If you owned a legal, money-printing press, would you borrow money? Think about it.

The U.S. government has the infinite ability to create (aka “print”) U.S. dollars. So why would it ever borrowdollars?

It doesn’t.

The same “bark”?

Despite what “learned” pundits tell you, the U.S. government never, never, ever borrows U.S. dollars.

The government issues U.S. Treasury bonds, which are totally unlike the private sector bonds that corporations issue.

The fact that the same words — “bills,” “notes,” and “bonds” — are used to describe completely different things, has confused people who should know better — politicians, economists, and the media — for decades.

It’s as though a professional botanist told you dogs are like trees because they both have “bark.”

In the same vein, the so-called federal “debt” is not debt. It’s not even federal.

Here are Warren Buffett’s comments. He gets it about 95% right.

The U.S. Treasury is borrowing $3 trillion in three months to pay for the pandemic response, a record sum that dwarfs the $1.8 trillion borrowed in 2009 during the financial crisis.

The debt will be sold in bonds to a variety of foreign and domestic investors.

Sorry, Mr. Wolff-Mann, but because the federal government is Monetarily Sovereign, the U.S. Treasury has the infinite ability to create dollars (at the behest of Congress).

If Congress voted for the Treasury to create $3 trillion, or $300 trillion, or $3,000 trillion, the Treasury could do it at the touch of a computer key.

Clearly, it has no reason to borrow dollars.

So it doesn’t.

The so-called, misnamed “debt” is two separate things that have been merged for obsolete reasons:

1. The “debt” is the net total of all deficitsthrough history. Deficits are the difference between taxes received and financial obligations (aka “bills”) paid.

The government doesn’t owe deficits. They already have been paid for. That is what makes them “deficits.”

2. The “debt” also is the total of deposits into Treasury Security accounts, those T-bills, T-notes, and T-bonds that are nothing whatsoever like private sector bills, notes, and bonds.

The government accepts deposits into Treasury Security accounts to provide a safe storage place for unused dollars. This stabilizes the dollar and is partly responsible for the U.S. dollar being the most popular currency in the world.

Rather than putting unused dollars into risky private bank accounts, foreign governments and private investors prefer the safety of U.S. Treasury accounts.

The accounts resemble safe deposit boxesin that the money in these accounts is wholly owned by the depositors, not by the U.S. government, which never touches those dollars.

To pay off these accounts, the government simply returns the contents of the accounts to the owners, i.e. the depositors.

At the 2020 Berkshire Hathaway Annual Shareholders Meeting on Saturday, billionaire investor Warren Buffett carefully explained in simple terms why the U.S. will never default on its debt.

When a concerned shareholder asked him whether there was a risk, he didn’t prevaricate, but started with a “no.”

“If you print bonds in your own currency, what happens to the currency will be the question,” said Buffett. “But you don’t default. The U.S. has been smart to issue its debt in its own currency.”

A U.S. dollar bill actually is a zero-interest, Treasury bond. It is evidence that the bearer owns a U.S. dollar.

Other countries don’t do this, Buffett pointed out.

“Argentina is now having a problem because the debt isn’t in their own currency, and lots of countries have had that problem,” he said.

“And lots of competent countries will have that problem in the future.”

Similarly, U.S. state and local government and euro nation debt isn’t in their own currency. State and local governments use the dollar. Euro nations use the euro, which is the currency of the European Union (EU).

France, Germany, Italy et al have problems with their debt (which is real debt) because they do not issue the euro. The EU does.

Over the years, many have worried about the growing national debt as tax cuts and spending have created an ever-widening gap between revenue and outflows.

But in his explanation, Buffett highlighted the distinctions that make the U.S. Treasury much different than your personal checkbook.

Mainly, the government owns the printing press to pay the money to the holders of its debt.

Close, but that’s not precisely what happens. The money already exists in the accounts. The depositors put it there.

Paying off the “debt” merely involves returning the depositors’ dollars. The only function of the metaphorical “printing press” is to add interest dollars to the accounts.

“It is very painful to owe money in somebody else’s currency,” said Buffett. “If I could issue a currency Buffett bucks, and I had a printing press and I could borrow money, I would never default.”

