LUTNICK, magically GDP changes to the numbers we want. We simply change the definition

When a Trump appointee realizes the facts contradict his boss, he either misrepresents the facts or hides them.

The facts are the facts. They never change, but for a Trumper, it’s the perception, not any fact, that matters.

Thus, when Trump claims Ukraine invaded Russia, the lie doesn’t change the facts. But Trump and his MAGAs care only about public perception.

The economy is measured by a statistic known as Gross Domestic Product (GDP), calculated using the formula: Federal Spending + Non-federal Spending + Net Exports.

In the U.S., the National Bureau of Economic Research (NBER)—a nonprofit, nonpartisan organization dedicated to economic research—determines when we are in a recession by examining indicators of prolonged economic decline across various sectors.

It analyzes data points including real income, which reflects individuals’ purchasing power after adjusting for inflation; employment levels; industrial production output; wholesale and retail sales; and gross domestic product (GDP).

Mathematically, imposing high tariffs on imports, while deporting millions of workers and consumers, must raise prices and decrease GDP. Neither of these is a hypothesis or a prediction. It is a statistical certainty.

When GDP declines over several months, it is referred to as a “recession.” Conversely, when GDP decreases significantly and/or extensively, it is known as a “depression.”

Trump’s advisors must have realized that Trump’s plan to levy import duties and cut federal spending must result in inflation and recession or depression.

Rather than trying to correct Trump’s flawed policies, and actually prevent the depression, MAGAs prefer to change the measure.

Imagine selling a 2,000-square-foot house and wanting to tell the buyer it’s bigger than 2,000 square feet. Instead of physically enlarging the house, you simply change the measurement and decide that from now on, a foot will be eight inches long.

So your 2,000 foot house suddenly would be listed as 4,500 square feet. The house didn’t change, but by arbitrarily changing the measure, you could claim it was bigger.

Sounds ridiculous, even fraudulent, doesn’t it? But that is exactly what the Trump administration wants to do with GDP, in a futile effort to hide the inevitable recession and depression.

“A more accurate measure of GDP would exclude government spending,” Musk wrote on his social media platform. “Otherwise, you can scale GDP artificially high by spending money on things that don’t make people’s lives better.”

Is Musk asserting that federal spending on bridges, roads, dams, flight control, disaster recovery, anti-poverty efforts, medical research and development, Social Security, Medicare, Medicaid, and countless other initiatives the government undertakes to enhance our lives “doesn’t create value for the economy”?

That’s such nonsense.

Due to Musk’s budget cuts, GDP will decline. This presents a significant issue that Musk is well aware of. He is scared silly that when people see the decrease in GDP, they will accurately conclude that he is responsible for causing a recession.

The argument as articulated so far by Trump administration officials appears to play down the economic benefits created by Social Security payments, infrastructure spending, scientific research and other forms of government spending that can shape an economy’s trajectory.

“If the government buys a tank, that’s GDP,” Lutnick said Sunday. “But paying 1,000 people to think about buying a tank is not GDP. That is wasted — inefficiency, wasted money. And cutting that, while it shows in GDP, we’re going to get rid of that.”

Is Lutnick paid to come up with such a nonsense objection? His salary could be considered a waste of money. Thinking about war strategy is as important as building tanks.

The Commerce Department’s Bureau of Economic Analysis published its most recent GDP report on Thursday, showing that the economy grew at an annual rate of 2.3% in the final three months of last year.

The economy will drop like a stone under Trump, no matter how hard he tries to fake the numbers. While he remains in office, we will fall deeper and deeper into a depression.

The report makes it possible to measure the forces driving the economy, showing that the gains at the end of last year were largely driven by greater consumer spending and an upward revision to federal government spending related to defense.

Still, the federal government’s component of the GDP report for all of 2024 increased at 2.6%, slightly lower than overall economic growth last year of 2.8%.

Thus, even eliminating Federal Spending from the GDP equation won’t save Trump. His economy is doomed and everyone will know it. Fudging the figures won’t save him.

Lutnick’s false claim that federal spending doesn’t “make people’s lives better” is evident. Cutting federal spending will reduce personal income.

The government is not always a contributor to GDP and can subtract from it, which is what happened in 2022 as pandemic-related aid expired.

Lutnick said that the Trump administration would balance the federal budget with spending cuts, saying that would help growth and reduce the interest rates paid by consumers.

