(Bloomberg) — Even before global finance chiefs fly into Washington over the next few days, they’ve been urged in advance by the International Monetary Fund to tighten their belts.

Two weeks ahead of a potentially era-defining US election, and with the world’s recent inflation crisis barely behind it, ministers and central bankers gathering in the nation’s capital face intensifying calls to get their fiscal houses in order while they still can.

The IMF’s Fiscal Monitor on Wednesday will feature a warning that public debt levels are set to reach $100 trillion this year, driven by China and the US.

Managing Director Kristalina Georgieva, in a speech on Thursday, stressed how that mountain of borrowing is weighing on the world.

How to lie with facts. Use meaningless numbers and compare non-comparable things.

Before we continue, let me show you the graphs showing the debt/GDP ratios of several countries. Look at the graphs and tell me what is misleading about them.

The graphs at the right have two main problems:

1. They combine two completely different things: Monetarily Sovereign nations and monetarily non-sovereign nations.

A Monetarily Sovereign nation has the infinite ability to create its own sovereign currency. It never can run short of money to pay its bills.

The U.S. cannot run short of dollars. China cannot run short of yuan. Japan cannot run short of yen, and the UK cannot run short of pounds. These nations are Monetarily Sovereign.

They all can pay any debt denominated in their sovereign currency, merely by tapping a computer key.

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

By contrast, Germany, France, and Italy are monetarily non-sovereign. They all use the euro, and can run short of euros to pay their debts. They must borrow from the European Union (EU) when they run short of euros.

The G-7 graph is a mongrelization of Monetarily Sovereign and monetarily non-sovereign nations (Canada, France, Germany, Italy, Japan, United Kingdom, United States) and thus is useless and misleading.

2. The debt/Gross Domestic Product ratio, which is the subject of the graphs is meaningless, though it often has been used by those who do not understand Monetary Sovereignty.

Here are the ten nations with the supposedly “worst” (highest) ratios:

Debt to GDP Ratio (%); Japan 264%, Venezuela 241%, Sudan 186%, Greece 173%, Singapore 168%, Eritrea 164%, Lebanon 151%, Italy 142%, United States 129%, Cape Verde 127%

Japan and the U.S. are ranked worst, along with Sudan, Greece, Lebanon, and Cape Verde.

Who would you prefer to lend to, Japan or Cape Verde? The United States or Sudan?

Now, here are the ten nations with the “best” (lowest) debt/GDP ratios: Brunei 2.1%, Kuwait 2.9%, Cayman Islands 4.5%. Afghanistan 7.4%. Turkmenistan 8%, Azerbaijan 11.7%, Burundi 14.5%, DR Congo 14.6%, Russia 17.2%, Palestine 18.5%

That’s right. According to the IMF, those are the financially safest places in the world.

The debt/GDP ratio is akin to a butter/butterfly ratio. Completely and utterly useless, yet here is the equally useless IMF shrieking about it.

This is what the IMF says about itself:

The International Monetary Fund (IMF) is an organization that aims to ensure the stability of the international monetary system. Its primary purposes are to:

1. Foster collaboration among countries to achieve global monetary stability.

2. Promoting exchange rate stability

3. Support economic policies that promote growth and reduce poverty.

4, Offer loans and financial aid to member countries facing balance of payments problems or economic crises.

5. Provide economic and financial advice.

It does none of those, except #4, which it uses like a loan shark, extorting unreasonable terms from weak countries. And really, would you take “economic and financial advice” from a group that doesn’t know the difference between Monetary Sovereignty and monetary non-sovereignty.

It is like taking medical advice from a quack doctor who doesn’t know the difference between heartburn and sunburn.

Continuing with the article:

“Our forecasts point to an unforgiving combination of low growth and high debt — a difficult future,” she said. “Governments must work to reduce debt and rebuild buffers for the next shock — which will surely come, and maybe sooner than we expect.”

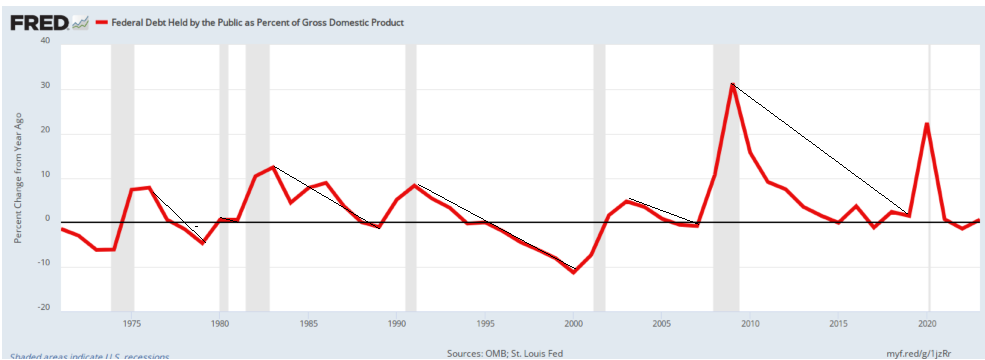

For a Monetarily Sovereign nation “high debt” generally means the government is pumping more growth dollars into the economy. Lack of debt growth leads to recessions:

A decline in debt growth (red line) causes recessions (vertical gray bars) which are cured by an increase in debt growth.