If he could print Buffet bucks, that would be widely accepted, he never would borrow money, just as the U.S. federal government never borrows dollars.

This is a common refrain of Modern Monetary Theory as well as longtime Fed Chair Alan Greenspan, who once said something similar: “The United States can pay any debt it has because we can always print money to do that. So there is zero probability of default.”

The chief worry about just printing money to pay obligations is inflation.

That is another widespread, false belief. Creating (aka “printing”) dollars doesn’t cause inflation. Shortages of critical goods and services — mostly oil and food — cause inflation. (See: Inflation: Why the Fed is confused)

“What you end up getting in terms of purchasing power can be in doubt,” Buffett said.

But whether the U.S. can pay the dollars that it owes is not in doubt. The Oracle of Omaha noted back to when Standard & Poor’s downgraded the U.S.’s credit rating in 2011.

The U.S. government does not “owe” any dollars. It already has paid for what it has purchased. That is the “deficit.”

And the dollars in Treasury Security accounts — the T-bills, notes, and bonds — are owned by the depositors. The government doesn’t owe them just as your bank doesn’t owe you the contents of your safe deposit box.

“To me that did not make sense,” he said. “How you can regard any corporation as stronger than a person who can print the money to pay you, I just don’t understand. So don’t worry about the government defaulting.”

