Imagine you were in charge of the advanced mathematics department at a university. You would be expected at least to understand arithmetic.

Similarly, if you were the Secretary of the U.S. Treasury, Chair of the Federal Reserve, or President of the United States, you should understand what former Chairs seem to know, i.e., the difference between a Monetarily Sovereign entity and a monetarily non-sovereign one.

It’s that basic.

Alan Greenspan:“A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke:“The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Alas, we are not so fortunate with our leadership’s knowledge:

In 2016, (former President) Trumpsaid he could pay down the national debt, then about $19 trillion, “over a period of eight years” by renegotiating trade deals and spurring economic growth.

In 2018, he said, “We have $21 trillion in debt. When this [the 2017 tax cut] really kicks in, we’ll start paying off that debt like it’s water.

I’ve decided that what we successfully have done for the past 84 years, to build the world’s greatest economy, is unsustainable.

“Because of Tariffs we will be able to start paying down large amounts of the $21 trillion in debt that has been accumulated, much by the Obama Administration.”

He urged policymakers to prioritize fiscal sustainability, warning that running large deficits during good economic times cannot continue indefinitely.“

In the longer run, we’ll have to do something sooner or later, and sooner will be better than later,” he added.

Notice that Powell uses the favorite word of debt fear-mongers: “Unsustainable.” (See here and in many other posts on this blog). Despite false claims since 1940 that the debt and deficits are “unsustainable,” we have sustained it.

The debt fear-mongers never learn from experience.

In 2022, President Biden said, “My Treasury Department is planning to pay down the national debt this quarter, which never happened under my predecessor.”

Every U.S. depression has come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Treasury Secretary Janet Yellen agrees that the federal debt is too high, but when a simple, non-recession solution was presented to her, she preferred austerity, i.e., the mathematical certainty of a recession or depression.

The solution demonstrated the federal government’s total sovereignty over the U.S. dollar:

Legislation enacted in 2001 allows the treasury to mint platinum coins of any value without congressional approval.Under that law, the coin’s value could be anything, but it would have to be platinum, not gold or silver, nickel, bronze or copper, which are under Congress’ control.

President Joe Biden could order Treasury Secretary Janet Yellen to have a coin with the value of $1 trillion be minted and deposited into the Treasury, giving the government an extra trillion dollars to cover debts and prevent default.

The idea was floated before in 2011 when the government faced another debt ceiling crisis. Former President Barack Obama said in 2017, on the podcast “Pod Save America,” that he and his advisers discussed use of a trillion dollar coin as a safety valve.

“There were all kind of wacky ideas about how potentially you could …. have this massive coin.” Obama said in the 2017 interview. “I mean … it was some primitive — it was like out of the Stone Age or something and I pictured rolling in some coin.”

Thus, as usual, President Obama demonstrated his abject ignorance about federal finance. Remember, he was the one who created the Simpson/Bowles Commission that labored to create these recommendations:

Reduce the deficit by $4 trillion over ten years

Cap government spending at 21% of GDP

Reduce discretionary spending to 2008 levels, adjusted for inflation

Raise the retirement age and reduce Social Security benefits

Reduce Medicare benefits.

Fortunately, none of this was done; otherwise, we would have had the worst depression since the Great Depression. However, it reflects Obama’s economic ignorance (or intent?).

Getting back to the platinum coin solution to the debt ceiling idiocy:

Treasury Secretary Janet Yellen said Tuesday in an interview with CNBC that she is “opposed” to the idea, and doesn’t believe it should be considered seriously.

“It’s really a gimmick and what’s necessary is for Congress to show that the world can count on America paying its debts,” Yellen said Tuesday on CNBC’s “Squawk Box”.

And there you have it. Janet Yellen, Secretary of the U.S. Treasury, thinks there is a danger the Monetarily Sovereign U.S. government might not be able to “pay its debts” unless something is done about the federal debt (which isn’t federal and isn’t debt.

Yellen also raised concerns about how using a trillion dollar coin would affect trust in and independence of the Federal Reserve and treasury.

“The platinum coin is equivalent to asking the Federal Reserve to print money to cover deficits that Congress is unwilling to cover by issuing debt, it compromises the independence of the Fed conflating monetary and fiscal policy, and instead of showing that Congress and the administration can be trusted to pay, to pay the country’s bills, it really does the opposite,” Yellen said.

