I’ve been traveling lately. Just returned from Put-in-Bay Island and Cleveland (Cleveland???) and found that in the interim, nothing changed.

MAGAs still ignorantly agree with a dangerous, stupid, amoral, Hitlerian leader, along with his dangerous. stupid, amoral Nazi appointees.

To demonstrate their fealty, MAGAs still spend their precious dollars on worthless air sold by dear leader, while decrying federal dollars for the poor. The GOP still favors free speech, so long as the dear leader approves.

SCOTUS and Congress still are hopelessly corrupt. The economy remains the “greatest of all time” as it begins its swirl down the stagflation toilet.

The hero of the day is a dead bigot. America still is hated, only more so, and fewer people wish to live here. Goodbye to the “shining city upon a hill” myth.

The only “real” Americans still are straight, white, male CINOs (Christians in Name Only), who demonstrate their faith in Jesus by doing exactly the opposite of everything Jesus preached, not the least of which is continuing to express hatred of Jesus’s own religion.

Thousands of our most honest, hardest-working, tax-paying, valuable consumers are being deported by Nazi masked brownshirts in favor of useless, rich slugs who can afford to buy their way into the country for the purpose of plunder.

People still “wonder” whether dear leader, who has been convicted of, and admitted to, attacking dozens of women, miraculously found the moral and legal restraint not to abuse his friend Epstein’s young girls — as though that were the greatest of his sins.

And I still am old – er.

Thus, since I have been doing this for well over twenty years and have effected precisely zero change, my motivations, as well as my strength, have declined.

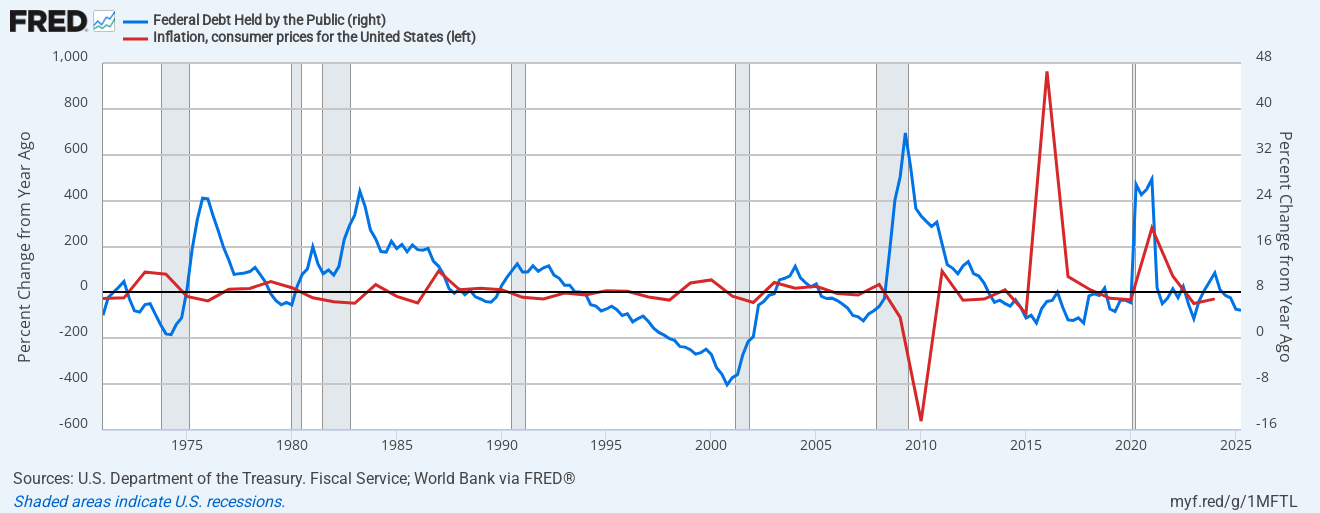

Hey, even my MMT pals still believe that a Jobs Guarantee would be a viable solution to unemployment, and federal deficit spending causes inflation.

So, what the hell?

Lately, I’ve speculated that what we term quantum “weirdness” is absolutely necessary for the existence of the universe (and thus, not weird at all), and that locality is a figment of our limited imagination. I’ll ask my AI friends about that.

Until America comes to its senses — or doesn’t — to tide you over, I’ll offer a few predictions you can mull about:

- Our dear leader will continue his march toward Hitlerism, aided and abetted by a corrupt and weak Congress and an even more corrupt Supreme Court.

- We will enter a deep recession, which will be blamed on Democrats, immigrants, the poor, Jews, and liberals, in no particular order.

- In response to the recession, the government will institute austerity measures, which will cause a depression.

- The following programs will be cut because they are “unaffordable,” (meaning they benefit those who are not rich): Social Security, Medicare, Medicaid, Supplemental Security Income, Supplemental Nutrition Assistance Program (SNAP, “food stamps”), Temporary Assistance for Needy Families (TANF), Children’s Health Insurance Program (CHIP), Unemployment Insurance (UI), Earned Income Tax Credit (EITC), Child Tax Credit (CTC), Section 8 Housing Assistance (Housing Choice Voucher Program), Special Supplemental Nutrition Program for Women, Infants, and Children (WIC), School Lunch and Breakfast Programs, Head Start / Early Head Start, Pell Grants, Veterans Benefits, Federal Employee Retirement / Disability Programs.

- Food-borne diseases will become more common as more inspectors will be fired.

- All federal government services will be reduced.

- The military will take over more cities.

- Airplane accidents will increase.

- Our dear leader will introduce more programs to enrich himself and his family. MAGAs will continue to invest in those programs and lose their money, learning nothing from the experience.

- Tax dodges for the rich will be expanded.

- Books that mention sex, bigotry, slavery, gays, mistaken executions, glass ceilings, religious quotas, or anything that reveals any flaws in America will be burned to “protect our children.”

- Criticism of the government or politicians will be subject to punishment. (Harvard, take note.)

- It will be determined that the Constitution really doesn’t provide for a two-term Presidential limit, and even if it does, dear leader will avoid it by running as a VP, then “allowing” the President to resign.

- The Second Amendment again will be reinterpreted, this time to mean that anyone, regardless of age, mental capacity, or criminal history, can carry and use any kind of weapon at any time and in any place for any purpose.

- SCOTUS will decide that past, current or future Presidents will be immune to all legal claims, civil or criminal.

- SCOTUS will decide that any form of gerrymandering or voting restriction is legal.

- Millions of Americans will be unvaccinated, and so will sicken or die of polio, measles, mumps, rubella, chickenpox, diphtheria, tetanus, whooping cough, hepatitis A, hepatitis B, pneumococcal disease. meningococcal disease, rotavirus, influenza, COVID-19, human papillomavirus, shingles, pertussis, and RSV.

- Anyone, whether criminal or not, will be able to purchase and sell an immediate American citizenship for $1 million or two for $1.5 million.

Be well. Be safe. Be smart. Vote if they let you.

Rodger Malcolm Mitchell

Twitter: @rodgermitchell

Search #monetarysovereignty

Facebook: Rodger Malcolm Mitchell;

MUCK RACK: https://muckrack.com/rodger-malcolm-mitchell;

……………………………………………………………………..

A Government’s Sole Purpose is to Improve and Protect The People’s Lives.

MONETARY SOVEREIGNTY