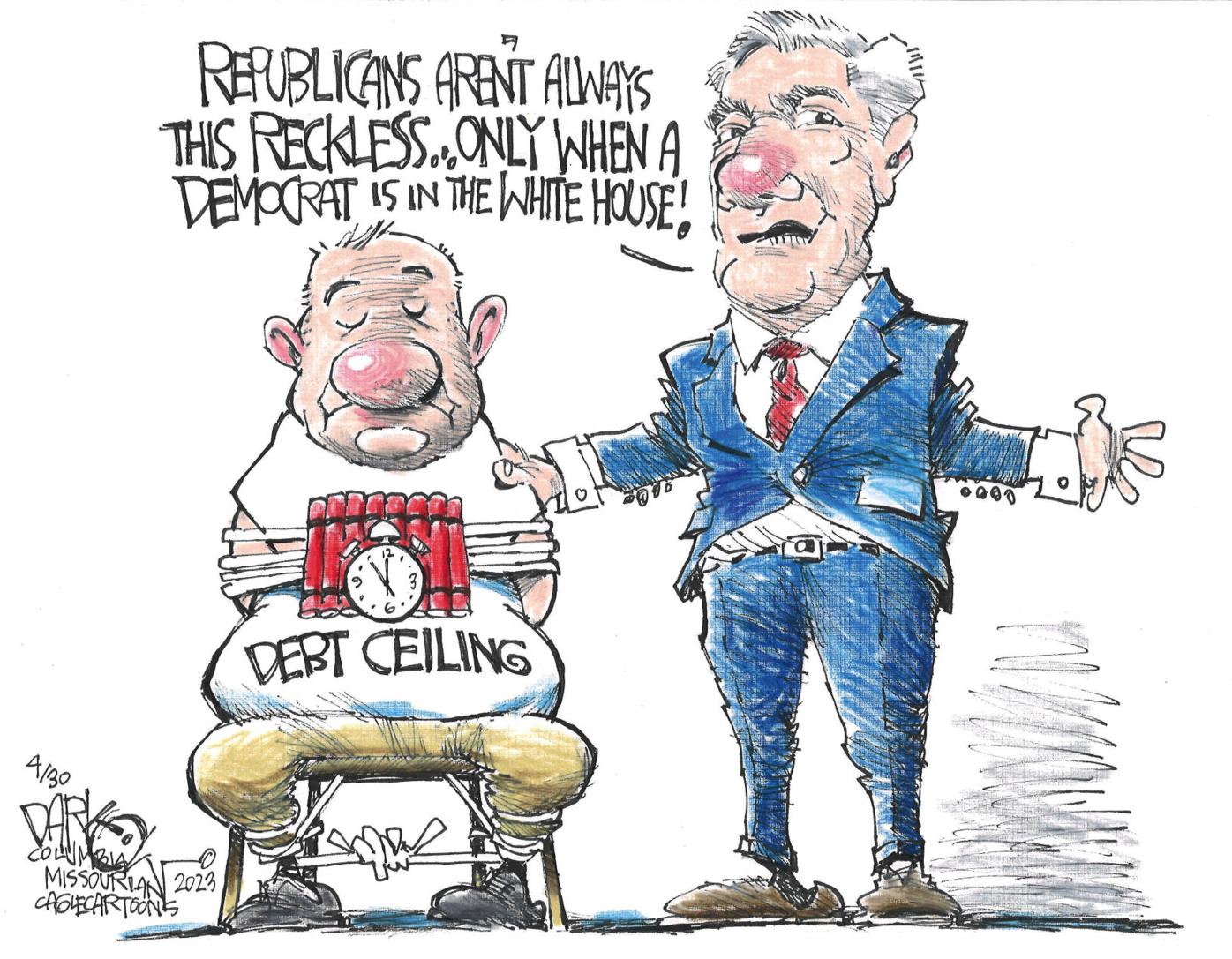

Buffett then addressed the frequent government shut-downs that happen over partisan arguments about raising the debt ceiling.

“I think it’s kind of crazy incidentally…to have these limits on the debt,” he said. “And then [the] stopped government, arguing about whether it’s going to increase the limits. We’re going to increase the limits on the debt.”

Buffett pointed out that the debt “isn’t going to be paid, it’s going to be refunded,” and referenced the period in the 1990s when the debt came down and the country simply created more.

“When the debts come down a little bit, the country’s going to print more debt. The country is going to grow in terms of its debt-paying capacity,” he said. “But the trick is to keep borrowing in your own currency.”

Ethan Wolff-Mann is a writer at Yahoo Finance focusing on consumer issues, personal finance, retail, airlines, and more. Follow him on Twitter @ewolffmann.

Paul Krugman

That was Warren Buffett. Now, here is Paul Krugman, winner of the economics version of the Nobel Prize. He too gets it about 95% right.

The US doesn’t actually have to pay off its $31 trillion mountain of debt, according to top economist Paul Krugman, hitting back at the idea that government finances can be compared to household balance sheets.

Though individual borrowers are expected to pay off debts, the same isn’t true for governments, Krugman argued in a column for the New York Times on Friday.

That’s because unlike people, governments don’t die, and they gain more revenue with each passing generation.

Not quite right. State and local governments are expected to pay off debts. Euro governments are expected to pay off debts.

But the Monetarily Sovereign U.S. federal government always pays what it owes to vendors, on time. It does not accumulate debt.

The reason is notthat “governments don’t die and gain more revenue.” Monetarily nonsovereign governments do borrow and must pay off loans, and may not gain enough revenue to pay off those loans.

Our Monetarily Sovereign government is a different animal, altogether. It does not borrow, it does not have loans to pay off, and its tax revenue does not pay for anything.

Its tax revenue is destroyed upon receipt. (See: “Does the U.S. Treasury Really Destroy Your Tax Dollars?”)

“Governments, then, must service their debts – pay interest and repay principal when bonds come due – but they don’t necessarily have to pay them off; they can issue new bonds to pay principal on old bonds and even borrow to pay interest as long as overall debt doesn’t rise too much faster than revenue,” he added.

Treasury bonds don’t supply the federal government with spending money. The government never touches those dollars. The government doesn’t use bond deposits to pay anything.

Treasury securities provide two main functions:

They help the Federal Reserve control interest rates by providing a “base” rate.

They help stabilize the dollar by providing a safe haven for unused dollars.

They do not help the federal government fund any thing.

The debt-to-GDP ratio is oft-quoted, but completely meaningless. The federal government can pay all its financial obligations whether the ratio was 10%, 100%, or 1,000%. (See: Enough Already, With The Debt/GDP ratio)

Federal purchases are part of GDP, but are not paid for with GDP. All federal financial obligations are funded by newly created ad hoc dollars.

Historically, it’s also unusual for governments to pay off large debts, Krugman said. Such was the case for Great Britain, which has largely held onto the debt it incurred as far back as the Napoleonic wars.

