The Washington Post and Jeff Stein have joined the ranks of IAMS (Ignorant About Monetary Sovereignty). The following article was published yesterday.

ECONOMIC POLICY:U.S. deficit explodes even as economy grows

Jeff Stein

A strong economy usually reduces the deficit. Not this time.

By Jeff Stein, September 3, 2023 at 6:00 a.m. EDT

The federal deficit is projected to roughly double this year, as bigger interest payments and lower tax receipts widen the nation’s spending imbalance despite robust overall economic growth.

The so-called spending “imbalance” implies that federal spending should be “balanced” against federal taxes. Nothing could be further from the truth.

The U.S. government is unlike state/local governments, businesses, and individuals. It uniquely is Monetarily Sovereign. It alone has the unlimited ability to create dollars. It never unintentionally can run short of dollars.

Even if the federal government collected $0 taxes, it could continue spending forever. The purpose of collecting federal taxes is to control the economy by taxing what the government wishes to discourage and giving tax breaks to what it wishes to encourage.

Unlike state/local taxes which provide state/local governments with spending money, federal taxes do not provide the federal government with spending money.

The typical measure of the economy is GDP. For the economy to grow, the federal government must run deficits, as demonstrated by the formula for GDP:

GDP = Federal Spending + Non-federal Spending + Net Exports

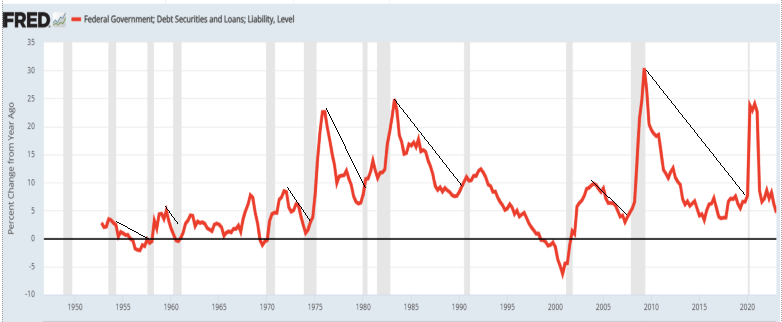

When federal spending declines or doesn’t grow enough, GDP declines. Not only does the formula demand it, but this graph illustrates it:

The red line demonstrates changes in federal deficits. The vertical gray bars are official recessions. The slanted lines show declining deficits leading to recessions, which then are cured by increased deficits.

The graph shows that when federal debt increases too little, we have recessions, which are cured by federal debt increases.

After the government’s record spending in 2020 and 2021 to combat the impact of COVID-19, the deficit dropped by the greatest amount ever in 2022, falling from close to $3 trillion to roughly $1 trillion.

Did you get that line, “Record spending in 2020 and 2021 to combat the impact of COVID-19?” Here, Stein demonstrates his understanding that deficit spending grows the economy, yet still complains about it. And he fails to understand the reverse, that the lack of federal spending will recess the economy.

Quite amazing.

But rather than continue to fall to its pre-pandemic levels, the deficit shot upward.

The deficit shot upward to cure the 2020 recession, a cure that the deficit accomplished.

Budget experts now project that it will probably rise to about $2 trillion for the fiscal year that ends Sept. 30, according to the Committee for a Responsible Federal Budget (CRFB), a nonpartisan group that advocates for lower deficits.

The so-called “non-partisan CRFB” leans heavily to the right, invariably recommending fewer benefits and higher taxes on the middle- and lower-income people, but seldom (if ever) mentions the tax loopholes of the wealthy.

If you go to the CRFB website, you will see many articles grousing about the federal debt and deficits, but none explaining exactly why these are bad for the economy. Perhaps this is the reason for their reticence:

U.S. Depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857. 1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929. 1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

That is the information you never will see on the CRFB website nor presumably in any article written by Jeff Stein for the Washington Post.

