The debt hawks are to economics as the creationists are to biology. Those, who do not understand Monetary Sovereignty, do not understand economics. If you understand the following, simple statement, you are ahead of most economists, politicians and media writers in America: Our government, being Monetarily Sovereign, has the unlimited ability to create the dollars to pay its bills.

======================================================================================================================================================

The Tea (formerly Republican) Party wants lower taxes (good) and less federal spending (bad). The Tea Party hero of the day, Rand Paul is an ardent follower of Ayn Rand. Yes, that Ayn Rand, the one who believes the rich are gods who deserve more, while the poor are leeches who deserve less.

He has couched his beliefs in Tea appeals to tax cuts, patriotism and freedom from government interference, as in freedom from health care, freedom from military protection, freedom from good roads and safe bridges, freedom from healthful medicines and food, freedom to discriminate against gays, freedom from safe banks, freedom from a good education, freedom from clean air, freedom from energy saving, freedom from police protection, freedom from Social Security, freedom from safe air travel, and the many other freedoms we so ardently desire.

But the Tea night is ending, and the dawn of realization has begun.

Washington Post: by Jon Cohen and Dan Balz, Wednesday, April 20, 2011. “Despite growing concerns about the country’s long-term fiscal problems and an intensifying debate in Washington about how to deal with them, Americans strongly oppose some of the major remedies under consideration, according to a new Washington Post-ABC News poll.

“The survey finds that Americans prefer to keep Medicare just the way it is. Most also oppose cuts in Medicaid and the defense budget. More than half say they are against small, across-the-board tax increases combined with modest reductions in Medicare and Social Security benefits. Only President Obama’s call to raise tax rates on the wealthiest Americans enjoys solid support.”

Now, as we Americans awaken to the fact that the Tea/Republican plan to reduce federal spending amounts to the reduction of all the things we want, as well as benefitting those hated rich people, somehow President Reagan’s “government is the problem” mantra doesn’t seem so attractive.

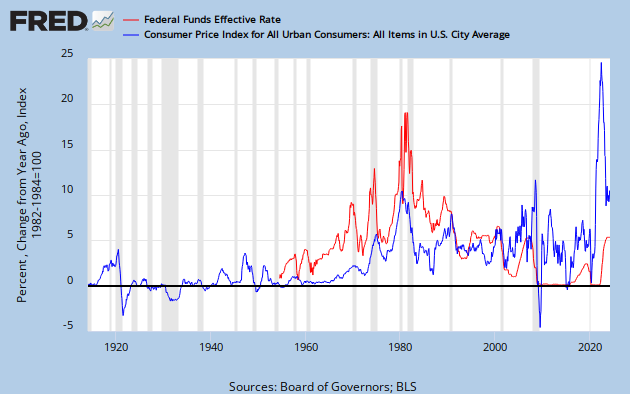

Of course, increasing taxes on anyone, rich or poor, is a typically bad, Democratic idea. All taxes remove money from the economy, and removing money from the economy causes recessions and depressions. Further, this removal of money always hurts the poor more than it hurts the rich. See: Taxing the rich hurts the poor.

That said, I favor Obama’s plan to the Tea/Republican “plan.” Before you faint, let me explain. Both plans are equally ignorant in that they begin with the false assumption federal deficit spending must be reduced. In the Economics Common Sense and Knowledge race, both parties come in last.

However, they have convinced the innocent public of this falsehood, which forces on us a lesser-of-two-evils choice, and Obama’s plan is less evil. Why? Because raising tax rates on the rich not only will satisfy the jealous public, and not only will preserve the various benefits of federal spending, but in reality, will not collect much more in taxes.

We already have learned that higher taxes beget better tax “loopholes.” Remember, rich people know how to bribe politicians better than do poor people. So as those rates rise, the deductions will rise, too. A (for instance) 10% increase in tax rates on those making more than $250K per year, will not net a 10% increase in taxes collected from the rich – maybe not even 5%. Depending on the effectiveness of the bribery, a tax rate increase actually could net less money, because better deductions could be worth more than the marginal rate.

Bottom line, the Obama plan will make everyone happier. The poor will benefit; the rich won’t care and the economy will be less injured by losing money.

As an aside, if I were running for office, my opponent would tell the voters I voted in favor of tax increases, and this is why the politicians find themselves surrendering to their party, rather than thinking.

Rodger Malcolm Mitchell

http://www.rodgermitchell.com

![]()

==========================================================================================================================================

No nation can tax itself into prosperity, nor grow without money growth. It’s been 40 years since the U.S. became Monetarily Sovereign, and neither Congress, nor the President, nor the Fed, nor the vast majority of economists and economics bloggers, nor the preponderance of the media, nor the most famous educational institutions, nor the Nobel committee, nor the International Monetary Fund have yet acquired even the slightest notion of what that means.

Remember that the next time you’re tempted to ask a dopey teenager, “What were you thinking?” He’s liable to respond, “Pretty much what your generation was thinking when it screwed up the economy.”

MONETARY SOVEREIGNTY