“As the U.S. faces the consequences of runaway pandemic spending and deficitsthat could add $25 trillion to our existing $36 trillion national debtover the next decade, “neither party is serious” about tackling the problem.”

“The so-called ‘debt’ is nothing more than the total of deposits in T-security accounts at the Federal Reserve—a form of savings for the private sector, not actual borrowing.”

So, calling it a “national debt” is actually misleading. It’s not something the U.S. must “repay” in any traditional sense. It’s more accurate to think of it as net financial assets that the federal government has injected into the private sector.

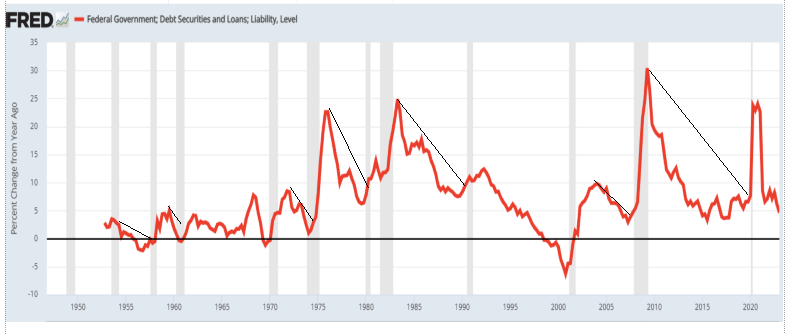

The so-called debt has risen, as the above graph demonstrates. It was very high during World War II, then fell to nearly nothing post-war.

But to cure the 2008 recession, it began its dramatic rise, which has Ms. de Rugy and virtually every other economist all aflutter. As she said:

“With Washinton in a state of bipartisn denial,’ the debt crisis will only get worse.’”

What exactly is the “debt crisis”? She never says. Actually, no one ever says what that “crisis” is. In fact, all the data seem to show that as the “debt” rises, the economy grows:

Gross Domestic Product grew dramatically as federal “debt” rose.

Along with fears about the federal “debt,” economists seem to shudder about the Debt/GDP ratio. We often have been told that when the ratio reaches 50%, 80%, 100%, or some other arbitrary number, then awful things will happen.

But they never happen.

The debt/GDP ratio now has exceeded 100%, and the economy continues to grow.

In our earlier posts, we demonstrated that the debt-to-GDP ratio is not a meaningful indicator. It does not predict the federal government’s ability to pay its debts (Its ability is infinite). The ratio does not show anything. See: “Enough already with the Debt/GDP ratio“)

What has been missing from all those claims is specificity. What exactly is the problem with high federal debt?

Here are some general claims, none of which is supported by data:

Higher Interest Rates

Claim: As the government “borrows more,” it competes with private borrowers, driving up interest rates (the “crowding out” argument).

No data supports this. The Fed sets interest rates. The U.S. doesn’t borrow in a market-driven way; it issues currency. So interest rates are a policy choice, not a supply-and-demand issue. There is no evidence that the vastly increased debt has forced interest rates up.

Inflation

Claim: More government spending = more money = inflation.

No data supports this: All inflations are caused by shortages, not “too much money.” Deficit spending that eases shortages (labor, housing, energy) can reduce inflation. The solution to inflation is targeted spending, not austerity. There is no relationship between federal spending and inflation. See: “At long last, let’s put this inflation question to bed.“

Debt Service Becomes Unsustainable

Claim: As debt rises, so do interest payments, “crowding out” other spending.

No data supports this: The federal government can always pay interest in its own currency. And again, it chooses interest rates. There’s no risk of involuntary default. There is no evidence that the vastly increased debt has crowded out private borrowers.

Burden on Future Generations

Claim: Today’s borrowing saddles future taxpayers with repayment.

No data supports this: Taxes don’t fund federal spending. “Paying off the debt” is just swapping Treasury securities (savings) for cash. No burden is passed on—future generations inherit the assets, not a liability.

Loss of Investor Confidence / Currency Collapse

Claim: If debt gets too high, investors may stop buying Treasuries, or the dollar could collapse.

No data supports this. Treasuries aren’t “bought” to fund the government—they’re offered as a place to park dollars that already exist. The government doesn’t need to entice buyers—it creates the dollars it spends. Plus, confidence in the dollar is based on productive capacity and stability, not some debt-to-GDP ratio.

SUMMARY

The so-called “federal debt” isn’t federal (the dollars in Treasury Securities are owned by the depositors, not by the government) or debt(the government merely holds the dollars for safekeeping, as with a bank safe deposit box).

It poses no threat to, or burden on, the government or the public.

The entire debt story is designed to convince the public to forego some of the benefits the federal government provides.

As Ms. de Rugy claims, “Republicans, for their part, try to convince voters they care about the deficit but feed the delusion that they can balance the budget through discretionary spending cuts that leave Social Security and Medicare untouched.”

That is the story the wealthy tell. They want to cut social programs to widen the income/wealth/power Gapbetween them and the rest of America. The wider the Gap, the richer are the wealthy.

I can’t say whether Ms. de Rugy is in cahoots with the rich or merely ignorant of Monetary Sovereignty. Still, articles like hers greatly damage the nation’s economy and people.

Economics is a science loaded with data, but economists don’t believe the data.

This is what passes for “science” in the world of economics:

Raising interest rates increases the prices of everything. Therefore, raise interest rates to cure inflation.

Inflation happens when the economy grows too much (“overheated”). Therefore, to cure inflation, cause a recession or depression.

Any normal scientist would scoff at these beliefs, but economists are neither normal nor scientists. They are believers. They are cultish followers of the standard thinking, as exhibited in the following article.

When a hypothesis doesn’t work, a scientist uses that information to develop a new hypothesis. In economics, when a hypothesis doesn’t work, the economist merely shrugs and continues to claim it works.

