No sooner do I publish, “Historical BULLSHIT Claims the Federal Debt Is a ‘Ticking Time Bomb’” than this IMF article pops up:

World’s $100 Trillion Fiscal TIMEBOMB Keeps Ticking

Story by Craig Stirling(Bloomberg) — Even before global finance chiefs fly into Washington over the next few days, they’ve been urged in advance by the International Monetary Fund to tighten their belts.

Two weeks ahead of a potentially era-defining US election, and with the world’s recent inflation crisis barely behind it, ministers and central bankers gathering in the nation’s capital face intensifying calls to get their fiscal houses in order while they still can.

Debt Loads Are Set to Expand Globally |

© Bloomberg

The fund, whose annual meetings begin there on Monday, has already pointed to some of the themes it hopes to press home with a barrage of projections and studies on the global economy in coming days.The IMF’s Fiscal Monitor on Wednesday will feature a warning that public debt levels are set to reach $100 trillion this year, driven by China and the US.

Managing Director Kristalina Georgieva, in a speech on Thursday, stressed how that mountain of borrowing is weighing on the world.

Before we continue, let me show you the graphs showing the debt/GDP ratios of several countries. Look at the graphs and tell me what is misleading about them.

The graphs at the right have two main problems:

1. They combine two completely different things: Monetarily Sovereign nations and monetarily non-sovereign nations.

A Monetarily Sovereign nation has the infinite ability to create its own sovereign currency. It never can run short of money to pay its bills.

The U.S. cannot run short of dollars. China cannot run short of yuan. Japan cannot run short of yen, and the UK cannot run short of pounds. These nations are Monetarily Sovereign.

They all can pay any debt denominated in their sovereign currency, merely by tapping a computer key.

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

By contrast, Germany, France, and Italy are monetarily non-sovereign. They all use the euro, and can run short of euros to pay their debts. They must borrow from the European Union (EU) when they run short of euros.

The G-7 graph is a mongrelization of Monetarily Sovereign and monetarily non-sovereign nations (Canada, France, Germany, Italy, Japan, United Kingdom, United States) and thus is useless and misleading.

2. The debt/Gross Domestic Product ratio, which is the subject of the graphs is meaningless, though it often has been used by those who do not understand Monetary Sovereignty.

Take a look at this worldwide comparison of debt/GDP and see if you can find any evaluative or predictive purpose for the ratio.

Here are the ten nations with the supposedly “worst” (highest) ratios:

Debt to GDP Ratio (%); Japan 264%, Venezuela 241%, Sudan 186%, Greece 173%, Singapore 168%, Eritrea 164%, Lebanon 151%, Italy 142%, United States 129%, Cape Verde 127%

Japan and the U.S. are ranked worst, along with Sudan, Greece, Lebanon, and Cape Verde.

Who would you prefer to lend to, Japan or Cape Verde? The United States or Sudan?

Now, here are the ten nations with the “best” (lowest) debt/GDP ratios: Brunei 2.1%, Kuwait 2.9%, Cayman Islands 4.5%. Afghanistan 7.4%. Turkmenistan 8%, Azerbaijan 11.7%, Burundi 14.5%, DR Congo 14.6%, Russia 17.2%, Palestine 18.5%

That’s right. According to the IMF, those are the financially safest places in the world.

The debt/GDP ratio is akin to a butter/butterfly ratio. Completely and utterly useless, yet here is the equally useless IMF shrieking about it.

This is what the IMF says about itself:

The International Monetary Fund (IMF) is an organization that aims to ensure the stability of the international monetary system. Its primary purposes are to:

1. Foster collaboration among countries to achieve global monetary stability.

2. Promoting exchange rate stability

3. Support economic policies that promote growth and reduce poverty.

4, Offer loans and financial aid to member countries facing balance of payments problems or economic crises.

5. Provide economic and financial advice.

It does none of those, except #4, which it uses like a loan shark, extorting unreasonable terms from weak countries. And really, would you take “economic and financial advice” from a group that doesn’t know the difference between Monetary Sovereignty and monetary non-sovereignty.

It is like taking medical advice from a quack doctor who doesn’t know the difference between heartburn and sunburn.

Continuing with the article:

“Our forecasts point to an unforgiving combination of low growth and high debt — a difficult future,” she said. “Governments must work to reduce debt and rebuild buffers for the next shock — which will surely come, and maybe sooner than we expect.”