The unexpected deficit surge, which comes amid signs of strong growth in the economy overall, is likely to shape a fierce debate on Capitol Hill about the nation’s fiscal policies as lawmakers face a potential government shutdown this fall and choices over trillions of dollars in expiring tax cuts.

The deficit surge didn’t come “amid” the signs of strong growth. The deficit surge caused the strong growth. It’s like saying the Cubs’ good pitching came amid signs of a winning streak. No, the good pitching caused the winning streak.

Stein and the Washington Post don’t see the relationship between adding dollars to the economy and economic growth, despite the abovementioned formula for GDP.

The Senate will return from the August recess this week, and the House will return the following week. Biden and House Speaker Kevin McCarthy (R-Calif.) approved a deal in June to raise the nation’s borrowing limit, but it did little to alter the long-term debt trajectory.

Except, the U.S. federal government, which has the unlimited ability to create U.S. dollars, never borrows U.S. dollars. Who says so? The Federal Reserve:

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

That phrase, “not dependent on credit markets,” is Fed-speak for “doesn’t borrow.” Accepting T-security deposits is not “borrowing,” as the government never touches the money. The dollars are held in privately-owned accounts and upon maturity, they are returned to the depositors.

The higher deficit may undermine Biden’s attempts to take credit for reining in the budget ahead of the 2024 presidential election.

Because Americans have been programmed to believe, falsely, that federal spending is bad — and perhaps because of his own ignorance about federal financing — Biden takes credit for doing something stupid: Reducing the amount of growth dollars the federal government pumps into the economy.

And it could pose a challenge to Republican lawmakers, who — despite their calls for fiscal responsibility — are pushing to extend more than $3 trillion in tax cuts they approved in 2017.

The Republicans always call for “fiscal responsibility” (i.e. the fiscal irresponsibility of reduced spending) when the President is a Democrat. They don’t want the economy to grow during a Democratic administration.

The 2017 tax cuts were cuts for the rich. The GOP, the party of the rich and Trump, always wants those tax cuts. They don’t want cuts to taxes that ordinary people pay, i.e., FICA.

“The deficit will double from 2022 to 2023,” said Marc Goldwein, senior vice president of the Committee for a Responsible Federal Budget. “This should prompt a serious evaluation of federal policy going forward, though I worry it won’t.”

If the deficit actually does double, the economy will grow beautifully. Remember: GDP = ….etc., etc.

Stock market tip: The larger the deficit spending, the faster the stock market will grow. Cut deficit spending, and we’ll have a recession. We always do.

The surge in red ink has confounded many economists’ expectations. Typically, deficits contract when the economy grows because businesses and consumers owe more taxes, and the government does not need to spend as much to protect those who have lost their jobs.

It confounded only those economists who don’t understand Monetary Sovereignty. (Yes, they exist and some have “Peter Principled” their way up to important jobs. Hello, Larry Summers.)

Deficits begin to contract when the economy grows because the ignorante believe they no longer are needed. Eventually, however, this contraction leads to a recession that is cured by increased deficit spending. Recessions aren’t necessary. They are caused by reduced deficit spending.

Think Jeff, if deficit spending grows the economy and cures recessions, why wouldn’t deficit spending grow the economy during non-recession times?

Then deficits typically expand again in downturns, as those factors go into reverse. And yet, the current surge in the deficit is coinciding with a period of unusually strong economic growth amid historic lows in unemployment and robust corporate profits.

No, Jeff, deficits are intentionally expanded to cure downturns.

Jason Furman, who served as a top economist in the Obama administration and is now an economics professor at Harvard, said the current jump in the deficit is only surpassed by “major crises,” such as World War II, the 2008 financial meltdown, or the coronavirus pandemic.

During a major crisis, the government spends more to cure the problem. One wonders why this is so difficult for Furman to understand. Obama was notorious for not understanding the economy. Perhaps Furman was at fault.