Thus, the IMF’s “cut debt” advice is diametrically wrong, like taking blood from a patient to cure his anemia.

Some finance ministers may get further reminders even before the week is over.

UK Chancellor of the Exchequer Rachel Reeves has already faced an IMF warning of the risk of a market backlash if debt doesn’t stabilize. Tuesday marks the last release of public finance data before her Oct. 30 budget.

The UK tax office is taking a tougher approach to clawing back debts, insolvency specialists say, a bid to squeeze £5 billion ($6.5 billion) in extra revenue.

The above simple proves that many government economists are as financially ignorant as the IMF economists.

We have the same problem in the U.S., with so-called experts claiming our federal debt (which isn’t “federal” and isn’t “debt”) is a “ticking time bomb.” Total bullshit.

What Bloomberg Economics Says: “For all the talk of black holes, the overall effect of Reeves budget will be a policy that’s looser, not tighter, relative to the previous government’s plans.”

As it should be if the UK wants economic growth. If the UK is foolish enough to listen to the IMF and cut debt (which means take dollars out of the economy), it will have a recession.

Meanwhile, Moody’s Ratings has slated Friday for a possible report on France, which faces intense investor scrutiny at present. With its assessment one step higher than major competitors, markets will watch for any cut in the outlook.

France, being monetarily non-sovereign, does risk it’s debt being too high to service. The EU, which is Monetarily Sovereign, could solve France’s financial problems by simply giving them euros. That would cost European taxpayers nothing, and would prevent debt from being an issue.

As for the biggest borrowers of all, the glimpse of the IMF’s report already published contains a grim admonishment: your public finances are everyone’s problem.

True for monetarily non-sovereign nations; not true for Monetarily Sovereign nations.

“Elevated debt levels and uncertainty surrounding fiscal policy in systemically important countries, such as China and the United States, can generate significant spillovers in the form of higher borrowing costs and debt-related risks in other economies,” the fund said.

We’ll end with the final dollop of bullshit from the IMF. China’s and the US’s increase in debt means other nations are being enriched by dollars and yuan. The more these two governments spend on foreign goods and services, the better all the other governments’ finances will be.

As usual, the fools and con men of the IMF offer diametrically the opposite of good advice.

In the previous post (“They feed you garbage to improve your health), we addressed some of the usual false claims about the so-called “federal debt.” We showed why “federal debt”:

Isn’t “federal,” and it isn’t “debt.” (It’s non-federal deposits.)

Doesn’t consider the differences between a Monetarily Sovereign government vs. a monetarily non-sovereign government.

The much-feared Debt/GDP ratio shows a repeated pattern: It declines because debt fear mongers (like J.D. Tuccille) complain about it until it reaches a low point. Then, we have a recession, which is cured by an increase in the ratio, after which the fear-mongers again begin their complaints.

If you are unfamiliar with the above facts, you may wish to read the previous post and rid yourself of the nonsense that J.D. Tuccille spouts in the opening paragraphs of the following article.

J.D. Tuccille

First, his rehash of the old, familiar, wrongheaded, fact-free stuff:

Misery loves company, as they say. But does financial irresponsibility also enjoy spending a little quality time with friends? If so, it’s quite a party.

While the U.S. government is famously running up debt to stratospheric levels, governments worldwide have been spending beyond their means and borrowing to make ends meet.

The likely result: financial markets put at risk by over-extended governments and slow economic growth for pretty much everybody.

“Public debt as a fraction of gross domestic product has increased significantly in recent decades, across advanced, emerging, and middle-income economies,” write Tobias Adrian, Vitor Gaspar, and Pierre-Olivier Gourinchas for the International Monetary Fund (IMF).

“It is expected to reach 120 percent and 80 percent of output respectively by 2028.”

Public debt—money borrowed by governments—has steadily risen, they add, because years of very low interest rates “reduced the pressure for fiscal consolidation and allowed public deficits and public debt to drift upwards.” Then, COVID-19 disrupted the global economy, and governments responded by funding “large emergency support packages” on credit.