Historically, balancing the federal budget has led to depressions.

“When we balance the budget of the United States of America, interest rates are going to come smashing down,” Lutnick said. “This is going to be the best economy anybody’s ever seen. And to bet against it is foolish.”

Under Biden, the economy grew massively. Under Depression Don Trump it will sink. My advice: Do what I have done. While Depression Don remains in office, convert a significant part of your asset portfolio to Treasuries.

Mitchell’s laws: The more budgets are cut and taxes inceased, the weaker an economy becomes. Austerity = poverty and leads to civil disorder. Those, who do not understand the differences between Monetary Sovereignty and monetary non-sovereignty, do not understand economics.

This is an update of a post that ran in 2009.

Kermit the frog famously said, “It isn’t easy being green.” It also isn’t easy convincing people that traditional economics not only is hypothetically wrong, not only is factually wrong, but is wrong to such a degree it is extremely harmful to our economy.

The more extreme debt hawks believe the U.S. federal government should run a balanced budget or even have no debt at all. The more moderate debt hawks feel some debt may be necessary at times, but to them, federal debt is like bitter medicine you take only when absolutely necessary.

All debt hawks, whether extreme or moderate, are long on twisted “facts” but short on evidence.

Their “facts” inevitably include federal deficit and debt measures, projections for the future, debt/GDP ratios, and spending on Medicare and Social Security.

However, when they interpret the facts, they provide no evidence that their interpretations reflect reality.

By contrast, here are facts and a few opinions, which you may interpret for yourself.

1. Fact: Money is the way modern economies are measured. By definition, a large economy has a larger money supply than does a small economy. Therefore, a growing economy requires a growing supply of money. QED

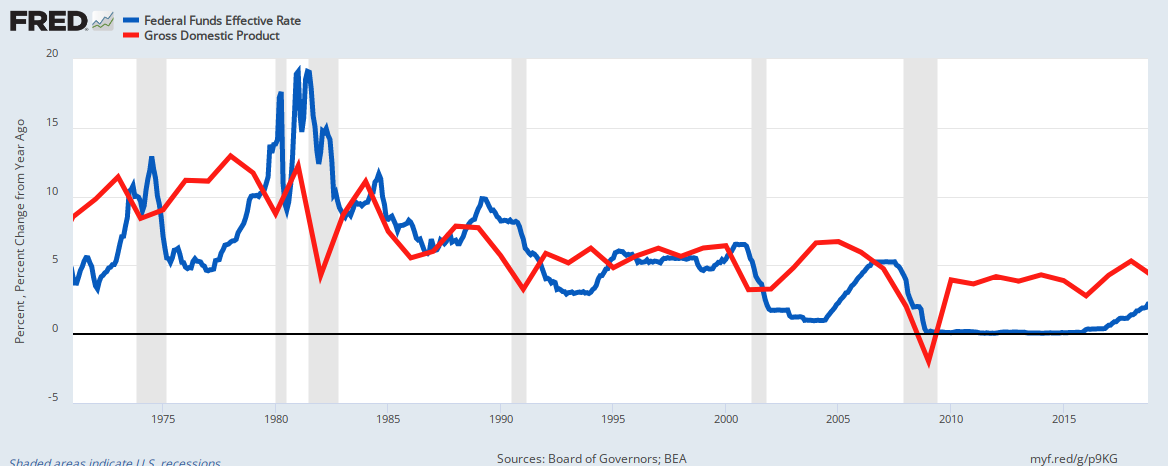

The graph below shows the essentially parallel paths of GDP vs. perhaps the most comprehensive measure of the money supply, Domestic Non-Financial Debt:

One could argue that money begets production or that production begets money, and both would be correct. The point is that money supply (i.e. debt) and GDP go hand-in-hand. Reduced debt growth results in reduced economic growth.

Gross Domestic Product = Federal Spending + NonFederal Spending + Net Exports.

Thus, by formula, a cut in federal spending cuts GDP.

2. Fact: All money is debt and all financial debt is money. In addition to being state-sponsored, legal tender, there are four criteria for modern money:

–Monetarily Sovereign money must be defined in a standard unit of currency.

–MS money has no, or limited, intrinsic value.

–The demand for money is determined by its risk (danger of default or devaluation, i.e., inflation) and its reward (interest rates).

–To have value, money must be owned by an entity other than the entity that created it.

