We Americans are accustomed to puffing out our chests and claiming that we are the greatest nation on earth. We probably have the greatest fighting force (or did until Trump appointed a clown to lead it), but otherwise we have fallen far from the top.

(And please no smart-ass “Love it or leave it” comments. If that’s your best, you are a FOX News viewer without the intelligence or honesty to understand facts. So stop reading now, and get the rest of your information from Donald Trump.)

Here is an example of the greatest nation on earth:

By Sriparna Roy. March 12, 202612:03 AM EDT Updated March 13, 2026

Unlike state and local governments, the U.S. federal government never can run short of dollars. Even if it stopped collecting taxes, while tripling its spending, it still would not run short of money.

March 12 (Reuters) – Roughly one-third of Americans cut back on food, utilities or other daily expenses to pay for healthcare last year, research from the West Health-Gallup Center showed on Thursday, as steeper prices and rising living costs hit households.

A nationally and state-representative survey of nearly 20,000 U.S. adults in all 50 states and in the District of Columbia, conducted from June to August 2025, found that 33% of respondents had made at least one trade-off in daily expenses to pay for healthcare.

This was far more common among Americans who do not have health insurance, with 62% of those surveyed saying they have made at least one sacrifice to pay for healthcare, including 32% who had to borrow money and 24% who had prolonged their current medication.

Among those with insurance, close to three in 10 have made at least one sacrifice, the survey found.

Most Americans with private health insurance are paying higher premiums and steeper out-of-pocket costs in 2026, including millions of people in the government-subsidized Affordable Care Act plans in which extra COVID pandemic-era subsidies have expired.

One-third of Americans had to cut back on food, utilities, or daily expenses to pay for healthcare? The greatest nation on earth??

Hah. Gimme a break.

It’s not that the “greatest nation on earth” can’tafford healthcare. It’s simply that the right-wing government of the greatest nation on earth doesn’t want to pay for it because …uh…it would benefit the poor, whom everyone knows are lazy, good-for-nothings who want everything free. Right?

Oh, and then there’s the right-wing excuse that aiding the poor is “Socialism” while aiding the rich (via tax dodges) is good old capitalism.

Here is what some capitalists say about that:

Fed Chair Greenspan

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Fed Chair BernankeFed Chair Beardsley Rummel

Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.

Former Federal Reserve Chairman Beardsley Ruml: “The necessity for a government to tax in order to maintain both its independence and its solvency is true for state and local governments, but it is not true for a national government. The public purpose which is served should never be obscured in a tax program under the mask of raising revenue.”

Federel Reserve Chairman Jerome Powell stated, “As a central bank, we have the ability to create money digitally.

Former Secretary of the Treasury Paul O’Neill

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.” You can find it in their publication titled “Why Health Care Matters and the Current Debt Does Not”

Former Secretary of the Treasury Paul O’Neill: “I come to you as a managing trustee of Social Security. Today we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.”

Former President of the ECB and Prime Minister of Italy Marie Draghi

The European Central Bank (ECB), like the U.S. government, is Monetarily Sovereign. Press Conference: Mario Draghi, President of the ECB, 9 January 2014 Question: I am wondering: can the ECB ever run out of money? Mario Draghi: Technically, no. We cannot run out of money.

Paul Krugman, an award-winning economist

Paul Krugman (Nobel Prize–winning economist): “The U.S. government is not like a household. It literally prints money, and it can’t run out.” — Numerous op-eds/blog posts

Hyman Minsky (Economist, key influence on MMT) “The government can always finance its spending by creating money.”

Eric Tymoigne (Economist) “A sovereign government does not need to collect taxes or issue bonds to finance spending. It finances directly through money creation.”

Yes, though the compulsive liars of FOX News may disagree, true experts will tell you that the U.S. government has the unlimited capacity to finance healthcare insurance for every man, woman, and child in America, while still having sufficient funds for any future wars that Presidents may initiate to distract voters from the latest scandals.

Then, in a last-ditch effort to take dollars from the pockets of the poor, the right wing will falsely claim that “too much” federal spending causes inflation. (“too much” is any amount that helps the poor but doesn’t enrich the President’s family).