Now, with interest rates rising, the cost of servicing debt is going up, too. But governments continue to borrow as if nothing has changed. Of course, riskier governments have to pay higher interest rates.

“On average, African countries pay four times more for borrowing than the United States and eight times more than the wealthiest European economies,” United Nations Secretary-General António Guterres cautioned last summer with the release of A World of Debt: A Growing Burden to Global Prosperity. “A total of 52 countries – almost 40 percent of the developing world – are in serious debt trouble.”

As of 2022, that report revealed, global public debt stood at $92 trillion and rising. Interest payments displaced other expenditures in a growing number of nations, especially developing countries. High public debt crowds out financial room for everything else, including the ability of private parties to borrow to start or expand businesses that create jobs and build wealth.

Then we come to a criticism we didn’t remember to address in the previous post:

Public Debt Crowds Out Private Investment“Households who buy government debt reduce their savings in productive private investments,” Kent Smetters and Marcos Dinerstein wrote in 2021 for the Penn Wharton Budget Model. As the spending is unproductive, the economy is poorer, and total savings are lower due to capital crowding out.”

At first blush, that sounds reasonable. Putting your dollars into a T-security account seems to remove them (temporarily) from the economy.

If you had bought stock or private sector bonds, the dollars would have remained in the economy — except for three facts:

1. You still own those dollars. They are part of your wealth. You can sell them or use them as collateral for loans. Your ownership allows you to borrow more at lower rates than if you didn’t own them. This ability is economically stimulative.

2. They earn net additional dollars in interest. While stock dividends and private-sector bond interest increase your wealth, those dollars come from the private sector.

They do not earn net dollars. They are mere dollar transfers within the private sector. By contrast, federal interest comprises new dollars that add to the private sector’s money supply.

3. That so-called “reduction in savings” is offset by the federal government’s spending into the economy. The dollars you deposit into a T-bill, T-note, or T-bond were derived from the federal government’s deficit spending.

Federal total net deficit spending = Total T-security deposits.

Thus, Tuccille doesn’t realize he is taking both sides of the issue. He dislikes federal deficits, which add dollars to the economy, but criticizes deposits into T-security accounts for taking dollars from the economy.

“Government spending redirects real resources in the economy and can crowd out private capital formation,” they add. “An additional $1 trillion debt this year could decrease GDP by as much as 0.28 percent in 2050.”

How does federal spending crowd out capital formation? Does the government paying your Medical bills crowd out anything? No.

Does paying your Social Security crowd out anything? No.

Does paying private contractors to build a road, bridge, or dam crowd out anything? No.

Does even paying federal employees crowd out anything? No.

Every dollar the federal government spends is a newly created dollar that winds up in the U.S. economy or other nations’ economies. Nothing is crowded out. Capital formation is a result of federal deficit spending.

If you take that insight and apply it to a world of governments on a collective borrowing spree, you end up with a hobbled global economy where prosperity becomes increasingly elusive.

Except for a tiny reality. Prosperity has not become increasingly elusive for the Monetarily Sovereign nations and even for most of the monetarily non-sovereign nations.

The reason: U.S. deficit spending pumps new inflation-adjusted dollars into the world’s economies. We are net importers, meaning we export more dollars than we import.We help the world (and ourselves) become richer.

“Medium-term growth rates are projected to continue declining on the back of mediocre productivity growth, weaker demographics, feeble investment and continued scarring from the pandemic,” note IMF’s Adrian, Gaspar, and Gourinchas.

“Projections for growth five years ahead have fallen to the lowest level in decades.”

First, these are IMF projections, which notoriously are suspect. These folks don’t even say how or whether they include Monetary Sovereignty in their analyses.

Second, it is not reasonable to make a general statement about “medium-term growth rates” without specifying the term and the difference between Monetarily Sovereign nations and monetarily non-sovereign nations.

It is like predicting the growth rate of the world’s children, without specifying their diet and living conditions.

Heavy government borrowing also creates risk for the financial sector by putting banks at the mercy of massive debtors of uncertain creditworthiness.

“The more banks hold of their countries’ sovereign debt, the more exposed their balance sheet is to the sovereign’s fiscal fragility,” note the IMF analysts.

The article supposedly is about U.S. federal debt being too high. But Tuccille drifts off into non-sequiturs.

The U.S. government does not borrow. It creates every dollar it needs ad hoc. This is the process:

1. To pay a bill, the federal government creates instructions (checks, bank wires, currency), not dollars.

2. It sends those instructions (“Pay to the order of . . . ) to each creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

3. At the instant the creditor’s bank does as instructed, dollars are created and added to the M2 money supply measure.

4. The bank then clears its action through the Federal Reserve, a federal agency. One branch of the federal government approves another branch’s instructions.

