Here are three current articles that demonstrate the economic ignorance of the American public. We’ll begin with an article that reflects American’s beliefs about immigration:

According to a Pew Research Center survey conducted from January 16 to 21, 2024, 78% of Americans believe that the large number of migrants seeking entry into the United States at the U.S.-Mexico border is either a crisis (45%) or a major problem (32%).

Republicans are more likely to describe it as a “crisis” (70%) than Democrats (22%), who mostly view it as a “major problem” (44%) or a “minor problem” (26%).

Concerns raised by respondents include economic burdens associated with the migrant influx and issues related to how migrants are cared for and the overall immigration system.

Additionally, in a nationwide poll conducted in late March, 83% of respondents expressed support for a complete cessation of immigration across the U.S.-Mexico border.

Furthermore, a Rasmussen Reports survey found that even among Hispanics, 55.8% supported closing the border.

A majority of Americans believe immigrants are an economic burden on America. Compare that with these facts:

Immigrants boost job growth

The labor shortage has employers pinning hopes on arrivals, By Paul Wiseman, Gisela Salomon, and Christopher Rugaber Associated Press.The millions of jobs that new immigrant arrivals have been filling in the United States appear to solve a riddle that has confounded economists for at least a year: How has the economy managed to prosper, adding hundreds of thousands of jobs, month after month, at a time when the Federal Reserve has aggressively raised interest rates to fight inflation — usually a recipe for a recession?

The answer appears to be immigrants. The influx of foreign-born adults vastly raised the supply of available workers after a U.S. labor shortage had left many companies unable to fill jobs.

More workers filling more jobs and spending more money has helped drive economic growth and create still more job openings.

Immigrants have

- Helped solve a severe labor shortage

- Reduced inflation

- Driven economic growth

- Prevented a recession

- Created more job availabilities.

“There’s been something of a mystery — how are we continuing to get such extraordinary strong job growth with inflation still continuing to come down?” said Heidi Shierholz, president of the Economic Policy Institute. “The immigration numbers being higher than what we had thought — that really does pretty much solve that puzzle.”

While helping fuel economic growth, immigrants also lie at the heart of an incendiary election-year debate over the control of the nation’s southern border.

In his bid to return to the White House, Donald Trump has vowed to finish building a border wall and to launch the “largest domestic deportation operation in American history.”

Millions of Americans think that is a great idea.

Whether he or President Joe Biden wins the election could determine whether the influx of immigrants, and their crucial role in propelling the economy, will endure.

The immigration boom was a surprise.

In 2019, the Congressional Budget Office estimated that net immigration—arrivals minus departures—would equal about 1 million in 2023.

The actual number, the CBO said in a January update, was 3.3 million.

That’s 3.3 million workers and consumers helping to build our nation.

Thousands of employers desperately needed the new arrivals. The number of native-born Americans in their prime working years — ages 25 to 54 — was dropping because so many of them had aged out of that category and were nearing or entering retirement.

Their numbers had shrunk by 770,000 since February 2020, just before COVID-19 slammed the economy.

Filling the gap has been a wave of immigrants. Over the past four years, the number of prime-age workers who either have a job or are looking for one has surged by 2.8 million.

And nearly all those newcomers — 2.7 million, or 96% of them — were born outside the United States.

As older people leave the work force, young immigrants enter, the ideal situation for our economy, given our reduced birth rate.

(The nationwide birth rate fell significantly between 2007 and 2022, dropping from 14.3 births per 1,000 people to 11.1, or nearly 23%, per new CDC data.)

Where else will we find new, young workers to fill the voids left by older retiring for dying workers, if not from immigrants? But Trump wants to force “the largest domestic deportation operation in American history.”

It makes no sense.

A study by Wendy Edelberg and Tara Watson of the Brookings Institution found that new immigrants raised the economy’s supply of workers and allowed the United States to generate jobs without overheating and accelerating inflation.

