If you are a regular reader of this blog you may be familiar with this post: Historical claims the Federal Debt is a “ticking time bomb.” It describes the ongoing, relentless claims that the federal debt is “unsustainable and a “ticking time bomb.

The first entry was in 1940, when the so-called “federal debt” was about $40 Billion. Today, it is about $30 Trillion, a monstrous 74,900% increase.

You read that right. The so-called “federal debt” has increased nearly seventy five thousand percent since Robert M. Hanes, president of the American Bankers Association, claimed, the federal budget was a “ticking time-bomb which can eventually destroy the American system,”

Now, here we are, 84 years and $30 Trillion dollars later. And still we survive. Not much of a time bomb.

I was reminded yet again, about the absurdity of the debt worries, when I read the following article, Here are some excerpts:

Record-high national debt is fiscal time bomb for US. Congress must defuse it. Founding Father’s fear has come true: Federal debt burden now is the greatest threat to the U.S. economy, national security and social stability. David M. Walker and Mark J. Higgins Opinion contributors

Apparently the “time bomb” still is ticking in the minds of the debt fear mongers.

In the late 1780s, the finances of the United States were in disarray. Revolutionary War debts incurred by the Continental Congress and former colonies were defaulting, and the democratic experiment in the New World was on the brink of failure.

But the nation caught a break when President George Washington appointed Alexander Hamilton as the first secretary of the Treasury.

In 1790 and 1791, Hamilton persuaded a reluctant Congress to establish the nation’s first central bank and consolidate all outstanding state and federal debt.

The federal debt burden after this action was just 30% of gross domestic product. A few years later, President Washington reinforced in his farewell address the need to avoid excessive debt.

We repeatedly have shown that the Debt/GDP ratio signifies nothing. It predicts nothing. It says nothing about a nation’s ability to pay its financial debts. It has no meaning whatsoever.

Yet it is quoted, again and again, by pundits who use it as evidence of . . . whatever they are trying to prove.

What next, Annual Rainfall/Number of Children named “Tom”? Here is the nonsense being peddled by Investopedia:

The debt-to-GDP ratio is the metric comparing a country’s public debt to its gross domestic product (GDP).

By comparing what a country owes with what it produces, the debt-to-GDP ratio reliably indicates that particular country’s ability to pay back its debts.

Often expressed as a percentage, this ratio can also be interpreted as the number of years needed to pay back debt if GDP is dedicated entirely to debt repayment.

Oh, really? The ratio “reliably indicates”?

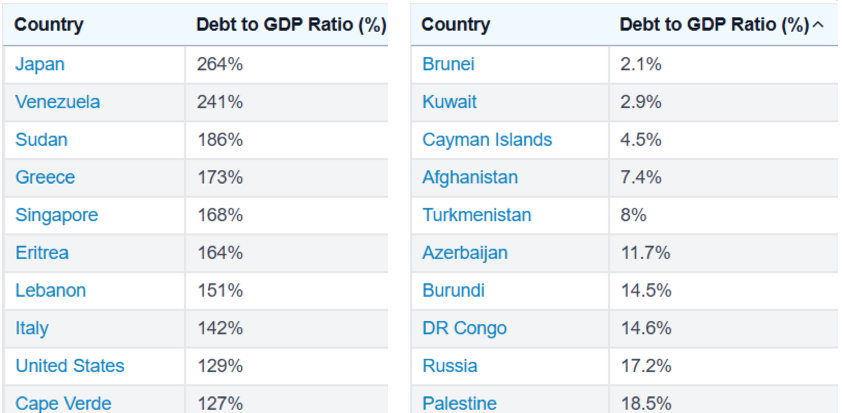

Here are some sample ratios. The nations with the ten highest ratios are shown to the left. The nations with the ten lowest ratios are shown to the right. According to the debt fear-mongers, the most financially secure nations are listed in the right-hand column:

According to the infamous Debt/GDP formula, the U.S. government has less ability to pay its debts than Cape Verde, and every one of the nations in the right-hand column.

And Japan supposedly has less ability to pay its debts than any other nation in the world. Does anyone really believe this nonsense?

But wait. Buried deep in the Investopedia article is this little paragraph:

Economists who adhere to modern monetary theory (MMT) argue that sovereign nations capable of printing their own money cannot ever go bankrupt, because they can simply produce more fiat currency to service debts; however, this rule does not apply to countries that do not control their monetary policies, such as European Union (EU) nations, who must rely on the European Central Bank (ECB) to issue euros.