Thus, in a literal sense, banks create dollars. The notion that banks are “at the mercy of governments” is absolutely true because governments make all the rules by which banks must live.

And yes, banks are at the mercy of a government’s fiscal fragility.

But that begs the question, “Is the U.S. federal government fiscally fragile? The answer is a resounding “No”! (unless Congress, in a moment of MAGA insanity, insists on not paying bills.

Heavily indebted governments also reduce their ability to act as backstops in a financial crisis as they become the likeliest causes of future crises.

As they continue to borrow, they reduce the likelihood that productive private economic activity will grow them out of their financial problems.

Here, Tuccille demonstrates abject ignorance about the difference between Monetary Sovereignty and monetary non-sovereignty. The U.S. federal government is not “heavily indebted” because it could if it chose to, pay all its current and even future bills today.

It simply could send instructions to every creditor’s bank, instructing all those banks to increase the balances in the creditors’ checking accounts. Instantly, all debt, current and future, would disappear.

“Higher government debt implies more state interference in the economy and higher taxes in the future,” The Economist points out in its interactive overview of global government debt.

One would think that a publication titled “The Economist” would understand that while state/local taxes fund state/local spending, federal taxes do not fund federal spending. Even if the federal government didn’t collect a penny in taxes, it could continue spending forever.

The purpose of federal taxes is to:

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward, and

Assure demand for the U.S. dollar by requiring the dollar to be used for tax payments.

To make the populace wrongly believe that federal benefits are unaffordable without tax increases, thus reducing the clamor for more benefits.

Also, add the editors, rising debt “creates a recurring popularity test for individual governments,” which often goes poorly regarding fiscal responsibility because paying outstanding bills isn’t popular with voters.

Paying outstand bills isn’t unpopular. It’s collecting taxes that ostensibly are necessary; that’s the unpopular part.

Higher Debt Leads to Lost Prosperity

Well, isn’t that cheerful? It’s also extraordinarily unfortunate. After thousands of years of grindingly slow progress, recent decades saw the human race escaping poverty.

According to the World Bank, even as populations increased, the number of people living below the poverty line, adjusted for inflation, plummeted from 2.01 billion in 1990 to 689 million in 2019.

In 2016, the economist Deirdre N. McCloskey attributed improving prospects for many of the world’s people to “liberalism, in the free-market European sense.”

But that progress reversed in recent years, with poverty blipping back up (712 million people in 2022) amidst slower economic growth and after drastic government interventions during the pandemic.

A future of stumbling economies hobbled by debt-ridden governments that crowd out private investment is one in which more people are poorer than they would have been if the world had stuck with free markets and implemented a modicum of financial responsibility.

Again, Tuccille was supposedly talking about the U.S. government, except he is mixing some monetarily nonsovereign governments into his comments.

The U.S. “federal debt” has grown from $40 billion in 1940 to $30 trillion in 2024. Where is the crowding out and the poverty he is wringing his hands about? Certainly, not in the U.S., the supposed subject of his article.

I can’t say whether Tuccille is incompetent or dishonest. You decide. Either way, he is wrong, wrong, wrong.

As concerned as the U.N. is about rising public debt, its proposed “solutions” are pretty much what you would expect from that organization. A lot of verbiage about a “more inclusive” system providing “increased liquidity” and “affordable long-term financing” boils down to letting the riskiest governments have a greater say in offering themselves cheap financing. What could possibly go wrong?

The IMF analysts, on the other hand, propose “durable fiscal consolidation” while “financial conditions remain relatively accommodative and labor markets robust.”

I take that as a gentle suggestion that governments need to start paying down their debt to sustainable levels before interest rates and economic conditions deprive them of any options in the matter.

There is only one way for the U.S. government to “pay down its debt.” It has to run surpluses, i.e., to take dollars out of the economy.

That is the worst idea since investing money with Bernie Madoff. Here is what happens every time the federal government pays down its “debt.”

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Recessions (vertical gray bars) are preceded by declines in federal deficits and cured by increases in federal deficits.

It’s not just deficits, but deficit increases that are necessary for economic growth.

Would someone please tell Mr. Tuccille that taking money out of the economy causes recessions if we are lucky and depressions if we aren’t. Remind him that GDP = Federal Spending + Non-federal Spending + Net Exports.

Gentle suggestion or not, governments need to get their fiscal affairs in order before they take us all down with them.

Heavily indebted governments result in burdened economies, leading to a poorer world for everybody.

With its irresponsible borrow-and-spend ways, the U.S. government is, unfortunately, not alone. Most, if not all, world governments are hanging out in very bad company.