It also is difficult to understand why economists, people who spend their lives looking at the economy and federal spending, can’t make that mental connection. It’s quite simple:

The government has infinite dollars.

Adding dollars to the economy grows the economy.

Therefore the federal government always should run deficits.

Is that really beyond their ken? Or is the problem simply semantic? Words like “debt,” “borrow,” and “deficit” do not have the same implications for a Monetarily Sovereign entity as they do for monetarily non-sovereign entities.

Or do they falsely believe that federal spending causes inflation?

The wrongheaded printing of larger currency denominations when facing inflation gives the illusion that the currency printing causes inflation, when in fact, inflation causes the wrongheaded currency printing.

The slogan, “Inflation is too much money chasing too few goods and services,” should be, “Inflation is too few goods and services.” Period.

Today’s inflation was caused by shortages of oil, food, lumber, computer chips, shipping, labor, and other goods and services. If the Saudis keep cutting production, we will have another increase in inflation. And no, raising interest rates will do nothing to stop it.

In fact, raising interest rates makes things more expensive as interest is a business cost that must be overcome.

The U.S. economy is expected to grow at a steady 2.1 percent this year.

Thankfully, the government was smart enough to increase the spending that pumped growth dollars into the economy.

“To see this in an economy with low unemployment is truly stunning. There’s never been anything like it,” Furman said. “A good and strong economy, with no new emergency spending — and a deficit like this.

The fact that it is so big in one year makes you think it must be some weird freakish thing going on.”

The “weird, freakish thing” is the economy’s normal reaction to federal spending. Seemingly, Mr. Furman, the Harvard economist, doesn’t understand basic algebra: GDP=Federal and Nonfederal Spending + Net Exports.

From August 2022 to this July, the federal government spent roughly $6.7 trillion while bringing in roughly $4.5 trillion. According to the Committee for a Responsible Federal Budget, that represents a total increase in spending of 16 percent relative to last year and a 7 percent decrease in revenue.

Let me rephrase his statement: “From August 2022 to this July, the federal government pumped a net of 2.2 trillion growth dollars into the economy.” And he thinks the GDP growth is “weird and freakish”??

The Treasury Department is also on track to take in substantially less new revenue this year, partly because of the stock market’s slump last year.

Rephrase: “The Treasury Department is also on track to take in substantially fewer growth dollars out of GDP this year.”

In 2021, amid a cryptocurrency bubble and an explosion in housing prices driven by rock-bottom interest rates, investors recorded huge gains that led them to pay capital gains taxes at record levels. But then the bubble burst, leading to a sharp drop in capital gains tax revenue.

Automatic adjustments to the tax brackets to account for inflation also reduced tax obligations for many Americans, resulting in less incoming revenue relative to last year.

Then, a number of other spending increases contributed to the rising deficit — Social Security payments increased because they are indexed to inflation; the government spent more on education, veterans benefits, and health care; and the bipartisan infrastructure law, as well as the 2022 Inflation Reduction Act, started sending billions of dollars out from the government’s accounts.

Experts are fiercely divided on the extent to which the higher deficit amounts to a pressing problem for the economy.

The experts who understand basic algebra and Monetary Sovereignty are not divided. Deficits are not a problem; they are how the economy grows.

The federal government can issue more debt even as interest payments rise, with demand for the dollar remaining strong.

The federal government doesn’t need to “issue debt.” The sole purposes of so-called “debt” (i.e., T-securities) are:

To provide a safe place for people and nations to store unused dollars. This stabilizes the value of the dollar.

To provide a continuing demand for the dollar because taxes must be paid in dollars.

Issuing debt does not provide the federal government with spending money. It creates, ad hoc, all the dollars it spends.

That isn’t always the case: In Argentina, soaring debt levels have forced the government to impose limits to prevent citizens from taking money outside the country.

Argentina printed currency rather than curing the food shortages causing its inflation.

Other government debt crises have been marked by catastrophic drops in the exchange rate amid investor concerns that the currency will be devalued. These signs of distress have not materialized in the United States.

