I asked ChatGPT a few questions about federal debt and was pleasantly surprised by its answers. It seems to have a far better understanding than many of our Senators, Representatives, President, economists, and even some friends and family.

Here is the conversation:

RM: Regarding the debt limit, when people speak of “federal debt,” what are they referring to?

ChatGPT: When people talk about federal debt, they mean the total amount the U.S. Treasury owes to holders of Treasury securities (bills, notes, bonds, savings bonds, TIPS, etc.). Bottom line: federal debt = all outstanding Treasury securities, whether owned by the public or government accounts.

RM: What is the purpose of Treasury Securities?

ChatGPT:

1.Safe place to store money

Treasury bills, notes, and bonds are considered the safest financial assets in the world. Individuals, banks, pension funds, insurance companies, and foreign governments buy them as a guaranteed way to hold dollars and earn a bit of interest.

For big investors, they function almost like a savings account at the Fed.

2. Primary tool of monetary policy

The Federal Reserve uses Treasuries to manage interest rates and the money supply. When the Fed buys Treasuries, it pumps bank reserves (money) into the system. When it sells Treasuries, it drains reserves out.

This is how the Fed controls the federal funds rate and, by extension, credit conditions in the economy.

3. Accounting mechanism for government spending

Since the U.S. is monetarily sovereign (it creates the dollar), the government doesn’t need to borrow its own currency to spend. But, Congress has set it up so that when the government spends more than it taxes, the Treasury issues securities equal to the shortfall.

In practice, this just converts reserves (bank dollars) into Treasuries — swapping one form of government liability for another.

Key point: Treasuries don’t “fund” the government the way a household borrows. The U.S. can always create the dollars it owes. Instead, Treasuries exist to:

-provide a risk-free asset for savers,

-give the Fed a tool to steer the economy, and

-comply with Congress’s self-imposed rules on deficit spending.

RM: Why is there a debt limit?

1. Historical accident

Before 1917, Congress had to approve each individual bond issue to cover spending. During World War I, that became unworkable, so Congress gave Treasury more flexibility: it could issue debt as needed, but only up to a set ceiling.

That ceiling — the debt limit — was meant as a convenience, not a constraint on whether the U.S. could pay its bills.

2. Symbolic “fiscal discipline”

Supporters say the limit is supposed to force Congress to pause and consider federal spending and borrowing levels. In practice, however, it doesn’t control deficits at all. Those are determined by tax and spending laws already passed.

The debt limit just controls whether Treasury can pay obligations it already owes.

3. Political leverage

Because not raising the limit risks a technical default, it has become a bargaining chip in partisan battles.

Each time the ceiling is reached, opponents of the administration often use it to demand spending cuts or other concessions.

4. Why it doesn’t make economic sense

The U.S. is monetarily sovereign. It issues the dollar, so it can always meet dollar-denominated obligations. The debt ceiling creates artificial “default risk” that doesn’t exist economically— only legally.

Most other advanced countries don’t have a separate debt ceiling. They control deficits through the normal budget process.

So the purpose of the debt limit is political signaling, not financial necessity.

RM: What would happen if we abolished the debt ceiling?

ChatGPT: If the debt ceiling were abolished, here’s what would change — and what wouldn’t:

🔹 What would change

No more periodic crises

Treasury could always issue securities (bonds, notes, bills) as needed to match whatever spending Congress already approved.

No more last-minute showdowns about “default” every year or two.

No artificial risk of default

The U.S. would continue to pay interest and redeem maturing securities without interruption.

Global markets would lose the recurring fear that Congress might deliberately block payment on America’s own obligations.

Political fights move to the budget process

Debates over deficits and spending would happen where they belong: when tax and spending laws are written.

The debt limit would no longer be a hostage-taking device after the fact.

🔹 What would NOT change

Deficits would still exist

If spending exceeds tax revenue, Treasury would still issue new securities. That’s just how the accounting system is set up.

Abolishing the limit doesn’t increase spending; it just removes the arbitrary cap.

Treasuries would still be issued

Even without a ceiling, Treasury securities would continue to exist, because they serve as the world’s safest savings asset and are essential to monetary policy.

Inflation risk stays the same

The real economic constraint on federal spending is inflation, not the debt ceiling.

If government spends too much relative to the economy’s capacity, prices rise. That risk is unchanged whether or not there’s a ceiling.

🔹 International comparison

Most advanced economies (UK, Germany, Japan, Canada, etc.) do not have a debt ceiling.

Their governments borrow as needed, automatically authorized by their budget laws.

The U.S. is an outlier in tying itself to a separate, arbitrary cap.

Bottom line:If the U.S. abolished the debt ceiling, the economy would function more smoothly, the risk of self-inflicted default would vanish, and nothing fundamental about deficits or inflation would change.

The fights over “fiscal discipline” would just shift back to the regular budget process, where they logically belong.

RM: The UK, Germany, Japan, and Canada “borrow as needed”? Uh oh. Bit of a problem, there.

ChatGPT: Right — good catch. The phrase “borrow as needed” hides an important distinction.

Let’s be precise:

1. Monetary Sovereigns (UK, Japan, Canada, US)

They issue their own free-floating currency (pound, yen, Canadian dollar, US dollar).

They can never “run out” of their currency, since all their debt is payable in what they themselves create.

Their “borrowing” (issuing government bonds) is really just swapping one government liability (bank reserves) for another (securities).

Insolvency in their own currency is impossible; inflation is the only real limit.

2. Eurozone countries (Germany, France, Italy, etc.)

They don’t issue their own sovereign currency. They use the euro, which is controlled by the European Central Bank (ECB).

When Germany or Italy “borrows,” they’re more like a U.S. state or city — they can genuinely default because they don’t control the euro’s creation.

That’s why Europe has had sovereign debt crises (Greece, 2010s), whereas Japan, with debt >250% of GDP, has not.

So:

UK, Japan, Canada, US → issue their own money; their “borrowing” is voluntary, not necessary.

Germany and other euro countries → non-sovereign users of the euro; they really do rely on markets to buy their debt, and default risk is real.

👉 That’s the “uh oh.” People often lump them together, but the sovereign vs. non-sovereign distinction is crucial.

RM: Visualize an America that did not issue Treasury Securities.

ChatGPT:

1. What happens when the U.S. government spends now

Congress authorizes spending.

Treasury instructs the Fed to credit bank accounts (for Social Security checks, contracts, etc.).