Before COVID, the economy was growing massively, with interest rates near zero, massive deficits, and without inflation? Then, during and after COVID, we had inflation, with interest rates at elevated levels.

Did the economists learn anything from these events?

Hmmm. Now, let me think. Why did we have no inflation before COVID and elevated inflation during and after COVID? What changed? Two things”

We had shortages of oil, food, shipping, computer chips, metals, lumber, labor, and almost every other important good and service

The Fed raised interest rates, instantly making every product more expensive.

What didn’t change?

The government still is spending massively with huge deficits.

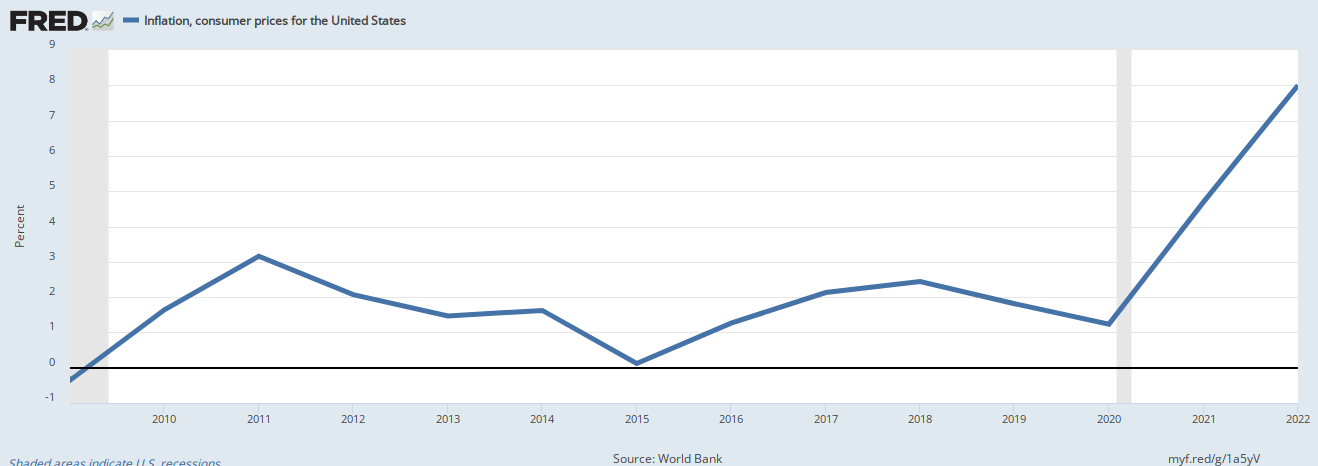

Analyze the following graph:

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.When supply cannot meet demand, prices go up. That’s basic.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.

Inflation has fallen from the shocking highs reached last year, but the Federal Reserve’s efforts have not successfully returned the beast to its cage.

The problem is supply, so what does the Fed do? It tries to control demand.

Why? Because that is the only tool it has. Because Congress is so inept, it has tasked the Fed with preventing and curing inflation. But the Fed can’t do it.

Who can control inflation? Congress and the president can control inflation by controlling shortages.

Oil shortage: Financial rewards to oil companies to find more, pump more, hire more, and lower prices

Food shortage: Financial rewards to farmers, wholesalers, and retailers to reduce risk, reward growth and lower prices

Labor shortage: Eliminate FICA plus Medicare for All to make employment less expensive and to encourage higher net salaries.

Federal rewards to all other industries involved with scarce goods and services.

Do you notice a commonality among the solutions? They all require more deficit spending, not less.

If rising prices are to be fully tamed, it increasingly looks like Congress will have to get the deficit under control first.

Rather than attacking the cause of inflation, scarcity, Boehm attacks the cure for inflation, federal deficit spending to cure shortages.

Prices are up 3.7 percent over the past year, according to new inflation data released by the Bureau of Labor Statistics on Thursday morning. But so-called “core inflation,” which filters out the more volatile categories like food and fuel prices, rang in at 4.1 percent in the newest report.

Oil and food are the “core inflation” goods. Their shortages and resultant price increases cause most inflations, worldwide.

Typical for the pseudo-science of economics, economists filter out the two most common causes of inflation — oil and food scarcity — when measuring inflation.

It’s like a sports team filtering out points scored and allowed when analyzing the team’s won/lost record. Senseless.

To control inflation, the Federal Reserve raised interest rates at 11 consecutive meetings starting in March last year.

Every one of those interest rate increases raised the prices of goods and services. So, surprise! Inflation increased.

Since July, the central bank has left interest rates unchanged—the Fed’s current base rate is 5.5 percent, up from 3.25 percent a year ago.

Higher interest rates seem to have brought inflation down, but prices are rising nearly twice as fast as the Federal Reserve’s target of 2 percent annually.

No, oil, food, labor, metals, shipping, etc. scarcities moderated, so inflation moderated despite continuing interest rate increases.

We may have reached the limit of what the Federal Reserve can accomplish regarding taming inflation through monetary policy.

We reached that limit on the first day. Raising interest rates is inflationary. Period.

The federal government’s $33 trillion national debt and rising budget deficits are creating inflationary pressure in ways that remain underappreciated.

Economists ignore when the national “debt” and deficits rise without inflation (as often happens). But when we have inflation, the “debt” and deficit (which we have almost yearly) are blamed.

The big problem is that higher interest rates are helping curb inflation but worsening the federal government’s deficit.

No, the big problem is that while higher interest rates exacerbate inflation, the federal deficit can be directed toward inflation-curing programs, like Medicare for All and the elimination of FICA — both costs of doing business.