OMG, Secretary of the Treasury Yellen just gets worse and worse. She doesn’t seem to realize that U.S. dollars are debt, and every debt requires collateral.

The collateral for U.S. dollars is the full faith and credit of the United States government. This may sound nebulous to some, but it actually involves certain, specific, and valuable guarantees, among which are:

The government will accept only U.S. currency in payment of debts to the government

It unfailingly will pay all its dollar debts with U.S. dollars and will not default

It will force all your domestic creditors to accept U.S. dollars if you offer them to satisfy your debt.

It will not require domestic creditors to accept any other money

It will take action to protect the value of the dollar.

It will maintain a market for U.S. currency

It will continue to use U.S. currency and will not change to another currency.

All forms of U.S. currency will be reciprocal, that is five $1 bills always will equal one $5 bill and vice versa.

Yellen doesn’t want the Fed to print money. Yet, her signature is on Federal Reserve Notes!~

As economist Hyman Minsky said, “A government that can issue Treasury bills can issue dollar bills.”

Look at the dollar bill in your wallet. At the top, it says, “Federal Reserve Note“, and it is signed by — that’s right — the Secretary of the Treasury and the Treasurer.

Janet Yellen complains that “the platinum coin is equivalent to asking the Federal Reserve to print money,” while she has her signature on dollar bills, which are Federal Reserve Notes!

Many experts are unsure about what the economic effects of the move would be given that it is unprecedented.

But experts cite concerns about inflation, saying that creating more money would weaken the value of existing money circulating in the economy.

We have been “creating more money” for 84 years. In some years, inflation was above the Fed’s target. In other years, it was below. Just before COVID, inflation was quite low. Then COVID created shortages and, thus, inflation.

A “gimmick” too simple for our leaders. They prefer the insanity of the debt ceiling.

The platinum coin’s economic effects would relieve uncertainty about the extraordinarily ignorant Debt Limit. Economies don’t like uncertainty because it hinders investment in the future.

That would mean that existing dollars would have less buying power, which could affect American consumers.

I wonder why America hasn’t suffered that fate so far. Perhaps because it isn’t real??

Still, some Democratic lawmakers backed the idea. House Speaker Nancy Pelosi said that Rep. Jerod Nadler, D-N.Y., brought up the coin during a closed policy meeting last week as one of other “options” to prevent government default without congressional action.

And in case you miss your daily dose of debt fear-mongering about something that never happens, here’s a bit more.

US National Debt Hits $35 Trillion Milestone

In a historic fiscal milestone for the federal government, the national debt rose to $35 trillion for the first time, according to the latest Treasury Department data. Current debt levels are equal to $105,000 per person and $266,000 per U.S. household.

Washington accumulated $1 trillion in debt in less than seven months. Over the past year, the national debt has spiked by nearly $2.35 trillion, an average of about $6.4 billion per day.

The immense growth of red ink flooding the nation’s capital has captured the attention of public policymakers. Federal Reserve Chair Jerome Powell in February conceded that the federal government is “on an unsustainable fiscal path.”

Two of the big three credit agencies downgraded their outlook on the U.S. debt, citing fiscal deterioration, persistent debt ceiling negotiations, and ballooning interest payments. When these updates were released last year, the White House disagreed with the firms’ outlooks.

The two credit agencies referred to are likely Fitch Ratings and Moody’s. Fitch recently downgraded the U.S. government’s credit rating from AAA to AA+ while Moody’s has changed its outlook on U.S. debt to negative.

It’s ironic that two companies should downgrade the U.S. dollar. If the U.S. fails to pay it’s bills, not only will the dollar be worthless, but so will every business on earth, including Fitch and Moody’s.

But Yellen doesn’t want a simple solution to the crazy Debt limit, because “it’s a gimmick” that might (but almost sure will not) cause some inflation.

Economists told the Daily Caller News Foundation that persistent government spending under the Biden administration propped up U.S. economic growth in the second quarter of 2023.