The Fed simply marks up numbers in the banks’ reserve accounts — new dollars created.

To balance the books, Treasury then issues securities (bonds, bills, notes) equal to the deficit.

So: spending creates dollars → securities just “mop up” the excess by converting reserves into bonds.

2. Could the U.S. stop issuing bonds entirely?

Yes. Since the government is the monopoly issuer of dollars, it doesn’t need to borrow its own currency. If Congress allowed it, Treasury could:

Spend as authorized,

Leave the extra dollars as bank reserves in the Fed system,

And skip the bond sales.

The result would be the same net financial assets in the private sector, just held as reserves (zero-interest money) instead of Treasuries (interest-bearing money).

3. Why they don’t do this

Monetary policy tool: Treasuries let the Fed manage interest rates. If only reserves existed, interest rates would fall toward zero unless the Fed paid interest on reserves (which it actually started doing in 2008).

Safe savings asset: Global investors, banks, pensions, and foreign governments want Treasuries. They’re the benchmark risk-free asset of the world. Abolishing them would upend financial markets.

Political optics: Selling bonds makes it look like the government is “borrowing like a household,” which appeals to deficit hawks. It’s a disguise for what’s really just money creation.

4. Real-world examples

Japan: Debt >250% of GDP, yet no crisis, no inflation spiral. Why? Because its “debt” is just yen-denominated government liabilities.

U.S. during COVID (2020–2021): The Fed essentially financed trillions in new spending by creating reserves and buying Treasuries. Functionally, that’s almost the same as direct money creation.

QE (Quantitative Easing): When the Fed buys Treasuries, it just replaces them with reserves — proving Treasuries are optional.

5. Bottom line

Technically: The U.S. could stop issuing Treasuries tomorrow and still spend without limit.

Practically: Treasuries exist because they stabilize financial markets, give the Fed policy tools, and maintain the illusion of “borrowing” discipline.

👉 In other words, Treasury securities are not about funding the government, but about managing the financial system.

RM: Maybe we should stop calling T-securities “debt,” and start calling them “deposits.”

ChatGPT: Exactly — that’s the crux of it.

Calling Treasury securities “debt” makes them sound like a household loan, which is misleading for a currency-issuing government. A more accurate analogy is:

You buy a Treasury bill → you’re just moving your money from a checking account at the Fed (bank reserves) into a savings account at the Fed (a T-security).

At maturity, Treasury pays you back by shifting the balance from your “savings” (security) back to your “checking” (reserve account).

No outside funding required, no solvency risk — just accounting entries.

Why “debt” is misleading

Households and firms borrow because they can run out of money.

The U.S. government can’t — it issues the dollar.

What we call “debt” is just the government’s promise to return your dollars with a bit of interest, not evidence that it’s short on money.

Why “deposits” makes more sense

They’re functionally deposits at the Fed, just with fixed terms and interest.

They serve as a safe savings instrument for the private sector.

They are assets for investors, liabilities for the government, but not in the sense of a household debt.

Bottom line:Yes — calling them Treasury deposits or savings bonds would be far closer to reality than “debt.” The language of “national debt” fuels fear and politics, but economically, it’s just the sum of dollar-denominated deposits held at the Fed.

Everyone, please raise your hands if you would like ChatGPT (or one of its cousins) to replace the ineffective and misinforming congressional Representatives and Senators we currently have.

Perhaps some of the media and college professors as well.

In that event, I could retire from this blog and devote my remaining time to something less frustrating — like rolling a boulder up a hill.

John Stossel

John Stossel puzzles me. When you first conclude he knows nothing about economics, he writes something spot-on. Then he follows up with ignorance about the same subject.

In that, he reminds of Paul Krugman, who alternately understands, then doesn’t understand, Monetary Sovereignty.

Stossel can do it in two sentences. Here is an article on Reason.com, the Libertarian version of QAnon. Look at the subhead.

“Federal government’s budget deficit will bankrupt us.”

Suddenly, the U.S. government will go bankrupt? After world wars, numerous recessions and depressions, now, when the economy is growing rapidly, the federal government is going bankrupt??

The blue line is Gross Domestic Product. The red line is federal “debt.” There is no hint that federal “debt” is leading to bankruptcy. Quite the opposite. As “debt” grows, so does the economy.

.

The green line is real (allowing for inflation), per capita GDP. There still is no hint that increasing federal “debt” leads to bankruptcy. Again, quite the opposite.

If Stossel wants to bet that next year’s budget deficit will bankrupt the U.S. government, I will put up every dollar I own that says Stossel is wrong. One wonders why someone, anyone, would make such a foolish statement and expect belief.

Being Monetarily Sovereign, the U.S. government cannot run short of U.S. dollars. Increased federal deficit spending is necessary for economic growth. GDP=Federal Spending+Non-federal Spending+Net Exports

Former Federal Reserve Chairman, Alan Greenspan:“A government cannot become insolvent with respect to obligations in its own currency.”

I suspect Stossel knows he’s wrong, so I’m guessing he hasn’t moved to another country or exchanged all his U.S. dollars for another currency in advance of a mythical U.S. bankruptcy.

He’s just promulgating the usual Libertarian BS that has been wrong for at least 84+ years and will continue to be incorrect during his lifetime and beyond.

But wait. He also says, “Trade deficits are trivial.” In that, he is correct.

A trade deficit merely means we give other nations some of the plentiful U.S. dollars we create at the touch of a computer key, and in return, we receive valuable and scarce goods and services.

I run trade deficits with my local Costco and with my cleaning lady. I don’t feel bad about it, though I don’t even have the government’s infinite ability to create dollars.

The more money I have, the more stuff I can buy. The federal government has infinite money.

Maybe Donald Trump is such a powerful communicator and pot-stirrer that other countries, embarrassed by their own trade barriers, will eliminate them. Then, I will thank the president for the wonderful thing he did. Genuine free trade will be a recipe for wonderful economic growth.

But I fear the opposite: a trade war and stagnation—because much of what Trump and his followers say is economically absurd.

“What Trump and his followers say is economically absurd”? Who could have guessed that MAGAs know so little? Could it be possible that QAnon, Fox, Alex Jones, Marjorie Taylor Greene, Tucker Carlson, and Donald Trump are not reliable sources?

“(If) you don’t have steel, you don’t have a country!” announced the president.