Writing at CNBC, Kelly Evans gets at the heart of this conundrum: “If we don’t quickly close the gap between spending and revenues, the debt load will keep growing, and interest costs will keep on rising, and the deficit will thus stay elevated, which grows the debt load even more.”

de Rugy

There is no debt load. It isn’t even debt. It’s deposits. They are not any sort of burden on the federal government or on the economy.

Those dollars are not owed by the federal government. The creditors all have been paid.

The deposits are owned by the depositors, who are paid off when deposits are returned to them.

So, what does that have to do with inflation?

As Reason contributor Veronique de Rugy, an economist at George Mason University, explains at National Review, there is an assumption built into monetary theory that says fiscal contraction—that is, smaller deficits—will necessarily follow a monetary contraction like the rising interest rates of the past year.

In other words, when central banks make it more expensive to borrow, they assume the politicians in charge of fiscal policy will respond by borrowing less.

But that hasn’t happened, and there is little indication that it will in the near future.

This assumption relies on federal politicians not understanding that spending by our Monetarily Sovereign federal government is not dollar-constrained. The government has the infinite ability to create and spend dollars on interest or anything else.

For that reason, the federal government does not borrow dollars. It does not need to obtain dollars from anyone.

The assumption also relies on the federal government spending less, which is recessionary. It is the false belief that recession is the cure for inflation when there is zero supporting evidence.

The federal budget deficit nearly doubled in the fiscal year that ended on September 30, and bigger deficits are expected in the next few years—in significant part because of the feedback loop between higher interest rates and rising debt costs.

That is not a “feedback loop” it is a tautology. The feedback loop is: Raise interest rates -> inflation –> raise interest rates again –> still higher inflation endlessly.

To fully get inflation under control, de Rugy says the country must experience a period of negative wealth effects—that is, a decline in demand driven by consumers choosing to rein in spending due to declining wealth.

Without her word salad, she says, “The country must experience a recession.” The Libertarians believe recessions cure inflation. Have they never heard of “stagflation”?

That’s hardly something worth cheering for, but it might be the only way to truly tame inflation—and it probably won’t happen until Congress curbs spending, too.

“The only way to get a reduction of total demand, which will ultimately rein in inflation, is for the fiscal authority to implement fiscal consolidation, hence creating a negative wealth effect,” writes de Rugy. “Absent that fiscal contraction, inflation will rise.”

Increased demand did not cause the sudden inflation of 2020. Demand didn’t suddenly appear overnight. But COVID made shortages occur overnight.

Changes to monetary policy have brought inflation down from last year’s near-record highs. Still, the monetary theory upon which that policy is built assumes that fiscal policy will finish the job by reducing deficits.

Congress, so far, doesn’t seem interested in cooperating—so expect prices to keep rising at an annoyingly fast rate.

You have just read the Libertarians’ false excuse for their cure not working. They claim the government’s massive spending (which has been in force for many years) suddenly decided to cause our inflation.

In short, because bleeding the patient with leeches didn’t cure his anemia, it must be that the patient is eating too much good food. Such is the nonsense that permeates economics today.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The Republicans who support rich, white, Christian, NRA men born in America, but claim too much money is given to everyone else.

The semi-Republicans (aka “Libertarians) who also claim the government spends too much helping the poor and middle-income people but support tax breaks for the rich.

The Dems who claim to love ordinary people but still yield to fairy tales about excessive federal deficits and debt.

There’s a fourth category: All those groups that claim to support a specific issue but, in reality, are designed to take votes from one of the major parties.

Veronique de Rugy

Here are some excerpts from an article that demonstrates the fairy tales they all promulgate. It was written by a semi-Republican (Libertarian).

‘Bidenomics’ Is Failing Everyday AmericansThe big spending has fueled higher inflation, resulted in larger-than-projected deficits, and contributed to a record level of debt.

By Veronique de Rugy, 9/21/2023

We’ve shown you data (here, here, here, here, and elsewhere) that demonstrate why even massive federal spending does not cause inflation.

All inflations are caused by shortages of critical goods and services. When anything is in short supply, its price rises.

When critical goods like oil and food are in short supply, prices generally increase. This general increase is called inflation.

These shortages can be cured by federal spending to obtain and disseminate the scarce goods and services.

The U.S. government spent massively for many years, and we experienced meager inflation. Only when COVID, the Russian/Ukraine war, immigration restrictions, and Saudi greed caused shortages of oil, food, computer chips, lumber, metals, labor, and other Gross Domestic Product necessities did we have the general increase in prices known as “inflation.”

GRAPH I.There is no historical relationship between highs and lows of federal spending (green) and inflation (red).GRAPH II.Also, there is no historical relationship between highs and lows of federal DEFICIT spending (blue) and inflation (red).GRAPH III.There is a strong correlation between the highs and lows of oil supplies (gray) and inflation (red).

Ordinary Americans aren’t feeling the so-called success of “Bidenomics.”

Superficially, the economy looks solid. Real gross domestic product (GDP) increased at an annual rate of 2.1 percent in the second quarter of 2023.

While August’s unemployment rate rose to 3.8 percent, that’s still considered full employment by economists.

Wages are rising, and we are often told we’re in a manufacturing boom.

But these numbers need perspective. Employment growth was inevitable because we lost millions of jobs during the pandemic.

De Rugy forgets she admitted we’re at full employment. This has nothing to do with employment growth. “Full” means “full.” She makes the strange claim that because we lost jobs during COVID, today’s full employment was a natural result.

Sorry, but that right-wing naysaying won’t fly. Federal spending helped create those jobs.

We have a labor shortage, partly because right-wingers falsely claim that undocumented immigrants bring crime and drugs to America.

Comparing Crime Rates Between Undocumented Immigrants, Legal Immigrants, and Native-born US Citizens in Texas

This study used uniquely comprehensive arrest data from the Texas Department of Public Safety to compare the criminality of undocumented immigrants to legal immigrants and native-born U.S. citizens between 2012 and 2018.