Real gross domestic product (GDP) grew 2.8% in the second quarter of 2024, far higher than economists’ expectations of 2.1%,

However, a significant portion of the recorded growth in the quarter was driven by government spending, both directly through a rise in government expenditures and indirectly through growth in sectors that benefit heavily from taxpayer dollars.

Apparently, some economists believe that when the government spends, it is not true economic growth, but when the private sector spends, that is true growth.

However, exactly the opposite is true. When the government spends, new stimulus growth dollars are created and added to the economy. By contrast, when the private sector spends, dollars are just moved from one hand to another.

Private sector spending that is not financed by borrowing creates no money.

“Government spending has played a large role in much of the economic growth seen over the past few years,” Peter Earle, a senior economist at the American Institute for Economic Research, told the DCNF.

Government spending supposedly is bad because it adds dollars to the economy. It’s also supposedly bad because it just redistributes existing dollars. Huh??

“The problem with that, of course, is that government spending is redistribution: taxing certain citizens or floating more trillions of dollars in debt to send those dollars to other citizens.

It’s not innovative entrepreneurship or other productive commercial undertakings.”

Peter Earle has it exactly backward. Federal spending is done with newly created money, not with tax money.

The crazy part of Earle’s comment is that the debt fear-mongers take both sides of the same issue.

They claim that federal deficit spending adds to the money supply, and so, is inflationary.

Then they claim federal deficit spending is redistribution — i.e., doesn’t add to the money supply.

And they ardently believe both opposing statements.

E.J. Antoni, a research fellow at the Heritage Foundation’s Grover M. Hermann Center for the Federal Budget, told the DCNF that even the increase in consumer spending, which totaled 2.3% in the second quarter — up from 1.5% in the previous quarter — was also partially driven by government expenditures.

That is exactly what federal spending is supposed to do. It puts spending money into consumers’ pockets. Why that is a bad thing is beyond all comprehension.

“Government purchases do not include all of government spending. When the government takes money from one person and gives it to another in the form of welfare, for example, it gets counted as consumer spending,” Antoni told the DCNF.

Trust the extreme right wing to come up with nonsense opposing welfare. No comments opposing the tax breaks given to the wealthy, however.

In any event, the federal government doesn’t give tax money to anyone. It destroys all the tax dollars it receives and creates new dollars to pay its bills.

“Currently, about $4.2 trillion of annual consumer spending is government transfers, illustrating how total government spending is much larger than the GDP report indicates.”

No federal spending is “transfers;” all state/local government spending is “transfers.”

That’s the difference between Monetary Sovereignty and monetary non-sovereignty. The former creates new dollars to pay its bills, while the latter uses borrowed money and taxes.

“What were the big things that contributed to the GDP number? You have a big increase in health care spending, which is consistent with all the jobs we’ve seen in health care, and a lot of that is paid for by government,” Faulkender told the DCNF.

“You have money going into transportation investment, which is deficit-funded [Inflation Reduction Act] money [and] you had the increase in government spending.”

Healthcare spending was responsible for approximately 16% of GDP growth in the second quarter, according to the BEA. In 2022, government sources accounted for just over 45% of healthcare spending, according to the Congressional Research Service.

The healthcare industry has also underpinned recent U.S. job gains, accounting for 49,000 of the 206,000 nonfarm payroll jobs added in June, and approximately 29% of all jobs added in the last twelve months, according to the Federal Reserve Bank of St. Louis (FRED).

In short, the government is spending heavily on transportation and healthcare, which in addition to helping people be healthy and get around, is creating jobs in these fields.

Is that supposed to be a problem?

“All — or nearly all — the apparent growth in the economy has really just been pulling future growth forward to today, at the expense of future growth,” Antoni told the DCNF. “It’s like when a consumer goes deeply into credit card debt to get a higher standard of living today, only to be drowning in debt payments tomorrow.”

No, Mr. Antoni, federal finances are not like personal finances. Not one word of the above paragraph is true. And really, how does today’s growth pull growth from tomorrow? It is nonsensical.

The federal government has been “drowning” in so-called “debt” since 1940, and here has been the result of all that deficit spending:

Real (inflation adjusted) GDP per person has moved up, up, up.

Americans as a group, are wealthier in real terms than ever. If this is what our government “drowning in debt” produces, please toss me in the pool.