Wrong in every regard. Not just wrong but diametrically wrong, pitifully wrong, harmfully wrong.

With Americans living longer and spending more years in retirement, the nation’s changing demographics are “putting the U.S. retirement system under immense strain,” according to BlackRock CEO Larry Fink in his annual shareholder letter.

One way to fix it, he suggests, is for Americans to work longer before they head into retirement.

The backstory: “Rich” is a comparative term. A person owning $100 thousand would be rich if everyone else had $10,000, but that person would be poor if everyone else had $1 million. The income/wealth/power Gap is the key.

The way to become richer is to accumulate more for yourself or to ensure that everyone else has less (i.e., widen the income/wealth/power Gap between you and those below you).

The illogic of cutting Social Security

The very rich, who run America, have chosen both paths. They bribe politicians to carve out income tax breaks for themselves so they can accumulate more money, while they insist that everyone else pay more taxes to widen the Gap.

“No one should have to work longer than they want to.

But I do think it’s a bit crazy that our anchor idea for the right retirement age — 65 years old — originates from the time of the Ottoman Empire,” Fink wrote in his 2024 letter, which largely focuses on the retirement crisis facing the U.S. and other nations as their populations age.

Rich man Fink begins with the pseudo-compassionate phrase, “No one should have to work longer than they want to.”

He cluelessly forgets that our finances require many of us to work longer than want to.

It’s the “Let ’em eat cake” syndrome.

And what is Fink’s definition of the “retirement crisis facing the U.S.”?

Fink’s suggestions about addressing the nation’s retirement crisis come amid a debate about the future of Social Security, which will face a funding shortfall in less than a decade.

Some Republican lawmakers have proposed raising the retirement age for claiming Social Security benefits, arguing, like Fink, that because Americans live longer, they should work longer, too.

Suddenly, Fink’s claim that “No one should have to work longer than they want to” disappears. Now it’s, “If you live longer, you should work longer” — uh, except if you’re rich, in which case you can retire any time you damn well please. Money has its privileges.

This is based on the preposterous notion that the Monetarily Sovereign U.S. government is running short of its own sovereign currency — a currency it creates at will by simply pressing a few computer keys.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Note that Mr. Fink’s implied claim of federal government poverty does not extend to setting a high minimum age for benefitting from tax shelters and other tax avoidance devices available to the rich.

See: Ten Ways Billionaires Avoid Taxes on an Epic Scale (Read these and you’ll be shocked and angered at the desire to cut your Social Security benefits.)

Why should the poor be allowed to retire at age 65? That’s reserved for us,

For example, At least 18 billionaires received stimulus checks in 2020, because their tax returns placed them below the income cutoff ($150,000 for a married couple).

Incredible, huh?

How about this suggestion: Change the laws so that none of these “ways” would be available to anyone under the age of, say 85?

Does that sound reasonable to protect our government from the phony insolvency the rich like to claim is imminent?

However, that ignores the reality of aging in the workplace, with the AARP finding in a 2022 survey that the majority of workers over 50 say they face ageism at work.

Many older Americans stop working before they plan to because of ill health or an unexpected job loss.

In fact, the median age of retirement in the U.S. is 62—even lower than the “traditional” retirement age of 65.

Did all those folks “want” to retire and live their remaining years in poverty? Fink must think so.

Fink is right in saying that the retirement system isn’t working for most households, noted retirement expert and New School of Research professor Teresa Ghilarducci told CBS MoneyWatch.

But his assessment that people should work longer misses the mark, she added.

“After a 40-year-old experiment of a voluntary, do-it-yourself-based pension system, half of workers have no easy way to save for retirement,” she said.

“And in rich nations, why isn’t age 65 a good target for most workers to stop working for someone else?”

She added, Working longer won’t get us out of this. Most people don’t retire when they want to, anyway.”

“Get us out of this?” What is the “this” we have to get out of?

Social Security is a federal agency. No federal agency can run short of U.S. dollars unless that is what Congress and the President want. Congress, the White House, and SCOTUS all are federal agencies. Where are the fake “trust funds” that supposedly support (i.e. limit) them?

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

For you folks who have been indoctrinated with the twin false notions that . . .

Federal taxes fund federal spending, and

Money “printing” causes inflation,

. . . why aren’t you screaming about the benefits to the rich rather than “getting out of this” by cutting benefits to the non-rich?

To be sure, America’s retirement gap, or the gulf between what people need to fund their golden years versus what they’ve actually saved, isn’t new, nor is Social Security’s looming funding emergency.

Social Security doesn’t have a “funding emergency.” It has a fake emergency based on ignorance of Monetary Sovereignty and promulgated by stooges for the rich.