The study found that undocumented immigrants had substantially lower crime rates than native-born citizens and legal immigrants across a range of felony offenses. Relative to undocumented immigrants, U.S.-born citizens are over 2 times more likely to be arrested for violent crimes, 2.5 times more likely to be arrested for drug crimes, and over 4 times more likely to be arrested for property crimes.

Drugs come in via legal entry ports, not via immigrant families desperate to escape gangs and poverty.)

Cocaine seizures on U.S. borders, for instance, regularly measure in tons, making it impractical to have individual migrants ferry it across. Instead, dealers prefer to smuggle drugs into the country via legal ports of entry, which allow them to bring in high-value substances that are more easily hidden.

“The majority of the illegal drugs that enter the United States through the U.S.-Mexico border cross through formal Points of Entry,” said Joel Martinez, a Mexico research associate for the Center for American Progress

“The drugs that cross in between are very minimal and non-expensive products like marijuana. All the cocaine, fentanyl and methamphetamine — they cross through formal portsbecause they’re easier to hide […in] freight comp and assorted vehicles.”

So, right-wing bigotry against foreigners, especially those of color, make it almost impossible for those people to gain citizenship.

Unemployment is low, but only because the economy is drunk on spending, simultaneously closing many people out of the labor force.

De Rugy, desperate to minimize Biden’s success, unknowingly admits that federal spending reduces unemployment. Then, strangely, she declares that in some unknown way, federal spending “closes people out of the labor force.”

It is not unusual for people to take both sides of an issue when they have no facts.

Moreover, inflation-adjusted median household income has declined—from $76,330 in 2021 to $74,580 in 2022. Labor tensions and strikes are also intensifying.

This problem is not caused by federal spending but rather by the greed of the rich. Plenty of profits reward shareholders via stock price growth and stock by-backs.

Companies have plenty of money to reward executives with excessive pay increases, many multiples higher than average workers’.

Now, we see the inevitable result: Strikes.

With all this in mind, is the average American becoming better off?

No, the average worker is not making more inflation-measured dollars, which is why Biden (but not the Libertarians and the GOP) favors the strikers.

They are striking to narrow the income/wealth/power Gap between the rich and the rest. This is anathema to the Republicans and the faux Republicans (Libertarians), who always favor cutting benefits to the not-rich (while cutting taxes on the rich.)

These troubles are partly caused by inflation, which continues to take its toll. Per the Consumer Price Index (CPI), year-over-year inflation rose to 3.7 percent in August, nudging back up after peaking at 9.1 percent not long ago.

“Core” CPI (excluding food and energy) is down slightly to 4.3 percent. Although these numbers are an improvement after we experienced their highest levels since 1982, they remain disturbingly high.

Excluding food and energy from the measure of inflation and calling the balance “core inflation” makes no sense. It’s like excluding all home runs, triples, and doubles from a baseball player’s statistics and calling singles his “core” batting average.

Scarities of energy and/or food are the most common and most important reasons for inflation. The Fed is so focused on money it has lost sight of reality. The reason: The Fed is tasked with curing inflation, and its only tool is interest rates.

So, the Fed ignores the scarcity of energy and food and proclaims these products are not “core,” when that is precisely what they are. (“Move on, folks. Nothing to see here.”)

This is bad news for Americans whose standard of living has fallen since early 2021.

The Bureau of Labor Statistics (BLS) reported real average hourly earnings declining in 2021 and 2022, meaning Americans can afford less with their hard-earned dollars.

More than three-quarters of people’s income is devoted to living expenses like housing, transportation, and food—all of which have become more expensive.

The federal government can make all of the above less expensive to Americans. Consumers could receive federal benefits for housing, transportation, and food.

FICA could be eliminated; being a federal tax, it pays for nothing. (The federal government pays for everything by creating new dollars ad hoc. Federal tax dollars are destroyed upon receipt.)

The right-wing opposes all these solutions to the fallen standard of living.

Food prices, for instance, rose by 19.3 percent. Shelter rose by 16.5 percent since 2021. Gasoline prices are up, too.

Inflation is a tax on every American’s standard of living. It’s also a regressive tax. Low-income workers tend to experience higher-than-average levels of household inflation.

Inflation would not take its toll on Americans if the federal government increased spendingto:

Provide free healthcare insurance to every man, woman, and child in America, regardless of wealth and income.

Provide Social Security benefits to every man, woman, and child in America, regardless of wealth and income.

Reduce energy prices by supporting renewable energy and oil drilling/refining.

De Rugy cries crocodile tears for the “Average American’s troubles” but refuses to consider any cure for those troubles.

Instead, she worries about the non-existent “troubles” of the federal government, the one entity in America with limitless funds, and never needs to worry about bankruptcy.

Making matters worse, high-interest rates resultingfrom the Federal Reserve’s fight against inflation also hit lower-income Americans the hardest.

These tend to consume a higher proportion of such incomes and take money from the pockets of people who hold assets in cash or low-yielding bank deposits.

In other words, inflation creates the opposite of an equitable economy.

Both inflation and high-interest rates take money from the pockets of average Americans. But both inflation and high-interest rates are unnecessary and totally within the control of the government.

High rates do not “result” from anything. They are the Fed’s primary inflation-fighting tool. Inflation can be cured by federal spending to cure the shortages that cause inflation. And interest rates are determined by the Fed.

Raising interest rates not only does nothing to cure inflation but also exacerbates inflationby increasing the price of nearly everything: Real estate, cars and trucks, food, clothing, all imported goods, construction materials.

The Fed feeds the patient salt tables to cure high blood pressure. Why does the Fed do it? Because the Fed focuses on money, raising interest rates increases the demand for the dollar.

The Fed ignores the obvious fact that adding interest payments to the price of everything increases the purchase price of everything.

