An alternative to popular faith

The 6/30/10 editorial in the Chicago Tribune, titled, “Enough debt, already,” had me confused. At first I thought they meant private debt. After all, consumers now deal with mortgages they can’t handle and credit cards charging 20% or more interest. And business profits, or lack thereof, won’t support much more debt without increased consumer buying. Consumers and businesses are going bankrupt in droves, so at this stage of the recession, “Enough debt, already” seems like good advice for the private sector.

But no, that is not what the Tribune meant. They wanted less federal debt and more private debt. The federal government has the unlimited ability to pay any debt of any size. It is a government that neither needs nor uses tax money to pay its debts. Yet the editors say, “. . . the U.S. has gone way, way down the path toward unsustainable debt . . .”

Will the government be unable to service its debts? No, that cannot happen. So, what makes federal debt “unsustainable”? The Tribune editors never say. However they call for more lending to business, despite the fact that growing business debt can be unsustainable. To make matters worse, the Tribune cheers the restriction on unemployment checks to those people who would have used those checks to buy things from businesses, thereby stimulating business. (“Unemployment checks extending up to 99 weeks instead of the usual 26 add more indebtedness.”)

The editors correctly say, “The U.S. economy is hungry for credit,” not realizing this means the U.S. economy is hungry for money, and federal deficit spending is the government’s method for adding money to the economy. The editors lament, “Washington already has bequeathed to our descendants a nation debt of $13 trillion,” – an untrue statement – and simultaneously wants to bequeath to our descendants added business debt. (Who do they think pays for business debt?)

To summarize: The Tribune editors oppose debt creation by the one entity that can afford unlimited debt service, but advocate more debt for the over-extended private sector. They support looser lending standards, so that less qualified businesses can go deeper into debt. They oppose increasing regulations on lenders, the same lenders whose unsupervised, profligate lending triggered the recession. They favor the end to federal stimulus plans, which would add the money they say the economy needs. And they hope the economy will recover — somehow.

Clearly, economics is not the Tribune editors’ forte.

Rodger Malcolm Mitchell

http://www.rodgermitchell.com

![]()

No nation can tax itself into prosperity

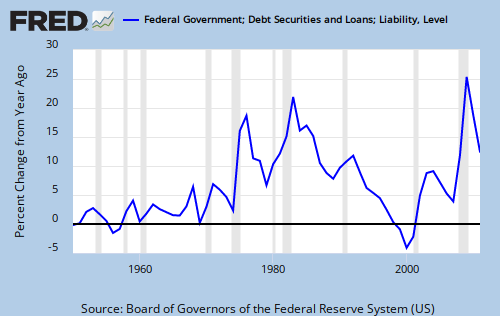

GRAPH

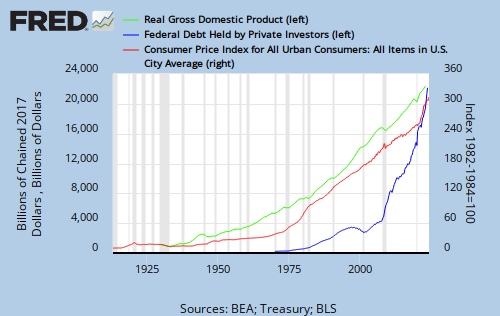

GRAPH