There. Is. No. Funding. Emergency.

Period.

The U.S. government has infinite money.Even if the federal government didn’t collect a single penny in taxes, it still could continue funding Social Security and Medicare and everything else, forever.

Federal taxes have two purposes, and neither of them is to fund federal spending:

To control the economy by taxing what the government wishes to limit (like your ability to acquire more wealth, unless you’re already wealthy) and

To assure demandfor the U.S. dollar by requiring you to pay taxes in dollars.

The federal government has run out of money. You have plenty. We need to raise your taxes.

There is a third, unofficial purpose.

3. To make you believe the Big Lie that federal benefits to you are “unsustainable” and imprudent. (Federal benefits to the richare O.K., however)

Yet Fink’s comments are noteworthy because of his status as the head of the world’s largest asset manager, with more than $10 trillion in assets, including many retirement accounts.

Gee, you think that wealth affects his ‘Qu’ils mangent de la brioche’ attitude?

Of course, Fink has a vested interest in Americans boosting their retirement assets, given that his firm collects fees from those accounts.

And in his letter, he also promotes a new target-date fund from BlackRock called LifePath Paycheck, which will roll out in April.

“He’s steering the conversation toward BlackRock — and a lot of people who talk about Social Security reform on Wall Street want to privatize it in some manner and make money,” Boston University economist Laurence Kotlikoff, an expert on Social Security, told CBS MoneyWatch.

Sure, privatize Social Security, so the rich, who never have enough, can have even more, thus widening the Gap.

It’s already begun with the deceptive Medicare Advantage plans, which are being promulgated by the rich as a new way to make money off of Medicare.

I’m broke. Send me money.

For no financial reason whatsoever, Medicare only covers 80%, and doesn’t cover things like dental care, weight loss drugs, and many other health care services.

So in step the rich, to provide what Medicare doesn’t, and thus make money: Medicare Advantage

But there is a kicker. When you need something really expensive, you run into the Medicare prior authorization scam. Gotcha!

Yes, your $100 dental bill may be covered, but that $50,000 surgery will require you to jump through hoops, and even then you may not be covered.

Surprised? You shouldn’t be. The profit motive in healthcare is ruthless and unnecessary.

To be sure, Fink also praises public policy success stories for addressing retirement savings, such as Australia’s system, which began in the early 1990s and requires employers to put a portion of a worker’s income into a fund.

Today, Australia has the world’s 54th largest population but the 4th largest retirement system, he noted.

That’s better than America’s system, but it still is divorced from reality. Australia’s government is Monetarily Sovereign. It could have an infinitely large retirement system without taking a penny from workers’ income. The U.S. could do the same.

“As a nation, we should do everything we can to make retirement investing more automatic for workers,” he noted.

Your doctor may say, “Yes, ” but our computers say, “No.”

Oh, how pious. Apparently, “everything we can” doesn’t include a federally funded Social Security benefit for every man, woman, and child in America.

The rich already are able to self-fund such a plan, but have convinced the not-rich that we don’t deserve that kind of help from an infinitely wealthy government.

Yeah, yeah, “too good to be true,” “it’s unsustainable,” “unaffordable,” “causes inflation,” “people won’t work if you give them benefits,” and all the other BS excuses the rich throw at you.

In America, we have 70 million + suckers who believe the idiocy a proven liar like Donald Trump tells them, but scant few who believe actual facts about our government.

We suckers don’t demand Social Security for All and Medicare for All. We argue against our own best interests. That’s what makes us suckers.

By contrast, the rich never argue against their own best interests.

Fink, who was born in 1952, said that his generation has an obligation to help fix the nation’s retirement problems.

The financial insecurity facing younger Americans, such as millennials and Gen Z, are creating generations of disillusioned, anxious workers, he noted.

How noble of Fink. How will he “face his obligation”? By cutting your benefits.

“They believe my generation — the baby boomers — have focused on their own financial well-being to the detriment of who comes next. And in the case of retirement, they’re right,” Fink wrote.

He added, “And before my generation fully disappears from positions of corporate and political leadership, we have an obligation to change that.”

Oh, they’ll change it . . . by applying leeches to cure our anemia.

Sure, Mr. Fink, we suckers accept your premise that the best way to cure our lack of money is to take money from us.

We believe it because it’s what everyone tells us, and we are too dense to understand reality.

But don’t worry that any of us will see the irony in all that.

For 25 years I’ve been preaching the idiocy of an infinitely wealthy government taking dollars from the populace, and what has that accomplished? Nada.

We couldn’t save enough to retire.

The vast majority still accept the obvious Big Lie that federal benefits are limited by federal taxes (except for benefits to the rich.)