Simple example: You buy a $50,000 car and finance the purchase with a 5-year, 3% loan. The total of your 60 monthly payments is $53,852.13.

Alternatively, say you finance that $50,000 car with a 5-year 6% loan. Now, the total of your monthly payments is $57,776.95

That $50,000 car cost you an additional $3,924.82, courtesy of the Federal Reserve. That is the very definition of inflation.

By now, it’s well-known that Bidenomics’ big spending has fueled higher inflation, resulted in larger-than-projected deficits, and contributed to a record level of government debt.

It may be “well-known” that federal spending causes inflation, but what’s “well-known” often contradicts the facts.

It once was “well-known” that the earth was the center of the universe, emotional stress was the primary cause of stomach ulcers, and drinking water during exercise causes cramps (Yes, really. When I was young, that was common knowledge.)

As GRAPH I and GRAPH II (above) demonstrate, there is no relationship between federal spending and inflation. Nor is there a relationship between federal deficit spending and inflation.

There is, however, a robust relationship between oil price increases (which are strongly related to oil scarcity) and inflation.

As for de Rugy’s concern about federal debt and deficits, she displays widespread ignorance about Monetarily Sovereign governments.

The U.S. federal government’s finances are nothing like those of monetarily non-sovereign governments such as state, county, city, and the euro governments. Monetarily, Sovereign government cannot run short of their own sovereign currency.

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

“Federal debt” is not a debt of the federal government. It is deposited into T-security accounts that are owned not by the government but by the depositor. The government never touches those deposits other than to add interest money, and upon maturity, the money in those accounts is returned to the depository.

The two purposes of T-accounts (T-bills, T-notes, T-bonds) are to:

Provide the public with a safe storage place for unused dollars.

To assist the Fed in setting interest rates.

T-securities do not provide the federal government with spending money. To pay its bills, the federal government creates new dollars ad hoc.

Federal deficits are not a burden on the federal government or on taxpayers. The government has the infinite ability to pay any obligations. Unlike state and local governments, the federal government does not need or use tax dollars to pay its bills. It always uses newly created dollars for that purpose.

Ms. de Rugy’s concerns about federal “debt” and deficits are unwarranted. Federal deficits add dollars to the economy. When federal deficits are too small, the economy ceases to grow (“recessions”) or shrinks (“depressions).

Graph II shows this effect. As deficit spending shrinks, the economy goes into a recession, cured by increased deficit spending.

Deficit spending grows the economy and does not cause inflation or require taxes. Even if no federal taxes were collected, the federal government could continue spending forever.

The most recent estimate of the full-year deficit for 2023 is $1.5 trillion, up from $946 billion last year. Total federal debt is more than $33 trillion, an increase from $28.5 trillion in 2021. Budget tensions led the credit agency Fitch Ratings to downgrade Treasury debt based on prospects of further fiscal deterioration.

Fitch Ratings did not downgrade Treasury debt because of the size of the debt or deficits. It downgraded the debt because of the uncertainty regarding one of the most ignorance-based laws in American history: The debt ceiling.

This harmful law is based on the false premise that federal debt and deficits burden the government and taxpayers. The law threatens to force the federal government to renege on its promise to return the money in T-security accounts to depositors or to fail to pay past obligations to creditors.

This is not great; federal borrowing is projected to be $120 trillion in the next 30 years.

The federal government never borrows dollars. It creates all the dollars it needs and uses ad hoc.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

The prospect of gigantic, never-ending deficits during good times makes investors nervous.

Knowledgeable investors are aware that the size of federal deficits does not, in any way, affect the federal government’s ability to pay its bills.

Borrowing costs like mortgage and car loan rates are rising, as are yields on benchmark 10-year treasury notes. They’re above 4.3 percent, their highest level since 2007—weighty burdens on lower-income Americans.

Here, Ms. de Rugy mixes two errors.

Mortgage rates are whatever the Fed wishes them to be. Sadly, the Fed believes raising rates is the way to fight inflation, while it causes more inflation.

Finally, while America may be experiencing a hike in real construction spending, that’s a far cry from a manufacturing boom.

According to the Institute for Supply Management Report on Business, economic activity in the manufacturing sector in August contracted for the tenth consecutive month following 28 months of growth.

Moreover, manufacturing only accounts for 11 percent of GDP. Even if this sector grew, the benefits wouldn’t be widely shared.

After the COVID recession, GDP grew faster than at any time since WWII.

Manufacturing will continue to contract as we transition to a computer-based society. One day, we all will have 3-D printers that allow us to create what we want without buying manufactured goods.

Ms. de Rugy is stretching to find fault with economic growth. She is a member of the “semi-GOP” Libertarians whose sole contribution to the economic discussion is to criticize Democrats.

Nor will Bidenomics’ manufacturing subsidies help workers with college degrees. These handouts, often extensive and rich, benefit companies for projects they would have likely taken on anyway.

It’s not clear why Ms. de Rugy believes manufacturing subsidies won’t help workers with college degrees. And as for projects that “likely” would be taken on without benefits, one wonders where she came up with that bit of fakery.

Take the Inflation Reduction Act, for example. About half of all projects included in the Act were announced before it was passed.

Meaning that half were announced after it was passed. That’s an excellent result.

The private green market was booming even before the subsidies. The remainder of those subsidies overwhelmingly benefit affluent consumersof electric cars and other Biden-favored products.

Ms. de Rugy’s complaint seems ever more desperate. The private green market may or may not have been “booming,” but is that a reason not to invest in green?

She objects to government aid for anti-global warming electric vehicles because rich people own them (though average workers build them).

Taken together, these facts can help explain the president’s low approval ratings and the American people’s overall pessimism about the economy’s direction.

With so many working people feeling pinched, who can blame them?