Fears of a debt crisis during the Obama administration also consistently failed to materialize, emboldening those who regarded the warnings of fiscal conservatives demanding budget cuts as overblown and ideologically motivated.

The demands being seen today are overblown, ideologically motivated, and based on national ignorance about Monetary Sovereignty. If the populace understood MS, the politicians would not be able to get away with nutty “debt ceilings” and ignorant arguments by the Committee for a Responsible Federal Budget.

“If you think of places that have actually had problems of real fiscal sustainability which have gotten to the point of crisis — we know what those places look like, and this doesn’t look anything look like that,” said Matthew C. Klein, publisher of the Overshoot, a subscription research service focused on the global economy.

“You can argue about whether you want it, but this is not a crisis.”

Krugman vacillates between understanding Monetary Sovereignty and not even understanding economics. A kind of is and isn’t, sort of like the Nobel-that-is-not-a-Nobel he won.

As a justification for his style of trade wars, President Trump had alluded to a goal of revitalizing jobs in the U.S. manufacturing industry by protecting it from unfair trade practices of other countries, particularly China. However, according to a study by two Federal Reserve Bank staff, the effect was just the opposite, i.e., a reduction in U.S. manufacturing employment (Flaaen and Pierce, 2019 https://www.federalreserve.gov/econres/feds/files/2019086pap.pdf ). President Biden has not reversed Trump’s trade measures, but the focus of U.S. actions has predominantly shifted to the science-and-technology dimension, notably on China’s access to semiconductors and other high-tech areas.

Neither Trump or Biden understand tariffs? Blind leading the blind.

Could forward this to the smug little twerp: http://heteconomist.com/exercising-currency-sovereignty-under-self-imposed-constraints/ “traces through six steps (identified by Scott Fullwiler) that are involved when the US government requires itself to match net spending with bond sales to the private sector. The effects are presented in terms of simplified balance sheets of government agencies (the central bank and fiscal authority) and members of the non-government (primary dealers, commercial banks, spending recipients).”

Of the three options only the two step one entirely does away with the fiction of government “borrowing” altogether. As I understand most of the MMTs favor the three step Overt Monetary Financing option. Though I have noticed Kelton on Twitter occasionally saying something outright in favor of the two step approach.

These are good articles, which will be understood primarily by people who ALREADY understand the process.

Does anyone believe that idiots like MTG or others of like ilk understand it? The House and Senate are filled with people whose ignorance is exceeded only by their stupidity.

By the way, he wrote, ” It creates the illusion that the currency issuer is revenue constrained when in actuality it is only constrained by real resources and politics.” I’m not sure what the “real resources” are that constrain a currency issuer. I can’t think of any.

Don’t all those business people in Congress understand that balance sheets have to ‘balance’ hence the name? Transactions on the two sides have got to net out to zero.

As for “real resources” that can constrain a currency issuer I understood that to mean the shortages of real resources that cause inflation. For a currency issuer inflation is the only limit besides politics but voting to create dollars to spend on increasing those real resources which are in shortage can alleviate that over a period of time.

Yes, agreed. Even if a government has zero resources, it still can spend money — on buying resources to cure inflation.

That is something even MMT doesn’t quite get. They still believe spending causes inflation. Stephanie and I have debated this.

History doesn’t support MMT on this. They see Zimbabwe et al and believe currency printing causes or worsens the inflation, but it is the inflation shortages that cause/worsen the currency printing. They have it bass-ackward.

Their logic is that adding to the supply of money cheapens the money. I once believed it myself because it is true of all other commodities. It’s the “marginal value” idea.

But money is not like any other commodity. The demand doesn’t lessen when more is added. Unique among goods.

Spending is constrained only by politics and ignorance.

Zimbabwe could not feed itself as well run farms were successively nationalized then broken up into smaller pieces that destroyed the economies of scale inherent in larger farms and then the bits and pieces handed out to persons with little to no agronomic aptitude.