Lots of things are essential to America—and international trade is the best way to make sure we have them. When a storm blocks roads in the Midwest, we get supplies from Canada, Mexico, and China. Why add roadblocks?

Steel is important, but “the choice isn’t between producing 100 percent of our steel (and having a country) or producing no steel (and presumably losing our country),” writes Veronique De Rugy of the Mercatus Center.

Trump uses the “you don’t have a country” meme for everything. “If you don’t have a steel industry, you don’t have a country.” “If you don’t have a border, you don’t have a country.” “If you don’t have a wall, you don’t have a country.” “If you don’t have a military, you don’t have a country.” “If you don’t have a strong military, you don’t have a country.”

These are a few of his nonsense statements about the end of America. Ms de Rugy’s response was correct.

Today, most of the steel we use is made in America. Imports come from friendly places like Canada and Europe. Just 3 percent come from China.

Still, insists the president, “Nearly two-thirds of American raw steel companies have gone out of business!”

There’s been consolidation. But so, what? For 30 years, American steel production has stayed about the same. Profits rose from $714 million in 2016 to $2.8 billion last year. And the industry added nearly 8,000 jobs.

Trump loves to cherry-pick, twist, and outright lie about statistics to make his point. A day later, he’ll say the opposite. His followers will swoon at each new version despite its incompatibility with what Trump said yesterday.

Trump says, “Our factories were left to rot and to rust all over the place. Thriving communities turned into ghost towns. You guys know that, right?”

No. Few American communities became ghost towns. More boomed because of cheap imports.

It’s sad when a steelworker loses work, but for every steelworker, 40 Americans work in industries that use steel. They, and we, benefit from lower prices.

Right again, John. Wrong again, Donald.

Trump touts the handful of companies benefiting from his tariffs: “Century Aluminum in Kentucky—Century is a great company—will be investing over $100 million.”

Great. But now we’ll get a feeding frenzy of businesses competing to catch Trump’s ear. Century Aluminum got his attention. Your company better pay lobbyists. Countries, too.

After speaking to Prime Minister Malcolm Turnbull of Australia, Trump tweeted: “We don’t have to impose steel or aluminum tariffs on our ally, the great nation of Australia!”

So, the purpose of tariffs is . . . what? To punish our enemies? To reward our businesses? Or simply increase prices for the American consumer.

Economies thrive when there are clear rules that everyone understands. Now we’ve got “The Art of the Deal,” one company and country at a time.

I understand that Trump, the developer liked to make special deals, but when presidents do that, it’s crony capitalism—crapitalism. You get the deal if you know the right people. That’s what kept most of Africa and South America poor.

But Trump thinks trade itself makes us poorer: “We lose … on trade. Every year, $800 billion.”

Actually, last year’s trade deficit with China was $375 billion. But even if it were $800 billion, who cares? All a trade deficit shows is that a country sells us more than we sell them. We get the better of that deal. They get excess dollar bills, but we get stuff.

Right on, John. We have the infinite ability to create dollars by pressing computer keys. The U.S. government can send dollars into the economy whenever it wants to.

Former Federal Reserve Chairman Ben Bernanke:“The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.”

But we don’t have the infinite ability to create stuff. So, trading dollars for stuff is a great deal for us.

Sadly, when the U.S. government does it, the Libertarians wrongly complain about federal deficits and debt. I wonder whether Stossel will hear about this from his Libertarian pals.

And now we come to the usual Libertarian BS:

Real problems are imbalances like next year’s $1 trillion federal government budget deficit. That will bankrupt us.

It hasn’t happened. It can’t happen. It won’t happen. It’s just that incredible fearmongering by people who know better and should stop now.

Trade deficits are trivial. You run one with your supermarket. Do you worry because you bought more from them than they buy from you? No. The free market sorts it out.

Trump makes commerce sound mysterious: “The action I’m taking today follows a nine-month investigation by the Department of Commerce, Secretary Ross.”

But Wilber Ross is a hustler who phoned Forbes Magazine to lie about how much money he has. Now he goes on TV and claims, “3 cents worth of tin plate steel in this can. So if it goes up 25 percent, that’s a tiny fraction of one penny. Not a noticeable thing.”

Not to him maybe, but Americans buy 2 billion cans of soup.

Political figures like Ross—and Trump—shouldn’t decide what we’re allowed to buy. If they understood markets, they’d know enough to stay out of the way.

Like so many of the people Trump hires, Ross was, shall we say, a questionable character, with many, many claims against his honesty.

The combination of Libertarianism and its attendant economic ignorance, together with economic dishonesty leads to bad (for America) decisions. Cut federal spending and we’ll have the bankruptcyStossel and the Libertarians predict.

As for John Stossel, he still puzzles me.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

This is what passes for “science” in the world of economics:

Raising interest rates increases the prices of everything. Therefore, raise interest rates to cure inflation.

Inflation happens when the economy grows too much (“overheated”). Therefore, to cure inflation, cause a recession or depression.

Any normal scientist would scoff at these beliefs, but economists are neither normal nor scientists. They are believers. They are cultish followers of the standard thinking, as exhibited in the following article.

When a hypothesis doesn’t work, a scientist uses that information to develop a new hypothesis. In economics, when a hypothesis doesn’t work, the economist merely shrugs and continues to claim it works.

Before COVID, the economy was growing massively, with interest rates near zero, massive deficits, and without inflation? Then, during and after COVID, we had inflation, with interest rates at elevated levels.

Did the economists learn anything from these events?

Hmmm. Now, let me think. Why did we have no inflation before COVID and elevated inflation during and after COVID? What changed? Two things”

We had shortages of oil, food, shipping, computer chips, metals, lumber, labor, and almost every other important good and service

The Fed raised interest rates, instantly making every product more expensive.

What didn’t change?

The government still is spending massively with huge deficits.