The president’s low approval rates are not related to reality but more to the relentless naysaying from extreme right-wingers like Ms. de Rugy. When you keep pounding people with the message that things are awful, they tend to believe it.

JUST SOME OF BIDEN’S ACCOMPLISHMENTS DESPITE

THE EFFORTS OF THE GOP

1) $1.2 trillion infrastructure package

2) $1.9 trillion COVID relief deal

3) Highest appointment of federal judges since Reagan

4) Halt on federal executions

5) Rejoined the international Paris Climate Accord

6) Mandated converting the federal fleet to zero-emission vehicles.

7) Support for transgender service members.

8) Reduced unemployment.

9) Strengthened QUAD alliance with the U.S., India, Australia, and Japan.

10) Student loan debt relief

11) Used the Russia/Ukraine war to strengthen NATO,

which Trump tried to weaken.

12) Imposed crippling sanctions on Russia

13) Fought Saudi’s oil price increases by releasing 180 million barrels

of oil from the country’s Strategic Oil Reserves.

14) Pardoned people convicted of a federal marijuana charge

15) Respect for Marriage Act

16) Prevented the rail strike and gave workers a significant raise.

17) Passed Government Funding Bill

18) Got us out of Afghanistan, ending years of American deaths.

19) Expanded healthcare.

20) Defended Obamacare

21) Negotiated lifting the debt limit to prevent an economic disaster

22) Rejoined UNESCO

23) Lowest unemployment in years

24) Massive job creation

25) COVID-caused inflation dropping

Considering that unemployment is at historic lows and GDP is at historic highs, consumers’ biggest problem is the COVID-caused shortages causing in inflation.

Without the obstinacy of the right-wing, Biden could have passed even more consumer benefit programs to “unpinch” working people. And yes, that would have increased federal spending, a good thing. It would have grown GDP further.

Federal Spending + Nonfederal Spending + Net Exports = GDP

Sen. Dick Durbin

Unfortunately, Republicans and faux Republicans are not the only parties guilty of misstating federal finances.

Here are excerpts from a Senator Dick Dubin (D-IL) letter I recently received:

September 22, 2023,

Dear Mr. Mitchell,

Thank you for contacting me about the Fiscal Responsibility Act (P.L. 118-5). I appreciate hearing from you.

The debt limit is a statutory limit on the amount of debt the federal government may incur. When government expenditures outpace revenues, the Treasury may issue debt to cover the shortfall.

Those T-securities don’t cover anything. The government never touches the dollars that purchase T-bills, T-notes, and T-bonds.

Though Sen. Durbin has been in Congress for over 26 years, he still does not comprehend the difference between federal and personal finance.

Government spending and revenues vary by month, and even if the government has a surplus for the year, it may need to borrow money to cover a shortfall at some point during the year.

Why would an entity having the infinite ability to create dollars ever “need to borrow money?” It doesn’t.

On May 26, 2023, Treasury Secretary Janet Yellen projected that without action from Congress, the federal government would be unable to meet its obligations and subsequently default on June 5, 2023.

Default would have crashed the economy and impeded the government’s ability to make payments to Social Security and Medicare recipients, military personnel, veterans, federal employees, defense contractors, state governments, and our bondholders.

The federal government never needs to default. Only foolish actions by Congress and the President can force the government to default.

On May 27, 2023, President Biden and Speaker Kevin McCarthy reached an agreement. The Fiscal Responsibility Act avoids default by raising the debt limit through January 1, 2025.

Notice that Congress can raise the meaningless debt limit merely by deciding to do so.

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

This agreement was a good-faith compromise between President Biden and Speaker McCarthy, and it included some provisions that alter several important federal programs, which includes clawing back unspent pandemic relief funding and expanding work requirements for some beneficiaries of the Supplemental Nutrition Assistance Program (SNAP). On June 5, 2023, President Biden signed the Bipartisan Budget Agreement into law.

There is no reason for the U.S. government to “claw back” anything or to expand work requirements. The government has infinite money. There is no reason, but there is a purpose: To make the rich richer by widening the income/wealth/power Gap between the rich and the rich.

The wider the Gap, the richer and more powerful are the rich.

This agreement did not include everything I wanted. I am incredibly disappointed in any reallocation of funding to medical research or the National Institutes of Health. However, this agreement is what was required to avoid default.

And, of course, there was no economic reason for the reallocation.

I also have joined Representative Brendan Boyle of Pennsylvania to introduce the Debt Ceiling Reform Act (S. 1882), which would take the threat of default off of the table in the future. This bill would permanently end the weaponization of the debt ceiling by giving the Treasury Department the authority to continue paying the nation’s bills unless Congress submits a resolution of disapproval, which would need to be signed by the president.

The full faith and credit of the United States is not a bargaining chip, and it should not be used to enact any party’s extreme agenda. The Debt Ceiling Reform Act has been referred to the Senate Committee on Finance.

The whole thing is an exercise in stupidity. If, for some strange reason, Congress and the President wished to reduce spending (a reduction that mathematically would force a recession or depression), Congress and the President merely could stop spending. Period.

Now that we have avoided the default crisis, we must look to passing our twelve regular spending bills through regular order. I will be sure to keep your views in mind as we develop these spending priorities, and I will continue working to protect and enhance the federal programs on which American families rely.

If he wants to “protect and enhance federal programs, he should learn Monetary Sovereignty. After 26 years, it’s about time he learned at least this fundamental truth: The federal government cannot unintentionally run short of U.S. dollars.

It has infinite dollars.

Thank you again for contacting me. Please feel free to stay in touch.

That didn’t work for Stephanie Kelton; I wonder whether it would work for me.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The author of the following article, Veronique de Rugy, may need help understanding federal government finance, for she has written several articles in the same misleading vein.