You will notice that there always is enough money to start wars and to prosecute enemies. As this is being written, the Conservatives request an additional $200 billion to fight an unnecessary war, which will subsequently require billions more to replenish our depleted munitions.

Those brave fighters won’t be deterred by the loss of human life or myths about inflation.

The next time you are forced to choose between paying for health care vs. food, clothing, or school for your kids, do remember to thank the Republican Party and President Trump, and name another street after him.

One would hope that historians, and especially economists, would understand the differences between federal financing (Monetary Sovereignty) and personal financing (monetary non-sovereignty).

Sadly, any such hopes seem dashed by this MSN article.

The national debt has grown to $38 trillion. The United States’ national debt, currently standing at $38 trillion and exceeding 120% of annual economic output, demands action, experts warn.

The article lists and describes the panic-stricken statements from “experts” about the federal debt from 1940 through today. In 1940, it was $43 billion— roughly 44% of GDP at the time.

As debt and the debt-to-GDP ratio rose, the economy grew and prospered. Yet, the panic has continued, and the screams have become ever more strident. Now, the so-called “debt” (that isn’t really debt; it’s deposits) has grown nearly a thousand-fold, the sky has not fallen, and we continue to be pummelled with articles like Nick Lichtenberg’s.

Having learned absolutely nothing in the past eighty-five (!) years, the experts continue to panic and scream, hoping you, too, will panic and scream. For your amusement, and perhaps sorrow, here’s the latest.

The nonpartisan Peter G. Peterson Foundation gathered a series of distinguished national economists and historians from outside the foundation in a collection of essays published Thursday.

They analyzed risks to U.S. economic strength, dollar dominance, and global leadership.

Ah, yes, distinguished national economists and historians — distinguished by their misunderstanding of the difference between federal government financing vs. state/local government financing. The former is Monetarily Sovereign; the latter is monetarily nonsovereign — two different animals.

The experts also explored the national debt’s impact on interest rates, inflation, and financial markets, with some characterizing this moment in history as a crisis.

A crisis of ignorance.

Collectively, they argue that the nation is operating under a dangerous fiscal gamble.

Assessing the mounting liabilities delivered a stark judgment: “In simpler terms, we are guilty of spending our rainy-day fundin sunny weather.” Meaning, the government has little “dry powder” left to fund a major military effort or stimulate the economy during a crisis.

And what exactly is our “rainy-day fund”? How much is it? Where is it stored? And that “dry powder,” how much is it and where is it stored?

Feel free to ask Council on Foreign Relations President Emeritus Richard Haass and NYU professor Carolyn Kissane. However, they won’t know, because the fund and powder do not exist, not in real or even metaphorical terms.

Well, in one sense, they do exist in the Monetary Sovereignty of the U.S. government, which has the infinite ability to create dollars (and dry powder) merely by pressing computer keys.

Who says so? A few real experts, not the self-proclaimed, self-aggrandized, overly anointed kind:

Former Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Fed Chairman Jerome Powell: “As a central bank, we can create money digitally.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Former Secretary of the Treasury Paul O’Neill: “I come to you as a managing trustee of Social Security. Today, we have no assets in the trust fund. We have promises of the good faith and credit of the United States government that benefits will flow.”

Nobel Prize–winning economist Paul Krugman: “The U.S. government is not like a household. It literally prints money, and it can’t run out.” — Numerous op-eds/blog posts.

Economist Hyman Minsky: “The government can always finance its spending by creating money.”

Economist Eric Tymoigne: “A sovereign government does not need to collect taxes or issue bonds to finance spending. It finances directly through money creation.”

Now, back to the fun:

The debt crisis has reached a critical threshold. The U.S. now spends approximately $1 trillion annually servicing its debt—a figure that surpasses its defense spending.

And why is spending more on interest than on defence significant? It isn’t. Spending is spending. All federal spending adds to GDP. The phrase was just a desperate attempt to shock you. It shouldn’t.