The above criteria describe many forms of money, including currency, bank accounts, T-securities, corporate bonds, and money markets. All forms of money are debt, and a growing economy requires a growing supply of debt/money.

2.a. Fact: Federal “deficit” is a statement of the net amount of money the federal government has created in one year. Opinion: The word “deficit” is pejorative. A more neutral description would be money “created” or “added,” as in, “The government has created $1 trillion,” or “The government has added $1 trillion to the economy.”

Compare the psychological meaning of those statements with the current phrasing, “The government has run a $1 trillion deficit.”

3. Fact: U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

4. Fact: Recessions tend to follow reductions in federal debt/money growth (See graph below), while debt/money growth has increased when recessions are resolving.

Taxes reduce debt/money growth. No government can tax itself into prosperity, but many governments tax themselves into recession.

Recessions repeatedly come on the heels of deficit growth reductions, and are cured with deficit growth increases.

5. Fact: On August 15, 1971, the federal government gave itself the unlimited ability to create debt/money by completely abandoning the gold standard. This ability is called Monetary Sovereignty.

Because the federal government now has the unlimited ability to create dollars, it neither taxes or borrows in order to obtain dollars. It simply creates them ad hoc. Tax dollars are destroyed upon receipt.

When you pay your taxes, you take dollars from your checking account. These dollars were part of the M2 money supply measure.

When they reach the Treasury, they cease to be part of any money supply measure. They effectively are destroyed. To pay its bills, the federal government creates new dollars, ad hoc.

6. Fact: Federal “debt” is the total of outstanding Treasury Securities. Here is how Treasury Securities, incorrectly termed “borrowing” come into existence.

–You tell the government to debit your checking account and credit your Treasury security account by the same amount. The process is similar to transferring money from your checking account to your bank savings account.

To “pay off” the Treasury Security, the government simply debits your T-security account and credits your checking account.

Thus, the government could pay off all its so-called “debt” tomorrow simply by debiting all T-security accounts and crediting the T-Security owners’ checking accounts.

The entire process neither adds nor subtracts money from the economy (but for interest paid).

Our Monetarily Sovereign government does not borrow the money it has already created but rather exchanges one form of U.S. money (T-securities) for another (dollars). The entire “borrowing” process is nothing more than an asset exchange.

Do T-securities have any benefit? Yes, federal interest payments add to the money supply, an economically stimulative event. Federal interest payments help the government control interest rates and the dollar’s value. (The higher the interest, the greater the value of the dollar, and the more the economy receives in growth dollars.)

The most important purpose of T-securities is to provide a safe place to store unused dollars. This stabilizes the dollar while increasing its value.

T-securities (debt) are not functionally related to the difference between taxes and spending (deficits). They are related only by laws requiring the Treasury to create T-securities in the amount of the deficit.

The Treasury can create T-securities (debt) without a deficit, and the government can run a deficit without creating T-securities. Federal debt is not functionally the total of federal deficits.

The federal government could pay off the entire so-called “debt” today, merely by returning the dollars to the T-security depositors.

7. Fact: Federal taxes, as a money-raising tool, are unnecessary, harmful and futile:

— unnecessary because since 1971 (when the U.S. government became fully Monetarily Sovereign), the government has had the unlimited ability to create money without taxes,

— harmful because taxes reduce the money supply, which reduction leads to recessions and depressions, and

–futile because tax money sent to the government is destroyed upon receipt by the U.S. Treasury.

When you send taxes to the government, you are sending M2 dollars, but when they reach the Treasury, they cease to be part of any money supply measure. They effectively are destroyed.

Our Monetarily Sovereign government does not store dollars for future use. It can create unlimited dollars ad hoc by paying bills.

The so-called “debt” merely accounts for the total outstanding T-securities created out of thin air by the federal government.

The government decides to create T-securities equal to the deficit, but this requirement became obsolete in 1971 when we went off the gold standard and became Monetarily Sovereign.

Today, the federal government creates money by spending, i.e. it credits checking accounts to pay its bills. This crediting of checking accounts adds dollars to the economy.

The federal “deficit” is the net money created in one year and the federal “surplus” is the net money destroyed in one year. In short, deficit spending creates money and taxing destroys money. If taxes fell to $0 or rose to $100 trillion, this would not affect by even one dollar, the federal government’s ability to spend.