The question: Is it ignorance or is it an agenda? Perhaps she needs to be more knowledgeable about federal finance. No problem. Most laypeople, and even many economists, suffer from that form of ignorance.

I suspect, however, that Ms. de Rugy is feigning ignorance and has an agenda, a pro-rich, pro-right, anti-poor agenda. You decide. Here are excerpts from her article:

Fitch Ratings just downgraded the U.S. government’s credit rating due in part to Congress’ erosion in governance.

Indeed, year after year, we see the same political theater unfold: last-minute deals, deficits, and, all too often, the passage of gigantic omnibus spending bills without proper scrutiny, repeated debt ceiling fights and threats of shutdown.

The blue line represents a standard measure of the economy, Gross Domestic Product (GDP). The red line represents what too often (and misleadingly) is termed “federal debt,” the “red ink” to which Ms. de Rugy refers.

We say “mistakenly termed debt” because it is unlike private debt. Federal “debt” is the total of deposits into privately owned, T-security accounts.

When you invest in a T-bill, T-note, or T-bond, you deposit your dollars into your T-security account at the U.S. Treasury.

This account is similar to your safe deposit box, where you deposit valuables. The bank does not touch the box’s contents, and they are not considered bank “debt,” though the bank owes you those contents in one minor sense.

Similarly, the federal government never touches the dollars held in your T-security account. Although some mistakenly refer to the dollars as borrowing, the federal government never borrows dollars.

Why would it? Given the federal government’s infinite power to create dollars at the touch of a computer key, borrowing dollars would be a ridiculous exercise:

Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency.”

Alan Greenspan: “There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody.”

Alan Greenspan: “The United States can pay any debt it has because we can always print the money to do that.”

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

Quote from former Fed Chairman Ben Bernanke when he was on 60 Minutes: Scott Pelley: Is that tax money that the Fed is spending? Ben Bernanke: It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

“Not dependent on credit markets” is Fed-speak meaning, “We don’t borrow.”

So what is the purpose of T-securities, the total of which erroneously is called “debt”? T-security accounts”

They allow holders of unused dollars to store them in a safe, interest-paying account, which stabilizes the dollar

They help the Fed control interest rates.

That’s it. The purpose is not to provide the federal government with spending dollars. The government creates all it needs. All federal spending is done with newly created dollars. No spending uses the dollars in T-security accounts.

For this reason, the size of the misnamed “debt” is irrelevant. Whether total deposits equal $100 or $100 TRILLION, the government has the same real ability to return them to depositors.

That is why the debt ceiling is so outrageously foolish. Why limit the amount of deposits that will be accepted if the dollars neither are used nor scarce to the government?

The confusion comes with the word “debt.” Federal “debt” differs from personal debt as an ink pen is a pig pen. Different meanings for the identically spelled and pronounced word “pen.”

If someone thought they could write with a pig pen, that would be equivalent to someone thinking the federal government was burdened by its federal debt.

Since 1940, there never has been a time when the government has not had Ms. de Rugy’s “red ink.” The lines essentially parallel, which should be no surprise to anyone because the formula for GDP is:

GDP = Federal Spending + Nonfederal Spending + Net Exports.

Federal Spending adds dollars to the economy, as do Net Exports, and those added dollars stimulate Nonfederal Spending. The three terms work in concert to create economic growth.

Sadly, “debt” confuses some economists, who wrongly equate it with private sector or state/local government debt.

But while the private sector and state/local governments are monetarily non-sovereign (i.e. they do not have the infinite ability to create U.S. dollars), the federal government is Monetarily Sovereign (it does have that limitless ability).

The difference is that the private sector and state/local governments unintentionally can run short of dollars, the federal government cannot unintentionally run short. That is a huge difference.

Imagine you had the federal government’s ability to create dollars at will. Why would you ever worry about debt? You wouldn’t.

A billion dollars in debt. No problem. A trillion? Still fine. A trillion trillion. Again, no problem.

So why is Ms. de Rugy worried about the “debt” if it’s no problem for the federal government? Does she understand that the federal government pays all its debts by creating dollars? Here is what she wrote:

Fitch Ratings just downgraded the U.S. government’s credit rating due in part to Congress’ erosion in governance.

Indeed, year after year, we see the same political theaterunfold: last-minute deals, deficits, and, all too often, the passage of gigantic omnibus spending bills without proper scrutiny, repeated debt ceiling fights and threats of shutdown.

In the above two paragraphs, Ms. de Rugy properly explains the reason for the rating downgrade: Political theater, debt ceiling fights and threats of shutdown.

It isn’t that the federal “debt” is too high. The reason for the downgrade is the political theater, the debt ceiling fights, and the shutdown threats. The federal government politically has become an unreliable payer.

It always can pay, but it might not choose to pay.

But, having expressed the truth, Ms. de Rugy goes off the rails.

But these are just symptoms of a budget-making process that desperately needs reform. In a world where politicians are rarely told no when it comes to creating or expanding programs, most simply refuse to have their hands tied or behave as responsible stewards of your dollars.

The lack of oversight and the general absence of a long-term vision is creating inefficiency, waste, and red ink as far as the eye can see. Without fundamental reform, no one can stop it. So, let’s have some real reform.

Inefficiency, waste, and red ink have nothing to do with the federal government’s ability to pay. I suspect Ms. de Rugy knows this because here comes what I believe to be her agenda.

We need a comprehensive budget process under which programs like Social Security, Medicare, and Medicaid can no longer grow without meaningful oversight.

Combined with other mandatory, more-or-less automatic spending items, they comprise over 70 percent of the budget.

Thus, they must be included in the regular budget process and subjected to periodic review.

Only then will our elected representatives be forced to stop ignoring the side of the budget that requires their attention the most.

Her solution to the federal credit rating cut is to cut Social Security, Medicare, and other spending items (like Medicaid and anti-poverty initiatives).