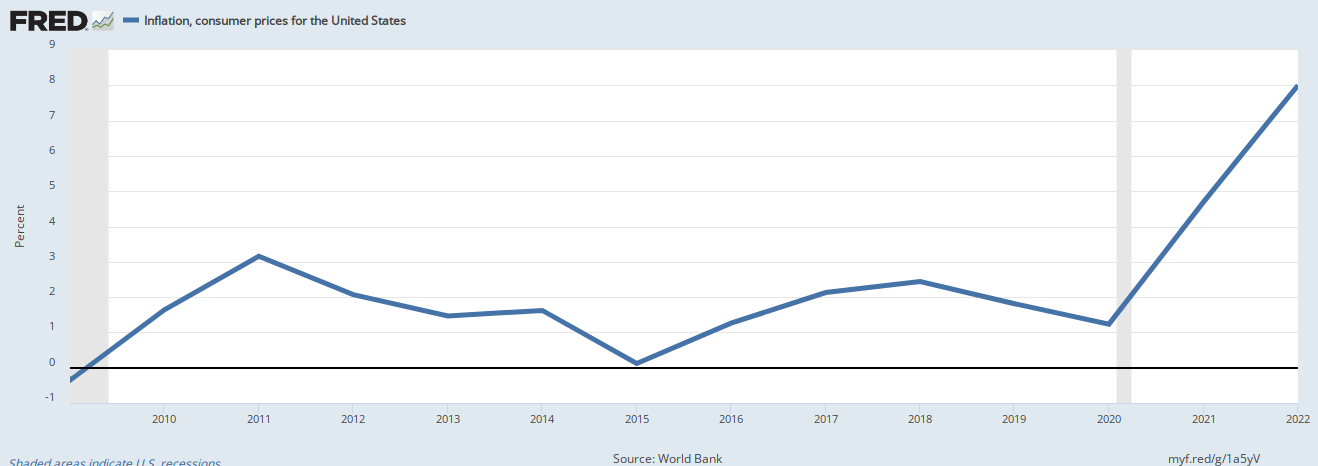

Analyze the following graph:

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.When supply cannot meet demand, prices go up. That’s basic.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.

Inflation has fallen from the shocking highs reached last year, but the Federal Reserve’s efforts have not successfully returned the beast to its cage.

The problem is supply, so what does the Fed do? It tries to control demand.

Why? Because that is the only tool it has. Because Congress is so inept, it has tasked the Fed with preventing and curing inflation. But the Fed can’t do it.

Who can control inflation? Congress and the president can control inflation by controlling shortages.

Oil shortage: Financial rewards to oil companies to find more, pump more, hire more, and lower prices

Food shortage: Financial rewards to farmers, wholesalers, and retailers to reduce risk, reward growth and lower prices

Labor shortage: Eliminate FICA plus Medicare for All to make employment less expensive and to encourage higher net salaries.

Federal rewards to all other industries involved with scarce goods and services.

Do you notice a commonality among the solutions? They all require more deficit spending, not less.

If rising prices are to be fully tamed, it increasingly looks like Congress will have to get the deficit under control first.

Rather than attacking the cause of inflation, scarcity, Boehm attacks the cure for inflation, federal deficit spending to cure shortages.

Prices are up 3.7 percent over the past year, according to new inflation data released by the Bureau of Labor Statistics on Thursday morning. But so-called “core inflation,” which filters out the more volatile categories like food and fuel prices, rang in at 4.1 percent in the newest report.

Oil and food are the “core inflation” goods. Their shortages and resultant price increases cause most inflations, worldwide.

Typical for the pseudo-science of economics, economists filter out the two most common causes of inflation — oil and food scarcity — when measuring inflation.

It’s like a sports team filtering out points scored and allowed when analyzing the team’s won/lost record. Senseless.

To control inflation, the Federal Reserve raised interest rates at 11 consecutive meetings starting in March last year.

Every one of those interest rate increases raised the prices of goods and services. So, surprise! Inflation increased.

Since July, the central bank has left interest rates unchanged—the Fed’s current base rate is 5.5 percent, up from 3.25 percent a year ago.

Higher interest rates seem to have brought inflation down, but prices are rising nearly twice as fast as the Federal Reserve’s target of 2 percent annually.

No, oil, food, labor, metals, shipping, etc. scarcities moderated, so inflation moderated despite continuing interest rate increases.

We may have reached the limit of what the Federal Reserve can accomplish regarding taming inflation through monetary policy.

We reached that limit on the first day. Raising interest rates is inflationary. Period.

The federal government’s $33 trillion national debt and rising budget deficits are creating inflationary pressure in ways that remain underappreciated.

Economists ignore when the national “debt” and deficits rise without inflation (as often happens). But when we have inflation, the “debt” and deficit (which we have almost yearly) are blamed.

The big problem is that higher interest rates are helping curb inflation but worsening the federal government’s deficit.

No, the big problem is that while higher interest rates exacerbate inflation, the federal deficit can be directed toward inflation-curing programs, like Medicare for All and the elimination of FICA — both costs of doing business.

Writing at CNBC, Kelly Evans gets at the heart of this conundrum: “If we don’t quickly close the gap between spending and revenues, the debt load will keep growing, and interest costs will keep on rising, and the deficit will thus stay elevated, which grows the debt load even more.”

de Rugy

There is no debt load. It isn’t even debt. It’s deposits. They are not any sort of burden on the federal government or on the economy.

Those dollars are not owed by the federal government. The creditors all have been paid.

The deposits are owned by the depositors, who are paid off when deposits are returned to them.

So, what does that have to do with inflation?

As Reason contributor Veronique de Rugy, an economist at George Mason University, explains at National Review, there is an assumption built into monetary theory that says fiscal contraction—that is, smaller deficits—will necessarily follow a monetary contraction like the rising interest rates of the past year.

In other words, when central banks make it more expensive to borrow, they assume the politicians in charge of fiscal policy will respond by borrowing less.

But that hasn’t happened, and there is little indication that it will in the near future.

This assumption relies on federal politicians not understanding that spending by our Monetarily Sovereign federal government is not dollar-constrained. The government has the infinite ability to create and spend dollars on interest or anything else.

For that reason, the federal government does not borrow dollars. It does not need to obtain dollars from anyone.

The assumption also relies on the federal government spending less, which is recessionary. It is the false belief that recession is the cure for inflation when there is zero supporting evidence.

The federal budget deficit nearly doubled in the fiscal year that ended on September 30, and bigger deficits are expected in the next few years—in significant part because of the feedback loop between higher interest rates and rising debt costs.

That is not a “feedback loop” it is a tautology. The feedback loop is: Raise interest rates -> inflation –> raise interest rates again –> still higher inflation endlessly.

To fully get inflation under control, de Rugy says the country must experience a period of negative wealth effects—that is, a decline in demand driven by consumers choosing to rein in spending due to declining wealth.

Without her word salad, she says, “The country must experience a recession.” The Libertarians believe recessions cure inflation. Have they never heard of “stagflation”?