Further, (opinion)all tax (money-destroying) systems are unfair. See: http://rodgermitchell.com/FairTaxes.html. For a country with the unlimited power to create money, spending is not related in any way to taxing.

8. Fact: Contrary to popular myth, there is no post-gold standard relationship between federal debt and inflation. (See graph, below)

Also, contrary to popular myth, inflation is not caused by “excessive federal spending.” Inflation is caused by shortages of crucial goods and services, most often oil and/or food. (See the graph, below)

In this regard, hyperinflations are not caused by “money-printing,” but rather by shortages. So-called “money printing” (ala Zimabwe and Germany), were the governments’ response to hyperinflation, not the cause.

The Zimbabwe inflation was caused by food shortages. (The government stole land from farmers and gave it to non-farmers.) Money “printing” was the faulty response to inflation, not the cause.

The most recent inflation was caused by COVID-related shortages of oil, food, shipping, computer chips, metal, housing, lumber, and labor, among other things. As the shortages have been reduced, so has the inflation.

WWII Context: During World War II, many consumer goods were in short supply because production was focused on the war effort. When the war ended, the supply of goods resumed, and the previously unmet demandwas suddenly able to be fulfilled.

Oil Crises: Similarly, during the oil crises of the 1970s, the reduced supply of oil caused prices to spike, not because of a sudden increase in demand, but because the existing demand couldn’t be met.

COVID-19 Pandemic: Supply chain disruptions and production bottlenecks during the pandemic created shortages in various goods, leading to price increasesonce supply constraints eased and the pent-up demand was met.

While the underlying demand might have been consistent, the ability to fulfill that demand was constrained by supply issues. When supply bottlenecks were removed, the previously suppressed demand could finally be expressed, leading to price increases.

Latent Demand: The concept of latent demand suggests that consumers’ desire for goods remains constant, but it is the availability of those goods that fluctuates.

Supply Constraints: Supply-side constraints create temporary mismatches between demand and supply, leading to inflationary pressures once those constraints are lifted.

Observing changes over time can reveal the true causes of economic phenomena. By examining what happens just before and during an inflationary period, we often find that supply-side disruptions are the primary drivers.

Gradual Demand Changes: Demand usually changes slowly, giving the economy time to adjust. This gradual change rarely leads to significant price fluctuations on its own.

Sudden Supply Changes: Supply-side shocks, such as natural disasters, geopolitical events, or production bottlenecks, can occur rapidly and unpredictably. The economy struggles to adjust quickly to these disruptions, leading to price increases as a balancing mechanism.

9. Fact: There is no post-gold standard relationship between federal debt and your taxes.

Unlike state/local governments, which are monetarily non-sovereign, the federal government does not use tax dollars to pay its bills. It creates new dollars, from thin air, every time it pays a creditor.

The sole purposes of federal taxes are:

–To control the economy by taxing what the government wishes to discourage and by giving tax breaks to what the government wishes to reward.

–To assure demand for the U.S. dollar by requiring all federal taxes to be paid in dollars.

Taxes do not pay for federal spending. Federal spending creates dollars.

9.a. Fact: Federal deficit spending does not use “taxpayers’ money.” Federal spending creates money ad hoc.

When the government spends it credits bank accounts. No taxes involved. By definition, deficit spending means taxes do not equal this year’s spending let alone previous year’s spending. Only surpluses use taxpayers’ money, by causing recessions.

For the above reasons, our children and grandchildren will not pay for today’s money creation. Still, they will benefit from today’s deficit spending — better infrastructure, army, education, R&D, safety, security, health, and retirement.

Any time you hear or read about the federal government spending “taxpayers’ money,” know that the person is ignorant about Monetary Sovereignty. The federal government doesn’t spend taxpayers’ money. Period.

10. Fact: There is no post-gold standard relationship between low interest rates and high GDP growth. Opinion: The opposite seems true:

The interest rate and economic growth lines move in opposite directions.

Why do high interest rates stimulate? Opinion: High rates force the federal government to pay more interest, pumping more money into the economy.

The Fed increases interest rates to fight inflation. But increasing interest rates increases the prices of goods and services, i.e. causes inflation.

The Fed, in a sense, is using leeches to fight anemia.

11. Fact: The Federal debt/GDP ratio is a meaningless fraction, because it measures two, mathematically incompatible pieces of data. It’s an apples/oranges comparison. GDP is a one-year measure of output; federal debt is the net outstanding T-securities created since the nation’s birth.