It’s more irrelevance from the Nobel winner. Deadbeat governments may not pay creditors, but the Great Britain “debt” is not owed to creditors. It’s an accounting myth for describing the total of deficit spending, which is funded by money creation.

Krugman’s argument comes amid growing contention over the US debt level, with policymakers still sparring over the conditions they want to raise the country’s borrowing limit.

House Speaker Kevin McCarthy has said he would reject a short-term debt ceiling increase unless spending cuts are negotiated, having proposed a bill that would slash around $4.5 trillion on spending.

This is purely a political ploy, having absolutely nothing to do with the realities of federal funding. The formula for GDP is:

GDP = Federal Spending + Nonfederal Spending + Net Exports

Slashing $4.5 trillion for federal spending would, by formula, slash at least $4.5 trillion from GDP (Probably more, because federal spending begets private sector, nonfederal spending.)

In short, Republican McCarthy wanted to trash the economy, because a Democrat was President.

Congress now has less than two weeks to raise the borrowing limit before the government could potentially run out of cash, US Treasury Secretary Janet Yellen warned.

Sadly, Yellen is too cowardly (or ignorant?) to tell the truth. The so-called “borrowing limit” is the ultimate fraud. It’s not a borrowing limit, because the U.S. doesn’t borrow.

It’s a limit on deposits into T-security accounts, which do nothing to change the federal government’s ability to fund its spending.

A default on the country’s obligations could result in catastrophe for financial markets, experts have warned.

Krugman is correct. The debt ceiling is a fraud being committed on naive American voters. It’s a bit of meaningless, though harmful, political chicanery, designed to pretend financial frugality.

All those who think the debt ceiling is a good idea either are liars or ignorant.There is no alternative.

Period.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The purpose of credit ratings is to assess the likelihood that an issuer of a debt document will adhere to the terms of the document.

The U.S. debt documents consist of Treasury bills, bonds, and notes, including the Federal Reserve Notes you carry in your wallet, aka “money.”

The value of U.S. debt/money is determined by the U.S. government’s full faith and credit,which includes:

A. –The government will accept only U.S. currency in payment of debts to the government

B. –It unfailingly will pay all its dollar debts with U.S. dollars and will not default

C. –It will force all your domestic creditors to accept U.S. dollars if you offer them to satisfy your debt.

D. –It will not require domestic creditors to accept any other money

E. –It will take action to protect the value of the dollar.

F. –It will maintain a market for U.S. currency

G. –It will continue to use U.S. currency and will not change to another currency.

H. –All forms of U.S. currency will be reciprocal; that is, five $1 bills always will equal one $5 bill and vice versa.

The key to the downgrade is item “B,” the “not default” claim.

The following article from Investor News attempts to explain why federal Treasuries were downgraded from AAA to AA+.

Credit Rating Alert: Why Did Fitch Downgrade U.S. Debt?Story by Josh Enomoto

Primarily, the negative reassessment focuses on “the expected fiscal deterioration over the next three years,” a matter worsened by increasingly bitter political infighting.

The matter was not “worsened” by political infighting. The matter was entirely political infighting.

As you will see, that was the sole reason for the downgrade.

Per the agency’s official statement, a “steady deterioration” in standards of governance during the past two decades imposes a dark cloud as policymakers struggle to navigate the extraordinarily difficult post-pandemic environment.

Specifically, “[t]he repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management.”

“Standards of governance” is the polite way to say that the GOP has become Trump-nuts, with such stellar brains as Matt Gaetz, Marjorie Taylor Greene, Lauren Boebert, Marsha Blackburn, et al leading the way.

Really, would you lend to those people?

The debt limit is 100% political. It is how the party not holding the Presidency exerts political power over the competing party. It has no other purpose.

As well, the combination of economic shocks and initiatives involving tax cuts and spending programs spiked the overall debt load.

Tax cuts and spending programs are irrelevant to the federal government’s ability to pay all its dollar debts.

Even if the total “debt,” which stands at about $30 trillion, were instead only $1, that would have no effect on the federal government’s ability to pay.