Trump has repeatedly attacked Biden’s immigration policy over the surge in migrants at the southern border.

Only 27% of the 3.3 million foreigners who entered the United States last year did so as “lawful permanent residents” or on temporary visas, according to Edelberg and Watson’s analysis.

Many economists suggest that immigrants benefit the U.S. economy. They take low-paying but essential jobs that most U.S.-born Americans won’t, like caring for the sick and the elderly.

And they can make the country more innovative because they are more likely to start businesses and obtain patents.

Ernie Tedeschi, a visiting fellow at Georgetown University’s Psaros Center and a former Biden economic adviser, calculates that the burst of immigration has accounted for about a fifth of the economy’s growth over the past four years.

Think of the Hitleresque realities. To fulfill his “largest domestic deportation operation in American history.” promise, Trump would need to:

- Hire, pay, and occupy the time of tens of thousands of police and/or National Guard

- Have them search house to house, millions of dwellings, from attic to basement

- Kick down doors if necessary

- Drag from their homes screaming men, women and children

- Put them on trains (cattle cars?) and ship them to the border

- Disregard the fact that many immigrants will have spent years in America building lives and contributing to our nation

- Split families, some of which will have had children born here and by law, are citizens.

- Turn millions of Americans into Gestapo-like spies, encouraged to rat out their neighbors, which will rip apart American society, changing our nation in ways we would regret, forever.

And why do this to America? Because one man, Donald Trump, has appealed to the ignorant, bigoted and haters in his base, convincing them that immigrants are not people, and that logic and compassion are not American virtues.

America needs to spend on better systems for vetting and assimilating immigrants, not on spending for higher walls and forced deportations.

=================================================

Immigration is not the only “problem” about which we have been lied by the politicians and some of the media. Consider inflation:

Elevated inflation will likely hinder rate cuts this year, Powell says

WASHINGTON — Federal Reserve Chair Jerome Powell on Tuesday cautioned that persistently elevated inflation will likely delay any Fed interest rate cuts until later this year, opening the door to a period of higher-for-longer rates.“Recent data have clearly not given us greater confidence” that inflation is coming fully under control and “instead indicate that it’s likely to take longer than expected to achieve that confidence,” Powell said during a panel discussion at the Wilson Center.

“If higher inflation does persist, we can maintain the current level of (interest rates) for as long as needed.”

The Fed chair’s comments suggested that without further evidence that inflation is falling, the central bank may carry out fewer than the three quarter-point reductions its officials had forecast during their most recent meeting in March.

We’ve discussed this previously, here and here and elsewhere, so I’ll just summarize for you:

Inflation is a general increase in prices.

Higher interest rates increase the prices of everything, because interest costs are added to nearly everything you buy.

Therefore, the Fed wants to fight inflation by raising the prices of everything!

In short, the Fed is applying leeches to fight anemia.

Prices go up when things are in short supply. Supply problems arise not because interest rates are too low but because of other economic factors.

America’s most recent inflation was caused by COVID-related shortages of oil, food, steel, paper, computer chips, lumber, shipping, labor and other goods and services.

The cure for inflation is not to raise prices further by raising interest rates, but instead increase government spending to acquire and distribute the scarce goods and services — exactly the opposite of the “cut-spending, raise-interest-rate” proclivity of the Fed.

In the past several weeks, government data has shown that inflation remains stubbornly above the Fed’s 2% target and that the economy is still growing robustly.

Year-over-year inflation rose to 3.5% in March, from 3.2% in February.

And a closely watched gauge of “core” prices, which exclude volatile food and energy, rose sharply for a third consecutive month.

The irony is that good economic news is bad news for the Fed, which raises interest prices in response to increased prices.

In summary, inflation is caused by shortages of critical goods and services, not by low interest rates or federal spending.

Despite the Fed’s “best” (actually worst) efforts, inflation has fallen because the federal government has subsidized industry to create more of the scarce products.