The T-securities created years ago affect this year’s debt in the debt/GDP ratio, while even last year’s GDP does not affect this ratio. See: Debt/GDP

Because federal debt is the total of T-securities, and the federal government has the functional ability to stop creating T-securities at any time, the Debt/GDP ratio easily could fall to 0, depending on federal law.

11.a. Fact: The debt/GDP ratio does not measure the federal government’s ability to pay its bills. The government does not pay bills with GDP; it creates the money ad hoc to pay its bills.

Were GDP to be $0, the government still could pay bills of any size, simply by crediting the bank accounts of its creditors.

12. Facts: In 1979, gross federal debt was $800 billion. In 2009 it reached $12 trillion, a 1400% increase in 30 years. During that period, GPD rose 440% (annual rate of 5.5%>) with acceptable inflation. The same 1400% increase would put the debt at $180 trillion in 2039, a mean annual deficit of $5+ trillion.

This calculates to a 9.5% annual debt increase for the past 30 years. Repeating that growth rate would put the 2010 deficit at about $1.14 trillion, and the 2011 deficit at about $1.25 trillion. The deficit for year 2039 would be about $15.8 trillion.

Opinion: I know of no reason why the results would not be the same as they have been in the past 30 years. However, increasing the debt growth rate above 9.5% might show even better results:

In the 10 year period, 1980 – 1989, federal debt grew 210%, from $900 billion to $2.8 trillion (a 12% annual debt increase), while GDP grew .96% from $2.8 trillion to $5.5 trillion (a 7% annual increase). During that same period, inflation fell from 14.5% in 1980 to 5.2% in 1989. See graph, below.

The peaks and valleys of federal deficits (blue) generally correspond to the peaks and valleys of real (inflation adjusted) Gross Domestic Product growth. The reason: GDP = Federal Spending + Nonfederal Spending + Net Exports

Facts: In summary, large deficits have coincided with real (inflation adjusted) GDP growth

12. Facts: Any health insurance proposal that covers more people will cost more money. Extracting that money from doctors, hospitals, pharmaceutical companies, by necessity, would reduce the availability of health care.

Increasing taxes on any individuals (even the wealthy) or on businesses, will depress the economy by removing money from the economy. Only the federal government can supply additional money while stimulating the economy.

13. Fact: Social Security is supported neither by FICA nor by a trust fund. Were FICA eliminated, and benefits doubled, Social Security still would not go bankrupt unless Congress decided to make this happen.

In June, 2001, Paul O’Neill, Secretary of the Treasury said, “I come to you as a managing trustee of Social Security. Today we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.“

Yet, SS continues to pay benefits. Your Social Security check comes from a mythical trust fund that contains no money and receives no money.

Social Security (and Medicare) benefits are paid ad hoc by the U.S. government, not from a trust fund, and are not dependent on FICA taxes. which (opinion:) can and should be eliminated. See: FICA

14. Fact: The finances of the federal government are different from yours and mine and businesses’ and state, county and city government finances.

Unlike the federal government, which is Monetarily Sovereign, we cannot create unlimited amounts of money to pay our bills. We first need to acquire money, either by borrowing or by saving, to spend.

The federal government does not acquire money. It creates money by spending. As an accounting principle, the tax money you send to the government is destroyed upon receipt. Then the federal government creates new money to pay its bills. The government has no fund from which it pays bills.

Fact: Were taxes to decrease to zero, this would not change by even one penny, the federal government’s ability to spend.

Opinion: The failure to recognize the difference between the Monetarily Sovereign federal government and all other entities, which are monetarily non-sovereign, is the primary reason for recessions and depressions.

15. Fact: The federal government has the unlimited ability to create the dollars to pay any bill of any size. It never can run short of dollars; it never can go broke.

Opinion: The federal government should distribute dollars to each monetarily non-sovereign state, on a per capita basis.

The states would determine how they distribute the dollars (to counties, cities and/or taxpayers). I suggest a distribution of $5,000 per person or a total of $1.5 trillion.

Fact: In 1971, the U.S. went off the gold standard, thereby becoming a Monetarily Sovereign nation, and at that moment, all economics textbooks became obsolete. Sadly, mainstream economists, the politicians and the media have not yet caught up.

Summary: So there you have a list of facts, plus a few opinions, which I have noted. Read the facts and draw your own inferences.