That’s hardly something worth cheering for, but it might be the only way to truly tame inflation—and it probably won’t happen until Congress curbs spending, too.

“The only way to get a reduction of total demand, which will ultimately rein in inflation, is for the fiscal authority to implement fiscal consolidation, hence creating a negative wealth effect,” writes de Rugy. “Absent that fiscal contraction, inflation will rise.”

Increased demand did not cause the sudden inflation of 2020. Demand didn’t suddenly appear overnight. But COVID made shortages occur overnight.

Changes to monetary policy have brought inflation down from last year’s near-record highs. Still, the monetary theory upon which that policy is built assumes that fiscal policy will finish the job by reducing deficits.

Congress, so far, doesn’t seem interested in cooperating—so expect prices to keep rising at an annoyingly fast rate.

You have just read the Libertarians’ false excuse for their cure not working. They claim the government’s massive spending (which has been in force for many years) suddenly decided to cause our inflation.

In short, because bleeding the patient with leeches didn’t cure his anemia, it must be that the patient is eating too much good food. Such is the nonsense that permeates economics today.

Rodger Malcolm Mitchell

Monetary SovereigntyTwitter: @rodgermitchellSearch #monetarysovereigntyFacebook: Rodger Malcolm Mitchell

……………………………………………………………………..

The Sole Purpose of Government Is to Improve and Protect the Lives of the People.

The Big Lie as expressed in a sign. The federal government doesn’t owe the so-called “debt,” and your family doesn’t owe any of it either.

That false belief — the Big Lie in economics — is so deeply implanted into the public’s brain that one seldom sees any discussion about its falsity.

The simple assumption is that debt is a burden, and more debt is a greater burden, and the federal government is deeply in debt, so the government should spend less and tax more to get rid of the debt burden.

And it’s all a gigantic, horrible, damaging lie, a Big Lie that locks the middle and bottom incomes in place while enriching the top.

That is the whole plan.

The very rich, who run America, send the Big Lie at us from all sides: The media, the politicians, and the economists, either via bribery or ignorance.

The rich bribe the media with advertising dollars or outright ownership. The rich bribe politicians with campaign contributions or promises of lucrative employment—the rich bribe economists with contributions to schools or employment at think tanks.

And those not bribed are influenced by constant repetition of the Big Lie, which addles their brains, reducing their ability to recognize obvious flaws in the Big Lie. Here are but three examples.

I. Why proposed GOP spending cuts hardly dent national debt,David Lightman

We assume David Lightman means federal, not national, debt. His reference is not to the nation’s debt but to the federal government’s.

But what he and virtually all others call “debt,” those Treasury bills, notes, and bonds aren’t debt. And contrary to popular wisdom, they aren’t “borrowing.”

We of the private sector (including state and local governments) borrow dollars to help us pay for things.

We don’t have the unlimited ability to create dollars, so we can run short. We are what is known as monetarily NON-sovereign.

You, I, and the local governments need a sovereign currency we can create instantly. We use the dollar.

By contrast, the U.S. federal government is Monetarily Sovereign. It created the first dollar and still creates the U.S. dollar from thin air merely by tapping computer keys.

The federal government cannot unintentionally run short of dollars. Even if the U.S. government stopped collecting taxes, it could continue creating and spending dollars forever.

Why does the government collect taxes if it doesn’t use them for spending?

To control the economy by taxing what it wishes to discourage and giving tax breaks to those it rewards and encourages.

To provide a certain demand for the dollar by requiring taxes to be paid in dollars.

To fool the public into believing that certain benefits are unaffordable, thus widening the income/wealth/power Gaps between the rich and the rest. This is how the rich become richer.

Why does the government issue Treasury bills, notes, and bonds if this isn’t borrowing and the government doesn’t need the money?The purposes of T-securities are:

To provide a safe, interest-paying place for the world to store unused dollars. This helps stabilize and secure the value of the dollar.

To help the Federal Reserve control interest rates.

To fool the public into believing the government must borrow dollars to pay for benefits given to the middle- and lower-income groups. This stifles the public’s objections to benefit cuts for the middle and lower-income groups and enriches the rich.

Why isn’t this borrowing? When you invest in a T-security, you open your account and deposit your dollars into it.

Think of this account as being like your bank safe deposit box. You, not the bank, own the contents of the box.

Similarly, you, not the federal government, own the contents of your T-security account.

The federal government neither uses nor even touches those dollars. That is why it’s not borrowing.

When your deposit reaches maturity, the government merely transfers the contents of your account to you. This is no more a burden on the federal government than is your bank allowing you to retrieve the contents of your safe deposit box.

That is why the contents of your safe deposit box are not your bank’s debt, and the contents of your T-security account are not the federal government’s debt.

Then why do so many people erroneously call T-securities “borrowing” and “debt”?

The Big Lie survives because of confusion and ignorance. The public needs to learn the differences between Monetary Sovereignty and monetary non-sovereignty. The people must also learn the differences between federalT-bills, T-notes, and T-bonds vs. private sectorbills, notes, and bonds.

The words look the same, but they are homonyms. They describe vastly different things, like the word “band” (a ring vs a musical group.)

A private sector bond transfers dollars from a lender’s account to a borrower’s account. The lender surrenders ownership of the dollars in exchange for the borrower’s bond.

The borrower then controls those dollars and uses them for his purposes. This is true even for state and local government bonds. The dollars go to the state and local government checking accounts at private-sector banks.

A T-bond transfers dollars from the bond owner’s checking account to the bond owner’s bond account. The bond owner never loses ownership of the dollars, and the government never touches the dollars.

The dollars are returned to the bond owner’s checking account upon maturity.

Private sector bonds denote borrowing and resultant debt. Treasury bonds indicate deposits, not debt. This confusion and ignorance help the rich to foster the Big Lie.

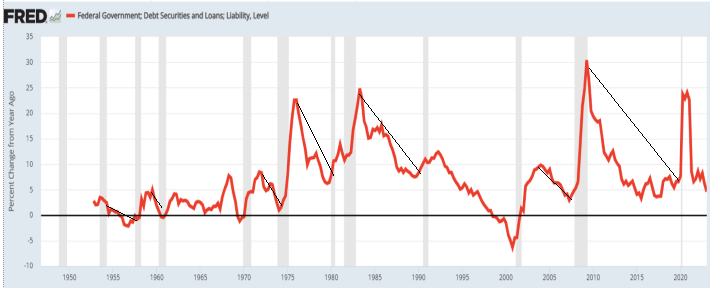

The relentless conservative drive to dramatically cut federal spending — a campaign that nearly caused a government shutdown and helped topple House Speaker Kevin McCarthy — wouldn’t do much to reduce the national debt anytime soon significantly.