The trick is to narrow the Gap between the rich and the rest, which the debt worriers seem to forget when they talk about cutting benefits and increasing taxes.

SUMMARY

Everything in economics eventually devolves to understanding Monetary Sovereignty. Our leaders either don’t understand the difference between Monetary Sovereignty and monetary non-sovereignty, or they don’t want you to understand.

In the latter category are those who want to widen the income/wealth/power Gap between the rich and you.

Both begin with the tacit (or not-so-tacit) assumption that government is harmful, and that people should be allowed to do what they darn well please.

The only significant difference between Libertarians and Republicans is the latter’s belief that only the rich should be allowed to do what they please, the rest of us being too lazy and too ignorant to know what is best.

Well, on reconsideration, that’s what they both believe, so perhaps there’s no difference at all.

Let us explore what the omniscient and omnipotent rich believe:

Moody’s calculates that interest payments on the national debt will consume over a quarter of federal tax revenue by 2033, up from just 9 percent last year. ERIC BOEHM | 11.14.2023 4:15 PM

The “national debt” doesn’t “consume”anything. The so-called “debt” is two things, related by law and size, but not by function, neither of which is debt. The national debt is the:

Total of federal deficits — the difference between federal tax collections and federal spending, which by law equal the:

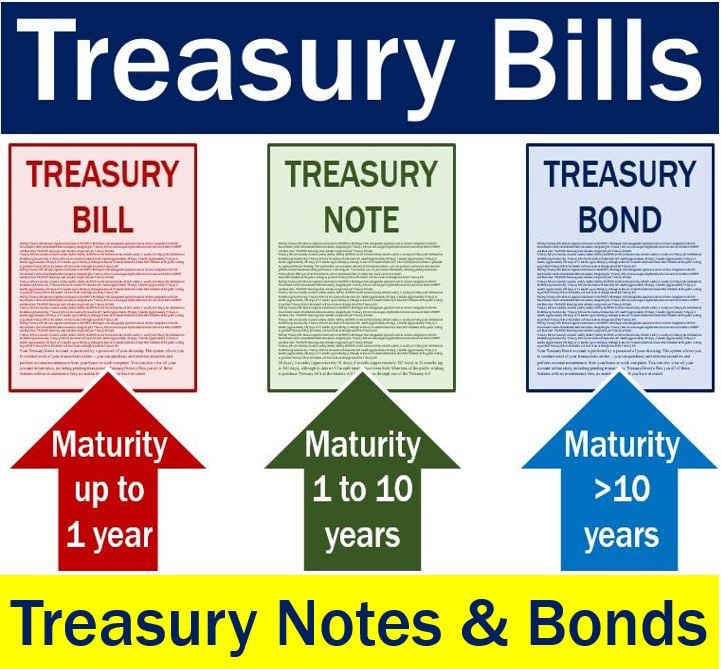

Net total of deposits into Treasury Security (T-bill, T-note. T-bond) accounts.

The government never touches the dollars in T-security accounts. Those dollars belong to the depositors.

Two weeks ago, Treasury Secretary Janet Yellen caused some eyebrows to tilt when she told reporters that rising bond yields were “an important reflection of the stronger economy.”

That’s contrary to the, let’s say, traditional view of how government-issued bonds work.

A bond’s yield—that is, the return an investor expects to be paid at the end of the bond’s term—is the result of buyers pricing their risk into the purchase.

That is true of privately issued bonds, but far less so of federal bonds, which are risk-free (or close to it, depending on what Congress does regarding the useless and infantile “debt ceiling.”)

Interest rates on federal bonds evolve from the basic T-bill interest rate the Federal Reserve creates by fiat in its attempts to fight inflation.

The Fed has no need to make rates attractive because it has no financial need to accept deposits in T-security accounts. The accounts resemble bank safe deposit boxes. The government holds and protects the contents but doesn’t take ownership of them.

Being Monetarily Sovereign, the federal government can create all the dollars it wants simply by stroking computer keys.

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Contrary to popular wisdom, the federal government does not borrow its own sovereign currency. That confuses people who should (and probably do) know better.

To “pay off” these bills, notes, and bonds, the federal government merely returns the dollars from accounts that are wholly owned by depositors. The government never uses those dollars; it merely stores them, meaning it did not borrow the money.