You can find a great number of debt-hawk sites (i.e. Concord Coalition, Committee for a Responsible Federal Budget), which in essence are privately funded think tanks, paid to influence popular belief, with propaganda masquerading as data.

There, you will see data showing the size of the federal debt. These data are presented in a way designed to imply that the debt (money created) is too large.

But you will find no proof of these ideas. You will see no historical graphs equating debt with any negative economic outcome, simply because such graphs do not exist. Debt hawks believe federal deficits are so obviously bad, no proof is needed.

Yet, despite lacking proof, debt-hawks have foisted their opinions on the media, the politicians, weak-minded economists, and the public, much to the detriment of our economy.

The prevention and cure for a loss of democracy is an informed and energized electorate.

With Donald Trump ripping the government and the economy apart, here is what you should know during the two years before casting your vote in the next Congressional elections.

If you voted Republican in previous elections, you probably thought you were voting for conservatives, not those big spending, big taxing bleeding heart liberals. You were fooled.

It’s almost like falling in love with a beautiful, kind, intelligent, compassionate college girl, and today you are shocked and dismayed to discover she has become a gnarly, mean-spirited, ugly wicked witch.

WHAT IS CONSERVATISM?

Conservatives support reduced government spending to limit the size and scope of government. They push for cuts to social programs and other non-defense discretionary spending.

Conservatives prioritize balancing the budget and reducing deficits. They support tax cuts, simplifying the tax code, and measures like a flat or national sales tax.

They are concerned about the national debt and argue that high debt levels can lead to higher interest rates, reduced economic growth, and increased vulnerability to financial crises. They propose measures to reduce spending and reform entitlement programs to address this.

TODAY’S REPUBLICAN PARTY

There was a time when the Republican Party was conservative. However, under Trump, there has been some slippage.

They still favor reduced spending, but only when the reductions don’t touch the very rich. They want to cut (they call it “reform”) Medicare, Medicaid, Social Security, school lunches, and other programs that primarily benefit the middle and the poor.

They still favor tax cuts and tax simplification, but only tax cuts that benefit the rich. And the simplification should not affect those complex tax loopholes that allowed billionaire Donald Trump to pay $500 a year in taxes.

The still claim to worry about the federal debt, but here is the sticking point. To give their millionaire and billionaire voting base those juicy tax cuts, the GOP has to cut other spending or increase the federal debt. But there isn’t enough “other spending” to cut, unless the radically cut all the social programs the majority of voters treasure.

They sent out Mad Dog Musk mindlessly to fire hundreds of thousands of good working people (without considering them as individuals), to take dollars from their pockets and to line the pockets of the millionaires and billionaires.

But even with those dollars stolen from the poor and middle-income families, there isn’t enough money to satisfy the rapacious rich.

Ah, what to do? What to do? While always lacking ideas to help poor and middle-income people, the Republicans never lack for ideas to enrich the rich. Here is the latest:

THE CURRENT POLICY BASELINE

Imagine that your credit card spending is $10,000 a year. Based on your income, you say, I can handle that. I’ll be able to pay it.” But you don’t. So, at the end of the year, you owe &10,000.

The following year, again your credit card spending will be $10,000, and you say, “Last year, I spent $10,000 and my income stayed the same, so I can spend another $10,000 this year.” Do you see anything wrong with that?

That is “Current PolicyBaseline,” and it is the gimmick being proposed by fake conservatives to claim they still are being conservative, by following last year’s policies again this year. They want you to forget that the debt grows while the deficit remains the same.

There is a huge difference between the “Current LAW Baseline and the Current POLICYBaseline, Here is the argument proposed by the U.S. Chamber of Commerce:

Under a current-lawbaseline, preventing the scheduled expiration of key individual, business, and estate tax policies enacted in the 2017 Tax Cuts and Jobs Act (TCJA) would be considered to cost around $4 trillion over 10 years.

Consider a family that paid $10,000 in federal taxes for 2025 but for whom, under existing law, tax rates are scheduled to double in 2026, meaning the family would have to pay $20,000 in federal taxes that year. A current-law baseline would assume this planned change in the law.

But if Congress later decides to increase tax rates by only 50%, using a current-law baseline would count the family as having received a $5,000 tax cut.

Of course, in the real world, the family didn’t receive a tax cut at all; they got a $5,000 tax increase.