Thus, the Debt/GDP “rule” does not apply to the United States, Canada, Mexico, China, Australia, the UK, Switzerland, Sweden, Norway, India, South Africa and others. The “rule” doesn’t apply to most of the world’s largest, most significant economies.

Yet, pundits in America insist on using the useless — no harmful — Debt/GDP ratio as a cudgel to ram debt reduction into financial planning.

Never mind that debt reduction causes depressions and recessions:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Why does that happen? Simple algebra. The formula for Gross Domestic Product is:

GDP = Federal Spending + Nonfederal Spending + Net Exports.

To reduce the so-called federal debt, one must decrease Federal Spending and/or increase federal taxes, which decreases Nonfederal Spending.

To increase real (inflation-adjusted) economic growth, a nation must do the opposite: Increase Federal Spending and/or decrease federal taxes, both of which add to the so-called “federal debt.”

Mathematically, there is no way to grow real GDP without growing “federal debt” enough to overcome inflation. So, if inflation is say, 2% (the Fed’s goal), the debt increase must overcome an annual 2% inflation handicap for GDP just to stay even.

Add to that, the need to overcome a net export figure (which America almost always has) and large annual deficits become vital.

When we have deficits that are too small, we have recessions, which the following graph demonstrates:

Strangely, the “science” of economics, which seems to love mathematical formulas and graphs, ignores the obvious. Growing an economy requires a growing supply of money.

Federal deficits add money to the economy. Federal taxes take money from the economy.

Continuing with the ticking time bomb article:

Over the next 175 years, politicians across the political spectrum largely adhered to Hamiltonian principles to preserve the integrity of the public credit.

The most important principle was that debt should be issued primarily to address emergencies – especially those involving foreign wars – and that debt burdens should be reduced during times of peace.

This changed completely in the 1970’s when President Nixon mandated the end of the dollar “backing” (actually the convertibility) to gold, and made the federal government Monetarily Sovereign in full.

Until then, the federal government’s ability to create dollars was limited by its inventory of gold. When the inventory did not keep up with GDP growth needs, recessions resulted.

Now, with gold no longer a factor, the government’s ability to grow the nation’s money supply also gave the government the ability to grow GDP.

This discipline enabled America to establish and maintain its excellent credit record, which provided ample lending capacity during periodic crises.

As Hamilton predicted, the ability of the nation to borrow proved critical during the War of 1812, the Civil War, World War I and World War II.

The nation now has no need to borrow, a far superior situation. It can create, at will, the growth dollars it needs.

After World War II, fiscal discipline was temporarily restored, and debt/GDP was reduced by growing the economy much faster than the debt even though the federal government continued to run budget deficits during most years.

Again, there is no magic. GDP still = Federal Spending + Nonfederal Spending + Net Exports.

If the Federal debt is reduced, the growth dollars must come from somewhere. In this case, growth came from Net Exports.

Subsequently, our wealthy economy began buying, buying, buying, which is a good thing. We were exchanging dollars that cost us nothing (We created them by pressing computer keys) for valuable goods and services.

Because the American government has access to infinite dollars, importing goods and services makes economic sense.

The one exception was in 1998-2001, when the federal government ran budget surpluses and even paid down debt in two of these years.

That exception proves the debt reduction is an economic disaster. Here is what happened when we paid down debt: 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Since then, the Hamiltonian principle has been decisively abandoned, and the federal government now routinely runs large deficits, resulting in ever-increasing debt burdens. This behavior is projected to worsen in the future.

Translation: The federal government now routinely runs large deficits, which pump growth dollars into the economy, thus growing GDP.

Mounting federal debt burdens now represent the greatest threat to the U.S. economy, national security and social stability.

The federal debt/GDP ratio is 123%. The nonpartisan Congressional Budget Office projects that, under current law, it will increase to 192% by 2053.

The federal government has the infinite ability to create dollars. The major threat to the U.S. economy (i.e. to GDP) is a reduction in federal money creation.

Clearly this is irresponsible, unsustainable and in sharp contrast to Hamilton’s founding principle.

There it is, the word “unsustainable,” to describe what we have been sustaining since 1940. Hamilton did not anticipate the post-1973, Monetarily Sovereign America.

National debt has topped $34 trillion.Does anyone actually have the guts to fix it?