The federal government can pay infinite interest, and the more it pays, the healthier the economy is. Here’s the evidence:

Gross Domestic Product = Federal Spending + Nonfederal Spending + Net Exports

Get it? The more the federal government spends, and the less it taxes (i.e., the greater the deficit), the more Gross Domestic Product grows.

What would be truly shocking is if the federal debt declined. History shows us examples of that decline:

Every Depression in U.S. History Came On the Heels of a Reduced Federal Debt

1804-1812: U. S. Federal Debt reduced 48%. Depression began in 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began in 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began in 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began in 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began in 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began in 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began in 1929.

1997-2001: U. S. Federal Debt reduced 15%. The recession began in 2001.

Economist Heather Long wrote that the 2020s are “fast becoming the era of big permanent deficits” with annual budget gaps projected to remain high (around 6% of GDP) even though unemployment is low, a startling departure from U.S. historical norms.

Let us pray for an “era of big permanent deficits.” The alternative is small deficits or surpluses (which lead to recessions or depressions).

When deficit growth decreases, we have recessions (vertical gray bars), which are cured by increases in deficit growth.

Economists warn that solutions that worked in the past—such as the post-World War II debt reduction or the 1990s surpluses—are unavailable today. Economist Barry Eichengreen explained that the debt’s steep decline after World War II was supported by a highly favorable interest-rate-growth-rate differential (low real interest rates and fast GDP growth). Likewise, the 1990s reduction was fueled by the “peace dividend,” enabling deep cuts in defense spending. “None of these facilitating conditions is present today.”

The only necessary “facilitating conditions” for economic growth are increased federal deficit spending — exactly the thing that creates economic growth.

The Threat to National Security and the Dollar

Eichengreen, for his part, noted that current security threats from Russia, Iran, and the South China Sea create pressure for defense spending increases, not cuts.

Defense spending increases, if they occur, will grow the economy.

Compounding the problem is political polarization, which is cited as the most robust determinant of unsuccessful fiscal consolidation.

“Successful fiscal consolidation” is economics-speak for reduced deficit spending, which causes recessions and depressions.

With major entitlement programs politically protected, this fiscal gridlock leaves raising additional revenueas the most viable path, given that the United States is a low tax-revenue economy compared to its peers.

As the real economists — Greenspan, Bernanke, and Powell — stated above, the federal government neither needs (nor even uses) revenue. It creates all its spending money in three easy steps:

Congress votes.

The President signs

Federal employees press computer keys

And voila, all the millions and billions of dollars the federal government spends are magically created. No tax dollars are involved. It’s all bookkeeping notations.

The debt is framed not just as a financial strain but as a direct threat to security. Haass and Kissane emphasized that money spent on borrowing is “money not available for more productive purposes, from discretionary domestic spending to defense,” a classic case of crowding out.

The above statement is ridiculous on its face, for two, what-should-be-obvious reasons:

The federal government has the infinite ability to create dollars and,

The dollars the government spends go into the economy, where the private sector can use them for productive purposes.

There never has been “crowding out,” and never will be. The government can’t run short, and every dollar spent is added to the economy, boosting spending.

Other underfunded programs—including cybersecurity and public health—hollow out internal capacities that protect the homeland.

It is unclear how an entity with the unlimited ability to create dollars can be “hollowed out,” nor is it explained how an economy that receives more dollars is being “hollowed out.”

I imagine there is no explanation simply because it cannot be explained. It is utter nonsense.

The crisis was characterized by Haass and Kissane as moving in “slow motion,” the most challenging type for democratic governments to address effectively. Avoiding a sudden “cliff scenario” in which bond markets crash, experts argue, is not avoiding the crisis itself; they added: “The day will come when the boiling water finally kills the frog.”

Ah, yes, “slow motion” because it isn’t happening yet, even though we’ve been predicting it for 85 years. And that darn old frog simply doesn’t understand that it’s supposed to have died by now.

The institutional integrity undergirding the U.S. dollar is also at risk. Historian Harold James wrote that he sees the situation as “the middle of a very dangerous experiment with the U.S. dollar, and with the international monetary system, whose fundamental driver is a fiscal gamble.” Erosion of the rule of law, accountability, and transparency raises the “specter of political risk in U.S. sovereign bond markets,” making it harder to maintain dollar dominance. Disturbingly, the potential for political interference in institutions, such as the Federal Reserve or the tampering with national statistics—as seen in Argentina’s cautionary tale—further erodes confidence.