It never occurs to us that though federal deficits have grown from 40 Billion in 1940 to 32 Trillion in 2023, we still believe deficit spending is unsustainable, unaffordable, and will cause the sky to fall.

We follow that up by laughing at the stupid public, except we are the stupid public.

(If life is like a poker game, and you’ve been playing for a while, but don’t know who the patsy is, you’re the patsy.)

Boomer (and older) lawmakers and politicians often don’t see eye-to-eye on how to fix the retirement crisis.

But failing to fix the issue damages not only the retirements of individual Americans, but the country’s collective belief in the future of the U.S., Fink noted.

“We risk becoming a country where people keep their money under the mattress and their dreams bottled up in their bedroom,” he noted.

How true.

I just turned 89 and am growing weary of telling you not to answer Emails from Nigeria, not to touch hot stoves, not to tell strangers your Social Security number, and not to believe a government that created the U.S. dollar from thin air can become insolvent.

This blog has posted more than 3,000 articles, most of which make two fundamental points.

The U.S. government can afford anything, without collecting money from you.

If you’re not screaming like hell at the Big Lie, if you’re not demanding that your politicians tell you the truth, you deserve what you get.

Or do nothing and let the rich continue to screw you.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

Some economists, politicians, and media talking heads might tell you it means the airlines are seriously in debt.

OK, that “3 trillion” is not dollars; it’s miles or points. But there is a point (pun intended) to be made.

Frequent flyers, consider yourselves warned: Sitting on a pile of unused airline miles could cost you.

Liabilities tied to the five most valuable airline-loyalty programs in the U.S. soared almost 12% to $27.5 billion last year, according to new analysis by LendingTree Inc.’s consumer-finance website ValuePenguin.

Airlines looking to shore up their balance sheets could reduce the value of those rewards or reinstate policies that allow miles or points to expire, the firm warned.

If the airlines wanted to reduce their mileage “debt,” they arbitrarily could reduce the value of their mileage reward points or allow miles to expire.

They are mileage-points sovereign.As the issuer of mileage points, the airlines can do anything they wish with those points. They can issue as many as they wish, increase or reduce the value, or void them simply by pressing computer keys.

If the Airlines felt generous, they could give you a few million mileage points. Or if they felt stingy, they could “tax” you points by reducing their value. Suddenly, flying to your favorite city would cost you double the number of points you thought. Effectively, that would be a 50% “wealth” tax on your point holdings.

Or they could tell you to use all your points by December 31st at which time the points would be worthless. The effect would be like a tax on you.

The airlines are to mileage points as the U.S. federal government is to U.S. dollars. By giving out more points than they receive, the airlines run “points deficits”; cumulatively, the airlines have “points debt.”

The airlines create points by pressing computer keys. Nothing prevents the airlines from pressing keys, forever. The U.S. government creates dollars by pressing computer keys. nothing stops the U.S. government from pressing keys, forever.

Being points sovereign, the airlines never can run short of mileage points. The U.S. government, being Monetarily Sovereign, never can run short of dollars.

The airlines never borrow points. The government borrows dollars.

“Especially in a time where airlines have gone through such financial issues, it would be easy to see that they would look at some sort of devaluation of the miles and points as a way to make up a little bit of financial ground,” Matt Schulz, LendingTree’s chief credit analyst, said in an interview.

“I would suspect we might see something like that going forward.”

This demonstrates the total control a Monetarily Sovereign entity has over its currency, whether airline points or dollars. The airlines create all the rules re. points. The government creates all the rules (i.e. laws) regarding dollars.

At the height of the Covid-19 pandemic, Delta, American, and United pledged their loyalty programs as collateral for bonds as the virus and resulting government restrictions sapped travel demand. Such deals could prevent any material changes to the programs, said Joe DeNardi, an analyst with Stifel Financial Corp., who follows airline loyalty programs closely.

United, for its part, doesn’t see currency devaluation as a handy tool to lower that accounting liability, said Michael Covey, managing director of the loyalty program at the airline.

Yes, it’s an accountingliability, but not a real liability because the airlines have total control over its value. They arbitrarily can create points by pushing computer keys, or they could eliminate the points altogether. Goodbye, “points debt.”

Does an airline owe someone a billion points? No problem. They can just type 1,000,000,000 into a computer and Voila! Here are the billion points.

Does the federal government owe someone a billion dollars? No problem. Just type the number into a computer and the dollars come into existence.

Think about that the next time someone tells you that Medicare or Social Security are running short of money.

A decade ago, revenue-based airline programs (rather than mileage-based) were fairly uncommon in the U.S. JetBlue was one of the first U.S. airlines to launch a revenue-based program when it revamped its program in 2009. Southwest followed with a program “enhancement” in 2011.