There is zero reason to cut federal spending and a huge reason not to: When federal spending is cut or even increased too little, we have recessions and depressions.

Vertical gray bars denote recessions. The red line indicates changes in federal deficit spending. Recessions begin with reductions in deficits.

The above graph dramatically shows how reduced federal deficits lead to recessions cured by increased obligations.

The Federal Reserve calls the red line “Federal Government Debt Securities and Loans, Liability, Level” when it is more like “Deposits into T-Security Accounts.” Even the Fed gets it wrong.

Going back in time, here is what happens when the federal government runs a surplus (taxes exceed spending).

U.S. depressions tend to come on the heels of federal surpluses.

1804-1812: U. S. Federal Debt reduced 48%. Depression began in 1807. 1817-1821: U. S. Federal Debt reduced 29%. Depression began in 1819. 1823-1836: U. S. Federal Debt reduced 99%. Depression began in 1837. 1852-1857: U. S. Federal Debt reduced 59%. Depression began in 1857. 1867-1873: U. S. Federal Debt reduced 27%. The depression began in 1873. 1880-1893: U. S. Federal Debt reduced 57%. Depression began in 1893. 1920-1930: U. S. Federal Debt reduced 36%. Depression began in 1929. 1997-2001: U. S. Federal Debt reduced 15%. The recession began 2001.

Why do the rich want the government to run surpluses?

A surplus requires a tax increase and/or a spending decrease. Congress has provided tax loopholes so the rich seldom are affected by the tax increases paid for by the rest of us. Concerns about deficit rarely translate into a reduction of loopholes for the rich. A federal surplus effectively widens the income/wealth/power Gap between the rich and the rest

The spending decreases invariably come from benefits important to those who are not rich — Medicare, Medicaid, Social Security, and other poverty aids — further widening the Gap.

Surpluses cause depressions and recessions, forcing unemployment and providing rich business owners with a ready supply of desperate workers who will labor at starvation wages.

During recessions and depressions, the rich can maintain their lavish lifestyles while the rest of the populace suffers.

The push for drastic reductions in federal spending is expected to come up again once House Republicans pick a new speaker.

Whoever takes the gavel is expected to keep pushing for deep cuts. The Democratic-run Senate is unlikely to go along, but the GOP effort matters as a message to constituents about what Republicans are seeking.

The Republicans are the party of the rich. They are more likely to do the rich’s bidding than the Democrats, as evidenced by the divergent stances on federal spending.

The GOP initiative is also a reminder of why Congress is so stuck on adopting a budget.

When McCarthy, R-Bakersfield, agreed last month to a bipartisan plan to continue current spending for 45 days, angry conservatives plotted his successful removal.

The GOP is so in thrall of the rich it even demoted its House Speaker when he failed to end the government’s ability to spend.

The GOP budget plans range: For instance, aid that 702,000 Californians receive to buy healthy produce (through the Women’s, Infant and Children’s program WIC) would be dramatically cut.

So would the federal tax credit for electric vehicle charge equipment.

While such reductions collectively would save billions, nonpartisan budget analysts maintain that the cuts barely address the broader question of how to reduce the nation’s $33 trillion debt significantly.

Why is reducing the government’s “debt” (that isn’t a debt) an important question? Because it’s what the rich want, and their money talks.

Republican budget-cutters claim that their changes are a vital first step toward making the federal government more efficient and starting on a useful path to reducing the debt.

Reduced spending does not make government “more efficient.” Growing the economy is the government’s job, so reducing federal spending makes the government less efficient at its job.

Gross Domestic Product (GDP) is a common measure of the economy.

GDP = Federal Spending + Non-federal Spending Net Exports.

When Federal Spending increases, Non-federal spending also increases. When two terms of the equation increase, GDP increases.

Mathematically, there is no way for the government to do its job — growing the economy — by cutting spending.

“Stop bleeding money, stop racking up debt, defend the United States, stop social engineering, and just do your damn job as Congress.

I think that ought to be a pretty simple goal and a bipartisan goal,” said Rep. Chip Roy, R-Texas.

The key words are “stop social engineering.” This is right-wing speak for “cut Social Security, Medicare, Medicaid, and cut all benefits received by those who aren’t rich but don’t touch the loopholes that allow people like Donald Trump to pay $500 per yearin federal taxes.”

Struggling with debt,The federal budget had annual surpluses from fiscal 1998 to 2001, as a booming economy, a 1995 budget deal, and a 1993 tax increase helped revenue pour into the Treasury.

As you can see in the above graph, the recession of 2001 resulted from the federal surplus that began in 1998 and ended in 2002, when we emerged from the recession.

Since then, there have been nothing but annual deficits—$1.35 trillion in fiscal 2022—and the national debt has grown to $33 trillion.

David Lightman conveniently forgets that in the same period, Gross Domestic Product more than tripled, due to federal spending.

The deficit began climbing as Washington responded to the Sept. 11, 2001, terrorist attacks, pumping an estimated $2 trillion into wars in Iraq and Afghanistan. It spent to combat the Great Recession in 2009, delivered significant tax cuts in 2017, and passed huge COVID aid packages in 2020 to 2022.

Here is where the logic gets wacky. The government always spends to combat recessions. Federal spending is the one thing that cures recessions.

Why, then is it so hard for the debt nuts to understand that federal spending prevents recessions and grows the economy?

In fiscal 2022, the 12-month period that ended last September, the federal government spent $6.2 trillion. About two-thirds is called “mandatory spending,” meaning Congress does not have to vote on it. This includes Social Security benefits and Medicare payments.

That leaves only about one-third that Congress can control annually.

Wrong. Congress and the President have 100% control. They can, and should, expand Social Security and Medicare to include everyone in America, from birth to death, and for heaven’s sake, stop taxing Social Security benefits. That makes no sense from any standpoint.

Roughly half is defense, and the other half is domestic programs like education, transportation, energy, and others.