The fastest way to “fix” the national debt would be to stop accepting deposits into T-security accounts (T-bills, T-notes, and T-bonds).

The government doesn’t use those dollars. They remain the property of the depositors. The problem is that those deposits do have two functions (neither of which is to supply the government with dollars):

- To provide a safer place to store dollars than bank savings accounts

- To help the Fed control interest rates by providing a floor for rates.

Why does the United States continue to behave so irresponsibly? One reason is that U.S. politicians routinely avoid spending cuts and tax increases because they may threaten their reelection prospects.

Voters rightfully don’t want tax increases and they don’t want federal benefit reductions, both of which take money out of voters’ pockets and lead to recessions.

Another is that, as the issuer of the world’s dominant reserve currency, the United States can run fiscal deficits so long as surplus countries, such as China and Saudi Arabia, continue to purchase U.S. Treasuries.

The U.S. does not need anyone to purchase U.S. Treasuries. The federal government creates all the dollars it needs simply by pressing computer keys. The government does not use the dollars in T-security accounts. They are the property of the depositors.

In fact, proponents of the flawed and failed Modern Monetary Theory implicitly argue that the dollar’s reserve currency status is permanent, which allows deficit spending to continue indefinitely.

The dollar is the world’s leading reserve currency, which is a currency banks keep on reserve to facilitate international commerce. But, other currencies — the British pound, the euro, the Chinese renminbi — also are reserve currencies.

Being a reserve currency has nothing to do with the federal government’s ability to spend indefinitely.

Congress must defuse America’s fiscal time bomb.

Yikes, there it is again, the silly “time bomb” analogy. It’s the time bomb that never explodes.

A debt crisis is not imminent in 2024, but one will occur in the future if the nation’s addiction to deficits and debt persists.

Translation: A debt crisis is not imminent in 2024. We have no idea when if ever it will occur, but it makes us sound smart to threaten it.

The greatest risk is the one that Alexander Hamilton feared most: One day, the United States could face a threat to its very existence – perhaps in the form of a foreign war – and Americans will lack the debt capacity to fund an adequate response.

Lack the capacity to fund? Utter nonsense. Here are the facts:

Former Fed Chairman, Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Fed Chairman, Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

That’s the real capacity.

Fortunately, the future is far from hopeless. America sits on a huge reservoir of natural resources and remains the world’s technological innovation engine.

It also possesses sufficient time to enact fiscal reforms and reestablish fiscal discipline.

Because the authors, David M. Walker and Mark J. Higgins, don’t understand Monetary Sovereignty, they think federal government fiscal discipline is the same a personal fiscal discipline.

Federal finance is so unlike personal finance that not understanding the difference is like not understanding the difference between butter and a butterfly.

The challenge for Americans today is that the longer we wait to reinstate this principle, the more pain that will be incurred. It is our belief that the solution is in the hands of “We the People.”

The math doesn’t lie.Republicans and Democrats own every missing dollar of our growing national debt crisis.

Politicians have powerful incentives to respond to short-term demands, and if Americans collectively demand that short-term desires must be satisfied at the expense of the nation’s long-term prosperity and solvency, that is what politicians will deliver.

Heaven forbid that Americans demand increases in taxes and cuts to federal spending. The result would be a depression.

On the other hand, if Americans place equal value on the longevity of their country and the prosperity of their children and grandchildren, they will demand that politicians take steps to defuse America’s fiscal “time bomb.”

Oops, more time bomb that never explodes.

Ever notice that the debt worriers never come up with evidence? They say “debt is bad,” but they don’t say,”Here is a graph of what has happened to the economy when federal debt increased and decreased.

Here is one such graph:

As you can see, there is no sign of a “debt crisis.”

History suggests that Americans will eventually pursue the correct course of action. Our hope is that they embrace it quickly to ensure that America’s future is brighter than its past.

David M. Walker, a former U.S. comptroller general, is also a recipient of the Alexander Hamilton Award for economic and fiscal policy leadership from the Center for the Study of the Presidency and the Congress.

Mark J. Higgins is author of “Investing in U.S. Financial History: Understanding the Past to Forecast the Future,” coming Feb. 27. Connect with Mark on LinkedIn.

It is frightening that a former U.S. comptroller general and recipient of an award for policy leadership, and the author of a book about U.S. finances can be so clueless about U.S. federal finances. No wonder the public is so ill-informed.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY