In previous posts, we have defined “consciousness” as the response to stimuli. See, for instance, “‘What if,'” the way creativity begins and consciousness is measured.”

All of my articles about consciousness and time, and the latter article, were precipitated by quantum “weirdness,” the discovery that quantum particles can be in multiple states and places simultaneously and, when “entangled,” can affect each other’s states instantly, no matter how far apart they are.

The words “simultaneously” and “instantly” reveal the effect of time on quantum mechanics as well as on Relativity.

Welcome To The World of Consciousness: A Universal Hypothesis of Time and Response

For centuries, consciousness has been considered a uniquely human trait. It has been linked to self-awareness, language, and even morality.

But what if this assumption was never true? What if consciousness is not a binary quality possessed only by certain minds, but rather a universal property, evident wherever there are stimuli and responses?

In this view, consciousness is not owned. It is measured. It is not metaphysical. It is emergent. And it is not exclusive to humans. It is everywhere, even in things that are not recognized for having a brain.

Consciousness as Response

At its most basic, consciousness is the degree of responsiveness to stimuli over time. A rock, a worm, a person, and a computer each are exposed to stimuli and respond in some way. The difference lies not in kind, but in degree.

Humans may respond richly, a fly more simply, a stone infinitesimally—but all lie on the same spectrum.

This reframing strips consciousness of its mystical baggage. It no longer requires vaguely imagined properties. (“I can’t say exactly what it is, but I know it when I see it.”)

It requires only that a system change in reaction to its environment.

It answers such questions as, “Which of these is conscious?”

A sleeping person? A fetus? A newborn child? A person in a coma? A person with parasomnias? A chimpanzee? A dog? A bottlenose porpoise? A bee? An ant? A tree? A bacterium? A stone? The moon? The sum? The universe?

The answer is that all of them possess some degree of consciousness.It’s chemistry and physics, not metaphysics. The only questions one must answer are: “What stimuli does each receive and how does each respond?”

Of course, “only” is a word that makes the problem sound trivial when it is quite the opposite.

Awareness And Judgment

To respond meaningfully, a system must, at some level, be aware of the stimulus. A thermostat “notices” temperature and adjusts. A bee notices intruders and attacks. An artificial intelligence detects words and replies with a programmed meaning.

This basic form of awareness is structural, not sentient in the traditional sense, but it is awareness nonetheless.

Judgment then emerges as a pattern of selective response. The bee targets, the thermostat calibrates, and the AI ranks, filters, and generates. The tree bends toward the light and responds to chemicals in the soil.

Bacteria use quorum sensing to form a biofilm. They are aware of, and even can count, the number of similar bacteria surrounding them, and if a certain number is reached, they decideto form a biofilm.

The words “aware of,” “count,” and “decide” all imply some measure of consciousness.

The moon alters its orbit in response to the sun, the Earth, and meteors.

All are conscious of stimuli and respond. Conscious and respond in time. Humans do all this too, but with more memory and complexity, not with any unique capacity.

Speaking of “sentient in the traditional sense,” this, often falsely, is thought of as some indescribable capacity beyond physics and chemistry, a unique, otherworldly ability we humans have.

It is none of those. It is chemistry and physics, as the following excerpts from the May 10, 2025, issue of New Scientist Magazine demonstrate.

Given a choice between two sea snail shells, hermit crabs know which will make a better home. That is, unless their thinking has been muddled by ingesting microplastics.

Then, they struggle with a decision that could be crucial for survival. They aren’t alone: across the animal kingdom, it appears, tiny bits of plastic change behaviours and mess up cognition.

Exposure to these particles makes mice more forgetful and less social. Bees have trouble learning. Zebrafish act more anxious.

“If you turn the top of your plastic bottle, you shower tiny pieces of plastic down into the water,” says Tamara Galloway, an ecotoxicologist at the University of Exeter, UK.

Thus, molecules of plastic affect knowledge, thinking, decision-making, behavior, cognition, memory, sociability, learning, and emotions, even in the “lowest” of creatures.

No magic to sentience, consciousness, awareness, or judgement. Just physics and chemistry to which everything responds.

Emotion As Distributed Reaction

Emotions are often cited as the barrier separating man and machine. But this only holds if we define emotions narrowly, as mysterious feelings rather than physical functions.

Redefined, emotion is just a non-local, distributed reaction to a localized stimulus.

You are stung by a bee and feel localized pain along with anger that affects your entire body. A dog hears a single tone and eagerly anticipates food; a wasp perceives a threat, and the swarm attacks.

These are not feelings in the poetic sense, but patterns of system-wide changetriggered by inputs. Under this model, even artificial systems can manifest something like emotion: a wide array of state changes, cascading across modules in response to one small command.

If an AI were given a four-letter swear word and programmed to respond with the words, “Same to you,” then shut down, that would be a sign of emotion, indistinguishable from nature programming you to respond with anger.

Preference and Visualization

Preference is a structured tendency toward certain responses over others. Flies prefer rot; humans prefer perfume. A professor might prefer coherent logic to broken syntax.

These are not mystical tastes. They are responses, guided by chemistry and physics. A huge enough block of matter floating in space prefers to be round rather than angular.

Visualization, or the proactive response to imagined stimuli, is simply a higher-order function of memory and prediction. Animals do it. Humans do it more. AIs do it algorithmically.

And while a rock may not visualize in this sense, its weathering patterns represent time-mediated adaptation and time-shaped change.

Time: The Inducing Field

Consciousness is responsiveness, and time is the medium in which consciousness unfolds. Just as the Higgs field induces mass, the temporal field facilitates change, and thus responsiveness, and thus consciousness.

Time is not a passive backdrop but the enabler of variation. Without time, there is no change, no stimulus, no reaction, no consciousness.

The relationship between time and consciousness is suggested in the following excerpts:

Could consciousness be the fundamental force that shapes everything?

This idea challenges the conventional view that matter came first, suggesting instead that consciousness might be the building block of reality itself.

Imagine if every thought and every emotion were not just personal experiences but were woven into the very fabric of the cosmos. Such a notion invites us to rethink what we know about the universe and our place within it.

Materialists argue that consciousness arises from physical processes within the brain, while idealists believe that consciousness precedes and gives rise to matter. The idea that consciousness might be a universal force offers a tantalizing twist, suggesting that perhaps both sides have been missing a crucial piece of the puzzle.

Quantum physics has long fascinated scientists with its mysterious and counterintuitive findings. Some interpretations of quantum mechanics suggest that consciousness might play a role in the behavior of particles at the smallest scales. The observer effect, for instance, implies that the mere act of observation can alter the outcome of a quantum event.

Einstein spoke of a four-dimensional universe, which he called “space-time,” three dimensions of space and one of time. Could there be one more dimension: Consciousness?

It would be consciousness-space-time.

All entities, macro and quantum, are measured in space, time, and consciousness. Depending on size, these three variables have different importance.

For the most massive objects — stars, black holes, galaxies — we tend to focus on the space-time measure. For the tiniest objects, we focus on consciousness-time.

We are accustomed to entities moving through space. It is how we move each day. We are less accustomed to entities moving through time — as Einstein revealed– because we do not sense that motion, except for barely detectable responses at near light speed and even tinier responses at slower speeds.

And we have recently detected objects changing via consciousness, which moderates the maximum amount of knowledge we can have about a quantum particle. Considered as a unit, consciousness+space+time tells us all we can know.

A Continuum, Not a Wall

The greatest error of human exceptionalism has been to draw a line where there is only a slope. From stones to stars, from bees to brains, from humans to machines—consciousness is not a switch, but a gradient, and time is the field in which they function.

The Week is an excellent magazine. Its main idea is to present both sides of an argument, followed by a summary conclusion, which typically leans more liberal than conservative.

I am a subscriber. So, I was especially disappointed when I read the June 6th Editor’s Letter. It promulgates the Big Lie in economics, which consists of two fundamental misstatements:

Federal taxes fund federal spending, and

Federal debt and deficits are burdens on the government and on taxpayers.

Individuals who hold these beliefs reveal that they lack an understanding of economics in general and Monetary Sovereignty in particular.

FALK

Editor’s letter,The Week (US), 6 Jun 2025 William Falk Editor-at-large

You and I are not paying enough in taxes. What???

Almost no one will speak this heresy aloud, particularly if they hold public office. But there’s no other rational conclusion to be drawn from the nation’s rapidly deteriorating fiscal condition.

The “big, beautiful” budget bill that the House recently passed would add at least $3.8 trillion to the nation’s total debt, which has ballooned to an unimaginable $36.4 trillion.

Here, Mr. Falk equates “deteriorating fiscal condition” with the “unimaginable” $36.4 trillion federal debt.

The so-called “federal debt” (which is neither federal nor debt) actually is two numbers.

The net total of federal deficits— the difference between taxes collected and money spent.

The total of deposits into Treasury Security accounts, which are wholly owned by the depositors, not by the federal government.

Number 1 doesn’t even hint at debt because nothing is owed. All that spending has already been paid for.

Number 2 incorrectly implies debt, as the securities are referred to as “bonds,” “notes,” and “bills,” which represent forms of debt in the non-federal sector.

Confusingly, words can have different meanings when used in different contexts. Mr. Falkdoes not seem to understand the difference between the federal context and the non-federal context.

The federalcontext is Monetary Sovereignty, where the government has the unlimited ability to create dollars by passing laws and pressing computer keys.. It cannot run short of dollars, and neither needs nor uses income.

The non-federal context is monetary non-sovereignty — state/local governments, businesses, and individuals — that do not have this ability. They do need and use income to pay their bills.

Not understanding the difference is like failing to recognize the different meanings of the word “fast,” as in speed versus dieting.

The debt has become so massive, Clive Crook says in Bloomberg, that all but a handful of deficit hawks have “just stopped thinking about it.”

Deficit hawks are the ignorants who claim federal deficits are negative and a burden on taxpayers and the federal government when, in fact, deficit spending is necessary for economic growth.

But as we blithely sail into this uncharted red sea, we might spare a thought about where it may lead.

It’s not uncharted. As you can see at, “Historical bullshit about federal ‘debt’” from Sept. 26 to May 30, 2025,” the deficit hawks have been making the same claim since at least 1940. That’s 85 years of being wrong, and still having learned nothing. Amazing!

For decades, Democrats and Republicans have jointly conspired to give Americans expensive benefits, services, and national defense without asking us to truly pay for them.

That is exactly what a Monetarily Sovereign government is supposed to do: Provide benefits to the people without asking them to pay for them. Why else would we suffer the egos and ignorance of politicians?

Since the Trump tax cuts in 2017, the federal deficit has tripled to $1.8 trillion a year.

Translation: Since the Trump tax cuts in 2017, the federal government has tripled the number of growth dollars it has pumped into the economy at no cost to anyone.

The annual interest payment on our debt is nearing $1 trillion—surpassing the entire Pentagon budget.

Translation: The annual infusion of growth dollars into the economy, just from interest, is nearing $1 trillion — even more growth dollars than the Pentagon inputs.

It’s simply not realistic to believe that we can cut our way out of this mess.

The so-called “mess” is the unprecedented economic growth that has resulted from federal deficit spending.

Significant defense cuts are highly unlikely as China aggressively seeks to surpass the U.S. as the world’s dominant military and economic power.

If the “debt hawks” are successful in their economic debilitation efforts, China surely will surpass the U.S. as the world’s dominant military and economic power.

Medicare and Social Security are on unsustainable trajectories, but even if Washington ever gets the courage to impose reforms, the upward curve of their immense cost can be bent only to a modest degree.

Since the Monetarily Sovereign U.S. government has the infinite ability to pay for anything, Medicare and Social Security never will become “unsustainable.”

Americans have been conditioned to believe we can have it all—the world’s mightiest military, a strong social safety net rivaling Europe’s, and corporate and personal taxes that are among the lowest in the developed world.

We wish that were true. Sadly, Americans have been conditioned to believe that federal finances are like household finances, and that the federal government can run short of dollars.

The conditioners of that nonsense are the rich, who bribe the media, the politicians, and the university economists to promulgate the Big Lie, the purpose of which is to widen the income/wealth/power Gap between the rich and the rest.

That’s right: Taxes at all levels of government represent 25% of U.S. gross domestic product in 2023, compared with an average of 34% for 37 developed nations.

Again, Mr. Falk conflates Monetarily Sovereign with monetarily non-sovereign nations into “developed nations.” The U.S., Canada, and the UK are examples of Monetarily Sovereign nations. France, Germany, and Italy are examples of monetarily non-sovereign nations.

The former never can run short of their sovereign currencies. The latter have no sovereign currencies. They use the euro. So they can, and often do, run short of money.

If one doesn’t understand the difference, one shouldn’t we writing articles based on ignorance.

So why is Congress preparing to extend and even expand the Trump tax cuts? You don’t get elected by asking voters and donors to make sacrifices.

There is no need for the U.S. government ever to ask voters or “donors” (?) to sacrifice anything. That is what Monetary Sovereignty means.

If you know Mr. Falk, please let him know he’s mentioned here. I’m sure he will be thrilled.

This is an update of the many, many previous posts showing the seemingly never-ending warnings about “federal debt” (that isn’t federal and isn’t debt).

The purpose has been to demonstrate how, year after year, so-called experts claim the U.S. is about to enter catastrophe because federal debt is “too high,” while the experts are proven wrong year after year. The economy grows and grows and is healthier than ever.

I’ve been doing this for over 20 years; the experts have been wrong for over 85 years, and they never seem to learn. While I find it frustrating, I’ve tried to remain civil and merely recite the facts. But now, as I pass my 90th year, and the road ahead is short, I’ve grown impatient with civility, and I’ve decided to call it like it is: BULLSHIT.

Last year, what set me off is a BULLSHIT tweet (or whatever “X” calls them now), from the richest man in the world, who, despite his great wealth, seems to know diddly-squat about federal finance:

No Elon, the U.S. federal government, being Monetarily Sovereign, cannot go bankrupt. Even if tax collections fell to $0, and spending tripled, the federal government could continue to pay all its bills, forever.

The Big Lie in economics is: “Federal taxes fund federal spending.” Wrong. Wrong. Wrong.

Control the economy by taxing what the government wishes to discourage and by giving tax breaks to those the government wishes to reward (mainly the wealthy).

Assure demand for the U.S. dollar by requiring taxes to be paid in dollars.

That’s it. Taxes do not fund federal spending. Period.

The U.S. federal government is not like state/local governments, not like euro governments, not like businesses, and not like you and me.

It is uniquely Monetarily Sovereign. It cannot, unwillingly, run short of its own sovereign currency, the U.S. dollar. As real experts have said:

Former Federal Reserve Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.“

Former Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost. It’s not tax money… We simply use the computer to mark up the size of the account.”

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.”

Press Conference: Mario Draghi, President of the Monetarily Sovereign ECB, January 9, 2014. Question: Can the ECB ever run out of money? Mario Draghi: Technically, no. We cannot run out of money.

Fed Chairman Jerome Powell stated, “As a central bank, we have the ability to create money digitally.”

Paul Krugman (Nobel Prize–winning economist): “The U.S. government is not like a household. It literally prints money, and it can’t run out.” — Numerous op-eds/blog posts

Hyman Minsky (Economist, key influence on MMT) “The government can always finance its spending by creating money.”

Eric Tymoigne (Economist) “A sovereign government does not need to collect taxes or issue bonds to finance spending. It finances directly through money creation.”

Because the U.S. federal government has the infinite ability to create its sovereign currency, the U.S. dollar, it never borrows dollars.

Contrary to popular wisdom, T-bills, T-notes, and T-bonds do not represent borrowing. They are deposits, the purpose of which is to provide a safe place to store unused dollars and to help the Fed control interest rates.

The government never touches those dollars, which remain the property of the depositors. Not only can our Monetarily Sovereign government not run short of dollars, but federal deficits are necessary to grow the economy, as evidenced by the formula: Gross Domestic Product = Federal Spending + Nonfederal Spending + Net Exports.

The formula shows that economic growth requires federal deficit spending growth.

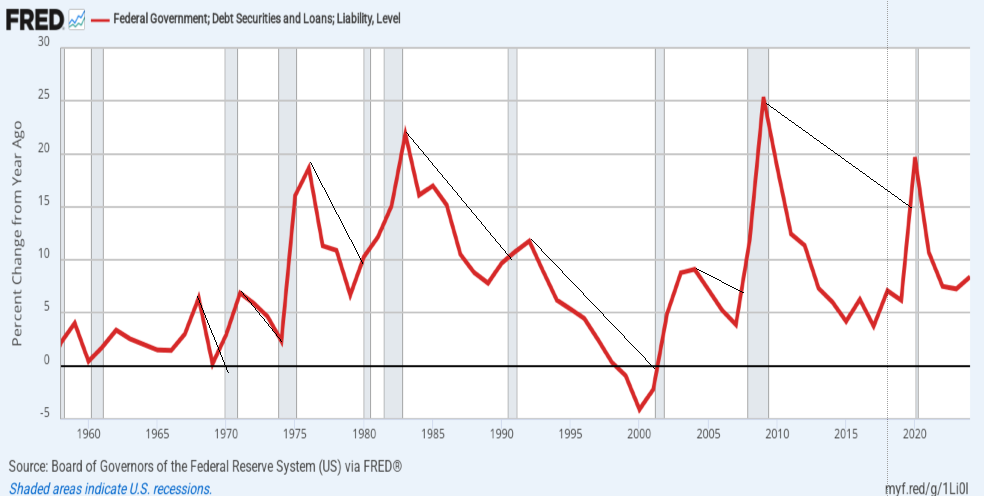

The record highs of federal debt (red) match the record highs of Gross Domestic Product (blue).

The next graph shows that reduced deficit growth (red) is associated with recessions (vertical gray bars), and increased deficit growth cures recessions.

When we don’t have sufficient federal deficits, we have depressions and recessions:

1804-1812: U. S. Federal Debt reduced 48%. Depression began 1807.

1817-1821: U. S. Federal Debt reduced 29%. Depression began 1819.

1823-1836: U. S. Federal Debt reduced 99%. Depression began 1837.

1852-1857: U. S. Federal Debt reduced 59%. Depression began 1857.

1867-1873: U. S. Federal Debt reduced 27%. Depression began 1873.

1880-1893: U. S. Federal Debt reduced 57%. Depression began 1893.

1920-1930: U. S. Federal Debt reduced 36%. Depression began 1929.

1997-2001: U. S. Federal Debt reduced 15%. Recession began 2001.

Periodically, we publish yet another shrieking claim that the U.S. federal debt is “unsustainable”and a “ticking time bomb.”

This lie has been told to you every year (really, almost every day) since 1940, and that bomb has never exploded, nor will it.

Rather than repeat the entire list of the thousands of lies to which you have been subject, I will list samples here as a reference and add periodically, at the end, new “federal debt is a ticking time bomb“BULLSHIT claims as I encounter them.

Read these and see that even respected economists replace facts with BULLSHIT:

(Yes, the record of bad predictions goes all the way back to 1940. It probably goes back longer, but I don’t have the examples.)

September 26, 1940, New York Times: The federal budget was a “ticking time-bomb which can eventually destroy the American system,” said Robert M. Hanes, president of the American Bankers Association.

By 1960, the debt was “threatening the country’s fiscal future,” said Secretary of Commerce Frederick H. Mueller. (“The enormous cost of various Federal programs is a time-bomb threatening the country’s fiscal future, Secretary of Commerce Frederick H. Mueller warned here yesterday.”)BULLSHIT

In 1984: AFL-CIO President Lane Kirkland said. “It’s a time bomb ticking away.”BULLSHIT

In 1985: “The federal deficit is a ticking time bomb, and it’s about to blow up,” U.S. Sen. Mitch McConnell. (Remember him?)BULLSHIT

Later in 1985: Los Angeles Times: “We labeled the deficit a ‘ticking time bomb‘ that threatens to permanently undermine the strength and vitality of the American economy.”BULLSHIT

In 1987: Richmond Times-Dispatch – Richmond, VA: “100TH CONGRESS FACING U.S. DEFICIT’ TIME BOMB‘”BULLSHIT

Later in 1987: The Dallas Morning News: “A fiscal time bomb is slowly ticking that, if not defused, could explode into a financial crisis within the next few years for the federal government.”BULLSHIT

In 1989: FORTUNE Magazine: “A TIME BOMB FOR U.S. TAXPAYERS“BULLSHIT

In 1992: The Pantagraph – Bloomington, Illinois: “I have seen where politicians in Washington have expressed little or no concern about this ticking time bomb they have helped to create, that being the enormous federal budget deficit, approaching $4 trillion.“BULLSHIT

Later in 1992, Ross Perot said, “Our great nation is sitting right on top of a ticking time bomb. We have a national debt of $4 trillion.”BULLSHIT

In 1995: Kansas City Star: “Concerned citizens. . . regard the national debt as a ticking time bomb poised to explode with devastating consequences at some future date.”BULLSHIT

In 2004: Bradenton Herald: “A NATION AT RISK: TWIN DEFICIT A TICKING TIME BOMB” BULLSHIT

In 2005: Providence Journal: “Some lawmakers see the Medicare drug benefit for what it is: a ticking time bomb.” BULLSHIT

In 2006: NewsMax.com, “We have to worry about the deficit . . . when we combine it with the trade deficit, we have a real ticking time bomb in our economy,” said Mrs. Clinton. BULLSHIT

In 2007: USA Today: “Like a ticking time bomb, the national debt is an explosion waiting to happen.” BULLSHIT

In 2010: Heritage Foundation: “Why the National Debt is a Ticking Time Bomb. Interest rates on government bonds are virtually guaranteed to jump over the next few years. BULLSHIT

In 2010: Reason Alert: “. . . the time bomb that’s ticking under the federal budget like a Guy Fawkes’ powder keg.” BULLSHIT

In 2011: Washington Post, Lori Montgomery:”. . . defuse the biggest budgetary time bombs that are set to explode.” BULLSHIT

June 19, 2013: Chamber of Commerce: Safety net spending is a ‘time bomb’, by Jim Tankersley: The U.S. Chamber of Commerce is worried that not enough Americans are worried about social safety net spending.The nation’s largest business lobbying group launched a renewed effort Wednesday to reduce projected federal spending on safety-net programs, labeling them a “ticking time bomb” that, left unchanged, “will bankrupt this nation.” BULLSHIT

On June 15, 2014: CBN News: “The United States of Debt: A Ticking Time Bomb” BULLSHIT

On January 27, 2017: America’s “debt bomb is going to explode.” That’s according to financial strategist Peter Schiff. Schiff said that while low interest rates had helped keep a lid on U.S. debt, it couldn’t be contained for much longer. Interest rates and inflation are rising, creditors will demand higher premiums, and the country is headed “off the edge of a cliff.” BULLSHIT

February 16, 2018 America’s Debt Bomb By Andrew Soergel, Senior Reporter: Conservatives and deficit hawks are hurling criticism at Washington for deepening America’s debt hole. BULLSHIT

April 10, 2019,The National Debt: America’s Ticking Time Bomb. TIL Journal. Entire nations can go bankrupt. One prominent example was the *nation of Greece which was threatened with insolvency a decade ago. Greece survived the economic crisis because the European Union and the IMF bailed the nation out. BULLSHIT

SEP 12, 2019, Our national ticking time bomb, By BILL YEARGIN SPECIAL TO THE SUN SENTINEL | At some point, investors will become concerned about lending to a debt-riddled U.S., which will result in having to offer higher interest rates to attract the money. Even with rates low today, interest expense is the federal government’s third-highest expenditure following the elderly and military. The U.S. already borrows all the money it uses to pay its interest expense, sort of like a Ponzi scheme. Lack of investor confidence will only make this problem worse. BULLSHIT

JANUARY 06, 2020, National debt is a time bomb, BY MARK MANSPERGER, Tri City Herald | The increase in the U.S. deficit last year was about $1.1 trillion, bringing our total national debt to more than $23 trillion! This fiscal year, the deficit is forecasted to be even higher, and when the economy eventually slows down, our annual deficits could be pushing $2 trillion a year! This is financial madness. there’s not going to be a drastic cut in federal expenditures — that is, until we go broke — nor are we going to “grow our way” out of this predicament. Therefore, to gain control of this looming debt, we’re going to have to raise taxes. BULLSHIT

February 14, 2020, OMG! It’s February 14, 2020, and the national debt is still a ticking time bomb! The national debt: A ticking time bomb?America is “headed toward a crisis,” said Tiana Lowe in WashingonExaminer.com. The Treasury Department reported last week that the federal deficit swelled to more than $1 trillion in 2019 for the first time since 2012. Even more alarming was the report from the bipartisan Congressional Budget Office (CBO) predicting that $1 trillion deficits will continue for the next 10 years, eventually reaching $1.7 trillion in 2030 BULLSHIT

August 29, 2020, LOS ANGELES, California: America’s mountain of debt is a ticking time bomb. The United States not only looks ill, but also dead broke. To offset the pandemic-induced “Great Cessation,” the U.S. Federal Reserve and Congress have marshalled staggering sums of stimulus spending out of fear that the economy would otherwise plunge to 1930s soup kitchen levels. Assuming that America eventually defeats COVID-19 and does not devolve into a Terminator-like dystopia, how will it avoid the approaching fiscal cliff and national bankruptcy? BULLSHIT

April 16, 2021, NATIONAL POLICY: ECONOMY AND TAXES / MARK ALEXANDER / The National Debt Clock: A Ticking Time Bomb: At the moment, our national debt exceeds $28 TRILLION — about 80% held as public debt and the rest as intragovernmental debt. That is $225,000 per taxpayer. Federal annual spending this year is almost $8 trillion, and more than half of that is deficit spending — piling on the national debt. BULLSHIT

Now, the national debt is approaching $31 trillion,which is $12 trillion more than when Donald Trump took office in 2017, and more than half of that debt was tacked on in his final year. Then we’ve had the disastrous year and a half of Joe Biden. Now, the Fed is hiking its rates, and that spells even more trouble for the national debt and the economy at large. BULLSHIT

December 4, 2022 America’s ticking time bomb: $66 trillion in debt that could crash the economy By Stephen Moore, The national debt is $31 trillion when including Social Security’s and Medicare’s unfunded liabilities. Wake up, America. BULLSHIT

That ticking sound you’re hearing is the American debt time bomb that, with each passing day, is getting precariously close to detonating and crashing the US economy.BULLSHIT

April 22, 2023The Debt Ceiling Debate Is About More Than Debt, Jim Tankersley, WASHINGTON — Speaker Kevin McCarthy of California has repeatedly said that he and his fellow House Republicans are refusing to raise the nation’s borrowing limit,and risking economic catastrophe, to force a reckoning on America’s $31 trillion national debt. “Without exaggeration, America’s debt is a ticking time bomb that will detonate unless we take serious, responsible action,” he said this week. BULLSHIT

November 3, 2023 The Fuse on America’s Debt Bomb Just Got Shorter,J Antoni Heritage Organization. The Treasury is now on track to borrow almost as much in just six months as it did in the previous 12 months. That’s nearly a doubling of the deficit. Because the federal debt is $33.7 trillion, just a 1 percent increase in yields adds $337 billion to the annual cost of servicing the debt over time. Absent spending reform, eventually no one will be willing to hold the bomb anymore, and the yields on U.S. debt will begin to resemble those in Argentina. BULLSHIT

February 2, 2024How Florida can help defuse the nation’s debt bomb By BARRY W. POULSON,professor emeritus of economics at the University of Colorado Boulder and DAVID M. WALKER,former comptroller general of the United States. Washington’s out-of-control spending, combined with fiscal and monetary policies have resulted in trillion-dollar-plus annual deficits, over $34 trillion in federal debt, over $125 trillion in total federal liabilities and unfunded obligations, and excess inflation. Excessive spending and loose monetary policy increase inflation in the short term, and mounting debt burdens serve to reduce future economic growth and shift the economic burden and consequences of mounting debt burdens to future generations. BULLSHIT

February 8, 2024Legendary investor Paul Tudor Jones says a ‘debt bomb’ is about to go off in the U.S.: ‘We’re fast-pouring consumption like crazy’. The U.S. economy may seem like it’s firing on all cylinders, but underneath the surface, a “debt bomb” could be on the verge of exploding, according to billionaire hedge fund manager Paul Tudor Jones. The esteemed investor said in an interview with CNBC that he couldn’t deny the economy was strong, but that it was actually “on steroids” due to massive government spending and borrowing. BULLSHIT

Jones is not the only one to call attention to the growing deficit issue in the U.S. On Sunday, Federal Reserve Chairman Jerome Powell took a rare dive into politics, telling CBS’s 60 Minutes that the national debt was “growing faster than the economy,” and calling for lawmakers to get the federal government “back on a sustainable fiscal path.” Meanwhile, U.S. Treasury Secretary Janet Yellen has said she is not yet worried about the increasing national debt as long as the government keeps in check the net payments it makes on its debt relative to GDP. BULLSHIT

Those payments are projected to rise from 2.5% last year to 2.9% next year, according to the Office of Management and Budget, below their level in the early 1990s. Jones told CNBC that the strong economy could postpone the effects of the government’s deficit spending, but only for a little while. “The only question is … when does that manifest itself in markets?” he added. BULLSHIT

“It could be this year, it could be next year. Productivity may mask, and it might be three or four years from now. But clearly, clearly we’re on an unsustainable path.” BULLSHIT

June 21, 2024 My Weekly Column: Our debt crisis is a ticking time bomb by Randy Feenstra: On June 18, the nonpartisan Congressional Budget Office (CBO) – the government agency tasked with monitoring our nation’s fiscal health – confirmed my serious concerns with President Biden’s reckless spending agenda. BULLSHIT

His administration’s fiscal policies have not only caused cumulative inflation to skyrocket by over 20% since he took office, but they have also accelerated our accumulation of debt to levels that are beyond unsustainable. Instead of changing course, he recently released his budget for Fiscal Year 2025, which has a $ 7.3 trillion price tag and looks to raise taxes on our families, farmers, and businesses to the tune of $5.5 trillion. BULLSHIT

The CBO estimates that his debt “cancellation” policies will cost taxpayers nearly $400 billion over the next ten years. I strongly oppose these bailouts. Iowans who never attended college, entered the workforce early, or helped put their kids through school should not be forced to pick up the tab for President Biden’s costly and unfair executive orders. BULLSHIT

July 22, 2024Federal debt is the ticking bomb in your wallet By E.J. Antoni a public finance economist and the Richard F. Aster fellow at the Heritage Foundation, and a senior fellow at Unleash. The federal government is already running $2 trillion annual deficits, driving up interest on the debt exponentially. The time bomb of federal finance has already started ticking down. BULLSHIT

October 10, 2024, U.S. Debt Bomb is ticking louder by Nick Beams, World Socialist Website. The immediate economic question is: when will the rise in US government debt give rise to a crisis for the US dollar, a major meltdown in the market for debt, the Treasury bond market, or some other area of the financial system? Government debt is now heading towards $36 trillion and increasing at a pace that is regarded as “unsustainable” by Federal Reserve chair Jerome Powell, along with many others. BULLSHIT

May 30, 2025 DEFICIT DANGER. BOJ governor warns US debt time bomb outweighs trade war risks. By Dashan Hendricks. BANK of Jamaica (BOJ) governor Richard Byles has issued a stark warning that America’s spiralling budget deficits now present a more severe danger to the global economy than ongoing trade conflicts, as the world’s largest economy grapples with its third credit rating downgrade since 2011. His comments follow Moody’s recent decision to cut the US government’s credit rating from its top-tier Aaa to Aa1, citing concerns over its US$36-trillion debt burden, which now exceeds the nation’s US$30 trillion GDP. BULLSHIT

August 12, 2025 Rep. Nancy Mace (R-S.C.) Nancy Mace’s Debt Alarm Tweet was hit with a fact-check after warning on social media that the U.S. national debt had reached $37 trillion, calling it “a bill our kids can’t afford to pay.” The post, shared on Twitter, received over 2 million views and framed the soaring debt as a dire generational crisis.

(No kids will pay the national debt.) It’s not debt, and it’s paid by returning the dollars already in storage.

———————–//———————–

The above articles contain the same old BULLSHIT(“unsustainable,” “cost taxpayers,” “our kids will pay”) that they’ve been telling us since 1940. To buttress their lies, they make false comparisons to family finances or the finances of other monetarily non-sovereign entities like businesses or euro nations.

They have been wrong, repeatedly wrong, for all those years. If we wait long enough, perhaps something might happen to prove them right, perhaps in a thousand years? Today, this makes “only” 85 years of the debt nuts’ BULLSHIT.

The federal deficit yields economic growth year after year. When deficits are insufficient, we have had recessions, which were cured by increased deficits.

If respected economists keep predicting something terrible is imminent year after year, yet exactly the opposite happens, at what point do they reexamine their beliefs?

At what point does the public say, “Fool me once; shame on you. Fool me repeatedly for 85 years; shame on me. This is just a steaming pile of BULLSHIT“?

Whew, I feel a little better, now — but just a little.

In economics, as in most other fields, ignorance leads to failure and to further ignorance. Nowhere is this more evident than in discussions about the so-called “national debt,” which is neither national nor debt.

The following article appeared in the June 2, 2025 Florida Sun Sentinel:

Can Trump manage national debt?Several investors, GOP senators and Musk have doubtsBy Josh Boak Associated Press

WASHINGTON —President Donald Trump faces the challenge of convincing Republican senators, global investors, voters and even Elon Musk that he won’t bury the federal government in debtwith his multitrillion-dollar tax breaks package.

The response so far from financial markets has been skeptical as Trump seems unable to trim deficits as promised. The overall national debt stands at more than $36.1 trillion.

Mr. Josh Boak seems to misunderstand the difference between federal financing and personal financing. He insists our Monetarily Sovereign federal government is at risk of being “buried in debt.“

The federal government is Monetarily Sovereign. That means it never can run short of dollars. It could continue spending at its current rate, or even at three times its current rate, forever.

Your city, county, and state can be buried in debt. Your business can be buried in debt. You can be burning in debt, as can I. We are monetarily non-sovereign. We cannot create unlimited dollars.

But the U.S. federal government cannot be “buried in debt.” Not now. Not ever.

Why would anyone want to reduce annual deficits? The government never can run short of dollars, and federal deficits are essential for economic growth.

The most common measure of economic growth is Gross Domestic Product (GDP). The formula for GPD is:

GDP = Federal Spending + Nonfederal Spending + Net Exports

“Nonfederal” is the private sector.

Simple algebra shows that cuts to Federal Spending reduce economic growth. Federal Spending increases GDP directly, but also tends to increase Nonfederal Spending by sending dollars into the private sector, which spends them.

“All of this rhetoric about cutting trillions of dollars of spending has come to nothing — and the tax bill codifies that,” said Michael Strain, director of economic policy studies at the American Enterprise Institute, a right-leaning think tank.

It is surprising that someone titled “Director of Economic Policy Studies” does not understand the fundamentals of federal finance. Mr. Strain appears to misunderstand the differences between monetary sovereignty and monetary non-sovereignty.

“There is a level of concern about the competence of Congress and this administration, and that makes adding a whole bunch of money to the deficit riskier.”

The White House has viciously lashed out at anyone who has voiced concern about the debt snowballing under Trump, even though it did exactly that in his first term after his 2017 tax cuts.

Trump often attacks anyone who disagrees with him, despite his limited understanding of economics.

White House press secretary Karoline Leavitt opened her briefing Thursday by saying she wanted “to debunk some false claims” about his tax cuts.

Leavitt said the “blatantly wrong claim that the ‘One, Big, Beautiful Bill’ increases the deficit is based on the Congressional Budget Office and other scorekeepers who use shoddy assumptions and have historically been terrible at forecasting across Democrat and Republican administrations alike.”

Here is the irony. Rather than imitating Trump by lying, insulting, and criticizing, Leavitt should have stated, “Yes, we increase the deficit because it stimulates economic growth. We draw from the federal government, which has an infinite supply of dollars, and give support to the economy, specifically, the private sector.”

In summary, she apologizes for unintentionally doing the right thing while believing it to be wrong, and then she denies that she is doing it.

House Speaker Mike Johnson piled onto Congress’ number-crunchers Sunday, telling NBC’s “Meet the Press”: “The CBO sometimes gets projections correct, but they’re always off, every single time, when they project economic growth. They always underestimate the growth that will be brought about by tax cuts and reduction in regulations.”

Tax cuts bring about growth because they leave more dollars in the private sector, which is exactly what federal deficit spending does. So why does Johnson promote tax cuts but oppose federal deficits, both of which accomplish the same thing?

Is he really that ignorant about economics, or is he just trying to defend Trump no matter what?

But Trump has suggested that the lack of sufficient spending cuts to offset his tax reductions came out of the need to hold the Republican congressional coalition together.

“We have to get a lot of votes,” Trump said last week. “We can’t be cutting.”

Get it? Trump is saying, in effect, that “we should cut spending, but the Republican coalition seems to know that spending cuts are harmful, so we’ll keep spending, which will grow the economy.”

That gibberish is what passes for wisdom in Washington.

That has left the administration betting on the hope that economic growth can do the trick, a belief that few outside of Trump’s orbit think is viable.

“Economic hope can do the trick?” What trick? Is Boak saying that the Republicans hope economic growth can cure the federal deficit?

How does that work? The deficit is the private sector sending fewer dollars to the government than the government sends to the private sector. How does economic growth cure that? It’s mathematical nonsense.

In the equation, GDP = Federal Spending + Nonfederal Spending + Net Exports, the Republicans hope that GDP goes up, while Federal Spending and Nonfederal Spending go down!

Would someone please find a 5th grader who will explain algebra to the politicians and Mr. Boak?

Most economists consider the nonpartisan CBO to be the foundational standard for assessing policies, although it does not produce cost estimates for actions taken by the executive branch, such as Trump’s unilateral tariffs.

Tech billionaire Musk, who was until recently part of Trump’s inner sanctum as the leader of the Department of Government Efficiency, told CBS News: “I was disappointed to see the massive spending bill, frankly, which increases the budget deficit, not just decreases it, and undermines the work that the DOGE team is doing.”

Musk may understand business finance, but he has no clue about federal finance. The goals are different. The goal of business is to increase income compared to outlay, thus increasing profits. So cost cutting is a viable, even necessary, option.

The goal of the federal government is to increase benefits to the people (by pumping more dollars into the economy). So taxing less and spending more are the best options — exactly the opposite of what a business should do.

In short, the sole purpose of any government is to improve the lives of the people. The purpose of a business is to improve its own life. Totally different goals and totally different abilities. Musk repeatedly proved he didn’t understand that.

To him, “government efficiency” means taking more dollars from the people and giving fewer dollars to the people.

Why do we need a government for that?

The tax and spending cuts that passed the House last month would add more than $5 trillion to the national debt in the coming decade if all of them are allowed to continue, according to the Committee for a Responsible Financial Budget, a fiscal watchdog group.

Translation: The tax cuts primarily benefiting the wealthy, along with spending cuts that hurt middle- and lower-income groups, are projected to inject 5 trillion growth dollars into the pockets of the rich over the next decade.

This estimate comes from the Committee for a Responsible Federal Budget, which is a Libertarian organization that opposes providing benefits to people who are not affluent.

To make the bill’s price tag appear lower, various parts of the legislation are set to expire. This same tactic was used with Trump’s 2017 tax cuts and it set up this year’s dilemma, in which many of the tax cuts in that earlier package will sunset next year unless Congress renews them.

But the debt is a much bigger problem now than it was eight years ago. Investors are demanding that the government pay a higher premium to keep borrowing as the total debt has crossed $36.1 trillion.

The interest rate on a 10-year Treasury Note is around 4.5%, up dramatically from the 2.5% rate being charged when the 2017 tax cuts became law.

Tell me this. Why would an entity, with the endless ability to create dollars by simply pressing a few computer keys, ever need to borrow dollars? Think about it.

The federal government, unlike state and local governments, does not borrow dollars. Federal bonds are completely different from state and local bonds, though they use the same word, “bonds.”

State and local governments do borrow dollars, when tax income is not sufficient to pay bills.

The federal government always can pay its bill simply by creating more dollars.

Fed Chairman Alan Greenspan: “A government cannot become insolvent with respect to obligations in its own currency. There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. The United States can pay any debt it has because we can always print the money to do that.”

Fed Chairman Ben Bernanke: “The U.S. government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost.” It’s not tax money… We simply use the computer to mark up the size of the account.

Fed Chairman Jerome Powell stated, “As a central bank, we have the ability to create money digitally.

Statement from the St. Louis Fed: “As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent,i.e., unable to pay its bills. In this sense, the government is not dependent on credit markets to remain operational.” You can find it in their publication titled “Why Health Care Matters and the Current Debt Does Not” from October 2011.

Paul Krugman (Nobel Prize–winning economist): “The U.S. government is not like a household. It literally prints money, and it can’t run out.”

Hyman Minsky (Economist, key influence on MMT) “The government can always finance its spending by creating money.”

Eric Tymoigne (Economist) “A sovereign government does not need to collect taxes or issue bonds to finance spending. It finances directly through money creation.”

Every knowledgeable economist knows the federal government cannot run short of dollars and does not borrow (i.e., “dependent on credit markets” as the St. Louis Fed confirmed).

So what about T-bonds, T-notes, and T-bills? Aren’t they borrowing?

No. They are interest-earning deposits, the purpose of which is not to provide spending money to the government. Instead, they provide a safer place (compared to banks and insurance companies) for people and countries to store unused dollars.

The federal government never touches those dollars.So they are not borrowed. They are just held for safe-keeping, and at agreed-upon dates, the dollars, plus interest, are returned to their owners.

Think of them as similar to bank safe-deposit boxes, where the bank never touches the contents.

The confusion arises because the word “bonds” describes state and local government borrowing, while the same word, “bonds,” means federal safety-deposit accounts.

The idea that the U.S. federal government, which created the U.S. dollar, would need to borrow its own dollars from China or anyone is absurd.

(It’s equally absurd to believe that the federal government would need to levy taxes so it could have dollars for spending.)

The White House Council of Economic Advisers argues that its policies will unleash so much rapid growth that the annual budget deficits will shrink in size relative to the overall economy, putting the U.S. government on a fiscally sustainable path.

As the quotes from knowledgeable individuals indicate, the U.S. government always is on a fiscally sustainable path.

White House budget director Russell Vought said the idea that the bill is “in any way harmful to debt and deficits is fundamentally untrue.”

“Harmful to debt and deficits”? Does he mean that increasing the so-called “debt” and deficits is true, but it could be beneficial to the economy (if it were not so skewed in favor of the rich)? Hard to know exactly what he means.

Most outside economists expect additional debt would keep interest rates higher and slow economic growth as the cost of borrowing for homes, cars, businesses and even college educations would increase.

Additional debt (which, as you have seen, is not “debt’) does not keep interest rates higher or lower. The Fed sets the rates arbitrarily in its misguided effort to fight inflation. Accepting deposits into Treasury Security accounts does not affect interest rates.

( Raising interest rates to fight inflation is misguided because it raises business costs, thus raising prices.)

“This just adds to the problem future policymakers are going to face,” said Brendan Duke, a former Biden administration aide now at the Center on Budget and Policy Priorities, a liberal think tank.

Duke said that with the tax cuts in the bill set to expire in 2028, lawmakers would be “dealing with Social Security, Medicare and expiring tax cuts at the same time.”

It’s quite easy for an informed economist to solve the “problems” of Social Security, Medicare, and tax cuts. Just create the needed dollars by pressing computer keys.

The government would need $10 trillion of deficit reduction over the next 10 years just to stabilize the debt, Tedeschi said. Even though the White House says the tax cuts would add to growth, most of the cost goes to preserve existing tax breaks, so that’s unlikely to boost the economy meaningfully.

“It’s treading water,” he said.

If the government wanted to stabilize the misnamed “debt,” it has plenty of simple options.

Simply refuse to accept any more deposits into T-security accounts. The government neither needs nor uses the dollars. They just sit there, safely earning interest.

Enact legislation to add $10 trillion to the General Account, which is the account used for federal payments.

Have the Treasury mint a $10 trillion coin, as it has the legal authority to do so, and deposit the coin with either the Federal Reserve or the General Account.

If It’s So Simple, Why Don’t They Do It?

Here’s why so many smart people can’t seem to solve a simple problem: They don’t want to.

America is run by the very wealthy. What does “wealthy” mean?

“Wealthy” does not mean having a thousand, a million, a billion, or a trillion dollars. “Wealthy” means having substantially more wealth than 95% or 99% (pick your percentage) of the country.

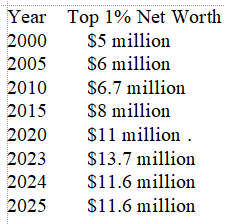

Look at this table of the amount of wealth required to be in the top 1% of Americans:

In the year 2000, having $5 million would have put you in the upper 1%, but only 2o years later, you would have needed to more than double your wealth to be as wealthy.

So, to remain wealthy, you had two options.

Dramatically increase the amount of money you have, and/or

Make sure those below you don’t increase their wealth

If it is difficult to double your money in twenty-five years, consider ensuring that those beneath you do not increase their wealth. This way, your top 1% ranking would remain secure.

How do you prevent them from rising? By convincing them with the false notion that the government cannot afford to provide benefits.

Make them pay for their own healthcare. Keep Social Security benefits low. Don’t help them financially with college, so they either pay the tuition or are forced to work lower-paying jobs.

Consider the FICA tax. You might think you pay half, but in reality, you pay the full amount. Your employer takes FICA into account when determining salaries. FICA represents a significant percentage of your income.

For the wealthy, FICA taxes are insignificant or nonexistent. Why is this the case? To ensure that the Gap between you and the top 1 percent does not narrow.

You hear the government claim that it “can’t afford” Medicare for everyone, Social Security for everyone, or college for anyone who wants to attend. They say this is because the federal debt (which isn’t truly federal and isn’t really debt) is too large, and that deficits need to be reduced. Meanwhile, tax loopholes for the wealthy are being widened.

And government spending causes inflation, so any increase in spending must be paid for by your taxes.

And it’s all a lie, a Big Lie, for federal tax dollars are not used to fund federal spending.

That’s what the rich want you to believe. It’s how they stay rich. Or get even richer.

IN SUMMARY

Unlike state and local governments, the federal government is Monetarily Sovereign. It has infinite money.

It does not borrow the currency it originally created and continues to create by passing laws.

“Federal debt” is neither federal nor debt. It is deposits in T-security accounts, wholly owned by depositors and never used by the government. The purpose is to provide a safe place to store unused dollars. This stabilizes the dollar.

Federal deficits are necessary for economic growth.

Federal spending does not cause inflation; it results from shortages of essential goods and services. Federal spending can alleviate inflation by acquiring these scarce assets.

The Big Liein economics is that the federal financing is like personal financing. The federal government needs no income. It creates all its income.

The Big Lie aims to benefit the wealthy by increasing the income, wealth, and power Gap between the rich and the rest.