That was how I heard it described by a refugee agronomist from Zimbabwe at a soil conservation thing I went to at one of the state university’s model farms.

Of course the MMTs who talk about jobs but don’t seem to have any history of doing any heavy lifting under the hot sun themselves wouldn’t know much about working the land.

The German inflation of the early 1920’s is easily explainable too in terms of fixed exchange rates [reparations were payable in gold-marks at the pre-war rate of exchange], the huge reparations required to be drained out of the economy month after month, a big chuck of the country under occupation. Was kind of like the Clinton Surplus on steroids.

‘Even if a government has zero resources, it still can spend money — on buying resources to cure inflation.’ Postwar Japan did that quite ably self financing most of it with Yen created by recapitalized banks which were rewarded by Tokyo for continually increasing their capital so to be able to continually bring into existence ever greater amounts of Yen to get the resources their country lacked. The Princes of the Yen understood the possibilities of that far better than did the Americans who laid out some simple rules of the road when in April 1949 they assigned Japan a ¥360 per USD peg within the Bretton Woods system of fixed exchange rates. At ¥360 per USD it stayed from Spring 1949 until December 1971 it rebalanced to ¥308 per USD under the short-lived Smithsonian Agreement the collapse of which in early 1973 yielded the fiat world of floating exchange rates too few understand even now 50 years on.

Clearly, banks don’t lend DEPOSITS; the lending by all banks greatly exceeds their deposits.

And, by law, banks are allowed to lend a multiple of CAPITAL, so again clearly, they aren’t lending capital.

So exactly what are banks lending? All limits on bank lending have to do with SAFETY, not with the banks’ ABILITY to lend. A tiny bank in a one-horse town has the ABILITY to lend many trillions of dollars.

It can do this simply by increasing its depositors’ checking account balances, which today involves pressing a couple of computer keys. Open a checking account in the Rodger M Mitchell Faux Bank, and I will “lend” you $10 trillion by increasing your checking account balance to $10 trillion. No problem.

Then, you will be able to write checks against that $10 trillion. Those checks will be perfectly good until the Fed refuse to clear the transaction or my depositors wish to close their accounts. At that time RMMB will be unable to cover — as would every bank in the world if enough depositors wish to close.

No bank has enough resources to cover ALL depositors wishing to close their accounts, but a big bank has the power to cover a $10 trillion check.

Money is not a “thing.” It is numbers. Period. The only thing that limits a bank’s lending is the lending laws created by the issuer. If, for instance, the U.S. government decided that banks are allowed to lend 1 million % of their capital, that’s what banks would do, and the resultant loan dollars would be perfectly good — for a while.

Case in point: The Federal government spends dollars it doesn’t have and never has. To pay a bill it sends INSTRUCTIONS, not dollars, to the creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

The bank obeys those instructions by pressing a couple of computer keys and voila (!), genuine dollars are created and added to M1.

The actual creation of dollars by banks has nothing to do with reserves, or capital, or deposits, or any other factor, all of which relate to SAFETY, not to the existence of the dollars.

Again, dollars are just numbers. Today, I could give you a check for a million dollars. That check is a form of INSTRUCTIONS telling your bank to raise your checking account balance by a million dollars. If your bank obeyed those instructions, a million new dollars would be created, instantly. Those dollars would be as real as any other U.S. dollars in the world.

Everyone who ever has passed a bad check has proved this many times, as has every counterfeiter.

Where did the dollars come from? This air and the rules of the game. That is where all money comes from: Thin air and the rules of the game — ruled that can be changed instantly by whomever has the power to change rules.

I must laugh at the economists who struggle to explain how banks and the U.S. government create dollars, as though dollars were physical things. All explanations relate to the then-current laws, which are related to SAFETY, not to the CREATION of dollars.

In short, the answer to the question, “How are dollars created and by whom?” is this: The numbers in dollar accounts simply are increased by whomever has the power to change those accounts.