Historian Harold James probably doesn’t realize it, but he’s not talking about the federal debt. Instead, he’s talking about dictator wannabe Donald Trump, and a cowardly do-nothing Congress, plus the morally compromised right wing of the Supreme Court.

They are the ones — not the essential debt growth –who are creating and countenancing the fall of the American economy, .

James’ colleague, Princeton politics professor Layna Mosley, cited the famous comment from the French statesman Valéry Giscard d’Estaing, who described the “exorbitant privilege” the U.S. enjoyed on the back of the dollar. She noted that, by virtue of the global role of the U.S. dollar and the U.S. leadership of the international financial system, the U.S. government has been able to borrow significant amounts on generous terms. But now, government actions and policy generate uncertainty and instability and “undermine the rules-based liberal international order from which the U.S. benefited greatly.”

Sounds frightening, except for one small detail. The U.S. federal government does not borrow.

As the representative of the St. Louis Fed correctly stated (above), “the government is not dependent on credit markets to remain operational.”

The federal government creates all the dollars it spends just by pressing computer keys. The government neither needs nor uses any income, whether from borrowing or taxes.

Rather than providing spending money, the purposes of federal taxes are to:

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to what it wishes to reward.

Assure demand for the U.S. dollar by requiring taxes to be paid in dollars.

The purposes of Treasury securities (T-bills, T-notes, T-bonds) are to:

To help the Fed control interest rates by providing a “floor” rate.

To provide dollar holders with a safe, interest-paying place to store unused dollars, which supports the value of dollars.

This loss of credibility empowers bond markets, and their displeasure can lead to sudden, painful economic consequences for everyday Americans through surging mortgage and loan interest rates. Haass and Kissane turned to another metaphor, saying the situation is akin to “forgoing fire or automobile insurance just because the odds are you will not suffer from a fire at home or an accident on the road.”

The above metaphor is a backward attempt to explain why all those “doomsday” predictions have been wrong. The better advice would be: “Don’t bet your life savings on misinformation from the media, the politicians and many economists, because for 85 years, you’d have lost.”

Learn from experience. The only loss of credibility will be endured by the noted historians and economists who, once again, as they have for the past eighty-five years, will be forced to come up with excuses for why the economy does not obey their dire predictions.

Here is a scam that even those who understand Monetary Sovereignty will fall for:

News article: President Donald Trump says the government might start cutting checks again, but this time, not for COVID-19 relief or tax refunds. Instead, the money could come straight from the tariffs his administration has slapped on foreign imports.

In his words, “We have so much money coming in, we’re thinking about a little rebate.”

And by “little,” he means from a pool of more than $100 billion in tariff revenue already collected this year.

Sounds good, right? Some of the dollars those tariffs are taking out of your pocket will come back in the form of rebates. What could be wrong with that?

This illustration actually exaggerates the impact of tariffs on the federal government’s ability to spend. The ocean doesn’t contain an infinite amount of water, but the government can create an infinite number of dollars.

It’s 100% misleading.

There is no “pool of tariff revenue.” The federal government has infinite dollars.

Every dollar that comes to the government disappears into an infinite pool of funds.

Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.

Fed Chairman Jerome Powell stated, “As a central bank, we have the ability to create money digitally.

The St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

If Trump wanted to send a “rebate” to Americans, he could do it tomorrow, simply by having his acquiescent Congress vote for it.

There, quite literally. is no limit to how much the federal government can send to anyone and everyone, today, tomorrow, or any time.

Then there is this nonsense:

The US government is raising record-high revenue from tariffs, thanks to President Donald Trump’s embrace of new import levies. The White House may exaggerate the potential, but independent budget analysts agree the new tariffs may bring trillions of additional dollars into government coffers over a decade.

The United States government has the potential to collect US$2trn or more in tariff revenue for its coffers in the next decade from President Donald Trump’s new import levies, according to economic and budget researchers.