As the creator and issuer of the U.S. dollar (aka Monetarily Sovereign), the government has the infinite ability to create enough dollars to pay all its dollar-denominated debts.

If, for instance, you sent a $50 trillion, or $100 trillion, invoice to the U.S. government today, it could pay that invoice today simply by passing laws and pressing computer keys.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Alan Greenspan: “The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes:Scott Pelley: Is that tax money that the Fed is spending?Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed:“As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

This infinite power is true not only of the U.S. federal government but also other Monetarily Sovereign entities. Consider the European Union, which is monetarily sovereign over the euro:

Question: I am wondering: can the ECB ever run out of money?Mario Draghi: Technically, no. We cannot run out of money.

No Monetarily Sovereign entity can run short of its sovereign currency unless it wishes to.

Some elements of today’s Republican Party would like to see the U.S. economy fail, so they can claim, before elections, that the economic failure is the Democrat’s fault.

In addition, Fitch took into account the Federal Reserve’s efforts in combating historically high inflation into account regarding its latest credit rating decision.

“While headline inflation fell to 3% in June, core PCE inflation, the Fed’s key price index, remained stubbornly high at 4.1% yoy,” wrote the agency. As a result, this framework will likely preclude benchmark interest rate cuts until March of next year.

All inflations are caused by shortages of crucial goods and services, most often oil and food. So-called “core inflation” refers to this:

“Inflation is based on the consumer price index (CPI), covering the inflation of all the goods and services except the volatile food & fuel prices, excise duties, income tax, and other financial investments.

It guides the government in forecasting long-term inflation trends for a country.

Using “core inflation” as a forecasting tool is nonsensical because the primary causes of inflation are those “food & fuel prices, excise duties, income tax, and other financial investments.”

It’s like predicting a baseball team’s wins while omitting runs-scored-and-allowed to get “core victories.”

In a possible reality check, the Fitch downgrade also incorporated recession risks. Based on the aforementioned tighter credit condition and a projected consumer spending slowdown, the U.S. economy may slip into a mild recession in the fourth quarter of 2023 and Q1 of 2024.

The predicted “mild recession and consumer spending slowdown have absolutely nothing to do with the federal government’s ability to service its Treasury paper. Zero.

The only thing that affects debt service is the federal government’s willingness to service its debt.

As The Wall Street Journal pointed out, the Fitch downgrade represents the first by a major credit rating agency in more than a decade. In theory, the unfavorable reassessment clouds the outlook for the global market for Treasurys, which stands at $25 trillion.

Indeed, the WSJ states that “America’s reputation for reliably making good on its IOUs has cast Treasury bonds in an indispensable role in global markets: a safe-haven security offering nearly risk-free returns.”

The U.S. dollar is a safe-haven security only if the government wants it to be a safe-haven security. All those other factors — total debt, spending, inflation, taxes, etc. — are meaningless to that safe haven.

There is but one question: Will the Republican party refuse, for political reasons, en masse, to authorize future payment. Period.

Treasury Secretary Janet Yellen blasted the Fitch downgrade as “arbitrary.” Yellen noted that the agency demonstrated deteriorating U.S. governance since 2018 but didn’t say anything until now. “The American economy is fundamentally strong,” she emphasized.

The downgrade was not arbitrary. The crazies have taken over the GOP, and Fitch merely is allowing for that craziness by, in effect, saying, “You have a political party that cares nothing about America’s credit rating, and instead, will do everything it can to destroy it.

If I were Fitch, I too would have downgraded the U.S. credit rating, not because of any economic problems but solely because of the political situation, notably the craziness of the Trump-led GOP.

The New York Times op-ed writer and Nobel laureate Paul Krugman chimed in, calling the credit rating decision “bizarre.” Also, former Secretary of the Treasury Larry Summers, in an interview with Bloomberg, stated, “I can’t imagine any serious credit analyst is going to give this weight.”

Sorry, guys, it’s not bizarre. It’s legitimate and will continue to be legitimate so long as the Republicans are enslaved to their MAGA wing.

On paper, the credit rating falling appears rather ominous. However, Axios — while not dismissing the relevant concerns leading to the decision — stated that the Fitch downgrade is “largely symbolic.”