I know you always say that but I don’t see it happening in my lifetime and I’m still in my forties. Every few years Republicans try to kill off that federally owned Import-Export Bank. Baby steps RMM maybe the other 49 states can first follow the lead of North Dakota or for cities to self finance through municipal public banks of their own. https://www.cutimes.com/2023/07/24/public-banks-an-important-idea-whose-time-is-overdue/

I am quite sure I didn’t invent it, as I am equally sure Warren didn’t. Webster says, “A governmental action or direction that purports to benefit the populace as a whole.” I don’t know the etymology of the phrase. If you can find it, please let me know.

https://www.debtclock.ca/ Holy Balls only $1.2 trillion for 40 million people. Should be spending more!

The Globe and Mail is a Canadian newspaper printed in five cities in western and central Canada. With a weekly readership of approximately 2 million in 2015, it is Canada’s most widely read newspaper on weekdays and Saturdays, although it falls slightly behind the Toronto Star in overall weekly circulation because the Star publishes a Sunday edition, whereas the Globe does not. The Globe and Mail is regarded by some as Canada’s “newspaper of record”.

Ignorance is bliss Rodger. The WPO is filled with blissful writers.

LikeLike

Does NYT’s cruddy Krugman live in bliss too? https://www.thestreet.com/economonitor/emerging-markets/krugman-rediscovers-the-wheel-commercial-banks-as-creators-of-money

LikeLike

Krugman vacillates between understanding Monetary Sovereignty and not even understanding economics. A kind of is and isn’t, sort of like the Nobel-that-is-not-a-Nobel he won.

LikeLike

A kind of is and isn’t:

As a justification for his style of trade wars, President Trump had alluded to a goal of revitalizing jobs in the U.S. manufacturing industry by protecting it from unfair trade practices of other countries, particularly China. However, according to a study by two Federal Reserve Bank staff, the effect was just the opposite, i.e., a reduction in U.S. manufacturing employment (Flaaen and Pierce, 2019 https://www.federalreserve.gov/econres/feds/files/2019086pap.pdf ). President Biden has not reversed Trump’s trade measures, but the focus of U.S. actions has predominantly shifted to the science-and-technology dimension, notably on China’s access to semiconductors and other high-tech areas.

Neither Trump or Biden understand tariffs? Blind leading the blind.

LikeLike

Could forward this to the smug little twerp: http://heteconomist.com/exercising-currency-sovereignty-under-self-imposed-constraints/ “traces through six steps (identified by Scott Fullwiler) that are involved when the US government requires itself to match net spending with bond sales to the private sector. The effects are presented in terms of simplified balance sheets of government agencies (the central bank and fiscal authority) and members of the non-government (primary dealers, commercial banks, spending recipients).”

There are only three choices for what to do. The convoluted status quo is 6 steps. Overt Monetary Financing is 3 steps and solely relying on the interest on reserves mechanism is two steps. http://heteconomist.com/overt-monetary-financing-in-terms-of-simplicity-and-transparency/

Of the three options only the two step one entirely does away with the fiction of government “borrowing” altogether. As I understand most of the MMTs favor the three step Overt Monetary Financing option. Though I have noticed Kelton on Twitter occasionally saying something outright in favor of the two step approach.

LikeLike

These are good articles, which will be understood primarily by people who ALREADY understand the process.

Does anyone believe that idiots like MTG or others of like ilk understand it? The House and Senate are filled with people whose ignorance is exceeded only by their stupidity.

By the way, he wrote, ” It creates the illusion that the currency issuer is revenue constrained when in actuality it is only constrained by real resources and politics.” I’m not sure what the “real resources” are that constrain a currency issuer. I can’t think of any.

LikeLike

Don’t all those business people in Congress understand that balance sheets have to ‘balance’ hence the name? Transactions on the two sides have got to net out to zero.