Since his second presidential term began in January, Trump has ordered a series of new import tariffs on a global, per-country and per-item basis. Among the president’s stated goals is to raise enough money to offset, or even eliminate, federal income taxes.

The independent analyses do not envision any possibility that tariffs, even under the highest plausible outcome, can replace the income tax. The US collects approximately US$2trn in income taxes annually.

There are no “coffers.”

This situation is similar to the ocean boasting about a tiny thimbleful of water being added to it.

However, that analogy isn’t quite accurate because even the ocean doesn’t have an infinite supply of water, while the U.S. government has an unlimited capacity to create dollars.

The government has the power to create a trillion, trillion, trillion dollars today, if it chooses to, simply by pressing a computer key.

Therefore, the government does not need to “raise” money to eliminate federal income taxes; it could eliminate those taxes immediately.

And this:

Howard Lutnick: “The tariff revenues are amazing — $700 BILLION a year. That’s just net new money the government never had before. You take that for ten years, that’s $7 TRILLION.”

An abject lie. The federal government has infinite money. The mythical $7 TRILLION would be taken from the private sector and disappear.

The purpose of federal income taxes is not to supply the federal government with money. Instead, the purposes of federal taxes are:

To control the economy by taxing what the government wishes to discourage (Examples: “Sin taxes on cigarettes, liquor, etc.) and by giving tax breaks to what the government wishes to reward (Examples: Tax breaks for charitable contributions, and tax loopholes for the rich.)

To assure demand for the U.S. dollar by requiring dollars to be used for tax payments.

Unlike state and local governments, which rely on tax dollars, the federal government does not need or use tax revenue.

Rather than taking tariff dollars from the public, the federal government should simply vote to eliminate poverty by funding comprehensive, no-deductible health care insurance and generous Social Security benefits for every man, woman, and child in America.

No, this wouldn’t cause inflation any more than Trump’s so-called “rebates” would. Inflation is caused by a shortage of essential goods and services, and it can be alleviated through federal spending to address those shortages.

At long last, when will the media, the politicians, and the economists acknowledge the federal government’s infinite supply of dollars?

In economics, as in most other fields, ignorance leads to failure and to further ignorance. Nowhere is this more evident than in discussions about the so-called “national debt,” which is neither national nor debt.

The following article appeared in the June 2, 2025 Florida Sun Sentinel:

Can Trump manage national debt?Several investors, GOP senators and Musk have doubtsBy Josh Boak Associated Press

WASHINGTON —President Donald Trump faces the challenge of convincing Republican senators, global investors, voters and even Elon Musk that he won’t bury the federal government in debtwith his multitrillion-dollar tax breaks package.

The response so far from financial markets has been skeptical as Trump seems unable to trim deficits as promised. The overall national debt stands at more than $36.1 trillion.

Mr. Josh Boak seems to misunderstand the difference between federal financing and personal financing. He insists our Monetarily Sovereign federal government is at risk of being “buried in debt.“

The federal government is Monetarily Sovereign. That means it never can run short of dollars. It could continue spending at its current rate, or even at three times its current rate, forever.

Your city, county, and state can be buried in debt. Your business can be buried in debt. You can be burning in debt, as can I. We are monetarily non-sovereign. We cannot create unlimited dollars.

But the U.S. federal government cannot be “buried in debt.” Not now. Not ever.

Why would anyone want to reduce annual deficits? The government never can run short of dollars, and federal deficits are essential for economic growth.

The most common measure of economic growth is Gross Domestic Product (GDP). The formula for GPD is:

GDP = Federal Spending + Nonfederal Spending + Net Exports

“Nonfederal” is the private sector.

Simple algebra shows that cuts to Federal Spending reduce economic growth. Federal Spending increases GDP directly, but also tends to increase Nonfederal Spending by sending dollars into the private sector, which spends them.

“All of this rhetoric about cutting trillions of dollars of spending has come to nothing — and the tax bill codifies that,” said Michael Strain, director of economic policy studies at the American Enterprise Institute, a right-leaning think tank.