Treasury bonds have historically been some of the most reliable investments out there and, as a result, have typically carried low yields.

In other words: Because you can be very confident that the U.S. government will pay you back at the end of the term, you know that your investment is safe, but you also don’t stand to make much on the risk.

And while U.S. Treasury bonds remain very safe investments, the traditional view would say that the recent uptick in yields means investors are pricing just a bit more risk into those purchases.

It really means:

The Fed arbitrarily has raised the prime interest rate and/or

Other investments carry low enough risk and/or are profitable enough to warrant switching over and/or

A potential investor wishes to make a sale and retrieve so many dollars the private markets couldn’t handle without causing significant price movement (This can be true of government purchases).

Or, a significant depositor (like China et al.) has decided to switch investments.

For example, the yield on 10-year Treasury bonds—a key benchmark that helps determine the rates of mortgages, student loans, and more—hit a 16-year-high of 5 percent late in October, though it has fallen a bit since then.

By no coincidence, the prime rate was last reconsidered on November 1, 2023. The Federal Open Market Committee voted to keep the target range for the fed funds rate at 5.25% – 5.50%. Therefore, the United States Prime Rate remains at 8.50%.

In short: Buyers will demand higher yields to make riskier investments.

That’s why the 10-year U.S. Treasury bond yield peaked at 5 percent, while a 10-year Russian bond comes with a yield north of 12 percent. (As an aside, there’s something cool and quite libertarian about all this: Governments must answer to the market.

It costs the Russian government more to borrow funds simply because investors are less confident that Russia won’t stiff them a decade from now.)

The U.S. government does not “answer to the market” the way a private bond issuer must.

The government arbitrarily sets the prime rate at any place it pleases, usually with an eye toward inflation.

Because the federal government is Monetarily Sovereign, it doesn’t need to set interest rates for its own financial reasons. It can pay any interest rate with equal ease.

Eric Boehm, the author of the article, seems ignorant of a Monetarily Sovereign government’s bonds from a private sector bond issuer.

Sadly, you can go on government websites that will tell you the government borrows and taxes to fund spending. This is wrong and results from ignorance and/or intent to deceive. Unlike you and me, the federal government has no need for any sort of income.

Why would a government, that has the infinite ability to create dollars, borrow dollars? It wouldn’t. As for taxes, the federal purpose is not to acquire spending funds but to:

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to whom the government wishes to reward

Create assured demand by requiring taxes to be paid in dollars.

At the direction of the rich, to fool the populace into accepting cuts to benefits and tax increases. both of which widen the income/wealth/power Gap between the rich and the rest. This is one way the rich become richer.

Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes: Scott Pelley: Is that tax money that the Fed is spending? Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

So, what could be causing investors to price higher risk into U.S. Treasury bonds right now? Yellen says it results from a strong economy and the sense that interest rates will remain higher for a longer-than-expected period.

But that seems to ignore the 300-pound gorilla in the room—or, rather, the $33 trillion mountain of IOUs threatening to bury the Treasury building and the U.S. economy.

Nonsense. That $33 Trillion is the most recent culmination of 84 years’ worth of deficits, beginning with a federal “debt” of $40 Billion in 1939.

Not once, in all those 84 years, has the misnamed “debt” buried the Treasury building or the U.S. economy.

On the contrary, deficits add growth dollars to the economy while the lack of deficits leads to recessions.

Declining deficits lead to recessions (vertical gray bars), which are cured by increasing deficits.

It seems more likely that investors are looking at the trajectory of federal budget deficits and the national debt and are now hedging their bets ever so slightly to account for the possibility of a first-ever federal default.

If there ever is a default, it will not be because the infinitely survivable federal “debt” is so large, but rather because an infinitely ignorant Congress arbitrarily has decided to enforce the infinitely stupid debt ceiling.

Moody’s, one of the world’s “big three” credit rating services, added a significant data point in favor of that conclusion on Friday when it lowered the federal government’s credit outlook from “stable” to “negative.”

As long as boobs like Marjorie Taylor Greene and Mike Johnson run the House of Representatives, I would put the risk of something stupid at nearly 100%

The change reflects Moody’s belief that “downside risks to the nation’s fiscal strength have increased ‘and may no longer be fully offset by the sovereign’s unique credit strengths,'” The Wall Street Journal reported.