As for “real resources” that can constrain a currency issuer I understood that to mean the shortages of real resources that cause inflation. For a currency issuer inflation is the only limit besides politics but voting to create dollars to spend on increasing those real resources which are in shortage can alleviate that over a period of time.

LikeLike

Yes, agreed. Even if a government has zero resources, it still can spend money — on buying resources to cure inflation.

That is something even MMT doesn’t quite get. They still believe spending causes inflation. Stephanie and I have debated this.

History doesn’t support MMT on this. They see Zimbabwe et al and believe currency printing causes or worsens the inflation, but it is the inflation shortages that cause/worsen the currency printing. They have it bass-ackward.

Their logic is that adding to the supply of money cheapens the money. I once believed it myself because it is true of all other commodities. It’s the “marginal value” idea.

But money is not like any other commodity. The demand doesn’t lessen when more is added. Unique among goods.

Spending is constrained only by politics and ignorance.

LikeLike

Zimbabwe could not feed itself as well run farms were successively nationalized then broken up into smaller pieces that destroyed the economies of scale inherent in larger farms and then the bits and pieces handed out to persons with little to no agronomic aptitude.

That was how I heard it described by a refugee agronomist from Zimbabwe at a soil conservation thing I went to at one of the state university’s model farms.

Of course the MMTs who talk about jobs but don’t seem to have any history of doing any heavy lifting under the hot sun themselves wouldn’t know much about working the land.

The German inflation of the early 1920’s is easily explainable too in terms of fixed exchange rates [reparations were payable in gold-marks at the pre-war rate of exchange], the huge reparations required to be drained out of the economy month after month, a big chuck of the country under occupation. Was kind of like the Clinton Surplus on steroids.

‘Even if a government has zero resources, it still can spend money — on buying resources to cure inflation.’ Postwar Japan did that quite ably self financing most of it with Yen created by recapitalized banks which were rewarded by Tokyo for continually increasing their capital so to be able to continually bring into existence ever greater amounts of Yen to get the resources their country lacked. The Princes of the Yen understood the possibilities of that far better than did the Americans who laid out some simple rules of the road when in April 1949 they assigned Japan a ¥360 per USD peg within the Bretton Woods system of fixed exchange rates. At ¥360 per USD it stayed from Spring 1949 until December 1971 it rebalanced to ¥308 per USD under the short-lived Smithsonian Agreement the collapse of which in early 1973 yielded the fiat world of floating exchange rates too few understand even now 50 years on.

From what I gather the MMTs don’t much like that German economist Werner whose focus is mostly on banking and what it is that banks actually do and how what they do sets them apart from all other entities within the economy. https://www.sciencedirect.com/science/article/pii/S1057521915001477?via%3Dihub

LikeLike

Question: How are dollars created and by whom?

Clearly, banks don’t lend DEPOSITS; the lending by all banks greatly exceeds their deposits.

And, by law, banks are allowed to lend a multiple of CAPITAL, so again clearly, they aren’t lending capital.

So exactly what are banks lending? All limits on bank lending have to do with SAFETY, not with the banks’ ABILITY to lend. A tiny bank in a one-horse town has the ABILITY to lend many trillions of dollars.

It can do this simply by increasing its depositors’ checking account balances, which today involves pressing a couple of computer keys. Open a checking account in the Rodger M Mitchell Faux Bank, and I will “lend” you $10 trillion by increasing your checking account balance to $10 trillion. No problem.

Then, you will be able to write checks against that $10 trillion. Those checks will be perfectly good until the Fed refuse to clear the transaction or my depositors wish to close their accounts. At that time RMMB will be unable to cover — as would every bank in the world if enough depositors wish to close.

No bank has enough resources to cover ALL depositors wishing to close their accounts, but a big bank has the power to cover a $10 trillion check.

Money is not a “thing.” It is numbers. Period. The only thing that limits a bank’s lending is the lending laws created by the issuer. If, for instance, the U.S. government decided that banks are allowed to lend 1 million % of their capital, that’s what banks would do, and the resultant loan dollars would be perfectly good — for a while.