===================================

The third article demonstrating the ignorance-forcing, false statements by the politicians and the media has to do with student loans.

The original American colonies, recognizing the vital need for education, set up schooling, initially teaching the reading of the bible.

Boston Latin became the first American public high school in 1820, and in 1827, the state of Massachusetts opened all public schools free to all students.

And we have hardly progressed from there.

Today’s more literate world competition demands more than a high school education, with college and beyond being ever more needed for economic and scientific growth.

America should be doing everything in its power to provide free education to young minds. Yet we remain stuck in the 1800’s, with state and local taxpayers funding K-12, plus some lower-level community colleges.

Rich kids go to the best schools; poor kids go to work. The implicit assumption is that poor kids aren’t smart enough to warrant the best education. That thinking creates a terrible waste of brainpower.

The federal government should take the education burden off taxpayers by funding all levels of education, including university and beyond. Being Monetarily Sovereign, the government does not spend taxpayer dollars. Its spending costs taxpayers nothing.

Yet, rather than providing free education, America puts its best students into debt by lending, rather than giving, them education dollars. Senseless.

And when someone tries to help students come out of debt, they meet objections based on ignorance.

Student loan plan: President Joe Biden’s latest plan for student loan cancellation is moving forward as a proposed regulation, offering him a fresh chance to deliver on a campaign promise and energize young voters ahead of the November election.

The Education Department on Tuesday filed paperwork for a new regulation that would deliver the cancellation that Biden announced last week.

It still has to go through a 30-day public comment period and another review before it can be finalized.

It’s a more targeted proposal than the one the U.S. Supreme Court struck down last year. The new plan uses a different legal basis and seeks to cancel or reduce loans for more than 25 million Americans.

Conservative opponents, who see it as an unfair burden for taxpayers who didn’t attend college, have threatened to challenge it in court.

In this regard, we meet ignorance in its various disguises:

1. The false belief that taxpayers fund federal spending. While taxpayers do fund state and local government spending (those governments are monetarily non-sovereign) taxpayers do not fund Monetarily Sovereign federal spending.

The federal government creates new dollars, ad hoc, to pay for all its spending. Even if the federal government collected $0 taxes, it could continue spending forever.

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

The purposes of federal taxes are not to provide spending money to the government, but:

A. To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward

B. To assure demand for the U.S. dollar, by requiring taxes be paid with dollars.

Taxpayers would not pay for federal funding of education just as taxpayers don’t fund tax breaks for mortgage interest, long-term capital gains, or any other tax benefits to the rich.

2. The false belief the federal government can’t afford more deficit spending. The federal government has the infinite ability to create its own sovereign currency, the U.S. dollar. It never can run short of dollars and can pay any bill of any size, without taxing or borrowing.

Those who complain about the size of the federal “debt” (that really isn’t federal or debt), demonstrate ignorance about federal financing.

3. The “If-I-didn’t-get-it,-he-shouldn’t-get-it” envy. This idea precludes any new government benefits, because benefits have to begin somewhere, and there always will be people who didn’t receive a benefit before it began.

4. The rich, who run America, don’t want the income/wealth/power Gap to narrow. Without the Gap, no one would be rich, and when the Gap, widens, the rich grow richer.

Giving free education to the average American would narrow the Gap and make the rich less rich. So, they spread the misinformation that while it’s OK for state/local government taxpayers to fund K-12, it’s not OK for the federal government to fund K-16+, with no help from taxpayers.

It makes no sense, but that is what you’re being taught.

Why do we treat grades K-12 differently from grades 13+?

Grades K-12 are free to students who don’t opt for private schools, paid for by taxpayers, and are mandatory to certain ages.

Grades 13+ are costly to students or funded by taxpayers and are optional. Entrance is based on merit (as judged by the school) and on affordability.

Why the cutoff at grade 13? Why don’t we treat all education levels the same? And if education is important for America’s international competitiveness, wellbeing and economic strength, why doesn’t the federal government fund it?