Get it? Congress passes a law that calls for a $10,000 tax increase, a later passes a new law that calls for “only” a $5,000 tax increase. Under the “current law” baseline, they could tell the voters they just cut taxes by $5,000.

MAGAs might believe it, but would you?

Suppose Congress adopts a current-law baseline in its FY 2025 budget resolution. In that case, it is all but certain that most—if not all—of the TCJA’s temporary tax provisions would once again have to be sunset to comply with the Senate’s Byrd rule, under which titles in reconciliation bills cannot increase the deficit in years beyond the usual 10-year budget window.

This is because making the TCJA’s temporary provisions permanent would be considered to increase the deficit when measured against current law.

If, on the other hand, Congress were to adopt a current-policy baseline, then lawmakers would have a real chance to deliver permanent tax relief to American families and employers because extending the TCJA’s temporary provisions would not increase the deficit relative to current policy.

It’s all hocus-pocus designed to confuse you, allowing the Republicans falsely to claim they are not increasing the federal deficit while it and the federal debt rises massively.

I AGREE WITH THE DECEPTION OF THE CURRENT POLICY BASELINE

Yes, I agree with the deception because:

1.The federal debt and deficit are not burdens on the government, the taxpayers, or the economy.

The so-called “federal debt” is neither federal nor debt. It is the total of deposits into Treasury Security accounts. These deposits are, and remain, owned by depositors who want a safe interest-paying place to store otherwise unused dollars.

The accounts resemble bank safe deposit boxes in that ownership never passes to the government, which only holds the dollars for safekeeping.

Our Monetarily Sovereign government does not offer these deposits to acquire spending money; the government already has infinite spending money. The sole purpose of T-security accounts is to provide a safe storage place for those unused dollars (which stabilizes the U.S. dollar) and to help the Fed regulate interest rates (by providing a base rate).

Taxpayers do not pay for the debt. Upon maturity, the stored money is returned to the depositors along with interest created by a government computer. Federal taxes don’t fund federal spending.

2.Federal deficit spending benefits the economy by adding growth dollars to GDP.

What does Congress do whenever we have a recession or even a threat of recession? It spends more to stimulate growth.

We have recessions when federal deficit spending growth (blue) declines (vertical gray bars). The government cures these recessions by increasing deficit spending growth.

Nine consecutive recessions have followed this pattern:

Spending growth declines

Recession begins

Spending growth increases

Recession is cured.

It is not a coincidence. It’s simple cause and effect.

SUMMARY

A growing economy requires an increasing supply of money. The so-called “federal debt” (should be termed “economic income”) is not a burden on taxpayers, the government or the economy. Concerns about the so-called “federal debt” and federal deficits hinder economic growth.

Under the “fight fire with fire” concept, I agree with deceiving the public about the Current Policy Baseline not increasing the deficit, because deficit increases are necessary for a healthy economy.

It’s like telling your kids that spinach will make them as strong as Popeye. It won’t, but the spinach is good for them, so . . . I see the current policy baseline as a white lie meant to accomplish a good purpose, though it exposes the hypocrisy of the GOP.

Are you black, yellow, or red? Are you Muslim, Jewish, Buddhist, or of any other non-Christian religion?

Are you female (not a minority but often treated like one), pregnant, or planning to be pregnant? Are you elderly, unemployed, or poor? Are you an immigrant, documented or otherwise.

Are you gay? Are you a descendant of a foreign nationality? Are you a liberal?

Do your leaders promulgate hatred toward any group? Do you feel safe because you’re not part of that group? Do you join in the hatred?

Realize this: Hatred knows no bounds.

Hatred of one group quickly devolves to hatred of other groups. The reason: Hatred of any group says nothing about the group, but it says a great deal about the haters.

None of the abovementioned groups are “good” or “bad.” They all contain individuals who vary according to many qualities and standards. To hate a group is to tell the world you have no discretion.

Assigning a “bad” quality to an entire religion, nationality, or gender is foolish on its face and is the mark of a bigot. When a politician claims that a nationality is composed of “rapists,” he merely announces to the world, “I am an ignorant bigot.” If someone agrees with that statement, they too become ignorant bigots.

Being Jewish, I have been made especially aware that all bigotry devolves to even more bigotry and sadly becomes the world’s oldest hatred. The term “world’s oldest hatred” is often used to describe antisemitism, which refers to hostility, prejudice, or discrimination against Jews.

