Mitchell’s laws: The more budgets are cut and taxes inceased, the weaker an economy becomes. To survive long term, a monetarily non-sovereign government must have a positive balance of payments. Austerity = poverty and leads to civil disorder. Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

==========================================================================================================================================

John Mauldin is a famous blogger, who publishes “Thoughts from the Front Line,” and books he promotes. He may be one of the best paid gardeners in the world. He never seems to understand Monetary Sovereignty, but today he may have outdone himself.

Here are a few excerpts from his blog:

Let me shock a few of my fellow Republicans and say that I think the deficit is such a deadly disease that it would be better for the country for the Democrats to be in power and forced to deal with the situation than to do nothing. I would not like their solution, and I think it would be harmful, but not as harmful as a second Depression, brought on by not dealing with the deficits and entitlement problems.

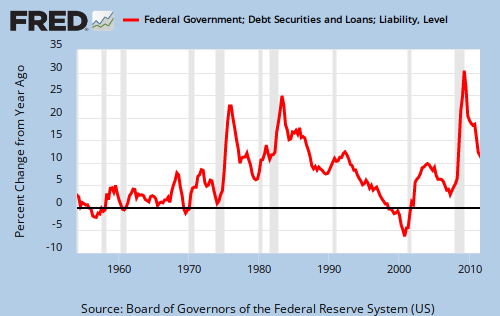

John, depending on how you define “Depression,” there have been at least six of them, not two, and all six have been brought on, not by deficits, but by surpluses:

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

The most recent recession, and virtually every recession, has come on the heels of reduced deficit growth and has been cured with increased deficit growth.

But why bother investigating facts when repeating popular wisdom is so much easier. After all, everyone is saying it, so it must be true.

Think what happens when any country has hit that debt limit. Greece is not having fun. And either Italy is going to be unhappy with the longer-term recession it will have, or Germany is going to be unhappy with the ECB backing Italian debt at below-market rates for a long time, which means printing money and a much lower euro.

Pardon me, John, but those countries are monetarily non-sovereign. The U.S. is Monetarily Sovereign. Really, after all these years, don’t you understand the difference? And “printing money and a much lower euro” translated means “deficits cause inflation.” But hasn’t the U.S. been running huge deficits for years? So where is the inflation?

The growing debt and the deficit is a deadly cancer on the economy. It will deliver a mortal blow to the economy if not dealt with. . . . Putting off treatment will not make the cancer go away by itself, and the cancer of our debt is clearly growing and malignant.

Allow me to translate, again. What John says is: The growing money supply is a deadly cancer on the economy. It will deliver a mortal blow to the economy if not dealt with. . . . Putting off treatment will not make the cancer go away by itself, and the money supply is clearly growing and malignant.

Yes, according to John, the economy has too much money, and GDP will grow better and faster if we reduce the supply of money. How that works, I’m not sure. I’ve asked him, but get no answer.

Then he goes on with the usual blah, blah, blah about how austerity now is better than austerity later, and we should increase taxes and/or reduce spending in order to achieve that austerity as soon as possible.

Yes, John, austerity is great. Ask those nations that have experienced it.

John Mauldin has outdone himself this time. He may be one of the best paid gardeners in the world. Think of how much makes spreading manure.

Rodger Malcolm Mitchell

http://www.rodgermitchell.com

![]()

==========================================================================================================================================

No nation can tax itself into prosperity, nor grow without money growth. Monetary Sovereignty: Cutting federal deficits to grow the economy is like applying leeches to cure anemia. Two key equations in economics:

Federal Deficits – Net Imports = Net Private Savings

Gross Domestic Product = Federal Spending + Private Investment and Consumption + Net exports

#MONETARY SOVEREIGNTY