It’s symbolic but also a warning. If you invest in a T-bill, T-note, or T-bond, buy U.S. dollars, or sell something to the U.S., and will be paid in dollars — and if the crazies decide not to raise the so-called “debt ceiling” — you will lose money.

Also, it’s important to remember that credit rating agencies don’t always issue accurate prognostications. For instance, in October of last year, Fitch stated that it expected a mild recession to materialize in Q2 2023.

However, CNN recently reported that the economy picked up steam in Q2 “despite punishing rate hikes and still-high inflation.”

The wrong prediction of a mild recession may have been based on “core inflation,” which is irrelevant. If it was based on predicted shortages of oil and food, and those didn’t materialize, Fitch should have stated that.

Bottom line: People are discouraged from buying the obligations of a crazy debtor. Wouldn’t you be?

That unpredictable craziness, and not the size of the so-called “debt,” “core inflation,” or any other factor, are solely responsible for the value loss of the federal government’s full faith and credit.

Eliminate the useless — no, harmful — debt limit, and/or get rid of the crazies, and the U.S. credit rating instantly will be AAA again.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Mitchell’s laws:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes. .

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

•The single most important problem in economics is the Gap between rich and poor.

•Austerity is the government’s method for widening the Gap between rich and poor.

•Until the 99% understand the need for federal deficits, the upper 1% will rule.

•Everything in economics devolves to motive, and the motive is the Gap between the rich and the rest..

You can read that post to see why he had me fooled.

Well Krugman, the winner of, not the Nobel Prize, but rather the “Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel” (commonly known as the “Bank of Sweden Prize”), still is fooling people.

Reader “Zen” commented: It looks like Paul Krugman may just be starting to get the MS/MMT idea. “Debt Is Good”

Unfortunately, Krugman has been “just starting,” and “just starting” and “just starting” for all these years, but like the guy who promises to quit being an alcoholic tomorrow, Krugman never seems to get there.

Here are some excerpts from the article:

Rand Paul decried the irresponsibility of American fiscal policy, declaring, “The last time the United States was debt free was 1835.”

Wags quickly noted that the U.S. economy has, on the whole, done pretty well these past 180 years, suggesting that having the government owe the private sector money might not be all that bad a thing.

Actually, having the federal government pay (not just owe) the private sector is a very good thing. Adding dollars to the private sector stimulates economic growth, which is why every recession is cured by increased federal deficit spending.

Can government debt actually be a good thing?

Many economists argue that the economy needs a sufficient amount of public debt out there to function well. And how much is sufficient? Maybe more than we currently have.

That is, there’s a reasonable argument to be made that part of what ails the world economy right now is that governments aren’t deep enough in debt.

The power of the deficit scolds was always a triumph of ideology over evidence, and a growing number of genuinely serious people — most recently Narayana Kocherlakota, the departing president of the Minneapolis Fed — are making the case that we need more, not less, government debt.

Now at this point, you, like reader Zen, might think, “At long last, this guy is beginning to understand a fundamental point in economics: A growing economy requires a growing supply of money.”

After all, the most common measure of economic growth is Gross Domestic Product (GDP), and the formula for GDP is:

GDP = Federal Spending + Non-federal Spending + Net Exports.

All three — Federal Spending, Non-federal Spending and Net Exports — are money measures. When they increase the money supply increases, and when they decrease, the money supply decreases.

That’s why recessions are cured by increased federal deficit spending.

But just when you think Krugman gets it, he writes:

Issuing debt is a way to pay for useful things, and we should do more of that when the price is right.

The United States suffers from obvious deficiencies in roads, rails, water systems and more; meanwhile, the federal government can borrow at historically low interest rates.

So this is a very good time to be borrowing and investing in the future, and a very bad time for what has actually happened: an unprecedented decline in public construction spending adjusted for population growth and inflation.

As grandma used to say, “Oy vey.” The man simply does not understand the differences between the federal government’s finances and private finances.

First, issuing debt does not pay for anything. The federal government, being Monetarily Sovereign, does not need to borrow its own sovereign currency — the currency it created out of thin air more than 230 year ago, and continues to create out of thin air, today.