Why does America force our students into debt poverty, when America needs them?

IN SUMMARY

Ignorance is expensive.

Ignorance about immigration costs America valuable workers and their beneficial output, while converting the search for the American dream to a nightmare of immoral selfishness and cruelty.

Ignorance about inflation dooms us to ideas that perpetuate inflation while costing us the products whose scarcity causes the inflation.

Ignorance about federal Monetary Sovereignty and schooling costs America the brainpower benefits millions of middle-to-lower income young people could provide.

Only two things keep people in chains: The ignorance of the oppressed and the treachery of their leaders.

Rodger Malcolm Mitchell

Monetary Sovereignty

Twitter: @rodgermitchell Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

MONETARY SOVEREIGNTY

The U.S. federal government is

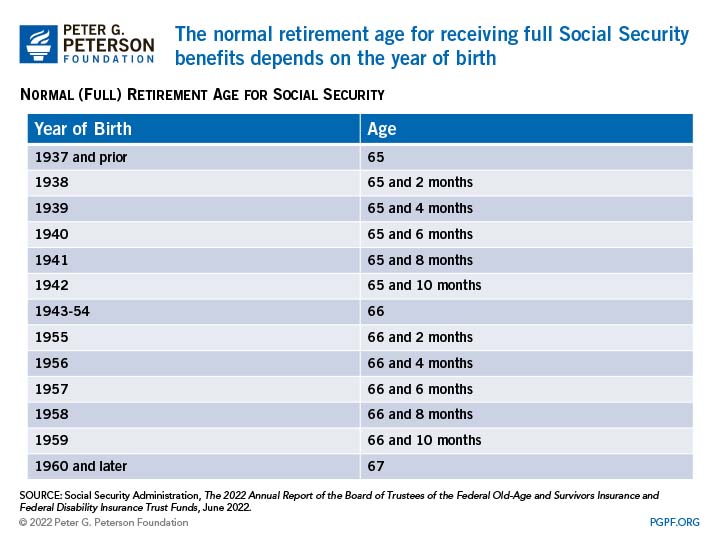

The U.S. federal government is The government also has the infinite power to change Social Security laws, as demonstrated by the 12 benefit changes shown in this chart.

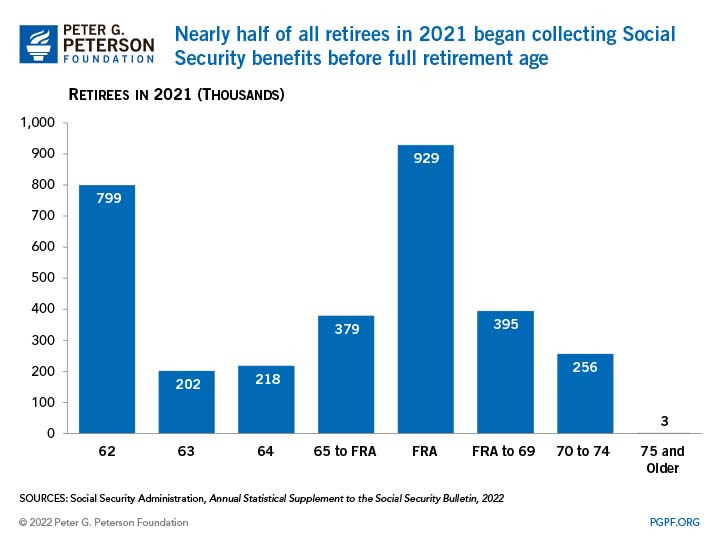

More than half of all Social Security recipients take benefits before the official retirement age when benefits are reduced.

This demonstrates an early need for benefits by those in lower-income groups.

The government also has the infinite power to change Social Security laws, as demonstrated by the 12 benefit changes shown in this chart.

More than half of all Social Security recipients take benefits before the official retirement age when benefits are reduced.

This demonstrates an early need for benefits by those in lower-income groups.