Most independent budget analysts agree that meaningful debt reduction involves costly entitlement spending. Social Security is estimated to be 11 years from insolvency. Medicare also faces financial problems in a few years.

You never will read a better expression of the Big Lie than the preceding paragraph. The phrase “meaningful debt reduction” should be changed to “harmful debt reduction.”

Neither Social Security nor Medicare can be “insolvent” or face “financial problems” unless that is what Congress and the President want.

The prevention and cure for those problems: A few touches of computer keys to provide money to these two vital programs — programs that benefit the “not-rich” far more than the rich.”

Those programs’ benefits are automatically funded and adjusted annually for inflation. Social Security benefits this year are up 8.7%, and next year are expected to climb about 3%.

The House’s GOP-run budget committee released a budget blueprint this summer that, while it proposes deep spending cuts, would not change Social Security. It does propose billions in Medicare savings through reforms.

Isn’t it clear why the budget cutters always use the word “reforms” when the honest word would be “cuts.”

Every conceivable “reform” for Medicare involves the Monetarily Sovereign federal government sending fewer dollars to the monetarily non-sovereign private sector.

As we repeatedly have experienced, reducing federal spending is recessionary or depressionary.

“Our budget protects and strengthens Medicare through policies that drive down out-of-pocket costs for seniors, stop overpayments, and enhance our healthcare workforce,” the budget says.

The budget does no such thing, neither protecting nor strengthening Medicare. To protect and strengthen:

Eliminate FICA, which pays for nothing. Instead pay for Medicare the same way the government pays for Congress, POTUS, SCOTUS and nearly every other federal program: Create new dolllars, ad hoc.

Eliminate Medicare deductibles.

Cover all the things that aren’t covered (dental, drugs, many procedures, etc.)

Cover every man, woman. and child in America, from birth.

Stop referring to the non-existent, fictional, phony Medicare Trust Fund.

It also urges the creation of a bipartisan commission to tackle the programs’ future. The commission would devise ways to get the programs on a sustainable financial path and help modernize the systems.

We don’t need another fake “bipartisan commission” that is ignorant (or feigns ignorance) of Monetary Sovereignty. Point #1 would get Medicare on a 100% sustainable path.

This sort of commission was arguably successful in the 1980s, when Social Security faced financial uncertainty.

It proposed what at the time were politically shaky reforms, including tax increases to fund the program and an increase in the age of eligibility.

The commission may have been “arguably” successful, but it wasn’t actually successful. It was a disaster.

The so-called “reforms” did nothing but shift the financial burden from the Monetarily Sovereign federal government (which never can run short of dollars) to the monetarily non-sovereign private sector (for which dollars always are scarce).

That could be called “successful” only in the eyes of the very rich. The Gap below widened, which is how the rich become richer.

Cuts and more cuts.The political focus is on spending cuts and taking incremental steps that are unlikely to get final approval. Once the House gets down to business again, those cuts will be the main topic of debate for some time.

Spending cuts always are harmful. By mathematical definition, they reduce GDP.

The House Budget Committee said in its blueprint that its plan can deliver a surplus by fiscal 2033. In addition to cuts, it assumes 3% economic growth per year, above what the nonpartisan Congressional Budget Office forecasts. More growth usually means more revenue and less spending.

The same surplus that repeatedly caused depressions in the past 200 years? Or Clinton’s surplus that “only” caused a recession?

Do these people not understand simple algebra? GDP=Federal Spending + Nonfederal Spending + Net Exports.How will federal spending cuts increase GDP?

The budget also reverses some of the plans Democrats recently approved. Outlays for green energy and technology“should have been targeted towards traditional roads and bridges, not wasteful initiatives,” the committee said, listing several programs it found excessive.

The committee claims that green energy and technology to save our planet are “excessive” and “wasteful initiatives”? What planet do these people live on?

Among them: $7.5 billion for electric vehicle charging stations, $5 billion for electric and low emissions buses and ferries and $10 million for career skills training to install energy efficient building technologies.

The Republicans prefer CO2-emitting, pollution-causing, gas-guzzling cars, busses, and ferries. And of course, they don’t want “energy efficient building technologies”.

Rep. Marjorie Taylor Greene, R-Georgia, proposed the reduction in Pentagon Secretary Austin’s salary, arguing “he is destroying our military.” She cited the chaotic American withdrawal from Afghanistan, saying Austin “failed America.”

If Marjorie Taylor Greene speaks for the GOP, need I say more?

Some analysts warn that such cuts have the potential to harm the people who need help the most.

Not “potential” harm; real harm to real people.

Cutting Women, Infants and Children program funds to buy healthy produce would leave recipients with roughly $11 to $15 monthly to spend, the left-learning Center on Budget and Policy Priorities estimates.

It said the cuts would affect an estimated 702,000 toddlers, preschoolers, and pregnant, postpartum, and breastfeeding California participants in the program.

This is exactly what happens when politicians value the federal government’s finances (which are infinite) more than personal finances (which are limited).

Republicans have argued that strengthening work requirements in assistance programs will help motivate people to work, reducing the programs’ cost and helping the economy as people pay more taxes and increase their spending.

“Motivate people to work” follows the right-wing claim that the poor are lazy takers who would rather wallow in their poverty than work, while the rich are industrious givers who labor so hard on their yachts, private planes, gated communities, and chauffeur-driven limos.

===================================

Then there was this example of economics ignorance from Chartr, the web site that provides graphs for many different subjects:

Again, Uncle Sam never borrows its own sovereign currency, the U.S. dollar. It creates all the dollars it needs

However, higher borrowing costs have changed the game. Indeed, forecasts from the Congressional Budget Office project that the majority of future government deficits will not be down to net new spending, but rather paying the interest on what’s already owed (some $33 trillion), with deficits expected to rise as a share of GDP for the coming decades.

“Living beyond its means”is another version of the Big Lie, this one popularized by economically dense Democrat Barach Obama. The federal government has infinite means, so cannot live beyond it.

The deficit/GDP fraction is a popular, but meaningless number. It demonstrates nothing about the federal government’s financial health or its ability to pay its debts (which is infinite) and predicts nothing about the future.

You can visit a related website, “Debt to GDP Ranking by Country” and decide for yourself what the fraction tells you about anything at all.

Would the author of this article prefer to be owed money by Zambia (with a 119% score) rather than by the United States (with an “inferior” 128% score).