The federal government creates dollars, ad hoc, by paying bills. It does not need to borrow the dollars it previously created, from anyone.

Second, the price of debt, (i.e. the interest paid on T-bonds) has absolutely, positively nothing to do with the federal government’s ability to pay for “roads, rails, water systems and more.” Zero. Zilch. Nada.

Even were interest rates to rise from their current near-zero to 20% or more, the federal government could continue spending as always.

Third, when Krugman says, “This is a very good time to be borrowing and investing in the future,” perhaps he is talking about you and me and private industry, but he sure as heck could not be talking about the federal government.

For the federal government, NO time either is a good or bad time to be borrowing, and EVERY time is a good time to invest in the future.

O.K., so Krugman remains clueless about federal financing, but why then does the federal government borrow (by selling T-securities)? Amazingly, Krugman supplies an answer:

According to M.I.T.’s Ricardo Caballero and others, is that the debt of stable, reliable governments provides “safe assets” that help investors manage risks, make transactions easier and avoid a destructive scramble for cash.

In this, Krugman (or more accurately, Ricardo Caballero) is correct.

That is one of the two reasons the government “borrows,” the other being that T-securities help the Fed control interest rates, which is how the Fed controls inflation.

Those are the two reasons. Remember, unlike you and me and your state and city, the federal government does not “borrow” to obtain dollars. The federal government creates dollars at will.

So Krugman was right about one function of T-securities (misnamed “borrowing”), but then he goes on to be completely at sea about the function of interest rates).

When interest rates on government debt are very low even when the economy is strong, there’s not much room to cut them when the economy is weak, making it much harder to fight recessions.

Here, he parrots the widely believed myth about low rates being stimulative and high rates being recessive (which is why the stock market tanks when the Fed says it will raise rates).

And then, after all the misstatements, misunderstandings and misinformation, Krugman finishes with something that actually is true — sort of:

In other words, the great debt panic that warped the U.S. political scene from 2010 to 2012, and still dominates economic discussion in Britain and the eurozone, was even more wrongheaded than those of us in the anti-austerity camp realized.

Not only were governments that listened to the fiscal scolds kicking the economy when it was down, prolonging the slump; not only were they slashing public investment at the very moment bond investors were practically pleading with them to spend more; they may have been setting us up for future crises.

It’s true, but only sort of, because the great debt panic didn’t end in 2012. It continues today, which is why President Obama brags about how he has reduced deficits (i.e. reduced economic growth).

But Krugman is correct about cutting deficits being wrongheaded and setting us up for future crises.

In short, the guy mixes right with wrong, so you can’t tell whether his bread is made with grain or sand.

Every time I’ve hoped he finally knows what he’s talking about, he’s dashed my hopes with large dollops of ignorance.

At long last I’m convinced: I’ve been way, way wrong about Paul Krugman.

So, reader Zen, I’m sorry to tell you. Krugman is hopeless and I’ve lost hope.

=================================================================================== Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

The Ten Steps will add dollars to the economy, stimulate the economy, and narrow the income/wealth/power Gap between the rich and the rest.

——————————————————————————————————————————————

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

No nation can tax itself into prosperity, nor grow without money growth. Monetary Sovereignty: Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

1. A growing economy requires a growing supply of dollars (GDP=Federal Spending + Non-federal Spending + Net Exports)

2. All deficit spending grows the supply of dollars

3. The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

4. The limit to non-federal deficit spending is the ability to borrow.

THE RECESSION CLOCK

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

The debt hawks are to economics as the creationists are to biology. Those, who do not understand monetary sovereignty, do not understand economics. Cutting the federal deficit is the most ignorant and damaging step the federal government could take. It ranks ahead of the Hawley-Smoot Tariff.

==========================================================================================================================================

One problem with the science of economics is: The people who win the awards don’t understand the science. Examples: Paul Krugman and Joseph Stiglitz, who do not know the implications of Monetary Sovereignty. The effect of our most respected (or at least most prominent) economists expounding with false information, is to create a vast blanket of ignorance that has shaded from knowledge, not only our political leaders, but the voters who select them.