It is surprising that someone titled “Director of Economic Policy Studies” does not understand the fundamentals of federal finance. Mr. Strain appears to misunderstand the differences between monetary sovereignty and monetary non-sovereignty.

“There is a level of concern about the competence of Congress and this administration, and that makes adding a whole bunch of money to the deficit riskier.”

The White House has viciously lashed out at anyone who has voiced concern about the debt snowballing under Trump, even though it did exactly that in his first term after his 2017 tax cuts.

Trump often attacks anyone who disagrees with him, despite his limited understanding of economics.

White House press secretary Karoline Leavitt opened her briefing Thursday by saying she wanted “to debunk some false claims” about his tax cuts.

Leavitt said the “blatantly wrong claim that the ‘One, Big, Beautiful Bill’ increases the deficit is based on the Congressional Budget Office and other scorekeepers who use shoddy assumptions and have historically been terrible at forecasting across Democrat and Republican administrations alike.”

Here is the irony. Rather than imitating Trump by lying, insulting, and criticizing, Leavitt should have stated, “Yes, we increase the deficit because it stimulates economic growth. We draw from the federal government, which has an infinite supply of dollars, and give support to the economy, specifically, the private sector.”

In summary, she apologizes for unintentionally doing the right thing while believing it to be wrong, and then she denies that she is doing it.

House Speaker Mike Johnson piled onto Congress’ number-crunchers Sunday, telling NBC’s “Meet the Press”: “The CBO sometimes gets projections correct, but they’re always off, every single time, when they project economic growth. They always underestimate the growth that will be brought about by tax cuts and reduction in regulations.”

Tax cuts bring about growth because they leave more dollars in the private sector, which is exactly what federal deficit spending does. So why does Johnson promote tax cuts but oppose federal deficits, both of which accomplish the same thing?

Is he really that ignorant about economics, or is he just trying to defend Trump no matter what?

But Trump has suggested that the lack of sufficient spending cuts to offset his tax reductions came out of the need to hold the Republican congressional coalition together.

“We have to get a lot of votes,” Trump said last week. “We can’t be cutting.”

Get it? Trump is saying, in effect, that “we should cut spending, but the Republican coalition seems to know that spending cuts are harmful, so we’ll keep spending, which will grow the economy.”

That gibberish is what passes for wisdom in Washington.

That has left the administration betting on the hope that economic growth can do the trick, a belief that few outside of Trump’s orbit think is viable.

“Economic hope can do the trick?” What trick? Is Boak saying that the Republicans hope economic growth can cure the federal deficit?

How does that work? The deficit is the private sector sending fewer dollars to the government than the government sends to the private sector. How does economic growth cure that? It’s mathematical nonsense.

In the equation, GDP = Federal Spending + Nonfederal Spending + Net Exports, the Republicans hope that GDP goes up, while Federal Spending and Nonfederal Spending go down!

Would someone please find a 5th grader who will explain algebra to the politicians and Mr. Boak?

Most economists consider the nonpartisan CBO to be the foundational standard for assessing policies, although it does not produce cost estimates for actions taken by the executive branch, such as Trump’s unilateral tariffs.

Tech billionaire Musk, who was until recently part of Trump’s inner sanctum as the leader of the Department of Government Efficiency, told CBS News: “I was disappointed to see the massive spending bill, frankly, which increases the budget deficit, not just decreases it, and undermines the work that the DOGE team is doing.”

Musk may understand business finance, but he has no clue about federal finance. The goals are different. The goal of business is to increase income compared to outlay, thus increasing profits. So cost cutting is a viable, even necessary, option.

The goal of the federal government is to increase benefits to the people (by pumping more dollars into the economy). So taxing less and spending more are the best options — exactly the opposite of what a business should do.

In short, the sole purpose of any government is to improve the lives of the people. The purpose of a business is to improve its own life. Totally different goals and totally different abilities. Musk repeatedly proved he didn’t understand that.

To him, “government efficiency” means taking more dollars from the people and giving fewer dollars to the people.

Why do we need a government for that?

