Twitter: @rodgermitchell; Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

============================================================================================================================================================================================================================================================

Science is the search for cause and effect. The human thought process first answers the question, “What?” then seeks, “Why?” and “How?”

Scientific thought begins with facts, from which are derived data and finally conjecture (hypothesis).

Scientific proof comes from physical evidence, predictability, and reproducibility. In chemistry, a physical science, the prediction can be made that combining chlorine with sodium will produce (predictability) common salt. So chemists repeatedly combine those two elements (reproducibility), and repeatedly produce salt (physical evidence).

Social sciences, of which economics is one, rely on the vagaries of human thought, emotion, superstition and belief. Predictability, reproducibility and physical evidence often are lacking.

What then constitutes proof in economics? There are no proofs in economics. There only are facts and data from which emerge hypotheses.

Hypotheses are not certainty. Facts and data can breed multiple hypotheses. The lack of scientific certainty can produce emotional certainty, with resultant firm beliefs leading to strong disagreements. (Think of disagreements about religion and politics.)

Though the science of economics is massively complex, and even includes its own mysterious technical jargon, the layperson can understand basic economics by learning just a few facts.

The following are what I believe to be those important facts of economics. If you, or any person, holds a conjecture that does not comport with these facts, this is your opportunity to eliminate a conflicting hypothesis from your beliefs.

Facts:

- All money is debt. There is no, nor ever has been, any form of money that is not debt.

- The value of debt/money is supported by collateral, which determines its acceptance.

- All money is created by debtors, who owe the holders of money, full faith and credit as collateral. The collateral for the U.S. dollar is the full faith and credit of the U.S. government.

- The secondary collateral for money may be a physical asset, for instance gold, a house, a car, land, etc. While gold, houses, cars and land are not in themselves money, additional collateral can increase the acceptance of money.

- All money is created by laws. In the late 1770’s, the new U.S. federal government created laws from thin air. Some of these laws created the original dollars, also from thin air. Money-creation laws may be written, oral or mutually understood. All laws and all forms of money are no more than ideas, with no physical existence. The federal government’s legal device for money creation is deficit spending.

- Any person or group of people can create money, simply by passing or agreeing to laws that create debt. Such money creators are known as “borrowers” and “debtors.” Examples are: Banks that accept deposits (which they owe to depositors), mortgagors (who owe to mortgagees). In each case, the acceptance and Value of money is based first on the borrower’s full faith and credit.

- In addition to full faith and credit, the Value of money is based on Supply and Demand, according to the formula: Value = Demand/Supply.

- Demand = Reward/Risk. The Reward for owning money is interest, with increased rates causing increased Demand. The Risk of owning money is inflation.

- Laws have no physical existence. Having no physical existence, laws can be created in unlimited quantities by any person or entity, their only effective limit being their acceptance.

- Because all money is created by laws, money can be created in unlimited quantities by lawmakers. This is known as Monetary Sovereignty, the unlimited ability to create a sovereign currency by the creation of laws.

- Lawmakers never can unintentionally run short of their own sovereign currency. The simple expedient of passing a new law, gives the lawmakers unlimited ability to pay any debt denominated in their own sovereign currency.

- A lawmaking entity never needs to ask (by taxing or borrowing) outside entities for supplies of its own sovereign currency. The U.S., for instance, being Monetarily Sovereign, neither needs nor uses taxing or borrowing to pay its obligations.

- Federal financing is unlike personal financing. Federal deficits are not directly linked to federal debt. Deficits, the difference between taxes and spending, are not directly linked to federal debt, the total of deposits in T-security accounts at the Federal Reserve Bank. Federal deficits could exist without federal debt, and federal debt could exist without federal deficits.

- U.S. “borrowing” consists solely of providing safe storage and investment of its own sovereign currency, the dollar, via Treasury accounts (bills, notes and bonds) at the Federal Reserve Bank, i.e bank accounts. (The term “debt” for these accounts can be misleading in that unlike personal and business debt, FRB accounts are not a burden on the Monetarily Sovereign federal government. The FRB accounts are paid off, as are all other bank accounts, by simple transfers of existing dollars from the FRB accounts to checking accounts.)

- A Monetarily Sovereign entity pays debts denominated in its own sovereign currency, by creating its sovereign currency ad hoc, and delivering that sovereign currency to creditors. The entity neither needs, nor uses, nor even retains taxes denominated in its own sovereign currency.

- Inflation (i.e price inflation) is the loss in Value of a currency compared with the prices of goods and services. Value (or Price) = Demand/Supply.

- Inflation can be caused by any combination of:

- An increase in the Supply of a currency

- A decrease in the Demand for a currency

- An increase in the Demand for goods and services

- A decrease in the Supply of goods and services.

- An decrease in the Reward for owning money (interest)

- An increase in the risk of owning money (cumulative inflation)

====================================================================================================================

You now know the most important facts in the science of economics.The following is a mention of selected data and conjecture. The purpose of this mention is to address certain common misconceptions about money.

The sole purposes of taxing are political and as money-supply control.

Politically, taxes give the illusion that they pay for spending. The purpose is to limit financial demands by the populace. (Many leaders fear that demands for money would grow excessively if the populace ever were to understand that the federal government is not limited in its ability to pay bills.)

- Leaders claim that money creation (incorrectly called “printing”) will lead to an uncontrollable inflation and,

- Leaders fear that the gap between the rich and the rest will narrow.