In this, she has become a shill for the Republican Party, which is a shill for the rich people of America.

The GOP has tried to eliminate the popular ACA (aka Obamacare) for many years, but it’s a program that helps the less affluent, a significant voting bloc.

This is the party that gave massive tax cuts to the rich, falsely complains about the Social Security and Medicare “trust funds”supposedly running short of dollars, and consistently votes against anything that would help the poor (whom they deem “lazy takers.”)

Federal “trust funds” differ from private trust funds as federal debt differs from personal debt.

A federal trust fund is an accounting mechanism the federal government uses to track earmarked receipts (money designated for a specific purpose or program) and corresponding expenditures.

The largest and best-known funds finance Social Security, Medicare, highways and mass transit, and pensions for government employees.

Federal trust funds bear little resemblance to their private-sector counterparts.

In private-sector trust funds, receipts are deposited and assets are held and invested by trustees on behalf of the stated beneficiaries.

In federal trust funds, the federal government does not set aside the receipts or invest them in private assets.

Again, the public and many economists are confused about the words “trust fund.” A federal trust fund is not a real trust fund and cannot run short of dollars unless Congress and the President want it to.

So all the bleating about the Social Security and Medicare trust funds running short of money is nonsense. Congress and the President could add $100 trillion to those trust funds or eliminate them completely at the touch of a computer key.

Medicare and Social Security could be funded directly like the military, Congress, SCOTUS, and the White House, none of which are burdened with fake trust funds.

This would also help deal with the fact that entitlement spending is, as every serious observer knows, unsustainable. Unless reformed, these programs will drain wealth from the government and the economy.

Ensuring their sustainability must be part of any serious budget process reform.

The above statements to too wrong to be accidental. They are outright lies. The government has proved it has the infinite ability to pay for things. It has been sustaining federal deficit spending since 1940, and the economy has continues to grow.

And federal spending, which adds dollars to the economy, certainly does not “drain wealth” from the economy, nor does it drain wealth from a government with infinite dollars.

Since 1940, people like Ms. de Rugy have complained that the federal “debt” is an unsustainable, ticking time bomb. Year after year, the same complaint and the lies are proven wrong year after year.

But the de Rugys of the world never stop.

Enter a “Base Closure and Realignment Commission (BRAC)”-style fiscal commission, an idea promoted by the Cato Institute’s Romina Boccia.

This commission would be “tasked with a clear and attainable objective, such as stabilizing the growth in the debt at no more than the GDP of the country, and empowered with fast-track authority, such that its recommendations become self-executing upon presidential approval, without Congress having to affirmatively vote on their enactment,” Boccia explains.

Go to the Cato Institute’s website and you’ll be greeted with more misinformation like the above.

Besides the fact that the economy has grown faster than the “debt” (see the graph above), what is the purpose of this objective?

The federal government cannot run short of dollars. And think of the reality: CATO and de Rugy want a group of unelected political bureaucrats to determine how much Social Security and Medicare should be cut.

It’s unimaginably ignorant.

And think of the result. By formula, cutting federal spending cuts GDP,so we would enter an endless spiral of spending cuts, GDP cuts, spending cuts, GDP cuts ad infinitum.

The euro nations, Greece, Italy, and France tried this. It’s called “austerity,” a process that dooms a nation to recessions, to borrow Ms. de Rugy’s phrase, as far as the eye can see.

Cutting federal spending cuts GDP, and cuts to GDP are, by definition, a recession. Why do the rich-loving Republicans want recessions?

Because recessions actually make the rich richer. Here is how that works.

“Rich” is a comparative.A person with $100 is rich if everyone else has $1, but that person is poor if everyone else has $1,000—the Gap between the richer and the poorer measures how wealthy a person is.

Recessions widen the Gap between the rich and the rest. During recessions, desperate people will accept menial, low-paying, demanding jobs, while wealthy business owners continue to profit by paying low salaries.

Here is what happens to an economy when the federal “debt” doesn’t increase substantially:

“Debt” doesn’t need to fall for us to have a recession; even when debt GROWTH falls, we have recessions (vertical gray bars).

Not just reduced debt but reduced deficits cause recessions. Imagine what would happen to the economy if de Rugy’s bureaucrats started making cuts. The idea is so screwball that even de Rugy is unsure about it:

I’m uneasy about delegating the president’s power to appoint “experts.” But, Congress would retain some veto power.

If they disapprove of the proposal, the House and Senate can reject it through a joint resolution within a specified period. Whether it’s the best solution to address our fiscal problems remains to be seen, but it’s worth considering.

No, Ms. de Rugy, it’s not “worth considering” any more than economic suicide is worth considering.

There are many more budget reform ideas out there. I’ll leave you with one more. For years, Congress has failed to pass a budget, bringing the country to the brink of a government shutdown by fighting over the need for a continuing resolution.

This temporary measure extends previous funding levels for a few months.

Making continuing appropriations automatic in case of a lapse could remove the threat of shutdowns.

As explained in one senator’s proposal, if appropriations work isn’t done, “implement an automatic continuing resolution (CR), on rolling 14-day periods, based on the most current spending levels enacted in the previous fiscal year.”

Further, to avoid over-relying on CRs, “all Members of Congress must stay in Washington, D.C., and work until the spending bills are completed.”

The problem is the nutty debt limit law.Just eliminate that law and Congress could not easily bring the economy to its knees.

It’s time to completely rethink how we approach the federal budget, grounding our efforts in transparency, accountability, and fiscal responsibility.

Yes, it is time to rethink how we approach the federal budget. First, learn Monetary Sovereignty. By learning how federal financing works, we could help our poor, retired, sick, homeless, and hungry.

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.

When supply cannot meet demand, prices go up. That’s basic.

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.

When supply cannot meet demand, prices go up. That’s basic.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.