropriately, it can cure inflation.

Those vivid photos of people pushing wheelbarrows full of currency are misleading. Printing higher currency paper didn’t cause hyperinflation; it was a harmful response to existing shortages.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.