Case in point: The Federal government spends dollars it doesn’t have and never has. To pay a bill it sends INSTRUCTIONS, not dollars, to the creditor’s bank, instructing the bank to increase the balance in the creditor’s checking account.

The bank obeys those instructions by pressing a couple of computer keys and voila (!), genuine dollars are created and added to M1.

The actual creation of dollars by banks has nothing to do with reserves, or capital, or deposits, or any other factor, all of which relate to SAFETY, not to the existence of the dollars.

Again, dollars are just numbers. Today, I could give you a check for a million dollars. That check is a form of INSTRUCTIONS telling your bank to raise your checking account balance by a million dollars. If your bank obeyed those instructions, a million new dollars would be created, instantly. Those dollars would be as real as any other U.S. dollars in the world.

Everyone who ever has passed a bad check has proved this many times, as has every counterfeiter.

Think of the board game Monopoly, which was described here: https://mythfighter.com/2017/04/13/does-the-u-s-treasury-really-destroy-your-tax-dollars/. Instead of using paper dollar bills, we used a record of dollars. If the rules of the game allowed the Bank to increase my balance by $10 million, I would be a million dollars richer.

Where did the dollars come from? This air and the rules of the game. That is where all money comes from: Thin air and the rules of the game — ruled that can be changed instantly by whomever has the power to change rules.

I must laugh at the economists who struggle to explain how banks and the U.S. government create dollars, as though dollars were physical things. All explanations relate to the then-current laws, which are related to SAFETY, not to the CREATION of dollars.

In short, the answer to the question, “How are dollars created and by whom?” is this: The numbers in dollar accounts simply are increased by whomever has the power to change those accounts.

LikeLike

So few understand the ‘reserves’ that never leave the Federal Reserve: https://www.newhavenbiz.com/article/tnb-seeks-to-become-states-newest-bank-in-face-of-fed-delays Who knew narrow banks were to be feared? https://www.tnbusa.com/news/

LikeLike

All unnecessary if all banks were owned by the federal government. There is no public purpose served by privately owned banks. See https://mythfighter.com/2019/09/10/more-evidence-that-the-federal-government-should-own-all-banks/

LikeLike

I know you always say that but I don’t see it happening in my lifetime and I’m still in my forties. Every few years Republicans try to kill off that federally owned Import-Export Bank. Baby steps RMM maybe the other 49 states can first follow the lead of North Dakota or for cities to self finance through municipal public banks of their own. https://www.cutimes.com/2023/07/24/public-banks-an-important-idea-whose-time-is-overdue/

LikeLike

Well, for sure, I don’t see much more happening in MY lifetime. But I’ll keep (verb here) ’til the end.

LikeLike

When Mosler talks now about ‘public purpose’ is that something he picked up from you?

LikeLike

I am quite sure I didn’t invent it, as I am equally sure Warren didn’t. Webster says, “A governmental action or direction that purports to benefit the populace as a whole.” I don’t know the etymology of the phrase. If you can find it, please let me know.

LikeLike

https://www.theglobeandmail.com/business/article-canada-interest-rates-government-debt/ Ever attempt to educate our northern neighbor about their parliament’s Monetary Sovereignty over their Dollar?

https://www.debtclock.ca/ Holy Balls only $1.2 trillion for 40 million people. Should be spending more!

The Globe and Mail is a Canadian newspaper printed in five cities in western and central Canada. With a weekly readership of approximately 2 million in 2015, it is Canada’s most widely read newspaper on weekdays and Saturdays, although it falls slightly behind the Toronto Star in overall weekly circulation because the Star publishes a Sunday edition, whereas the Globe does not. The Globe and Mail is regarded by some as Canada’s “newspaper of record”.

https://www.theglobeandmail.com/about/contact/#tgamcontactussubmitting

LikeLike