The tax and spending cuts that passed the House last month would add more than $5 trillion to the national debt in the coming decade if all of them are allowed to continue, according to the Committee for a Responsible Financial Budget, a fiscal watchdog group.

Translation: The tax cuts primarily benefiting the wealthy, along with spending cuts that hurt middle- and lower-income groups, are projected to inject 5 trillion growth dollars into the pockets of the rich over the next decade.

This estimate comes from the Committee for a Responsible Federal Budget, which is a Libertarian organization that opposes providing benefits to people who are not affluent.

To make the bill’s price tag appear lower, various parts of the legislation are set to expire. This same tactic was used with Trump’s 2017 tax cuts and it set up this year’s dilemma, in which many of the tax cuts in that earlier package will sunset next year unless Congress renews them.

But the debt is a much bigger problem now than it was eight years ago. Investors are demanding that the government pay a higher premium to keep borrowing as the total debt has crossed $36.1 trillion.

The interest rate on a 10-year Treasury Note is around 4.5%, up dramatically from the 2.5% rate being charged when the 2017 tax cuts became law.

Tell me this. Why would an entity, with the endless ability to create dollars by simply pressing a few computer keys, ever need to borrow dollars? Think about it.

The federal government, unlike state and local governments, does not borrow dollars. Federal bonds are completely different from state and local bonds, though they use the same word, “bonds.”

State and local governments do borrow dollars, when tax income is not sufficient to pay bills.

The federal government always can pay its bill simply by creating more dollars.

Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.” It’s not tax money… We simply use the computer to mark up the size of the account.

Fed Chairman Jerome Powell stated, “As a central bank, we have the ability to create money digitally.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent,i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.” You can find it in their publication titled “Why Health Care Matters and the Current Debt Does Not” from October 2011.

Paul Krugman (Nobel Prize–winning economist): “The U.S. government is not like a household. It literally prints money, and it can’t run out.”

Hyman Minsky (Economist, key influence on MMT) “The government can always finance its spending by creating money.”

Eric Tymoigne (Economist) “A sovereign government does not need to collect taxes or issue bonds to finance spending. It finances directly through money creation.”

Every knowledgeable economist knows the federal government cannot run short of dollars and does not borrow (i.e., “dependent on credit markets” as the St. Louis Fed confirmed).

So what about T-bonds, T-notes, and T-bills? Aren’t they borrowing?

No. They are interest-earning deposits, the purpose of which is not to provide spending money to the government. Instead, they provide a safer place (compared to banks and insurance companies) for people and countries to store unused dollars.

The federal government never touches those dollars.So they are not borrowed. They are just held for safe-keeping, and at agreed-upon dates, the dollars, plus interest, are returned to their owners.

Think of them as similar to bank safe-deposit boxes, where the bank never touches the contents.

The confusion arises because the word “bonds” describes state and local government borrowing, while the same word, “bonds,” means federal safety-deposit accounts.

The idea that the U.S. federal government, which created the U.S. dollar, would need to borrow its own dollars from China or anyone is absurd.

(It’s equally absurd to believe that the federal government would need to levy taxes so it could have dollars for spending.)

The White House Council of Economic Advisers argues that its policies will unleash so much rapid growth that the annual budget deficits will shrink in size relative to the overall economy, putting the U.S. government on a fiscally sustainable path.

As the quotes from knowledgeable individuals indicate, the U.S. government always is on a fiscally sustainable path.

White House budget director Russell Vought said the idea that the bill is “in any way harmful to debt and deficits is fundamentally untrue.”

“Harmful to debt and deficits”? Does he mean that increasing the so-called “debt” and deficits is true, but it could be beneficial to the economy (if it were not so skewed in favor of the rich)? Hard to know exactly what he means.

Most outside economists expect additional debt would keep interest rates higher and slow economic growth as the cost of borrowing for homes, cars, businesses and even college educations would increase.

Additional debt (which, as you have seen, is not “debt’) does not keep interest rates higher or lower. The Fed sets the rates arbitrarily in its misguided effort to fight inflation. Accepting deposits into Treasury Security accounts does not affect interest rates.

( Raising interest rates to fight inflation is misguided because it raises business costs, thus raising prices.)