Moody’s calculates that interest payments on the national debt will consume over a quarter of federal tax revenue by 2033, up from just 9 percent last year.

The “national debt” consumes nothing.

Unlike private sector (including state/local government) interest payments, federal interest payments do not burden our Monetarily Sovereign government. It could pay any amount of interest simply by tapping computer keys.

Need to make a $1 Billion interest payment? No problem for the federal government. What about a $100 Trillion payment? Still no problem.

The only thing that exceeds the government’s infinite ability to pay any financial obligation is the infinite ignorance of those who don’t understand Monetary Sovereignty.

The announcement from Moody’s comes just three months after another of the primary credit rating services downgraded the federal government’s rating from “AAA” to “AA+” in August.

The change made Friday by Moody’s is not a rating downgrade but signals that one could be coming soon.

Rating downgrades never came during significant deficit growth but only when Congress politically debated whether it wished to pay its bills.

The political party that doesn’t hold the Presidency always tries to prevent economic growth by cutting the federal spending that grows the economy, all in the name of “fiscal prudence.”

That way, they can criticize the President for lack of economic growth and hope to fool a naive voting public.

Forget the “unwieldy pile of debt. The downgrade is 100% based on the debt ceiling and Congress’s willingness (not ability) to pay.

“Without effective fiscal policy measures to reduce government spending or increase revenues, Moody’s expects that the US’s fiscal deficits will remain very large, significantly weakening debt affordability,” Moody’s said in Friday’s announcement.

The above sentence is wrong. The so-called “debt” (that is not a debt of the U.S. government) is infinitely affordable.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

“Continued political polarization within U.S. Congress raises the risk that successive governments will not be able to reach consensus on a fiscal plan to slow the decline in debt affordability.”

The polarization is entirely political. It has nothing to do with “debt affordability.” I suspect Eric Boehm knows this and simply is being paid to spread the bullsh*t.

Yet, in Washington, that announcement was greeted by a chorus of federal officials (and their mouthpieces) denying reality yet again.

White House Press Secretary Karine Jean-Pierre said in a statement that the outlook change from Moody’s was “yet another consequence of congressional Republican extremism and dysfunction.”

True.

Yellen, on Monday, said she “disagrees” with Moody’s decision and claimed the Biden administration is “completely committed to a credible and sustainable fiscal path.”

I don’t know what “credible” means in this context, but the fiscal path is infinitely sustainable.

There it is, where the Libertarians and the Republicans agree: Cut benefits to those who are not rich.

Both parties have sold their souls to the rich. You’ll notice no mention of raising taxes on the rich and no mention of eliminating the tax loopholes that allow billionaires like Donald Trump to pay less in taxes than you do.

No, the Libertarians and the Republicans want the money to come from the elderly on Social Security and from the sick on Medicare and Medicaid.

They claim it’s those poor lazy freeloaders who are taking all the money.

In Yellen’s view, then, increased bond yields do not reflect increasing concern from investors about the fiscal state of the federal government, and growing federal budget deficits are a “sustainable fiscal path.”

Neither claim makes much sense.

Boehm says Janet Yellen “may turn out to be right” about a statement that “makes no sense.”

Wrong, Eric. Both claims are correct.

She may turn out to be right, but this comes off as a lot of politically motivated gaslighting.

Huh? “Neither claim makes much sense,” but “She may turn out to be right”?

Poor Eric, he stands firmly with his legs planted on both sides of the fence.

Americans would be wise to keep in mind that the sky is still blue and gravity still pulls you toward the center of the Earth, no matter how many federal officials might claim otherwise.

Americans would be wiser to keep in mind that 84 years of politically motivated bullsh*t warnings about our “unsustainable” federal debt, have proven wrong, wrong, wrong.

Sadly, that has not stopped Boehm et al from taking paychecks to spread it thick and wide.

If you wish to contact Boehm, you can write to his employer at: Reason Foundation, 1630 Connecticut Ave NW, Suite 600, Washington, DC 20009, or call them at (202) 986-0916, or even tweet him at @EricBoehm87.