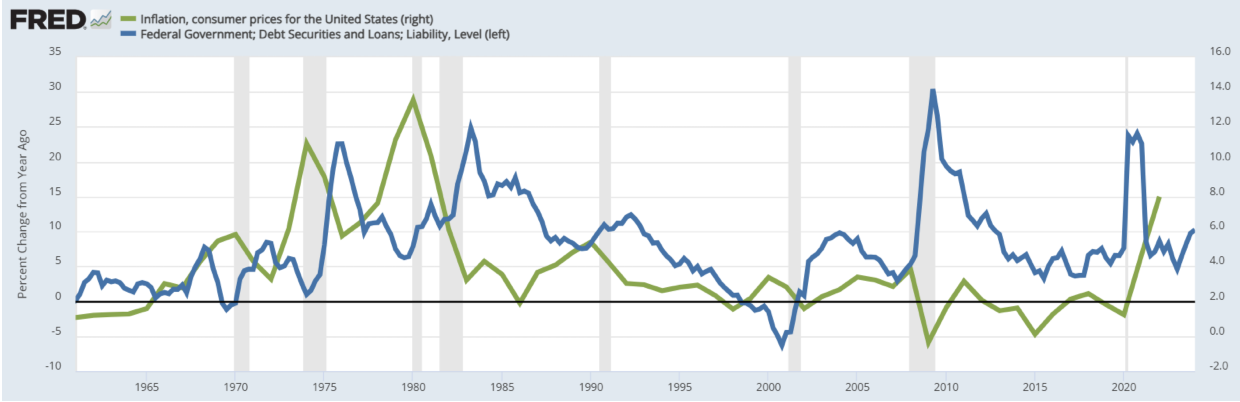

For a Monetarily Sovereign nation “high debt” generally means the government is pumping more growth dollars into the economy. Lack of debt growth leads to recessions:

Thus, the IMF’s “cut debt” advice is diametrically wrong, like taking blood from a patient to cure his anemia.

Some finance ministers may get further reminders even before the week is over.

UK Chancellor of the Exchequer Rachel Reeves has already faced an IMF warning of the risk of a market backlash if debt doesn’t stabilize. Tuesday marks the last release of public finance data before her Oct. 30 budget.

The UK tax office is taking a tougher approach to clawing back debts, insolvency specialists say, a bid to squeeze £5 billion ($6.5 billion) in extra revenue.

The above simple proves that many government economists are as financially ignorant as the IMF economists.

We have the same problem in the U.S., with so-called experts claiming our federal debt (which isn’t “federal” and isn’t “debt”) is a “ticking time bomb.” Total bullshit.

What Bloomberg Economics Says:

“For all the talk of black holes, the overall effect of Reeves budget will be a policy that’s looser, not tighter, relative to the previous government’s plans.”

As it should be if the UK wants economic growth. If the UK is foolish enough to listen to the IMF and cut debt (which means take dollars out of the economy), it will have a recession.

Meanwhile, Moody’s Ratings has slated Friday for a possible report on France, which faces intense investor scrutiny at present. With its assessment one step higher than major competitors, markets will watch for any cut in the outlook.

France, being monetarily non-sovereign, does risk it’s debt being too high to service. The EU, which is Monetarily Sovereign, could solve France’s financial problems by simply giving them euros. That would cost European taxpayers nothing, and would prevent debt from being an issue.

As for the biggest borrowers of all, the glimpse of the IMF’s report already published contains a grim admonishment: your public finances are everyone’s problem.

True for monetarily non-sovereign nations; not true for Monetarily Sovereign nations.

“Elevated debt levels and uncertainty surrounding fiscal policy in systemically important countries, such as China and the United States, can generate significant spillovers in the form of higher borrowing costs and debt-related risks in other economies,” the fund said.

We’ll end with the final dollop of bullshit from the IMF. China’s and the US’s increase in debt means other nations are being enriched by dollars and yuan. The more these two governments spend on foreign goods and services, the better all the other governments’ finances will be.

As usual, the fools and con men of the IMF offer diametrically the opposite of good advice.

:max_bytes(150000):strip_icc()/GettyImages-671519300-e1ecfe47b0734333a9ac17eb46f6f398.jpg)