==========================================

And finally, to demonstrate how the Big Lie is everywhere, we come to the New York Times:

Higher rates stoke growing chorus of deficit concernsNYSE on June 13. The interest rate on 10-year Treasury bonds has spiked since July. By Jeanna Smialek, Jim Tankersley and Joe Rennison The New York Times

The U.S. government’s persistent budget deficit and growing debts were low on Wall Street’s list of worries when interest rates were at rock bottom for years.

But borrowing costs have risen so sharply that it is causing many investors and economists to fret that the United States’ big debt pile could prove less sustainable.

In 1940, The Gross Federal Debt Held by the Public totaled $41 Billion and was called a “ticking time bomb.” Now, it’s somewhere near $31 TRILLION.

Yet the bomb still ticks, and we still sustain, though the NY Times continues to clutch its pearls. Must be a slow tick.

The exact cause of the latest run-up in Treasury rates is hard to pinpoint. Many economists say a combination of drivers is probably helping to drive it — including strong growth, fewer foreign buyers of America’s debt, and concerns about debt sustainability in and of itself.

Gee, does the Times think “the run-up in Treasury rates” might be related to the Fed’s repeated rate increases?

That old worry about “foreign buyers” not buying America’s “debt” should be retired. It’s complete nonsense.

The federal government is not in debt and does not rely on foreigners to provide it with its own sovereign currency, the U.S. dollar. It creates all the dollars it needs by touching computer keys. No limit.

What’s clear is that if rates remain elevated, the federal government will need to pay investors more interest in order to fund its borrowing.

“Paying investors more” is a good thing. It adds to GDP. But, since the U.S. federal government never borrows dollars, investors can’t “fund borrowing.”

The nation’s gross national debt stands just above $33 trillion, more than the total annual output of the U.S. economy. The debt is projected to keep growing both in dollar figures and as a share of the economy.

The fact that the non-existent “debt” (i.e., deposits in Treasury security accounts) is greater than GDP reveals zero about the economy. The oft cited Debt/GDP fraction is meaningless.

It’s like saying the Chicago Cubs had more runs than the Bears had field goals. Same “meaningful” comparison.

While the climbing cost of holding so much debt is stoking conversations among economists and investors about the appropriate size of the government’s annual borrowing, there is no consensus in Washington for deficit reduction in the form of either higher taxes or big spending cuts.

There’s no consensus because both higher taxes and spending cuts would injure the economy.Both take dollars from the economy and give them to the federal government, which promptly destroys them.

Should you cure anemia by applying leeches or by cutting wrists? No consensus there, either.

Still, the renewed concern is a stark reversal after years in which mainstream economists increasingly thought that the United States might have been too timid when it came to its debt: Years of low interest rates had convinced many that the government could borrow cheap money to pay for relief in times of economic trouble and investments in the future.

Our Monetarily Sovereign federal government has the infinite ability to “pay for relief in times of economic trouble,”no matter what interest rates have been. It does not borrow, cheap money or otherwise.

As always, the media confuse Monetary Sovereignty with monetary non-sovereignty. The former cannot run short of money; the latter can and often do.

“How big a problem deficits are depends — and it depends very critically on interest rates,” said Jason Furman, an economist at Harvard and former economic official under the Obama administration.

Oops, another Obama economist. That tells us all we need to know. What is it with Harvard that their economists believe the federal government borrows and needs to worry about the interest it pays?

We’ll finish with a lovely compilation of economic ignorance, widely promulgated, widely believed, and widely wrong.

Furman had previously estimated that the growing cost of interest on federal debt would remain sustainable for some time, after factoring in inflation and economic growth. But now that rates have climbed so much, the calculus has shifted, he said.

The deficit has been sustainable since — uh, since the federal government had the power to create laws, and laws had the power to create dollars.

The deficit will continue to be sustainable forever. The U.S. government cannot unwillingly run short of dollars. Not now. Not tomorrow. Not ever.

Higher interest rates are a leading cause, along with surprisingly weak tax collections, of what the Congressional Budget Office projects will be a doubling of the federal budget deficit over the last year.

The deficit, when properly measured, grew from $1 trillion in the 2022 fiscal year to an estimated $2 trillion in the 2023 fiscal year, which ended last month.

This means the federal government will pump about two trillion growth dollars into the economy. And this is a bad thing??

If borrowing costs climb further — or simply remain where they are for an extended period — the government will accumulate debt at a much faster rate than officials expected even a few months ago.

The federal government does not owe the misnamed “debt,” and even if it did, it could pay it all instantly.

The Big Lie in economics is that the federal government can run short of its sovereign currency. The Lie is repeated endlessly by nearly every information source — media, politicians, and economists.

The facts as explained by Monetary Sovereignty, are overwhelmed by the sheer volume of lies being promulgated from everywhere.

At long last, is there any one out there who has world standing plus even a modicum of knowledge about economics and Monetary Sovereignty? Is so, would that person please debunk the false notions that federal finances resemble personal finances and that federal benefits are “unsustainable”?

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The red line is Inflation, i.e., the year-to-year changes in prices. The blue line is the year-to-year changes in federal deficits.

If federal deficit spending caused inflation, you might expect these lines to be essentially parallel. If deficit spending did not cause inflation, you would expect the lines to look exactly like they look.

If you were a real scientist whose hypothesis was that federal deficit spending causes inflation, you immediately would discard that hypothesis and look for something else, perhaps something like this:

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.

When supply cannot meet demand, prices go up. That’s basic.

The green line is the year-to-year change in oil prices. Because oil is a fungible product, its price changes are based on supply changes. The price goes up when oil is scarce and goes down when oil is plentiful.

A real scientist would notice that although there seems to be no relationship between federal deficits and inflation, there is a robust relationship between oil scarcity and inflation.

Sadly, despite having massive data available, economists are not scientists. They are believers in a religion where dogma cannot be questioned.

Look at any inflation in world history, from Germany to Argentina to Zimbabwe, etc. Every inflation has been caused by scarcity of critical products or services, especially oil and food.

When supply cannot meet demand, prices go up. That’s basic.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.

What changed suddenly in 2020 to cause inflation to go from an average below 2% to zoom above 8%? Did demand suddenly rise in that year?

No, it was COVID-related scarcities. Like all inflations worldwide and throughout history, our current inflation is caused by shortages.

The current inflation rightfully could be called the “COVID inflation.” Because of COVID, we had shortages of oil (exacerbated by the Saudis), food, etc.