(The gap is what makes the rich rich. Without the gap, no one would be rich, and the wider the gap, the richer they are. So, the rich want the gap to widen. They pay politicians, the media, university economists, and other influentials to cut deficit spending [money creation] and to tell the populace that the federal government is monetarily non-sovereign, federal taxes are necessary for federal spending, and federal “debt” is owed by taxpayers.)

Historically, inflations have been caused by a decrease in the Supply of goods and services (primarily, oil and secondarily, food), with an increase in the Supply of currency being an exacerbating government response, not the initial cause.

Historically, inflations have been prevented and cured via interest rate control and increased Supply of goods and services.

Though some economists recommend controlling inflation by reducing the supply of money (increased taxation and/or reduced spending), these devices are determined by Congress, and therefore are slow, politically controversial and inexact. By contrast, interest rate increases can be accomplished quickly by the Federal Reserve and in small increments.

For comparison:

Meteorology, like economics, currently suffers limited predictability and reproducibility, primarily because of the mathematically chaotic nature of weather. Like economics, it one day may mature as a science, when computer modeling of historical data improves.

Religion is not, and never will be, a science. It is based solely on one fact (the universe exists), with no data leading to the prime conjecture, the existence of one or more gods, and no proofs.

Rodger Malcolm Mitchell

Monetary Sovereignty

===================================================================================

Ten Steps to Prosperity:

1. Eliminate FICA (Click here)

2. Federally funded Medicare — parts A, B & D plus long term nursing care — for everyone (Click here)

3. Provide an Economic Bonus to every man, woman and child in America, and/or every state a per capita Economic Bonus. (Click here) Or institute a reverse income tax.

4. Free education (including post-grad) for everyone. Click here

5. Salary for attending school (Click here)

6. Eliminate corporate taxes (Click here)

7. Increase the standard income tax deduction annually Click here

8. Tax the very rich (.1%) more, with higher, progressive tax rates on all forms of income. (Click here)

9. Federal ownership of all banks (Click here and here)

10. Increase federal spending on the myriad initiatives that benefit America’s 99% (Click here)

The Ten Steps will grow the economy, and narrow the income/wealth/power Gap between the rich and you.

========================================================================================================================================================================================================================================================================================================

10 Steps to Economic Misery: (Click here:)

1. Maintain or increase the FICA tax..

2. Spread the myth Social Security, Medicare and the U.S. government are insolvent.

3. Cut federal employment in the military, post office, other federal agencies.

4. Broaden the income tax base so more lower income people will pay.

5. Cut financial assistance to the states.

6. Spread the myth federal taxes pay for federal spending.

7. Allow banks to trade for their own accounts; save them when their investments go sour.

8. Never prosecute any banker for criminal activity.

9. Nominate arch conservatives to the Supreme Court.

10. Reduce the federal deficit and debt

![]()

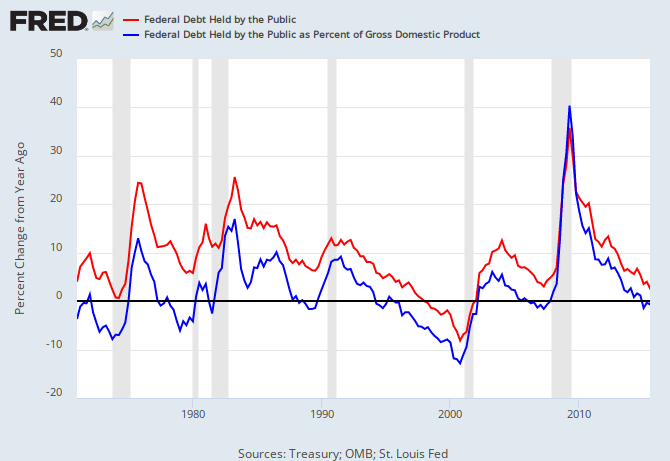

THE RECESSION CLOCK

Recessions begin an average of 2 years after the blue line first dips below zero. A common phenomenon is for the line briefly to dip below zero, then rise above zero, before falling dramatically below zero. There was a brief dip below zero in 2015, followed by another dip – the familiar pre-recession pattern.

Recessions are cured by a rising red line.

Vertical gray bars mark recessions.

As the federal deficit growth lines drop, we approach recession, which will be cured only when the growth lines rise. Increasing federal deficit growth (aka “stimulus”) is necessary for long-term economic growth.

————————————————————————————————————————————————————————————————————————————————————————————————-

Mitchell’s laws:

•Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

•Any monetarily NON-sovereign government — be it city, county, state or nation — that runs an ongoing trade deficit, eventually will run out of money.

•The more federal budgets are cut and taxes increased, the weaker an economy becomes..

•No nation can tax itself into prosperity, nor grow without money growth.

•Cutting federal deficits to grow the economy is like applying leeches to cure anemia.

•A growing economy requires a growing supply of money (GDP = Federal Spending + Non-federal Spending + Net Exports)

•Deficit spending grows the supply of money

•The limit to federal deficit spending is an inflation that cannot be cured with interest rate control.

•The limit to non-federal deficit spending is the ability to borrow.

•Liberals think the purpose of government is to protect the poor and powerless from the rich and powerful. Conservatives think the purpose of government is to protect the rich and powerful from the poor and powerless.

•The single most important problem in economics is the Gap between rich and the rest..

•Austerity is the government’s method for widening the Gap between rich and poor.

•Until the 99% understand the need for federal deficits, the upper 1% will rule.

•Everything in economics devolves to motive, and the motive is the Gap between the rich and the rest..

MONETARY SOVEREIGNTY