Antisemitism has a long and tragic history, dating back thousands of years. It has manifested in various forms, including religious, ethnic, and racial discrimination.

Throughout history, antisemitism has taken on different guises, from ancient prejudices in Greece and Rome to the religious persecution during the Middle Ages, and the racial antisemitism that culminated in the Holocaust.

Unfortunately, antisemitism continues to persist in various forms even today. Antisemitic claims are often based on stereotypes and conspiracy theories that have been used throughout history to justify prejudice and discrimination against Jewish people. Some common antisemitic claims include:

Blood Libel: A false accusation that Jews use the blood of non-Jewish children in religious rituals, particularly in the preparation of Passover bread.

Economic Control: The unfounded belief that Jews control the world’s financial systems and economies, often represented in the stereotype of the “greedy Jew.”

Global Conspiracy: The baseless idea that Jews are orchestrating a secret plot to dominate the world, often linked to the debunked publication, “The Protocols of the Elders of Zion.”

Deicide: The claim that Jews are collectively responsible for the crucifixion of Jesus Christ, used historically to justify religious persecution.

Dual Loyalty: The accusation that Jews are more loyal to Israel or international Jewish interests than to their own countries.

Cultural Corruption: The belief that Jews are responsible for promoting moral decay and corrupting cultural values through media and entertainment.

If you are not Jewish, you might feel safe when you read this article:

Antisemitism continues to surge in the United States, with the latest annual survey of American Jews reporting one-third have been targeted in person or online in the last 12 months — and more than half have changed their behavior, including taking steps so they’re not identified as Jewish.And a huge share — almost three-quarters of those surveyed — said Jewish Americans feel less secure than they were a year ago. Three years earlier, less than one-third felt that way.

That has led some people to avoid wearing anything in public that might identify them as Jewish or avoiding publicly commenting on Jewish issues.The sobering findings come from the American Jewish Committee, which commissions major surveys each year, one of Jewish Americans and one of the general population.

The implications are clear, said Ted Deutch, a longtime member of Congress from Broward and Palm Beach counties until he became CEO of the American Jewish Committee in 2022: “Jew hatred” has become “pervasive.”“I have black guys counting my money. … I hate it. Laziness is a trait in blacks. It really is, I believe that. The only guys I want counting my money are short guys that wear yarmulkes all day.”“Antisemitism has reached a tipping point in America, threatening the freedoms of American Jews and casting an ominous shadow across our society,” Deutch said in a statement.

Donald Trump is the quintessential bigot.

He spews hatred of Mexicans, Muslims, immigrants and foreigners in general, and anyone who may object to his hatemongering.

He lives on hatred. Seldom does a day pass when he is not expressing hatred for some group or individual.

To disagree with anything he says or does is to feel his wrath. This is not normal human behavior.

You may disagree with something I say, write, or believe, but being normal, you will not automatically hate me.

Trump would. He measures people, not by what they do, but by only one criterion, “Do they agree with Trump.”

If you criticize anything Trump says or does, he will vilify you as a person — not just your opinion, but you as a human being. To Trump, Vladimir Putin, who murders political opponents, is a “smart man” because he says nice things about Trump.

Trump likes and admires ruthless dictators and wishes to follow their examples. Trump sets the example for those in the MAGA movement, the basis of which is love for Trump and hatred of all others. It is their one unifying aspect and is the mark of a cult: Love for the leader and hatred of “outsiders.”

The Jan 6 attack on Congress resulted from Trump’s lying and hatemongering. People in the MAGA group were driven into a foaming frenzy, physically attacking anyone who stood in their way.

Later, many admitted they had lost their senses, and regretted what they did. These were not bad people. They were sucked into a raging mob by bad people.

The Republican Party has surrendered its moral ground to Trump. Listen to their speeches. Watch Fox News. You will hear snark and hatred far beyond what is customary even in political discourse.

And now, you have billionaire Elon Musk, trying to become a political power by being a Trump toady. He makes broad, bigoted generalizations about government workers being lazy, incompetent, or absent.

The irony of him raking in billions in payments from the government, is not lost.

I have Jewish friends who support Trump. I find this incomprehensible. Seemingly they have forgotten or ignore the lessons Hitler taught — the hatred, the book burning, the unnecessary cruelties inflicted on gays, immigrants, Muslims and opponents.

{kind=link}