For your amusement and/or anger, here is yet another misleading article, this time written by Stephen Gandel, who in it quoted Mr. Stiglitz:

View from Davos: How Bad is a $1.5 Trillion Deficit?

Posted by Stephen Gandel Thursday, January 27, 2011 at 12:38 pm.

The title itself misleads by talking about the deficit being “bad,” when in fact it not only is good, but absolutely necessary. A growing economy requires a growing supply of money, and the misnamed “deficit” is the federal government’s method for supplying the economy with money.

Joseph Stiglitz is one of the many economists talking about debt at Davos. Now that we have the recovery, we will have to pay for it. The question is did we take the appropriate measures or did we overspend.

The notion of having to “pay for” the recovery some time in the future, is nonsensical. The recovery was enabled by yesterday’s federal spending, or perhaps more accurately, yesterday’s money creation.

On Thursday, the CBO estimated that the federal deficit in 2011 will reach nearly $1.5 trillion. That’s up from nearly $1.3 trillion last year. Three years after the financial crisis many had hoped what were supposed to be temporary budget deficits would be shrinking by now.

Shrinking deficits cause recessions and depressions See: Recession cause. The “many” who had “hoped” the deficits would shrink do not understand the realities of economics.

At a dinner of economists on Wednesday night, economist Carmen Reinhart predicted that the US was headed toward a crisis where we would be forced to cut many of our social services. Raghuram Rajan, a former chief economist at the IMF, said that the measures that the UK were making to deal with their deficit right now were a good move. He said we too should deal with our fiscal problems now, rather than putting them off.

Lacking knowledge of Monetary Sovereignty, Messrs. Reinhart and Rajan equate Europe’s monetarily non-sovereign problems with U.S. finances. The U.K, which is Monetarily Sovereign, has begun to punish its children and grandchildren by choking off the nation’s money supply, needlessly.

But not everyone thinks the US debt problem is so dire. While the total deficit is larger this year than last year, it is slightly smaller as a percentage of GDP than last year.

Not only does Mr. Gandel misunderstand Monetary Sovereignty, he doesn’t realize he is making the classic apples/oranges comparison: Debt/GDP. Debt is the total of outstanding T-securities issued since the beginning of our nation. GDP is a one-year measure of production. How an intelligent person can compare a one-year measure with a 200-year measure is beyond me.

What’s more, the US may have more ability to borrow than other countries because of the dominant role of the dollar in the world economy. The fact that our dollars are so widely seen as a safe asset gives America the ability to borrow more than say Greece or Ireland before hitting the breaking point.

It gets worse and worse. A Monetarily Sovereign nation does not need to borrow the currency it previously created and has the unlimited ability to create. There is no “breaking point.” If tomorrow, the U.S. stopped “borrowing” (i.e. creating T-securities from thin air and exchanging them for dollars it previously created from thin air), this would not reduce by even one cent the federal government’s ability to pay its bills. And mentioning monetarily non-sovereign nations (Greece and Ireland) in the same breath as the U.S. displays stunning ignorance of economics.

Nobel prize winning economist Joseph Stiglitz, who is also at Davos, said that while he is worried about some of the US states debt problem, he thinks (federal) debt may not be as bad as some people think. In fact, Stiglitz would even be for increasing our debt even more. As long as it was spent on things like infrastructure and education, which can produce jobs, and boost incomes.

Mr. Stiglitz is correct that the “debt may not be as bad as some people think,” unless one realizes the debt is too small, which is bad. But, Mr. Stigltiz is a victim of “first use syndrome,” wherein he thinks money ceases to exist after its first use. No, Mr. Stigltiz, the first use does not need to be infrastructure and education. It can be virtually anything – aid to the poor, aid to states, army pay or research and development – anything that gets money circulating in the economy.

So there is a debt cliff, but the US may not be there yet.

No, no, no, Mr. Gandel. There is no debt cliff, unless spending too little can be considered a cliff. I urge my readers to contact Mr. Gandel and beg him to familiarize himself with Monetary Sovereignty. If he, Mr. Stiglitz and Mr. Krugman don’t get it, how can the average voter, much less the politicians, understand?