Then, the big airlines jumped on the bandwagon. Delta transitioned to a revenue-based system in 2015, and American Airlines and United quickly followed suit. Now, almost all major U.S. airlines operate a revenue-based program.

There again is that total control a monetary sovereign has over its currency. The airlines arbitrarily went from awarding mileage points to awarding revenue points.

However, programs differ a bit in how they award miles.

For better or worse, the three biggest U.S. airlines have similar mileage earning systems. General members earn 5 miles per dollar of eligible spending on travel with the airline.

Elite members earn a bonus on this base earning, with all three programs topping out at 11 miles per dollar for top-tier elites.

On Dec. 9, 2021, Delta became the first domestic airline to make basic economy fares ineligible for mileage earning. Basic economy flyers will no longer earn SkyMiles or Elite Qualifying Miles, Dollars, or Segments.

Again, the above demonstrates the total control by a monetary sovereign. Delta simply made the change by fiat. The federal government can, and often has, arbitrarily changed the value of the U.S. dollar.

The “Nixon shock” was an arbitrary move by President Nixon to end the convertibility of dollars into gold. Suddenly, the dollar was no longer worth 1/35th of an ounce of gold.

If airlines made the same kind of change, suddenly airline points would no longer be worth 1 cent or 1.5 cents each. The “problem” of the “points debt” would disappear.

Selling frequent-flyer points to banksAirlines make money from loyalty programs by selling frequent-flyer points to banks, which then award them to credit card holders as purchase rewards.

The banks pay airlines 1 to 1.5 cents per mile, plus a bonus when new customers sign up for their branded credit card.

By selling their loyalty program frequent flyer miles to banks, credit card companies, car rental firms, hotels, and supermarkets, the airlines have found an almost guaranteed way to make a profit from their tickets.

In effect, most major airlines have a business model which is more like a bank than a transport company.

No, it’s not more like a bank. It’s more like a Monetarily Sovereignnation— Canada, Mexico, the UK, Australia, Japan, China, and yes, the United States — all of whom can create andvprice their currencies at will (unlike monetarily non-sovereign entities like cities, counties, states, euro nations, businesses, you, and me.)

This is the airline profitability program:

The airlines create points from thin air. They create as many points as they wish at virtually no cost.

Of course, airlines have to offer travel in exchange for points, so that is a cost of the program, but:

Airlines control how many points each flight costs passengers. So, high-demand days cost far more points than other days. This way, the airlines dissuade passengers from using points on those days when they can sell seats for dollars.

This shows you that Monetary Sovereignty is everywhere, though the public is kept in the dark. (See: “The genius of the board game, Monopoly.”)

When a retailer issues coupons, they essentially issue money in lieu of a price reduction. The retailer is sovereign over the coupons and can issue as many coupons as he wishes and make them any value he wishes.

All outstanding coupons could be counted as retailers’ “debt” – -i.e., the value of outstanding coupons—except customers pay for the coupons when they buy the products.

Imagine an airline saying, “We are going to raise the price of a seat from 100 points to 200 points because we are running short of points.”

You would think that’s crazy. How could an airline run short its points, points it creates at will, by clicking computer keys?

But that is exactly what the federal government says when it claims Medicare and Social Security are short on dollars.

You should ask the same question. How can the U.S. federal government run short of its own dollars, dollars it creates at will by clicking computer keys?

The reason you don’t ask is simple. No one questions the airlines’ ability to create their points at will, but your information sources tell you the U.S. government can’t create its dollars at will.

They tell you the federal debt (that neither is federal nor debt) is “unsustainable.” They tell you the government should “ive within its means.” They tell you your taxes must be increased and/or your benefits reduced.

All these statements are deceptive, based on the hope that you don’t understand Monetary Sovereignty. The lie that the federal government can run short is dollars is told so that the rich can become richer while the rest survive in ignorance.

It’s that sort of ignorance someone like Eric Boehm promulgates when he writes an article like this:

The article pretends that the federal government is not Monetarily Sovereign, can’t create dollars at will, needs tax dollars to pay its bills, and in some unexplained way actually could run out of U.S. dollars.

It’s a monstrous lie, aimed at keeping you down and the rich up by widening the income/wealth Gap between the rich and you.

If you ever feel like protesting something, this is what you should protest. The Big Lie in economicsthat the federal government can’t afford to provide certain benefits and/or that taxpayers fund federal spending.

The lie claims the U.S. “debt” is a “ticking time bomb,” to scare you. (It’s a “bomb” that has been “ticking” since 1940, and still no explosion.)

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.