“This just adds to the problem future policymakers are going to face,” said Brendan Duke, a former Biden administration aide now at the Center on Budget and Policy Priorities, a liberal think tank.

Duke said that with the tax cuts in the bill set to expire in 2028, lawmakers would be “dealing with Social Security, Medicare and expiring tax cuts at the same time.”

It’s quite easy for an informed economist to solve the “problems” of Social Security, Medicare, and tax cuts. Just create the needed dollars by pressing computer keys.

The government would need $10 trillion of deficit reduction over the next 10 years just to stabilize the debt, Tedeschi said. Even though the White House says the tax cuts would add to growth, most of the cost goes to preserve existing tax breaks, so that’s unlikely to boost the economy meaningfully.

“It’s treading water,” he said.

If the government wanted to stabilize the misnamed “debt,” it has plenty of simple options.

Simply refuse to accept any more deposits into T-security accounts. The government neither needs nor uses the dollars. They just sit there, safely earning interest.

Enact legislation to add $10 trillion to the General Account, which is the account used for federal payments.

Have the Treasury mint a $10 trillion coin, as it has the legal authority to do so, and deposit the coin with either the Federal Reserve or the General Account.

If It’s So Simple, Why Don’t They Do It?

Here’s why so many smart people can’t seem to solve a simple problem: They don’t want to.

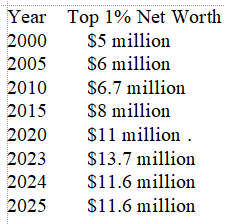

America is run by the very wealthy. What does “wealthy” mean?

“Wealthy” does not mean having a thousand, a million, a billion, or a trillion dollars. “Wealthy” means having substantially more wealth than 95% or 99% (pick your percentage) of the country.

Look at this table of the amount of wealth required to be in the top 1% of Americans:

In the year 2000, having $5 million would have put you in the upper 1%, but only 2o years later, you would have needed to more than double your wealth to be as wealthy.

So, to remain wealthy, you had two options.

Dramatically increase the amount of money you have, and/or

Make sure those below you don’t increase their wealth

If it is difficult to double your money in twenty-five years, consider ensuring that those beneath you do not increase their wealth. This way, your top 1% ranking would remain secure.

How do you prevent them from rising? By convincing them with the false notion that the government cannot afford to provide benefits.

Make them pay for their own healthcare. Keep Social Security benefits low. Don’t help them financially with college, so they either pay the tuition or are forced to work lower-paying jobs.

Consider the FICA tax. You might think you pay half, but in reality, you pay the full amount. Your employer takes FICA into account when determining salaries. FICA represents a significant percentage of your income.

For the wealthy, FICA taxes are insignificant or nonexistent. Why is this the case? To ensure that the Gap between you and the top 1 percent does not narrow.

You hear the government claim that it “can’t afford” Medicare for everyone, Social Security for everyone, or college for anyone who wants to attend. They say this is because the federal debt (which isn’t truly federal and isn’t really debt) is too large, and that deficits need to be reduced. Meanwhile, tax loopholes for the wealthy are being widened.

And government spending causes inflation, so any increase in spending must be paid for by your taxes.

And it’s all a lie, a Big Lie, for federal tax dollars are not used to fund federal spending.

That’s what the rich want you to believe. It’s how they stay rich. Or get even richer.

IN SUMMARY

Unlike state and local governments, the federal government is Monetarily Sovereign. It has infinite money.

It does not borrow the currency it originally created and continues to create by passing laws.

“Federal debt” is neither federal nor debt. It is deposits in T-security accounts, wholly owned by depositors and never used by the government. The purpose is to provide a safe place to store unused dollars. This stabilizes the dollar.

Federal deficits are necessary for economic growth.

Federal spending does not cause inflation; it results from shortages of essential goods and services. Federal spending can alleviate inflation by acquiring these scarce assets.

The Big Liein economics is that the federal financing is like personal financing. The federal government needs no income. It creates all its income.

The Big Lie aims to benefit the wealthy by increasing the income, wealth, and power Gap between the rich and the rest.